HCHDF - Hochschild Mining: Posse Progress Overshadowed By Continued Uncertainty

Summary

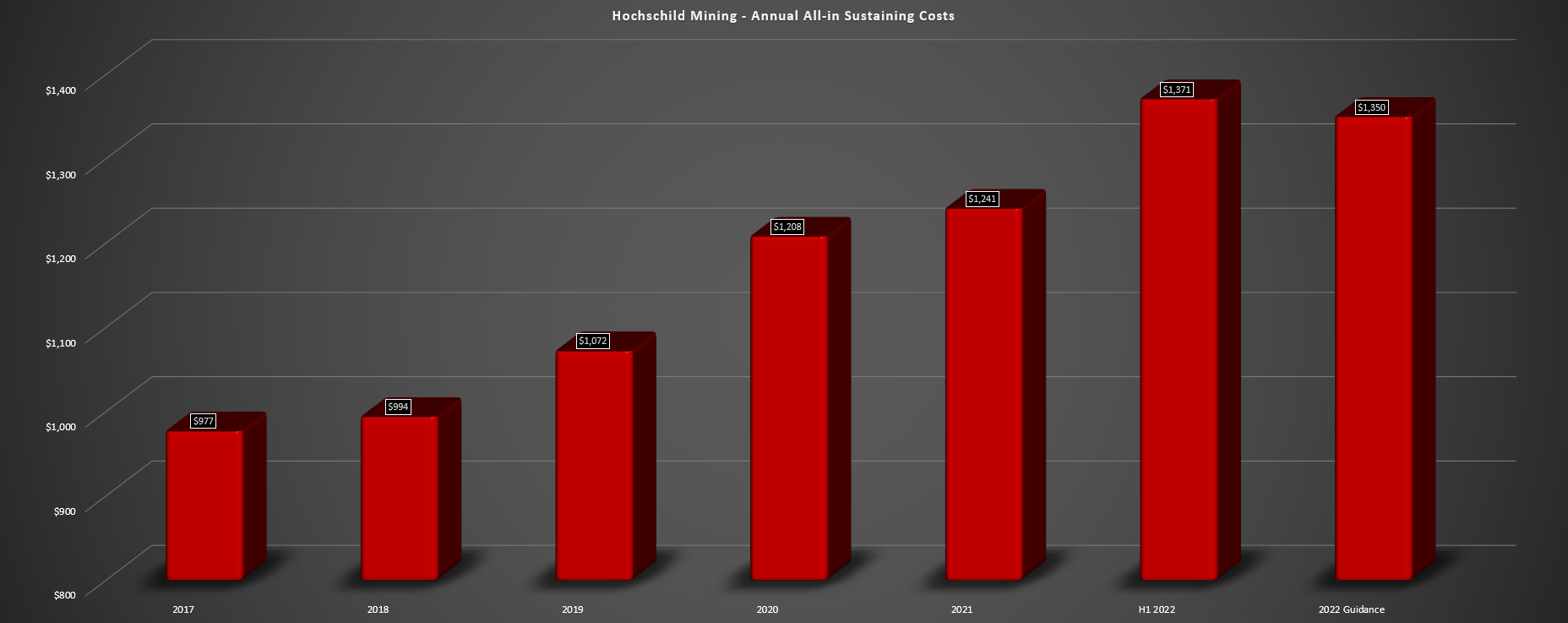

- Hochschild Mining released its Q3 results in November and is on track to meet its FY2022 guidance but at costs well above the industry average ($1,350/oz AISC midpoint).

- Meanwhile, the company appears to be on track for another year of declining production, and I wouldn't expect 2023 to be much better with mining activities nearing completion at Pallancata.

- Fortunately, Posse will provide a nice boost to production beginning in 2025, but this is partially overshadowed by permit delays at Inmaculada and the potential cessation of mining at Pallancata.

- Given Hochschild's mediocre portfolio with a lot of eggs in South America, sharply rising costs at San Jose, and a relatively short mine life at its #2 and #3 assets, I continue to see HCHDF as an inferior way to play the sector.

Hochschild Mining ( OTCQX:HCHDF ) had a rough year and seen considerable underperformance, declining ~75% from its 2020 highs and massively underperforming its peers in the Silver Miners Index ( SIL ). This can be attributed to declining production at higher costs, and the relatively short mine lives (Pallancata, San Jose) have created uncertainty around the future for these assets. Adding insult to injury, Inmaculada continues to wait for an updated permit required to keep operating post-2023, and hyperinflation in Argentina is certainly not helping matters and also impacting other miners in the country.

Fortunately, the company's development-stage Posse Project is a bright spot that should pour its first gold by H2 2024, and the company put together a decent quarter in Q3. This has placed Hochschild in a position to deliver into its output guidance, and combined with improving sentiment sector-wide, the stock has rallied over 70% off its lows. However, with a portfolio that lacks diversification, two assets with short mine lives, and one that's relatively marginal, plus uncertainty at its major producing asset, I continue to see the Hochschild investment thesis as weak. Hence, if this rally persists and we rally towards US$1.20, I would view this as an opportunity to book profits.

{kind=link}

Hochschild Operations (Company Website)

Q3 Results

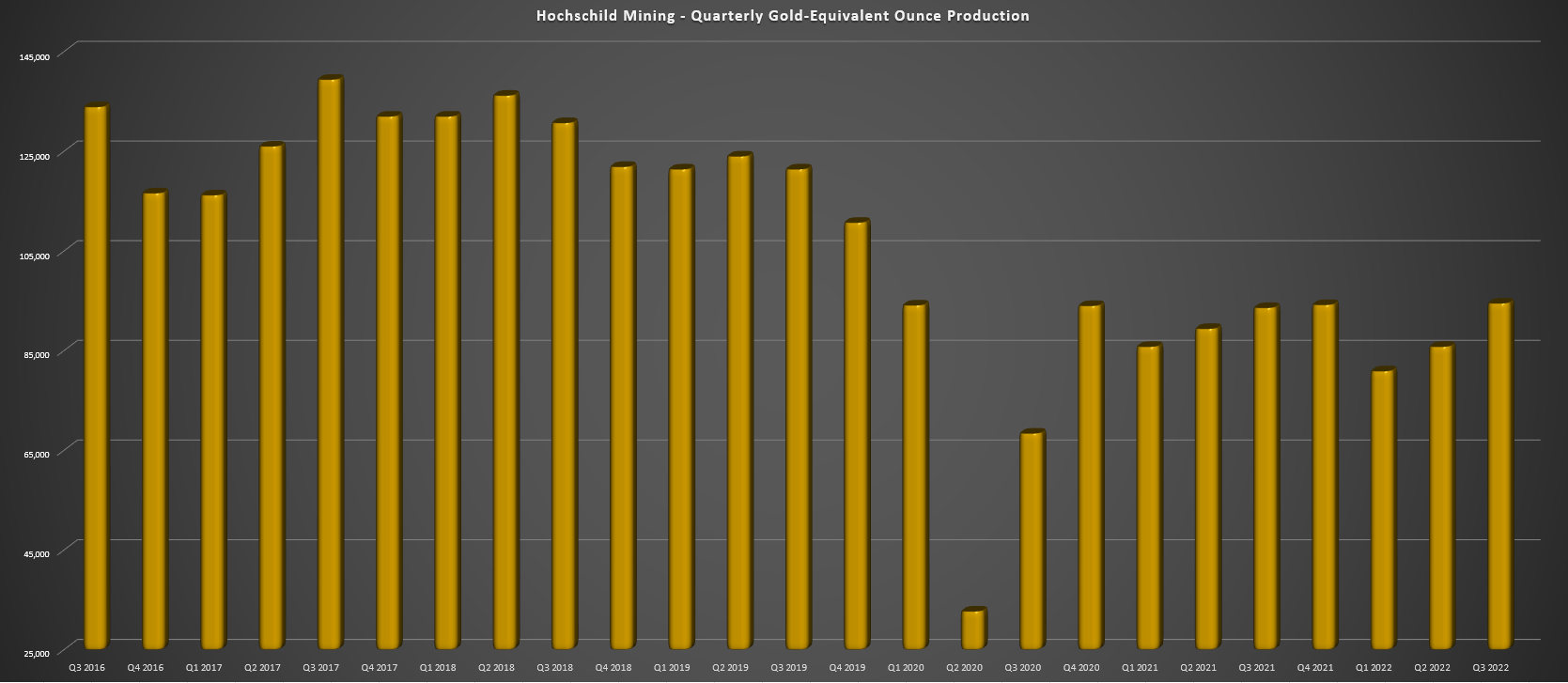

Hochschild Mining released its Q3 results in November, reporting quarterly production of ~52,700 ounces of gold and ~3.0 million ounces of silver, translating to ~94,500 gold-equivalent ounces [GEOs] in the period. This was a slight improvement from the year-ago period (~93,600 GEOs) and the best quarter year-to-date, helped by a solid quarter from its flagship operation, Inmaculada, and a better quarter at San Jose (51% interest). So, despite a slow start to the year, Hochschild is positioned to deliver into its FY2022 guidance of 360,000 to 375,000 GEOs but will need a 106,000+ ounce quarter to meet its mid-point.

{kind=link}

Hochschild Quarterly GEO Production (Company Filings, Author's Chart)

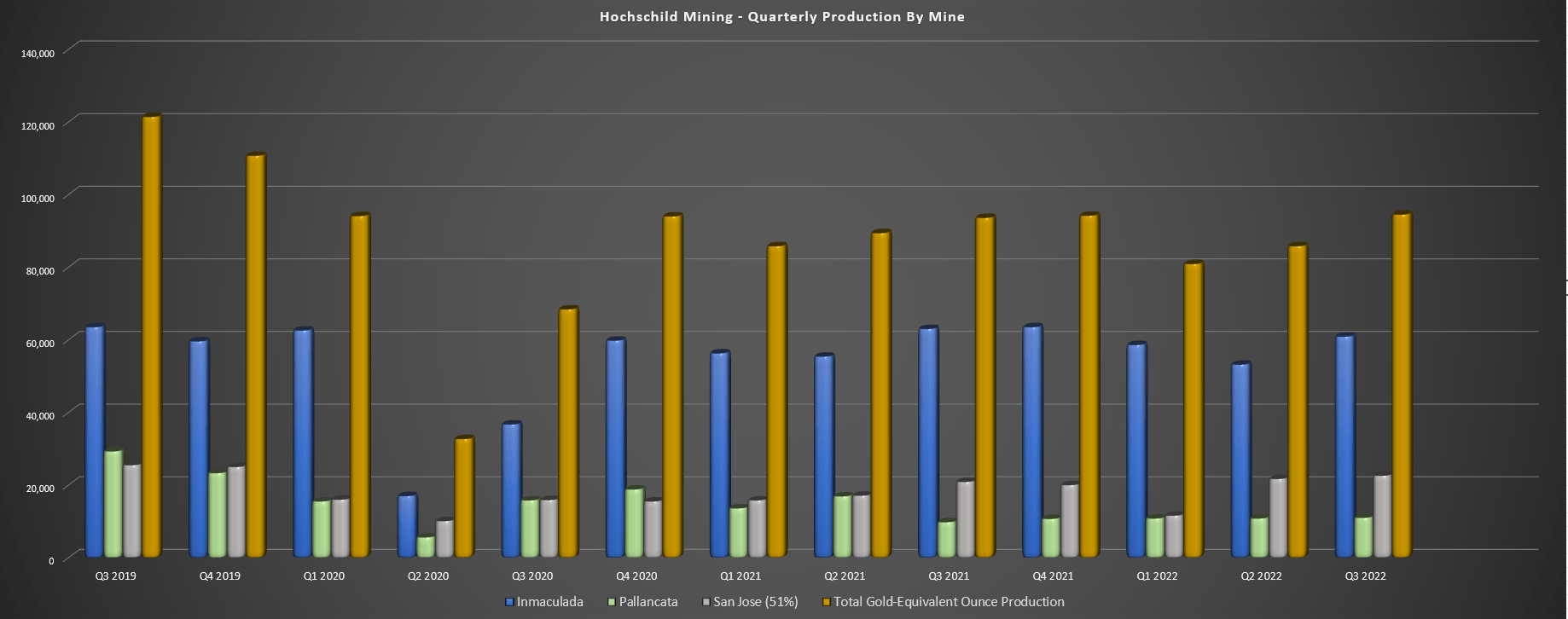

Digging into the results a little closer, its Inmaculada saw sharply lower grades in the period but mostly made up for this with increased throughput of ~348,100 tonnes. At Pallancata, the same was true from a grade standpoint, but ~30% higher throughput helped to pick up the slack, helping the mine to have another 10,000+ GEO quarter. Finally, at San Jose, production improved meaningfully to ~44,300 GEOs (22,600 GEOs attributable), but lower gold grades partially offset better-than-planned silver grades. Finally, at Mara Rosa in Brazil (Posse Gold Project), the company noted that total project progress is 16% complete, with detailed engineering 90% complete, keeping it on track for a mid-2024 gold pour.

{kind=link}

Hochschild - Quarterly Production by Mine (Company Filings, Author's Chart)

Given the expectations for another solid quarter in Q4 and the benefit of higher gold and silver prices, we should see a better-than-expected H2 for Hochschild from a financial standpoint vs. two months ago when it looked like silver might remain stuck under $20.00/oz. That said, Hochschild's costs continue to rise, eroding profitability, and there are a few negatives that might not be gleaned from the headline results that continue to weigh on the stock. These are not insignificant, and while the company is working towards progress on fixing these issues, it has somewhat muddied the investment thesis. Let's take a closer look below:

{kind=link}

Hochschild - Annual AISC (Company Filings, Author's Chart)

Recent Developments

Beginning with the company's flagship Inmaculada operation, the project has not had an easy year. For starters, the modified EIA to allow the mine to continue operating until 2041 was previously expected by H2 2022, which then turned into "before year-end" and has now been revised to Q1 2023. While I don't see any glaring reason that the company wouldn't receive its permit, the delays are not ideal given that this will be required for Inmaculada to continue mining post-2023, a similar position to the one that Fortuna Silver ( FSM ) was in which kept a lid on the stock. Recently, we got other negative news from the operation, with Peruvian demonstrators burning infrastructure as part of the protest, severely damaging non-critical installations.

While this appears to have been a temporary setback and scare for workers at the mine, this continues what's been a very difficult two years for the asset in terms of distractions. This includes the recent violence, a significantly delayed approval for its EIA, and the announcement that permit extensions would not be granted with an immediate backtrack of this statement but with the damage already done to Hochschild's share price. Fortunately, the asset has continued to operate during these issues, but with this being Hochschild's cash cow, the noise around the asset and uncertainty certainly doesn't help the investment thesis. Unfortunately, the major difference between Fortuna's San Jose and Hochschild's Inmaculada, which have both had a tough 18 months, is that San Jose represents less than 20% of NAV while Inmaculada represents over 60% of NAV, explaining the stock's underperformance.

The other negative development is that Pallancata's operations look to be winding down, given its short mine life. While the company made a new discovery (Royropata Zone) with an inferred resource planned this year, it is outside the permitted area. This means that even if this is advanced rapidly, it won't be able to supplement current production, given that permits will be required for this new mining area. Hence, even if a robust resource is delineated here that can keep the operation running, it looks like this is a post-2026 opportunity, meaning that Hochschild will see a dip in production as it likely places this asset in care & maintenance by year-end.

Outside of rising costs at its operations due to inflationary pressures, which aren't company-specific, the third negative is that San Jose is also looking like a somewhat marginal operation, and it doesn't have a long mine life either. This is evidenced by H1 2022 costs above $1,600/oz AISC at the Argentinian asset. Investors will be quick to point out that Posse is coming to the rescue with higher margins and a solid production profile, and this is a fair point. However, while a robust project, it doesn't help the company shed its solely South American jurisdictional focus, which appears to be heading more left quickly, and capex here is up substantially from estimates under Amarillo, with a hope that the project can be built for ~$200 million vs. $145 million previously. Let's see if the valuation has adequately priced in this less favorable outlook:

Valuation

Based on ~514 million shares and a share price of US$0.98, Hochschild trades at a market cap of $504 million and an enterprise value of ~$655 million. This leaves the company trading at a slight discount to an estimated net asset value of ~$550 million when adjusting for net debt and estimated future corporate G&A. While this P/NAV multiple of ~0.91 is a significant discount to other silver producers like First Majestic ( AG ), Hecla Mining ( HL ), and SilverCrest Metals ( SILV ) at 1.40x P/NAV or higher, I would argue that Hochschild should trade at a discount for several reasons. These are the following:

- uncertainty around its EIA at Inmaculada, which could impact cash flows if not granted by year-end (valid until the end of 2023)

- a short mine life at Pallancata, which looks like it will be placed into care & maintenance until at least 2026

- a lack of Tier-1 jurisdictional exposure with an entirely South American operating footprint and more than 60% of NAV at a single asset (Inmaculada)

{kind=link}

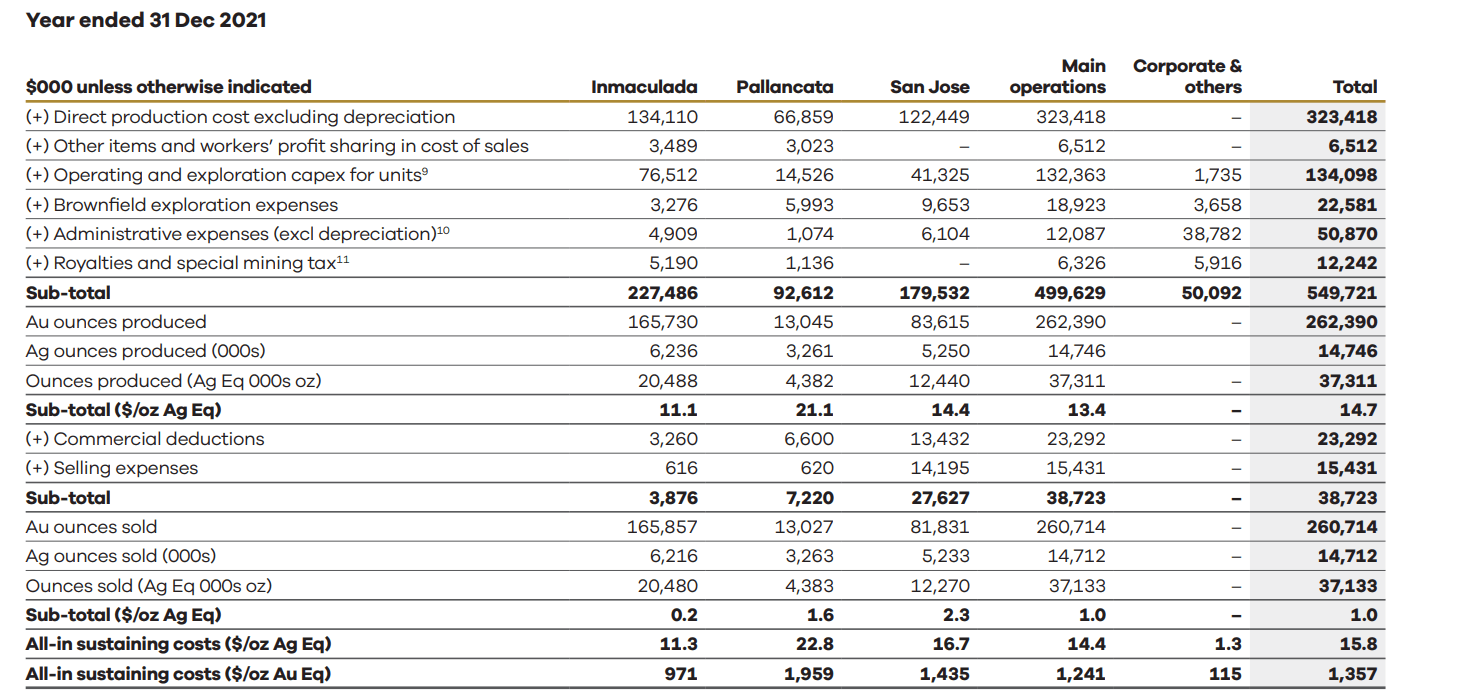

Corporate Expenses & 2021 Results (Company Annual Report 2021)

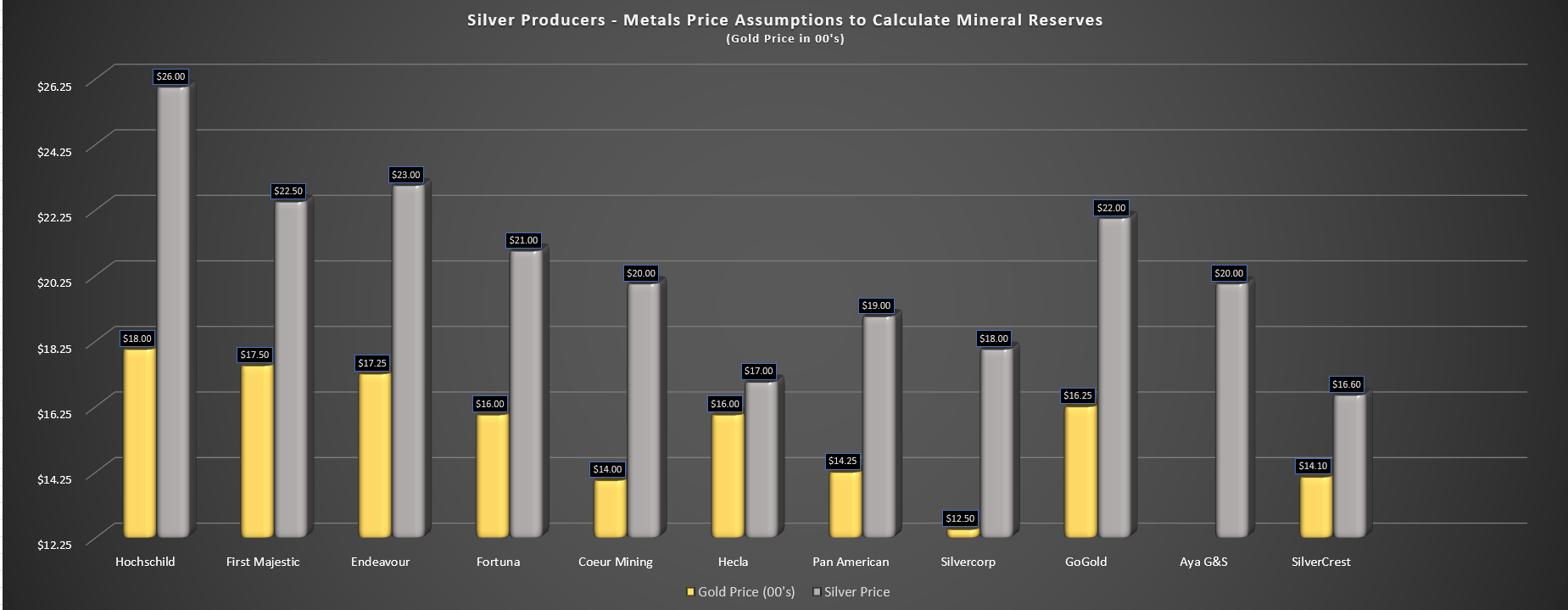

Some investors might argue that the addition of Posse is a very positive development, and I agree with this project adding ~100,000 GEOs per year over at sub $825/oz AISC. These costs are well below Hochschild's current cost profile, and we will see margin expansion as it sheds its high-cost Pallancata asset (C&M) and replaces this with Posse. Still, we will see limited production growth, given that this will be partially offset by Pallancata (FY2021 production: ~51,000 GEOs). Besides, San Jose (51% interest) isn't nearly as robust as it used to be, with a relatively short mine life here and ambitious prices used to calculate reserves ($1,800/oz gold, $26.00/oz silver).

Based on what I consider a mediocre operating portfolio relative to peers (one great asset in construction in Brazil, one high-cost and short mine life asset in Argentina) and continued uncertainty around its flagship asset, I believe a fair P/NAV multiple for Hochschild is 1.0 - 1.1x P/NAV. This translates to a fair value of US$1.07 to US$1.25, or a 27% upside at the high end of fair value. Given that I prefer a minimum 40% discount to fair value to justify buying small-cap stocks, Hochschild does not have an adequate margin of safety.

{kind=link}

Silver Producers - Metal Prices Used to Calculate Reserves (Company Filings, Author's Chart)

Finally, if we look at Hochschild from a technical standpoint, we can see that the stock has now rallied into the upper portion of its expected trading range, with strong support at US$0.59 and strong resistance at US$1.30. Based on $0.32 in potential upside to resistance and $0.39 in potential downside to support, this translates to a reward/risk ratio of 0.82 to 1.0, well below the 5/1 reward/risk ratio I prefer for smaller-cap names to justify starting new positions. To summarize, I do not see this as a low-risk buying opportunity, and if the rally persists, I would view any spikes above US$1.17 before April as profit-taking opportunities.

Summary

Hochschild Mining has seen a steady trend lower in production over the past few years, impacted by Arcata heading into C&M, declining grades, and a lacking development pipeline that hasn't been able to replace lost production. While the development pipeline is now much better with a new discovery at Pallancata, an option on Snip, and Mara Rosa, the former two are longer-term opportunities in my view (H2 2026 or later), and Mara Rosa is simply replacing lost production from Pallancata. Hence, it's not contributing to meaningful growth. So, while it has helped from a diversification standpoint, the company continues to have all of its proverbial eggs in South America (ex-Snip).

The other issue is that one of its mines (San Jose) has struggled with costs due to declining grades, and the situation in Argentina hasn't helped with hyperinflation, and inflationary pressures felt sector-wide. To summarize, with one mine having some uncertainty surrounding it, another struggling to break even at a $20.00/oz silver price, and another likely to head into care & maintenance, it's tough to balance the positives with the negatives. To summarize, I continue to see Hochschild as an inferior way to play the sector, and I would view any rallies above US$1.17 before April as selling opportunities.

For further details see:

Hochschild Mining: Posse Progress Overshadowed By Continued Uncertainty