HCHDF - Hochschild Mining: Tracking Behind FY2023 Guidance

2023-07-31 18:01:28 ET

Summary

- Hochschild Mining's Q2 production results showed a disappointing 15% decline in gold-equivalent ounces compared to the year-ago period.

- The company's lower production is attributed to delays in receiving the Modification of Environmental Impact Assessment (MEIA) and declining grade profiles at its mines.

- Hochschild is tracking at only 44% of its annual guidance midpoint and may not deliver on guidance without the timely receipt of the MEIA.

- Given the continued uncertainty with timelines pushed further on the MEIA and the fact that I still don't see enough margin of safety at a share price of US$0.95, I continue to see more attractive bets elsewhere in the sector.

Just over six months ago, I wrote on Hochschild Mining ( HCHDF ), noting that any rallies above US$1.17 would provide selling opportunities. This is because the company's flagship operation was continuing to see delays in receiving its Modification of Environmental Impact Assessment [MEIA] and this was likely to result in investors taking profits into strength until this issue was resolved. Plus, H1 2022 is typically much softer for its 51% owned San Jose Mine and Pallancata's grade profile was declining, which would likely result in a softer start to the year. Since rallying to US$1.20, Hochschild has suffered a 25% decline and while it's slightly outperformed the Silver Miners Index ( SIL ) this year, this has hardly made up for its 2900 basis point underperformance in 2022. And with a softer start to FY2023 than I expected with the company tracking at barely 44% of its annual guidance midpoint, it looks like it could be another underwhelming year. Let's look at the preliminary Q2 results below.

Q2 Production Results

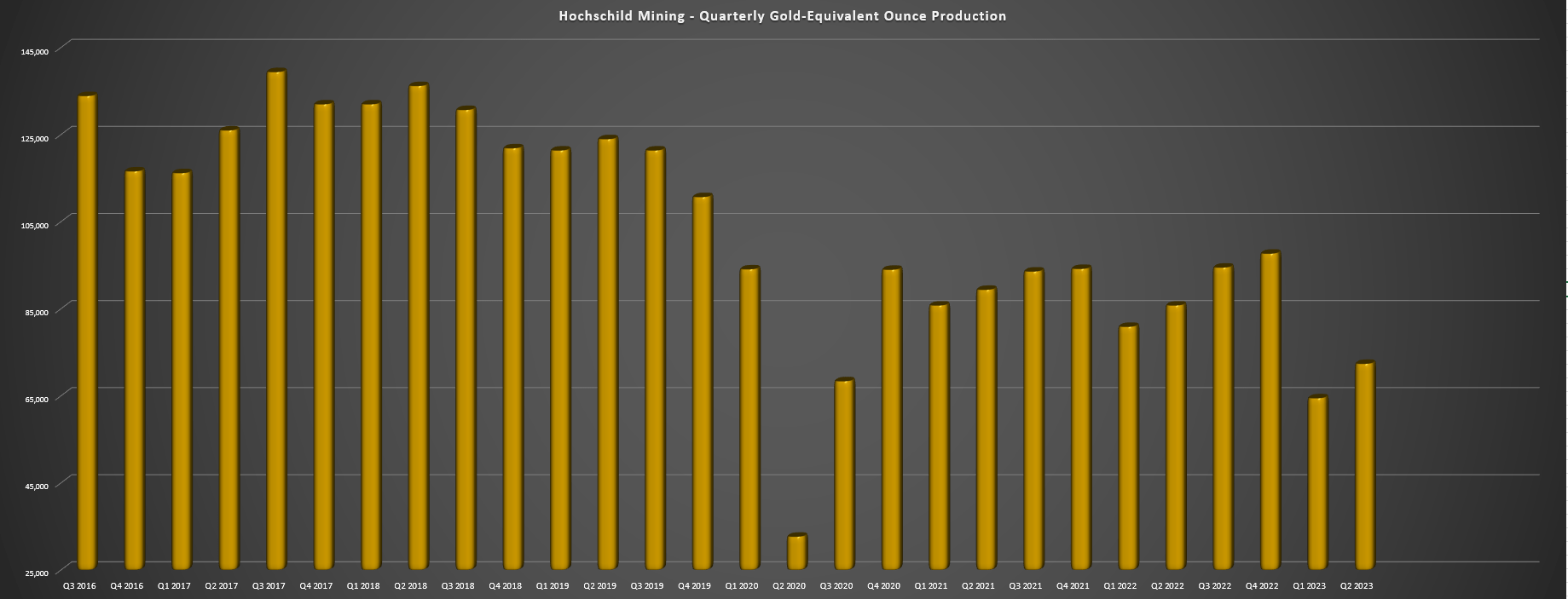

Hochschild Mining released its Q2 production results earlier this month, reporting quarterly production of ~43,600 ounces of gold and ~2.4 million ounces of silver, translating to production of ~72,400 gold-equivalent ounces [GEOs]. This translated to a disappointing 15% decline from the year-ago period (Q2 2022: ~85,800 GEOs), which was even worse considering that Hochschild was up against easier year-over-year comps, having seen a 4% decline in Q2 2022. The result is that quarterly GEO production has slid over 40% on a four-year basis (Q2 2023 vs. Q2 2019) affecting its cash flow generation, the company's net debt has soared from ~$60 million to ~$230 million, with the lower production attributed to the delayed MEIA receipt at Inmaculada and a steeply declining grade profile across its three mines (San Jose, Pallancata, Inmaculada).

Hochschild - Quarterly GEO Production (Company Filings, Author's Chart)

{kind=link}

The most pronounced of the grade declines is at Pallancata, where silver and gold grades have fallen nearly 50% in the period, down from 282 grams per tonne of silver and 1.01 grams per tonne of gold to 147 grams per tonne of silver and 0.60 grams per tonne of gold. Meanwhile, throughput is also down materially from ~241,000 tonnes to ~124,000 tonnes, with dwindling reserves at this asset and plans to move it into care and maintenance within the next year. However, we've seen a similarly declining grade profile at its 51% owned San Jose Mine, where gold grades have held up decently (5.4 grams per tonne vs. 6.9 grams per tonne) but silver grades have slid sharply, down from ~440 grams per tonne of silver to ~290 grams per tonne of silver. This is not surprising as no mine benefits from 800+ gram per tonne silver-equivalent grades forever, but the combination of lower grades and inflationary pressures has put a severe dent in profitability at this #2 asset.

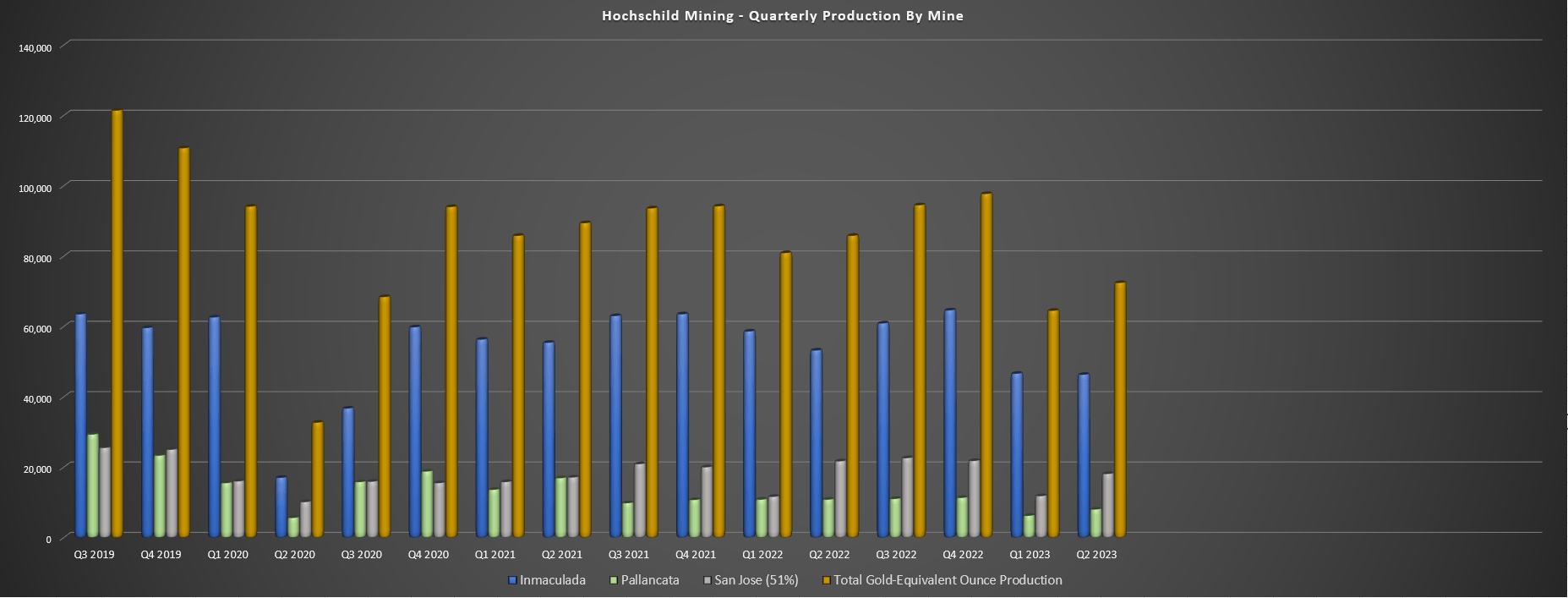

Hochschild Mining - Quarterly Production by Mine (Company Filings, Author's Chart)

{kind=link}

Digging into Q2's production results a little closer, Pallancata produced just ~8,000 GEOs in the period, down from ~9,800 GEOs in Q2 2022. The dip in production was related to lower grades and throughput, and H1 production was down just as significantly from ~19,500 GEOs in H1 2022 to ~14,200 GEOs in H1 2023. As for the company's San Jose Mine, we also saw a decline in production from ~20,500 GEOs to ~18,100 GEOs, with higher throughput in the period offset by lower grades of 288 grams per tonne of silver and 5.4 grams per tonne of gold, respectively. This resulted in less than 27,000 attributable GEOs from these two assets combined in the period, a relatively meager figure that didn't do anything to help what was also a softer start to the year at its flagship and much larger Inmaculada Mine.

As for the company's much larger Inmaculada Mine, mine development in Q2 was impacted similar to Q1 due to the delayed receipt of the MEIA. The result was that production slipped to ~46,300 GEOs (Q2 2022: ~50,800 GEOs), with lower throughput more than offfsetting the higher grades in the period. And while Hochschild is confident that it will receive its permits at Inmaculada, the timeline has now been pushed from H2 2022 as of last year to Q2 2023 as of its Q4 2023 Conference Call, and unless we see the receipt of the MEIA, production will continue to be impacted and will be halted by the end of December. As discussed by the company, it continues to work with SENACE to complete the final review.

"As we talked about, we are expecting the MEIA decision during the second quarter of 2023..."

- Hochschild Mining, Q4 2022 Conference Call

While the company didn't provide any update to its guidance, production is currently tracking at just ~44% of its annual guidance midpoint of 307,500 GEOs with six months left to go and I would be surprised to see Pallancata or Inmaculada's quarterly production improve much from Q2 2022 levels. This means that Hochschild is unlikely to deliver on guidance this year without the timely receipt of its MEIA to allow the company to ramp up mine development. And in a worst case that the MEIA is not approved this year, we could see the company incur up to $10 million in combined care & maintenance costs at Pallancata and Inmaculada next year, with any growth from Mara Rosa more than offset by sidelining these two assets. Normally, I would say that the worst case is not worth factoring in, but to date, the company has struggled to pin down a date for the MEIA which makes it hard to be overly optimistic about the imminent approval of this permit.

As noted in Hochschild's 2022 Annual Report:

Failure to secure approval of the Inmaculada MEIA (see Liquidity risk commentary above) would result in a suspension of operations at Inmaculada during H2 2023 until a new MEIA is approved. The specific date of suspension will depend on operational factors that are being evaluated.

Recent Developments

Outside of the continued delays in receiving the Inmaculada MEIA, we saw a CEO transition earlier in Q2, with its previous CEO stepping down to assume a new role at another company and Hochschild's Chief Operating Officer Eduardo Landin moving into the CEO role. In addition, we saw Rodrigo Nunes (Director of Technical Services) take over as Chief Operating Officer. Elsewhere, Mara continues to make solid progress, with the gold project in Brazil sitting at 88T total project completion and on track for first gold pour in H2-2024. Notably, 97% of purchase orders were issued which reduced any capex risk and deliveries for the crusher, belt conveyors, thickeners, ball mills, and other key parts remain on schedule per the latest disclosures.

{kind=link}

Meanwhile, from a financial standpoint, Hochschild is de-risking itself given its relatively large debt load (~$227 million in net debt for a company of its size, especially if Inmaculada must be moved into care and maintenance), by adding hedges in the 2025 to 2027 period. This included adding 150,000 ounces of gold hedges at an average price of $2,163/oz from 2025 to 2027, which increased its hedge position which currently stands at ~29,300 ounces at $2,047/oz and ~27,600 ounces next year at $2,100/oz. In my view, this is a positive development and a prudent move in case the company must move two of its assets into care and maintenance, and especially given that San Jose's costs have soared over the past couple of years, coming in at $21.70/oz per silver-equivalent ounce last year.

Valuation

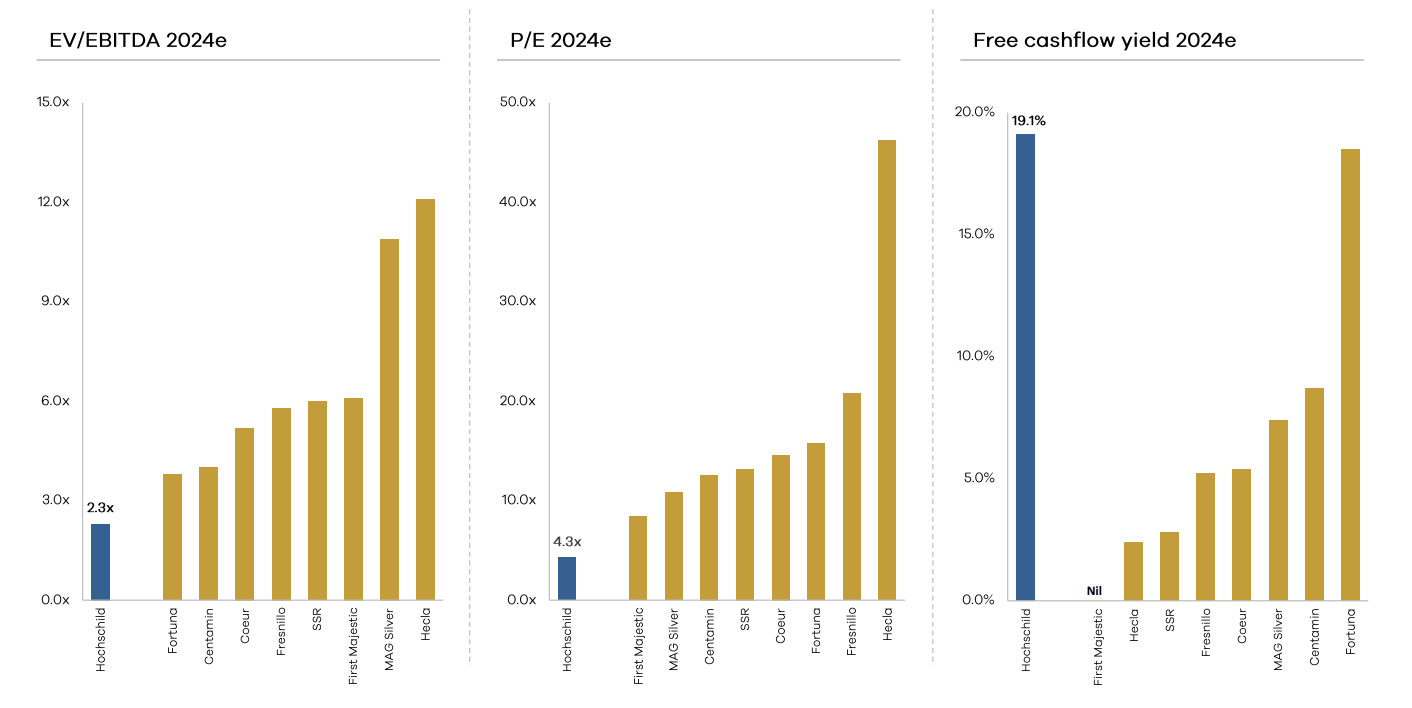

Based on ~514 million shares and a share price of US$0.95, Hochschild trades at a market cap of ~$488 million and an enterprise value of ~$715 million. At first glance, this may seem like a steep undervaluation compared to peers, especially when there are names like First Majestic ( AG ) trading a much higher valuation also as a high-cost producer in Tier-2 ranked jurisdictions. And as the chart below highlights, Hochschild trades at one of the highest free cash flow yields sector-wide and one of the lowest EV/EBITDA multiples. However, while this clearly highlights Hochschild's relative undervaluation, I would argue that many of these producers are richly valued for their level of quality, meaning that Hochschild is cheap when compared to overvalued producers. Plus, while many of these producers may be higher cost, Hochschild is in the unfavorable position of having a short mine life at two assets, a major delay in permitting at its flagship asset that's created uncertainty and its only real redeeming quality being Mara Rosa.

{kind=link}

Assuming Inmaculada sees the timely receipt of its MEIA which has already been pushed from H2 2022 to H1 2023 and now investors must hope that it gets delivered this year to not affect production further, the stock could rally sharply, especially with Mara Rosa nearing the finish line. However, I prefer to buy high-quality producers with a track record of beating guidance at an attractive price vs. what I would consider being lower-quality and high-risk producers at an attractive price. And while Mara Rosa is a very solid asset that is an upgrade to the Hochschild thesis, the overall thesis is weak when compared to some of the higher-quality names elsewhere in the sector, given that we have two short mine lives with declining grade profiles and two decent assets (Inmaculada, Mara Rosa), with all of these assets in non-Tier 1 jurisdictions. This doesn't mean that the thesis can't work, and there's certainly a lot of negativity priced in, but I still don't see a compelling enough reward/risk setup at US$0.95.

So, what would change my mind?

If we were to see a pullback below US$0.65 where the stock would drop back into the lower portion of its support/resistance range or if we saw the receipt of the MEIA at Inmaculada, these would make the stock a more attractive Speculative Bet. This is because at a price of US$0.65, the stock would trade at a ~$550 million market cap with Inmaculada and Mara Rosa alone easily justifying the valuation, meaning that the two short mine lives at San Jose (51% interest) and Pallancata would be irrelevant. And if Hochschild receives its MEIA at Inmaculada, this would reduce uncertainty and I would consider entertaining a higher buy point for the stock. That said, neither of these setups are present today, so I prefer to focus on more attractive risk-adjusted bets, especially with some higher-quality names also trading at high double-digit FY2025 free cash flow yields.

Summary

Hochschild Mining had a softer H1 2023 than I expected because of another relatively weak Q1 at San Jose (well below 2020 and 2021 levels) and a negative impact to Inmaculada's production for the duration of Q2 (whereas I was previously expecting the mine permit to be in place in May latest). This has left the company tracking behind its FY2023 guidance midpoint of 307,500 GEOs, and it looks like we'll see another consecutive annual guidance miss, especially if Pallancata sees a further dip in production as the year progresses (on track to head into care & maintenance). And given the delays we've already seen in receiving this permit, I'm a little surprised the company was not more conservative with guidance to ensure it didn't have to report another annual miss if the MEIA was a few months behind schedule.

On a positive note, Mara Rosa is nearing the finish line, and this is a very solid asset with all-in sustaining costs expected to come in at industry-leading levels below $1,000/oz even after factoring in inflationary pressures. Plus, the company has secured additional gold hedges from 2025 through 2027 to de-risk the company financially and it appears confident it will secure the MEIA this year. Still, at a ~$720 million enterprise value, I still don't see enough margin of safety here if we don't see a positive resolution to the MEIA by year-end and a second asset has to go into care & maintenance temporarily (Inmaculada and Pallancata). So, while I would consider Hochschild Mining as a Speculative Buy below US$0.65, I continue to focus on other names elsewhere in the sector.

For further details see:

Hochschild Mining: Tracking Behind FY2023 Guidance