HNW - HNW: This 10% Yielding CEF Gets A Downgrade

2023-12-20 22:08:11 ET

Summary

- The Pioneer Diversified High Income Fund is a fixed income CEF with a unique mix of asset classes with low correlations to each other.

- The vehicle's low volatility is attributed to its holdings of catastrophe bonds, which are not affected by traditional economic conditions.

- The fund's discount to NAV has narrowed, but US high yield spreads are now too low, leading to a downgrade in rating.

- The CEF has now delivered a total return exceeding 10% since our buy rating, but the current pricing is no longer attractive as an entry point.

Thesis

The Pioneer Diversified High Income Fund ( HNW ) falls in the fixed income CEF asset class. We have covered this name before here when we put a buy rating next to the fund stating the following:

The fund has a 30-day SEC yield in excess of 10%, which is 96% supported via net investment income cash. We like this fund because it is trading at close to historic discount levels (currently -14%) and its holdings composition (ILS asset class has a low correlation to the other sleeves).

All the elements from our thesis came to fruition, with the vehicle exhibiting low volatility during the recent market swoon, and the fund now having delivered a total return in excess of 10% from its discount narrowing and NAV moving up all while clipping a high dividend:

Performance (Seeking Alpha)

With the CEF's discount now back to its average cycle level and high yield currently on the pricey side, we no longer feel the current price represents a good entry point to warrant a buy rating. We are therefore moving to hold on to the name, having this CEF in our portfolio and clipping the dividends.

Volatility has been low

One item that was mentioned before and still persists for this CEF is its low volatility:

If we look at the CEF in the past three months, and benchmark it against the unleveraged SPDR Bloomberg High Yield Bond ETF ( JNK ) and the PIMCO Dynamic Income Fund ( PDI ), we will notice that HNW has a volatility profile very much akin to the unleveraged JNK. All else equal, a retail investor should prefer low-volatility instruments.

The CEF's low volatility is explained by its holdings which include a large sleeve of catastrophe bonds. Catastrophe bonds are debentures that only move when there is a natural event that could affect their pay-off profile:

A catastrophe bond ('CAT') is a high-yield debt instrument that is designed to raise money for companies in the insurance industry in the event of a natural disaster. A CAT bond allows the issuer to receive funding from the bond only if specific conditions, such as an earthquake or tornado, occur. If an event protected by the bond activates a payout to the insurance company, the obligation to pay interest and repay the principal is either deferred or completely forgiven.

Cat bonds therefore do not exhibit the usual widening of credit spreads during risk-off events, because the state of the economy does not affect the probability of a hurricane developing in Florida. Sometimes during true financial crises, one can see a slight move lower in prices due to forced selling. The great financial crisis of '08-'09 is famous for seeing cat bonds being sold because they were the only assets in some managers' portfolios that were still priced close to par.

Collateral profile

The fund counts US high yield as its top sector:

Sectors (Fund Fact Sheet)

The catastrophe bond sleeve we discussed above represents the second largest exposure at 20.3% of the collateral pool (called 'Event-linked Bonds' in the fact sheet). The fund has a very nice multi-asset mix which allows for a low vol build.

Given its holdings profile, it is not a surprise the majority of the holdings are below investment grade:

Ratings (Fund Fact Sheet)

The large 'Not Rated' bucket pertains to catastrophe bonds and some of the MBS holdings. 'Not Rated' should not be translated as toxic collateral, since many issuances chose not to pay the rating agencies since their distribution to institutional investors is well established and risks are well understood. Occasionally there are also private ratings in place which cost less and are available only to the institutional investor paying for said service.

Discount to NAV has now narrowed

An important structural feature of CEFs is represented by the discount to NAV, or the discrepancy between the net asset value for the fund and its market price:

When we wrote our first piece this year the fund was close to its historic highs in its discount to NAV. The CEF has now gained 4% from the narrowing, and is closing in on its average cycle mark of -10% discount. We can see from the CEF's performance in the past decade that it usually trades in the -8% to -10% band during normalized economic environments. During the zero rates period from 2020 to 2021 the CEF moved to being flat to NAV, but we do not anticipate that to repeat anytime soon.

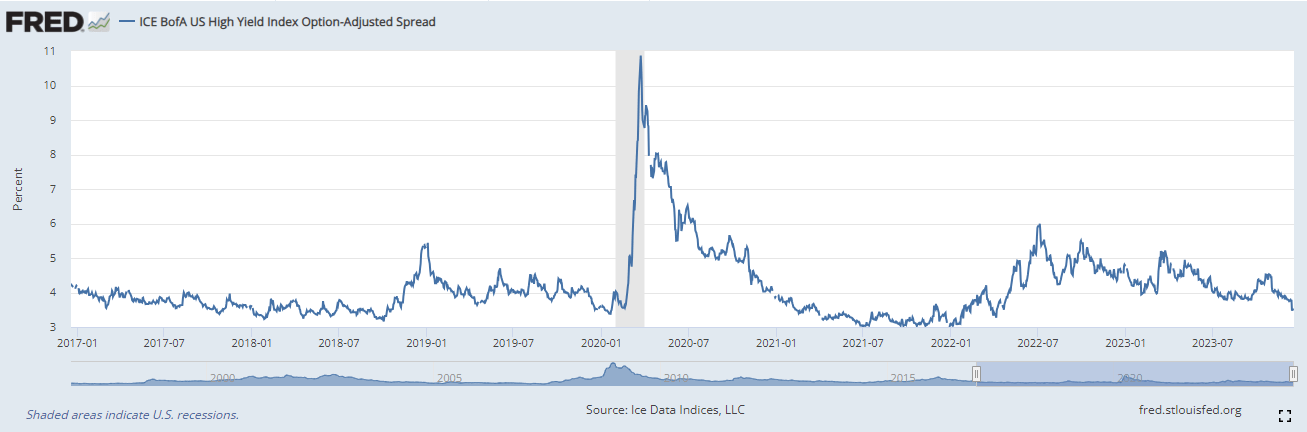

US high-yield spreads are now too low

One of the main reasons for the downgrade is the performance of US high yield spreads:

{kind=link}

Spreads measured by the ICE BofA US High Yield Index are at 351 bps, comparable with levels seen during the summer of 2021 when rates were close to zero. If we have a cursory look through the above graph, we can see that during the past five years, during normal times, spreads usually are above 4% but below 5%. During times of economic expansion and bull markets, they move lower to below 4%, while risk-off moves see them go above 5%. In essence, the signal to be derived is that above 5% makes spreads cheap, while below 4% they are pricey. Unless an investor thinks we are completely out of the woods in terms of all relevant economic indicators, then we should see a reversion to spreads above 4%, similar to what occurred in October.

In essence, a prudent investor should not buy spreads here unless they are 110% convinced there is no storm on the horizon and we have just entered another cyclical bull market. We are of a different opinion, thinking the market is in overbought territory currently and we will see another consolidation / risk-off move.

Conclusion

HNW is a fixed income CEF. The fund has a multi-asset composition, with large US HY and catastrophe bond buckets. The fund has been a nice low vol addition to a portfolio, with a 10% total return since our buy rating in August. With the CEF's discount to NAV now narrowing to its historic average and high yield becoming expensive when spreads are considered, we are of the opinion that the CEF's price does not represent an attractive entry point anymore. We hold this name clipping the dividends, and are moving the fund to a Hold rating.

For further details see:

HNW: This 10% Yielding CEF Gets A Downgrade