HOEGF - Hoegh Autoliners Benefits From Tailwinds Full-Year Dividend Could Exceed 15%

2023-05-16 08:30:00 ET

Summary

- Hoegh Autoliners owns and operates 40 car-carrying vessels.

- The market is facing capacity constraints which sent the average charter rates much higher.

- Hoegh Autoliners is definitely taking advantage of these tailwinds before new vessels will hit the water.

- The company uses a 50% payout ratio for its dividends. The Q1 dividend represented almost 5% of the current share price.

- Q2 will likely be equally strong as the first quarter of the year, which bodes well for the Q2 dividend.

Introduction

I have been keeping an eye on Hoegh Autoliners ASA ( OTCPK:HOEGF ) as the entire car carrier shipping industry appears to be on the verge of a perfect storm . The demand for shipping capacity is picking up while there are very few vessels available to be chartered. This resulted in upward price pressure and a massive tailwind for companies operating in this segment of the shipping industry.

{kind=link}

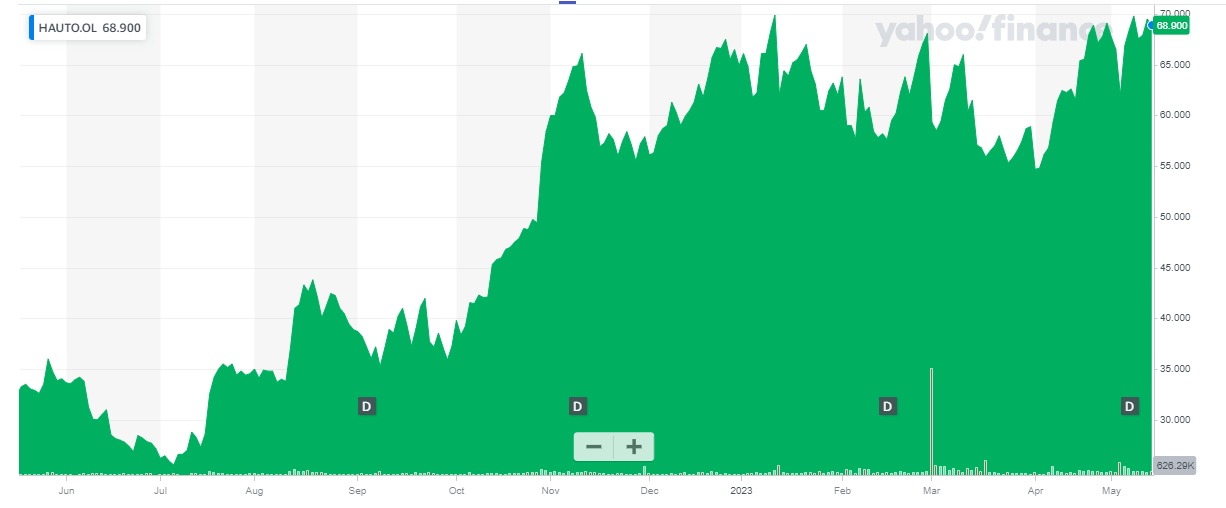

Hoegh Autoliners has its primary listing on the Oslo Stock Exchange where it's trading with HAUTO as its ticker symbol . There are 191M shares outstanding resulting in a current market cap of 13.1B NOK which is approximately 1.24B USD at the current exchange rate . As Hoegh reports its financial results in USD, I will use the USD as base currency throughout this article. The current share price of 68.9 NOK is the equivalent of approximately US$6.5 per share.

As expected, the first quarter was strong

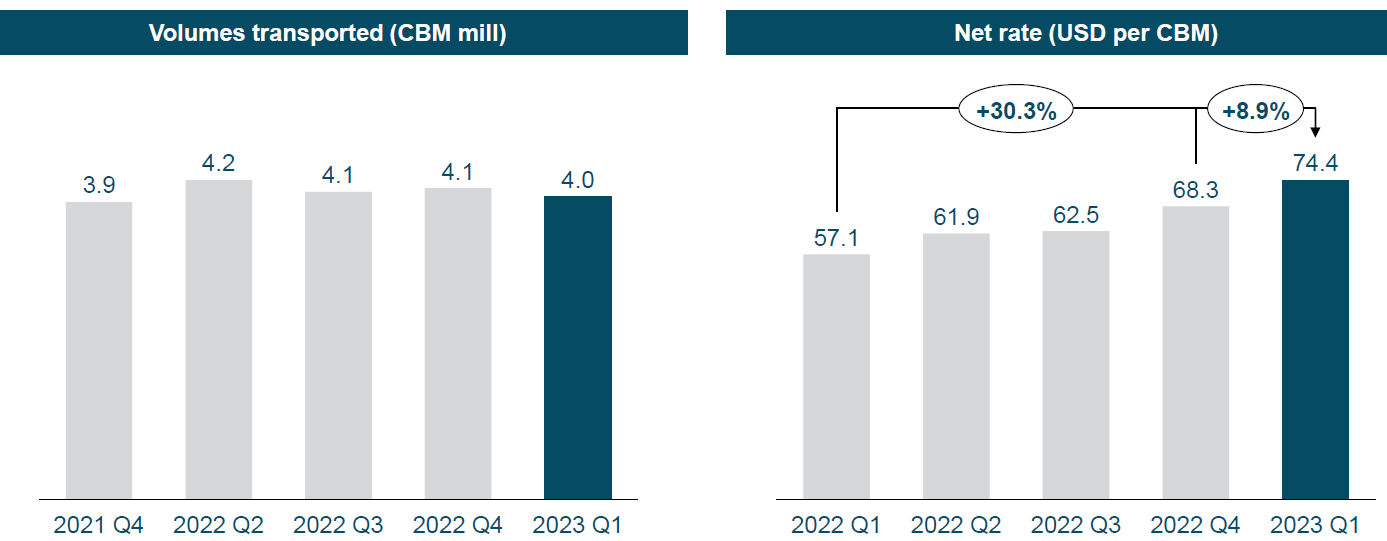

There are no signs of any weakness just yet as Hoegh was able to secure a very similar revenue in the first quarter of this year compared to the last quarter of this year. However, the operating expenses decreased in the first quarter of the current financial year which resulted in an EBITDA expansion . Although the total amount of volume transported by Hoegh decreased in the first quarter of the year to the lowest level since the final quarter of 2021, the average rate continued to increase: Hoegh reported an 8.9% QoQ rate increase and an increase of approximately 30% since the end of 2021.

{kind=link}

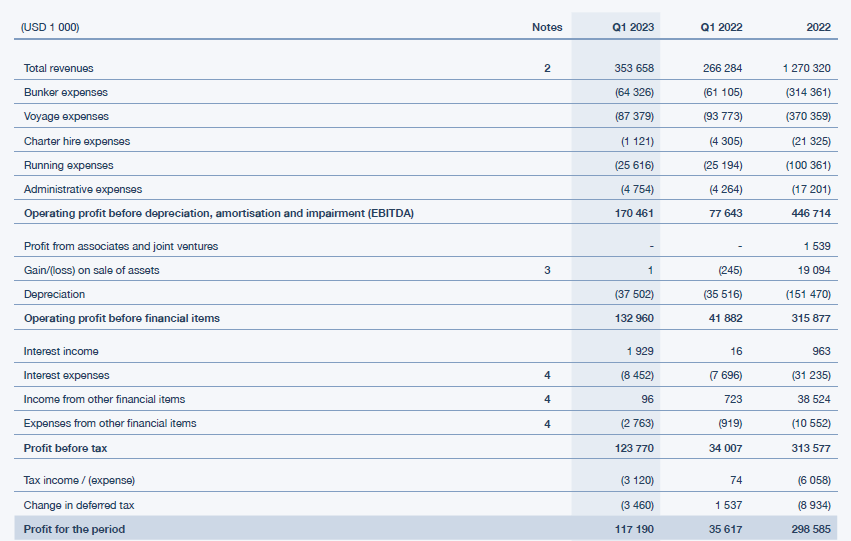

As you can see below, the company reported a total revenue of just under $354M but reported lower bunker and voyage expenses compared to the final quarter of last year. And despite a small increase in the administrative expenses, the EBITDA jumped from $156M in Q4 2022 to $170.5M in Q1 2023. That also is a very substantial increase from the less than $78M in EBITDA generated in the first quarter of 2022 before the charter rates started to increase.

{kind=link}

And thanks to Hoegh Autoliners running a conservative balance sheet, the net interest expenses remained very reasonable. This helped Hoegh to report a pre-tax income of $123.8M and after deducting the relevant taxes, the net income generated in Q1 2023 was $117.2M which results in an EPS of $0.61. Using the current exchange rate, that's approximately 6.47 NOK.

A great result, but just like the past few quarters, I wanted to dig a bit deeper into the company's cash flow performance. After all, vessels have a finite useful life and the company will have to make sure it will be able to rejuvenate the fleet when the older vessels need to be retired.

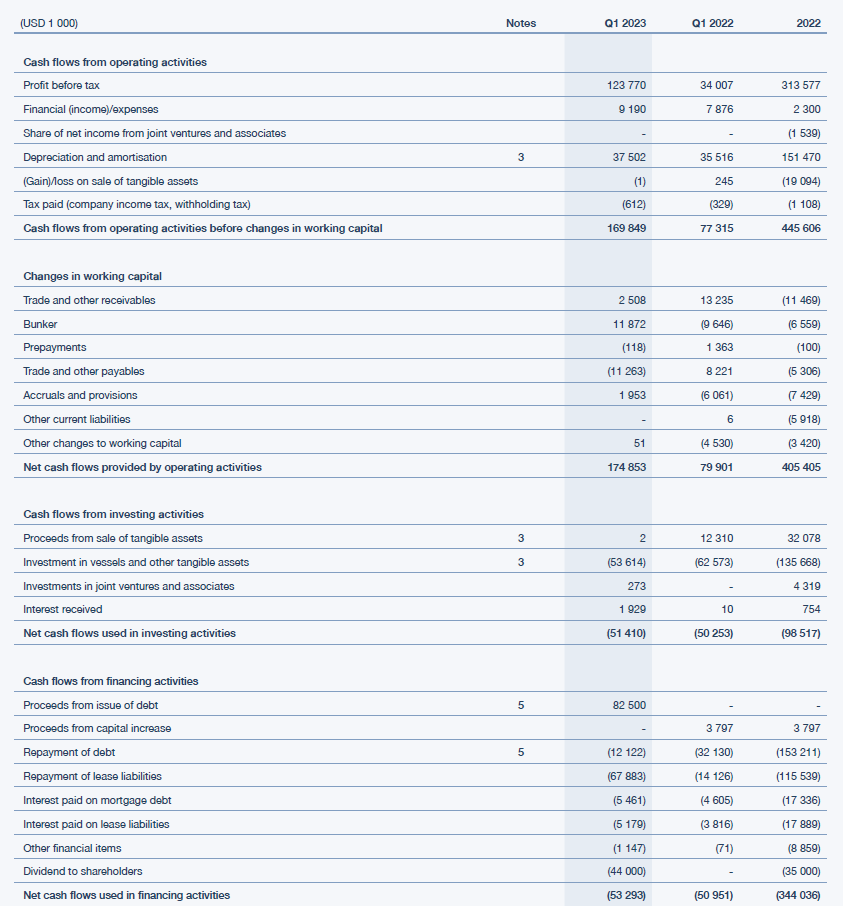

Hoegh Autoliners is managing its cash flows pretty well. The company reported an operating cash flow of just under $170M before changes in the working capital position, and after deducting the $68M in lease payments as well as the $8.7M net interest payments ($10.6M paid versus $1.9M in interest received), the underlying operating cash flow was roughly $93M. Keep in mind however that the lease-related cash flows are not linear and it fluctuates on a quarterly basis as some of the leased vessels have purchase options attached to them and from time to time, Hoegh effectively exercises those options. In the first quarter of the year, it took delivery of the Hoegh Berlin and the Hoegh Tracer.

{kind=link}

Hoegh Autoliners declared a dividend of $0.315 per share based on its Q1 results. This represents about 50% of the adjusted net profit. Using the current exchange rate, the dividend is approximately 3.34 NOK.

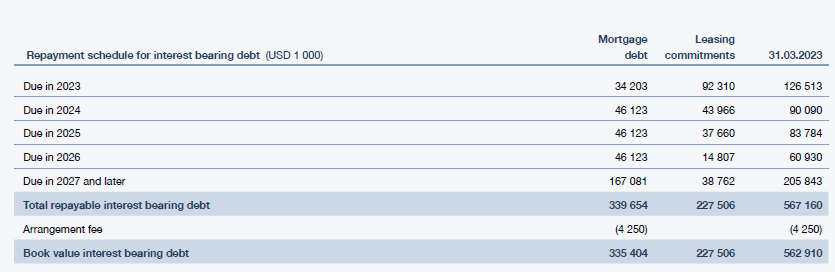

Notwithstanding the high amount of lease payments, the company still generated approximately $40M in free cash flow despite also investing almost $54M in new vessels. The image below shows the remainder of the scheduled debt and lease payments for the next few years, indicating the cash outflow related to these items will be substantially lower in the next few quarters and years.

{kind=link}

So while the total cost of the dividend ($60M based on the $0.315/share ) doesn't appear to be covered by the free cash flow, keep in mind the free cash flow was hit by a disproportional amount of investments in the first quarter of the year.

The balance sheet: very robust

The balance sheet is still very strong despite having exercised the options to acquire two vessels during the first quarter. As of the end of March, Hoegh had $253M in cash on the bank, it had about $289M in long-term debt and just around $46M in current debt (excluding lease liabilities, which totalled an additional $228M). The net financial debt on the balance sheet is just $82M which is a fraction of the annualized EBITDA adjusted for lease amortization. And even if you would include the lease liabilities in the equation, the debt ratio would still be pretty favorable thanks to the very strong EBITDA results right now.

{kind=link}

As the fleet has now been 'right-sized' I'm not expecting any more unexpected capital expenditures (other than the Aurora newbuild program ) from Hoegh Autoliners.

Investment thesis

Hoegh Autoliners expects its second quarter to be very strong as well. That's not a surprise as the market dynamics are still very much operating in favor of the operators of car carriers. As explained in a previous article on Gram Car Carriers , new vessels will hit the water over the next few years on which will likely put some pressure on charter rates (shipment volumes are also expected to increase so a portion of the capacity increase could be absorbed). That's inevitable and hardly a surprise given the cyclical nature of the shipping sector. This also means investors should be well aware of those risks and may want to look for an exit later this year, but for now, Hoegh Autoliners still has a license to print cash.

I currently have no position as my limit order from a few months ago appeared too optimistic and I didn't want to chase the stock. But Hoegh Autoliners is doing everything the right way and is taking optimal advantage from the tailwinds the industry is currently experiencing.

For further details see:

Hoegh Autoliners Benefits From Tailwinds, Full-Year Dividend Could Exceed 15%