HCHDF - Hochschild Mining: A Strong Q4 But Permitting Uncertainty Remains

2023-04-24 00:41:21 ET

Summary

- Hochschild Mining was one of the worst-performing precious metals stocks last year, declining 52% vs. a 15% decline in the Gold Juniors Index.

- The significant underperformance can be attributed to continued uncertainty related to the Inmaculada MEIA, a dwindling reserve life at San Jose/Pallancata, and another year of margin compression.

- The good news is that Mara Rosa continues to progress on schedule and will help to pick up some of the slack once Pallancata heads into care & maintenance.

- That said, while Hochschild remains reasonably valued at a ~$720 million enterprise value, I continue to see far more attractive bets elsewhere in the sector.

2022 was a difficult year for the Silver Miners Index ( SIL ), with inflationary pressures impacting costs, supply chain headwinds and COVID-19 related restrictions impacting some operations, and little help from the silver price which declined year-over-year to average just $22.00/oz. This sharp increase in costs made it more difficult for some companies to replace reserves given that the hurdle was higher for moving ounces into the reserve categories with rising cut-off grades at several assets. In Hochschild Mining's ( OTCQX:HCHDF ) case, it saw a sharp decline in reserves at its silver assets like Fortuna Silver ( FSM ), and its FY2022 results left much to be desired with a miss on output guidance. Let's take a look at its FY2022 results and 2023 outlook:

All figures are in United States Dollars unless otherwise noted.

FY2022 Results

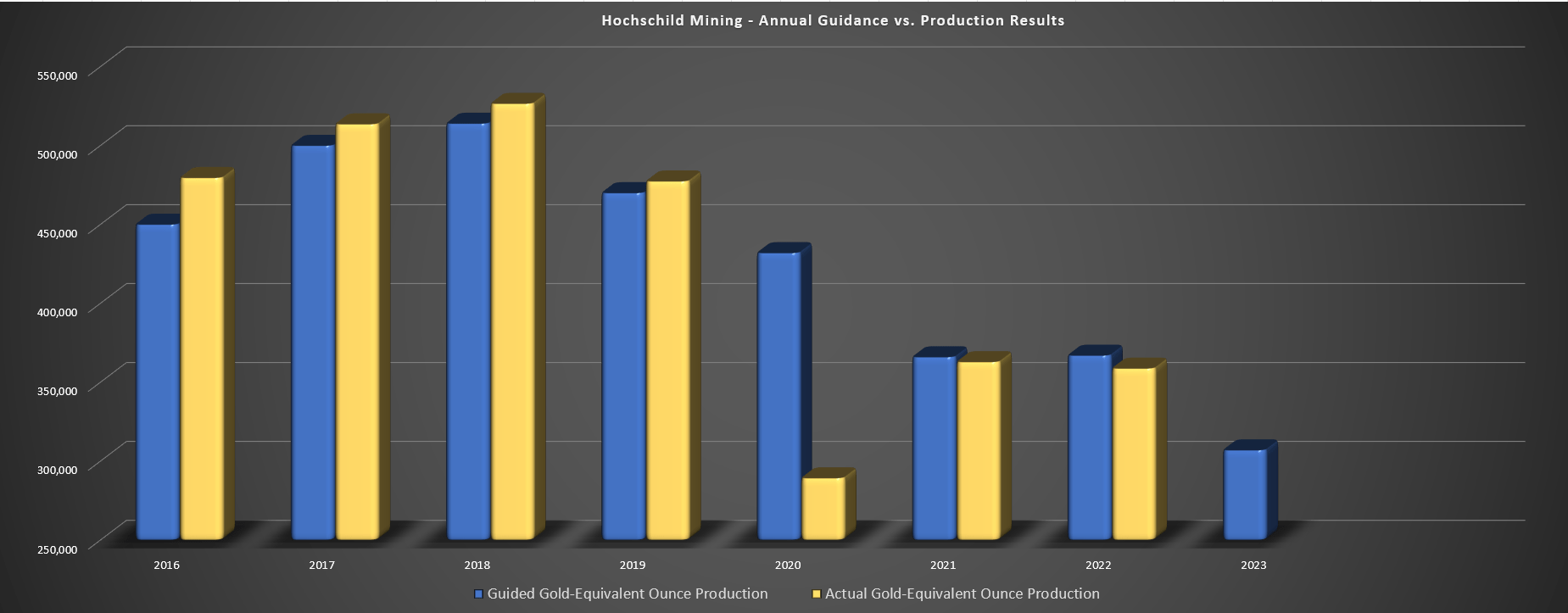

Hochschild Mining released its FY2022 results last week, reporting Q4 production of ~97,700 gold-equivalent ounces [GEOs], a 3% increase from the year-ago period. Unfortunately, the strong finish to the year could not make up for a soft start to 2022 at San Jose and the significantly lower grade profile at Pallancata, resulting in Hochschild's annual production declining to just ~358,800 GEOs (FY2021: ~362,900 GEOs). This translated to a miss vs. its guidance midpoint of ~367,000 GEOs, and it marked the third consecutive annual miss relative to its guidance midpoint. Worse, we saw another year of material cost increases, impacted by inflationary pressures felt sector-wide, with all-in sustaining costs increasing to $1,364/oz (+18% year-over-year) or $1,473/oz when including brownfield exploration, royalties/special mining taxes, and administrative expenses.

{kind=link}

Hochschild Mining - Annual Guidance Midpoint vs. Actual Production Results (Company Filings, Author's Chart)

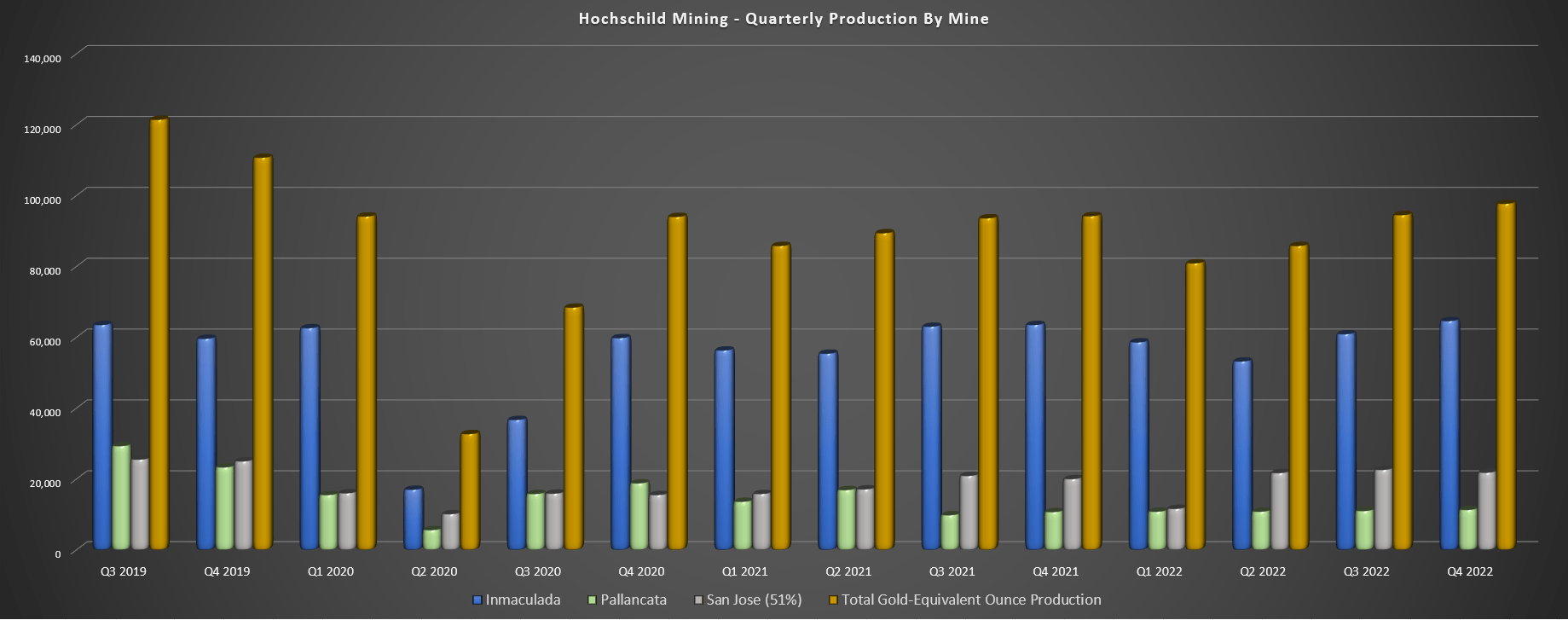

Digging into the production results a little closer, we can see that Q4 was the best quarter of the year, with attributable production of ~97,700 GEOs. The increase in output was helped by increased throughput at San Jose but offset by a softer quarter at Pallancata and Inmaculada. At Pallancata, grades were down sharply to 139 grams per tonne of silver and 0.68 grams per tonne of gold (Q4 2021: 177 grams per tonne of silver and 0.85 grams per tonne of gold). And at Inmaculada, grades came in at similar levels, but quarterly throughput was lower because of protests, which has also negatively impacted production at the Las Bambas Mine in Peru. And while there was little impact on operations for Hochschild's Inmaculada, unlike Las Bambas which continues to see issues, throughput was a little lower than planned in the period.

{kind=link}

Hochschild Mining - Quarterly Production by Mine (Company Filings, Author's Chart)

On a full-year basis, Inmaculada's production was down over 5% year-over-year due to lower throughput and grades, but the flagship asset still had a solid year with ~237,200 GEOs produced at all-in sustaining costs of $1,058/oz. Unfortunately, Pallancata didn't fare nearly as well, with annual output 25% to ~43,900 GEOs at all-in sustaining costs of $2,336/oz ($32.40/oz silver-equivalent), well above Hochschild's average realized prices of $1,791/oz for gold and $23.30/oz for silver. Meanwhile, the 51% owned San Jose Mine saw slightly lower production at ~152,300 GEOs (100% basis), but AISC also rose to $1,561/oz from $1,435/oz in the year-ago period. This resulted in AISC margins shrinking to $427/oz on a consolidated basis, down from $540/oz in FY2022, which is before administrative expenses, brownfields exploration, and royalties/special mining tax.

{kind=link}

Hochschild - Annual AISC - GEO Basis (Company Filings, Author's Chart)

Finally, looking at the financial results, annual revenue fell 10% year-over-year to $735.6 million, operating costs soared to $158.70/tonne vs. $133.50/tonne, and cash flow from operations fell over 60% to $102.9 million (FY2021: $282.5 million). Combined with increased spending at Snip (which Hochschild has since terminated its option) and capex to move its Mara Rosa Project forward in Brazil, Hochschild ended the year with just $144 million in cash and $175 million in net debt, down from $387 million and net cash of $86 million at year-end 2021. This has made Hochschild one of the more leveraged miners sector-wide and much more leveraged if it can't secure permits for Inmaculada, which would cause the operation to move into care & maintenance at year-end 2023.

2023 Outlook & Recent Developments

As for the 2023 outlook, there's not much to write home about, and any positive developments have been largely overshadowed by the delay in receiving Inmaculada's Modified Environment Impact Assessment [MEIA]. Starting with the 2023 outlook, Hochschild has another high-cost year ahead with ~$130 million in capex and expects to produce 301,000 to 314,000 ounces at all-in sustaining costs of $1,370/oz to $1,450/oz. This would translate to even higher costs year-over-year with a 12% decline in annual production even if it meets the top end of guidance. When we compare to declining cost profiles for some other companies like Alamos Gold ( AGI ), Newcrest ( OTCPK:NCMGF ) and others, this setup isn't ideal.

The silver lining is that the Mara Rosa Project is ~70% complete with detailed engineering nearly completed and this will be a transformative asset for Hochschild Mining even if it is smaller scale (~100,000 ounces for the first four years). This is because all-in sustaining costs should be well below $1,000/oz, over 40% below Hochschild's current cost profile based on FY2023 guidance. That said, San Jose continues to see dwindling reserves with barely two years of mine life based on reserves (~1.0 million tonnes of reserves vs. average annual throughput of ~500,000 tonnes) and without the MEIA at Inmaculada, it's not clear what this asset's production profile will look like post-2023. Finally, Pallancata is likely to move into care & maintenance by year-end.

{kind=link}

Mara Rosa Project Construction (Company Website)

This combination of a short mine life at San Jose based on reserves, uncertainty at Inmaculada, and Pallancata set to head into temporary care and maintenance means that Mara Rosa may offer margin expansion, but it's not offering growth. In fact, the ~100,000 ounce increase in production from Mara Rosa will be offset by ~40,000 GEOs at Pallancata and could be offset by a further 70,000 GEOs per annum from San Jose if the company can't replace reserves. Finally, on the off chance that Inmaculada doesn't receive its MEIA permit, Hochschild could be a two-mine company in 2024 (San Jose, Mara Rosa) even after adding a new gold operation in Brazil, down from a three-mine company this year.

Hochschild's management appears confident that they will receive the MEIA in Q2 2023, but this is well past the previous timeline of H2-2022 in which they also appeared confident, so it's hard to be overly optimistic regarding timelines. And while Inmaculada will operate until year-end, even without a favorable ruling, this would be a devastating blow to move this asset into care and maintenance given that it's a cash cow with San Jose barely profitable on an all-in cost basis. So, while the recent exploration success outside of the Pallancata permitted mining area is positive (potential to restart operation in 2027) and Mara Rosa is a solid asset that helps to diversify Hochschild, a lot is riding on the Inmaculada MEIA and the timely receipt of permits will be critical for the company.

Valuation & Technical Picture

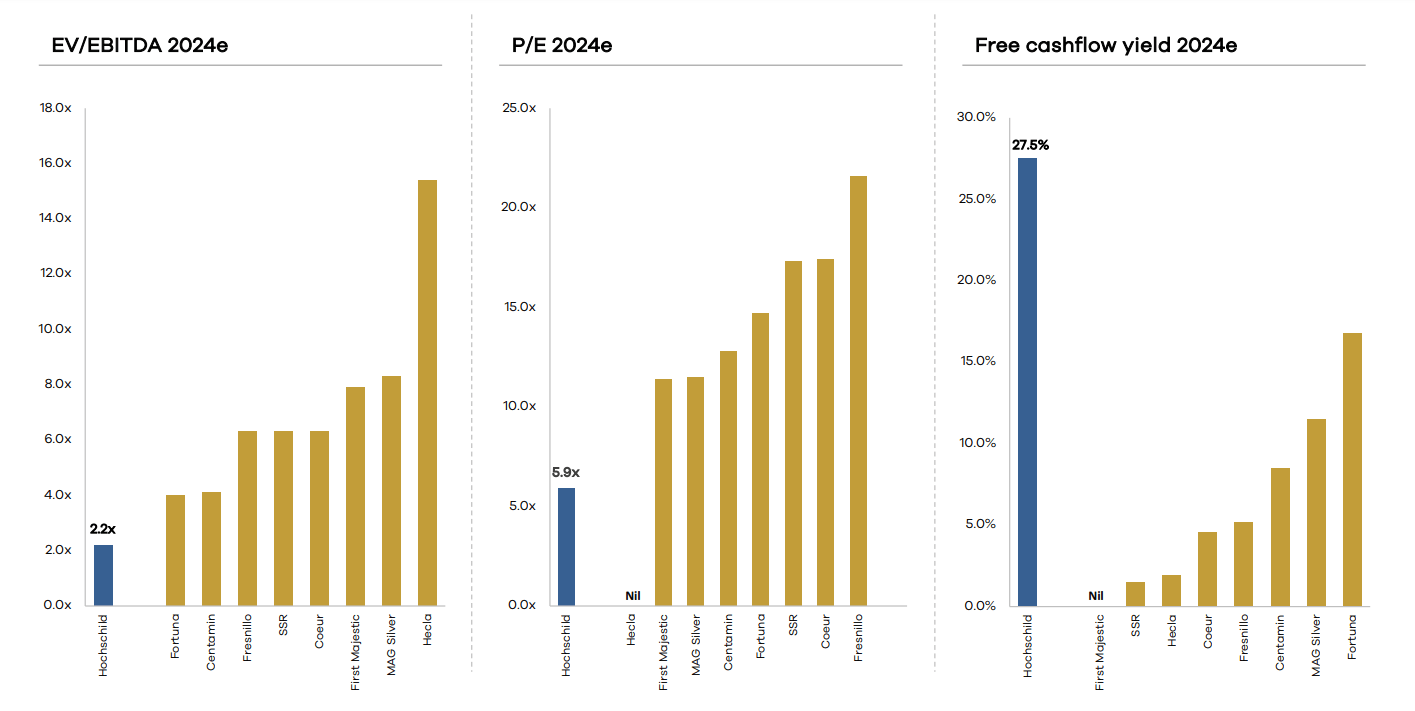

Based on ~514 million shares and a share price of US$1.06, Hochschild Mining trades at a market cap of ~$545 million and an enterprise value of US$720 million. This leaves the stock at a very reasonable valuation given that it could be a 400,000+ ounce per annum producer (gold-equivalent basis) in 2025 if the company receives its MEIA, leaving it trading at just $1,800/oz on an EV/production basis. That said, this continues to be a less favorable story when one digs into the details, with its flagship asset requiring the timely receipt of its MEIA, its #2 asset having a relatively small reserve base, and its #3 asset set to be placed in care and maintenance by year-end with no guarantees it will be restarted before 2027. Plus, Hochschild operates in Tier-2 jurisdictions (Argentina, Peru) with costs well above the industry average.

{kind=link}

Hochschild Mining Valuation Relative to Peers (Company Presentation)

Given the continued uncertainty, the lack of Tier-1 jurisdictional exposure, its higher leverage relative to peers and a short mine life, I believe much of its discount relative to peers is justified. This is especially true given that an inability to secure the Inmaculada MEIA in a timely manner would cause its FY2024 free cash flow yield to plunge with the company relying on production from a single gold operation in Brazil for a partial year (Mara Rosa) and a high-cost 51% owned operation in San Jose. Hence, a bet on Hochschild Mining is a bet on the Inmaculada permit being received this year. And although management sees a high probability of securing its MEIA in Q2-2023 (adjusted from H2-2022 previously), it's typically safer to take the over on permit grants/renewals.

Using what I believe to be a fair value of 1.10x P/NAV to reflect its silver exposure (which should command a premium) offset by its less favorable jurisdictional profile and an estimated net asset value of $520 million, I see a fair value for Hochschild Mining of ~$600 million. If we divide this figure by ~514 million shares, Hochschild's conservative fair value estimate comes in at US$1.17. Although this points to 11% upside from current levels, I am looking for a minimum 40% discount to fair value for small-cap producers, and especially those in less favorable jurisdictions.

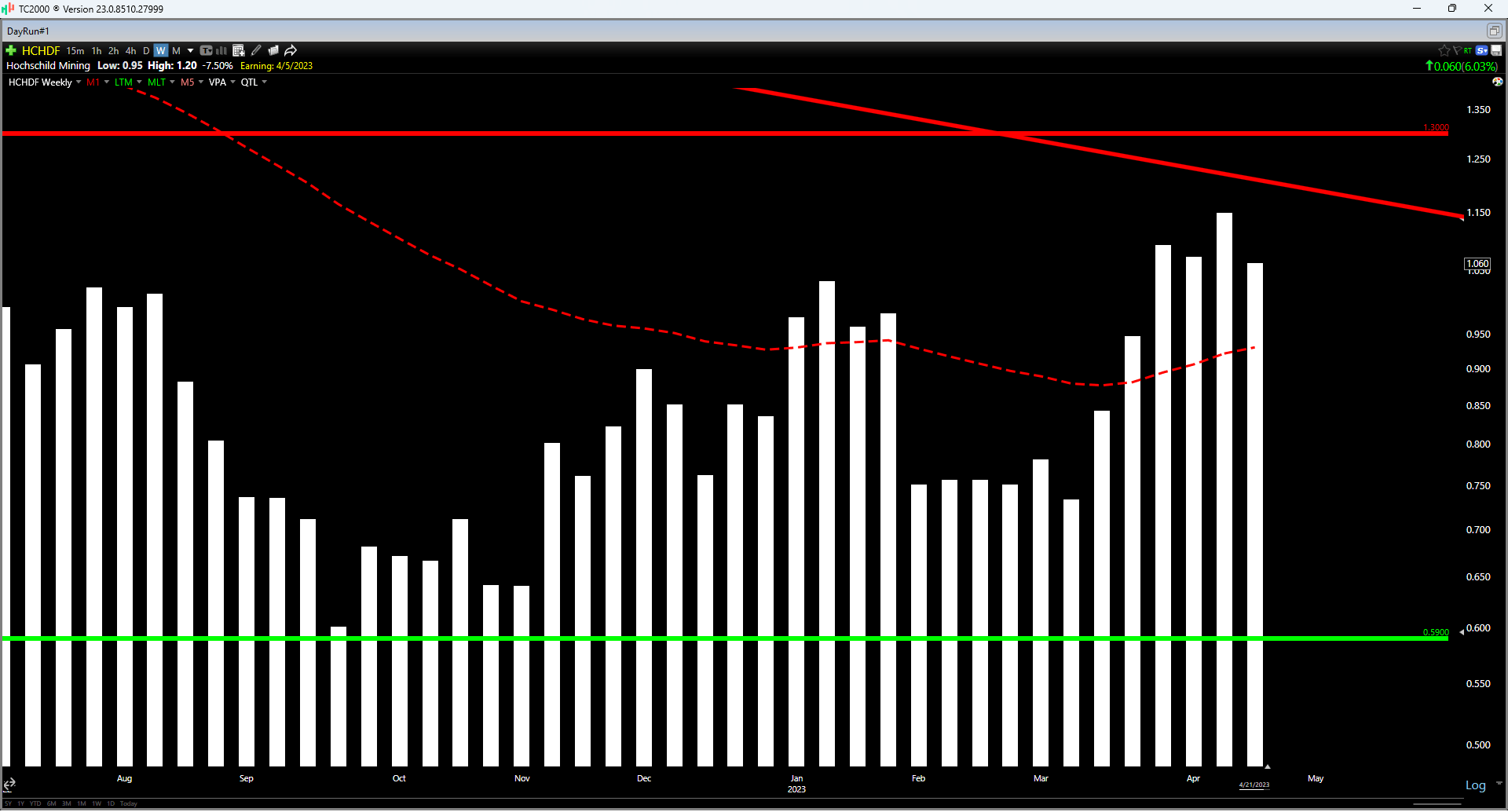

{kind=link}

HCHDF Weekly Chart (TC2000.com)

Finally, looking at the technical picture, Hochschild has rallied towards its multi-year downtrend line and has resistance in the US$1.18 - US$1.30 region. Meanwhile, it has no strong support zone until US$0.59. This corroborates the view that Hochschild is not in a low-risk buy zone currently at US$1.06, with a current reward/risk ratio of 0.21 to 1.0 from support to resistance. Therefore, Hochschild Mining is nowhere near a low-risk buy zone today in my view and would need to decline below US$0.70 to bake in an adequate margin of safety, suggesting that there are far more attractive ways to allocate one's capital in the sector.

Summary

Although the recent increase in metals prices is a positive for the sector and a rising tide will lift all boats, Hochschild Mining continues to be one of the riskier names sector-wide given the drawn out permitting process for the MEIA at its flagship asset. It's possible that this is resolved by summer, which could prompt a sharp rally in Hochschild's stock. However, I don't see enough margin of safety if the ruling is not favorable, and I prefer simpler stories that don't have considerable uncertainty tied to a key asset. So, on a risk-adjusted basis, I continue to see far more attractive bets elsewhere in the sector. One of the more attractive opportunities out there looks to be i-80 Gold ( IAUX ) which trades at a significant discount to net asset value in a more favorable jurisdiction with considerable exploration success across its portfolio.

For further details see:

Hochschild Mining: A Strong Q4 But Permitting Uncertainty Remains