HOEGF - Hoegh Autoliners Is Almost Debt-Free Trading At 2.5 Times Earnings

2023-03-17 11:30:00 ET

Summary

- Hoegh Autoliners is an operator of car carrier vessels and currently experiences a perfect storm in the RoRo market.

- Additional vessels will hit the water from 2024 on which will put pressure on the charter rates.

- Hoegh should be debt-free by then.

- The company is trading at less than 3 times earnings based on the Q4 results while offering a dividend yield of in excess of 15% using a 40% payout ratio.

- This is not a partnership, so a Hoegh LNG Partners scenario is unlikely here.

Introduction

In a December article, I explained why I had high hopes for Hoegh Autoliners ( OTCPK:HOEGF ), the owner and operator of car carrying vessels. The rates were going up as there were very few vessels available in Q4 2022 and 2023 as the demand for transportation capacity increased and the worldwide fleet will only start to grow from 2024 on when new vessels will hit the water. I argued the Q4 results would be good, and the company did not disappoint as it posted a record-high quarterly EBITDA result.

{kind=link}

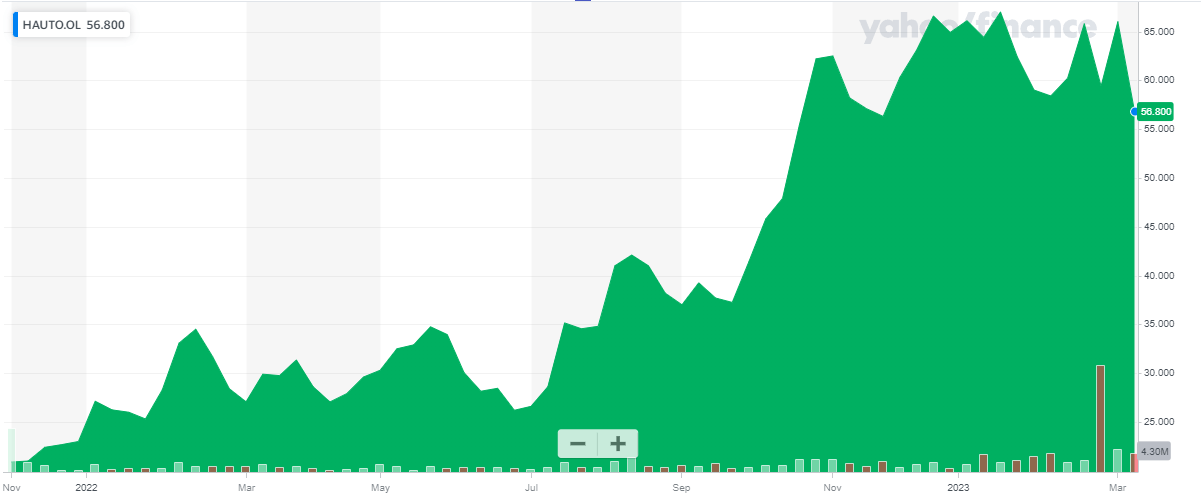

Hoegh Autoliners has its primary listing on the Oslo Stock Exchange where it's trading with HAUTO as its ticker symbol . There are 191M shares outstanding resulting in a current market cap of 10.9B NOK which is approximately 1B USD. As Hoegh reports its financial results in USD, I will use the USD as base currency throughout this article. The current share price of 56.8 NOK is the equivalent of approximately US$5.3.

All relevant information (the financial report as well as the corporate presentation) can be found here .

Q4 was a record quarter for the company

In my December article I mentioned I expected the fourth quarter of 2022 and 2023 as a whole to be better than the preceding few quarters as all the stars were aligning for the car carrier companies. To get a better understanding of why I was (and still am) bullish on the prospects of car carrier vessels, I’d invite you to read my previous article on Hoegh Autoliners which was published a few months ago.

{kind=link}

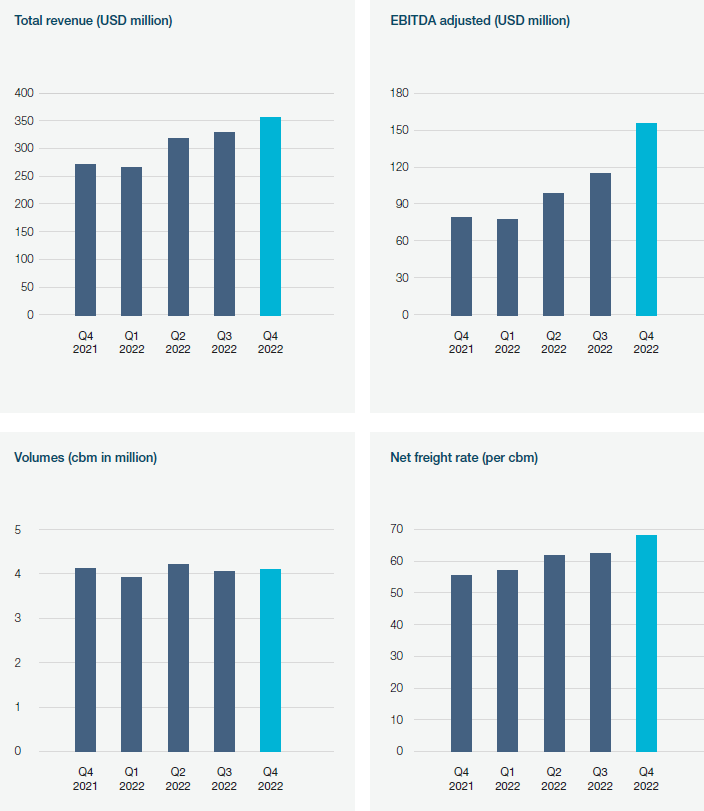

And I wasn’t disappointed when Hoegh reported on its Q4 2022 results. The total revenue increased to in excess of $350M (+8% QoQ) while the bunker expenses decreased by 16% and this obviously provided a major boost to the EBITDA which jumped from $114M in Q3 to a very stunning $156M in the final quarter of the year.

{kind=link}

The EBIT also increased quite substantially, from $100M to $116M. This 16% increase is much lower than the almost 40% jump in the EBITDA result but that’s mainly caused by a non-recurring gain on the sale of an asset to the tune of approximately $20M which was recorded in the third quarter. The underlying EBIT in Q3 was just around $80M which means the EBIT in Q4 came in more than 40 higher.

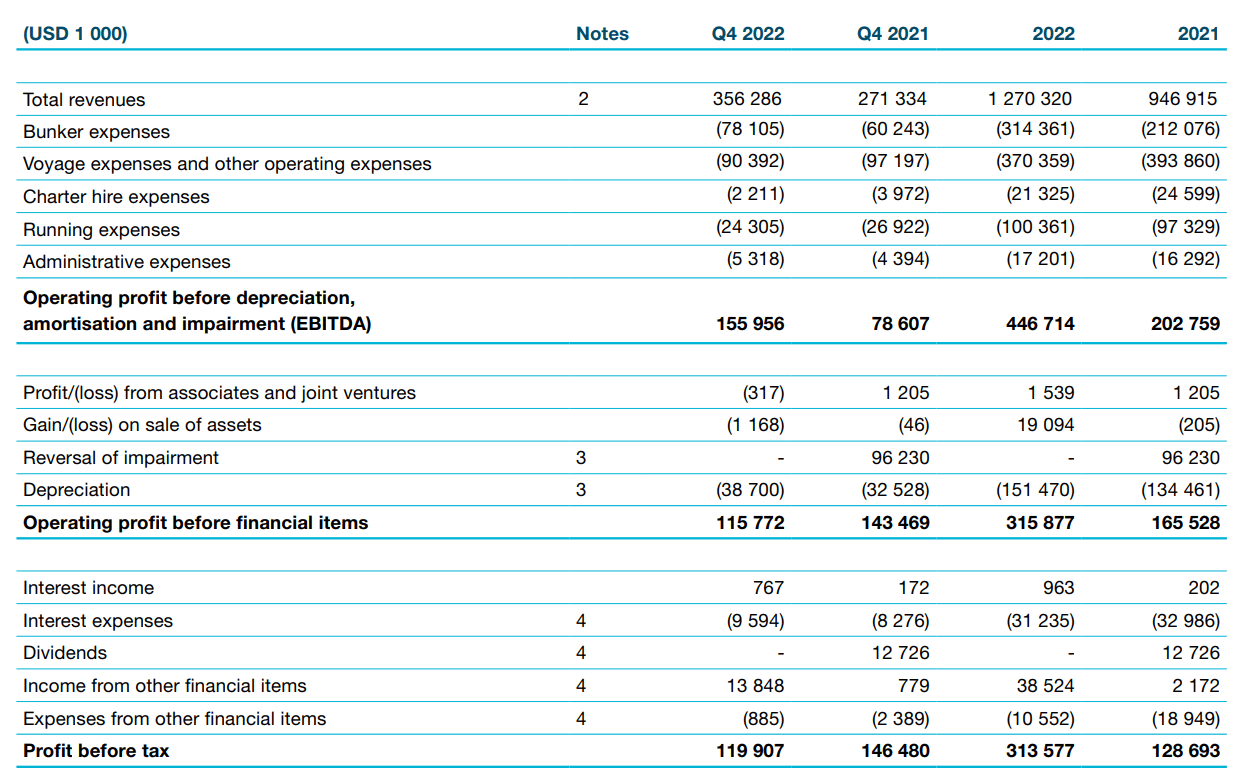

The one item Hoegh performed ‘worse’ on was the net interest expense. Hardly a surprise and because the company is running a lean balance sheet, the increase of just $3M for the quarter is very manageable. The bottom line shows a pre-tax income of $120M and a net income of approximately $118M which represents 62 cents per share.

This pushed the full-year EPS to $1.57M (with the caveat about 6.5% of this result was caused by the sale of a vessel which is a non-recurring item) but even after deducting this impact, the stock is currently trading at less than 4 times its earnings.

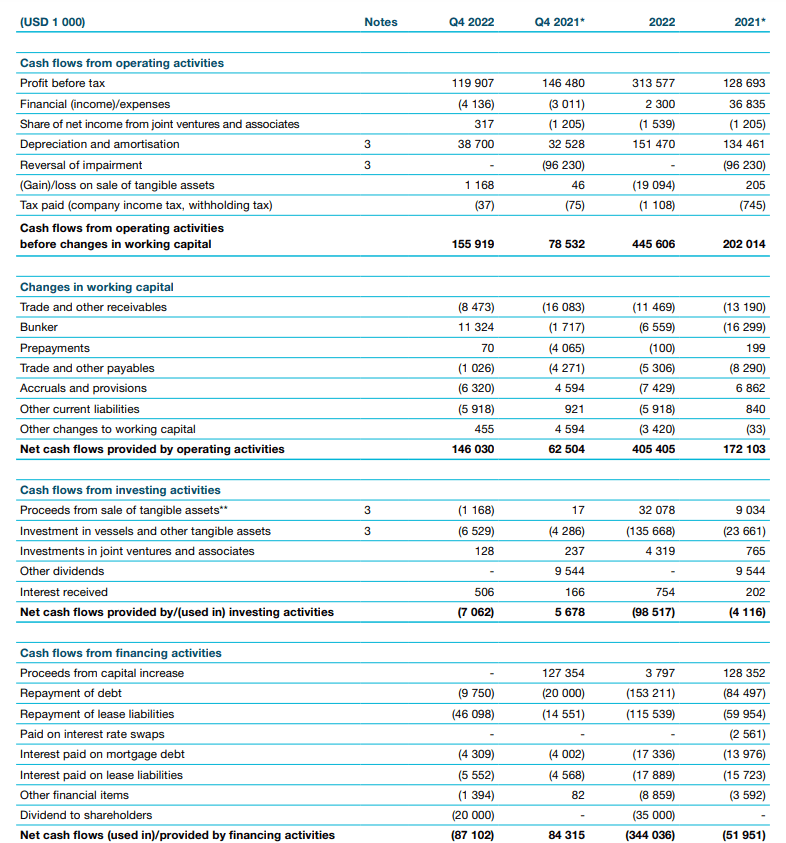

And those earnings aren’t inflated. The cash flow statement provided by Hoegh Autoliners paints a very similar picture.

As you can see below, the operating cash flow before changes in the working capital position was approximately $156M. We should still deduct the $46M in lease payments and the $10M in interest expenses on both the financial debt as well as the lease liabilities, and subsequently end up with about $100M in net operating cash flow during the quarter. As Hoegh did not purchase new vessels, the capex remained limited to just $6.5M and the underlying net free cash flow result was approximately $93.5M or $0.49 per share.

{kind=link}

That is lower than the reported net income, mainly due to the discrepancy between the depreciation and amortization charges and the incurred capex and cash lease payments.

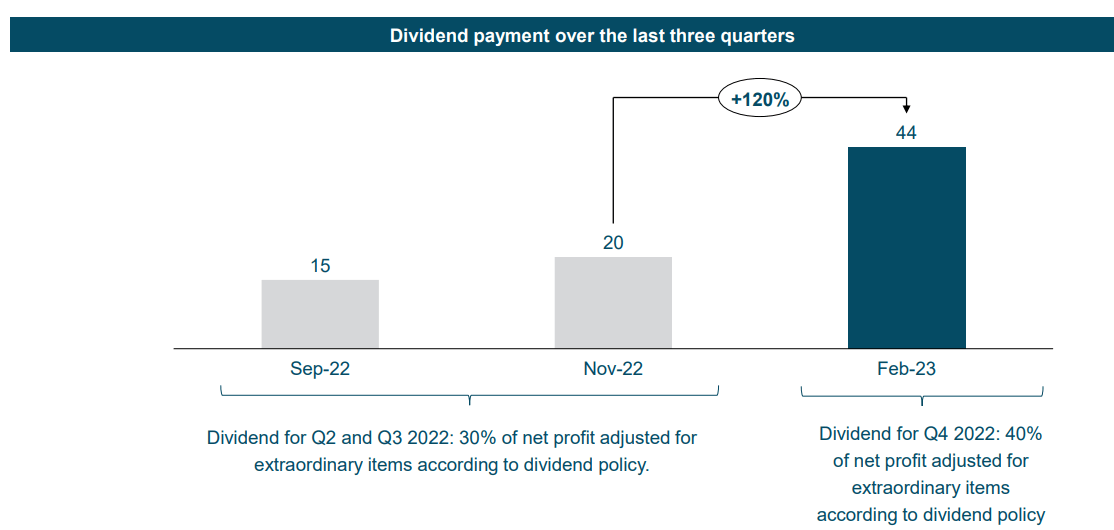

As the fourth quarter was very strong, Hoegh more than doubled its quarterly dividend from $20M to $44M which was the equivalent of approximately $0.23 per share. This has already been paid in February.

{kind=link}

Hoegh is still pretty optimistic on 2023 as the Norwegian operator expects the general market to be strong. Very few newbuilds will be delivered this year while Hoegh also expects the total transported volumes will increase compared to 2022 which should bode well for rates and the profitability of the company. Keep in mind that Hoegh works with longer-term contracts and the company reconfirmed its ‘contract portfolio is gradually renewed at higher rates’. Hoegh also confirmed the first quarter of 2023 has started well and the company expects to publish another set of strong results. It did not go into detail whether or not the Q1 2023 results would be as strong as the Q4 results so I should perhaps moderate my expectations a little bit.

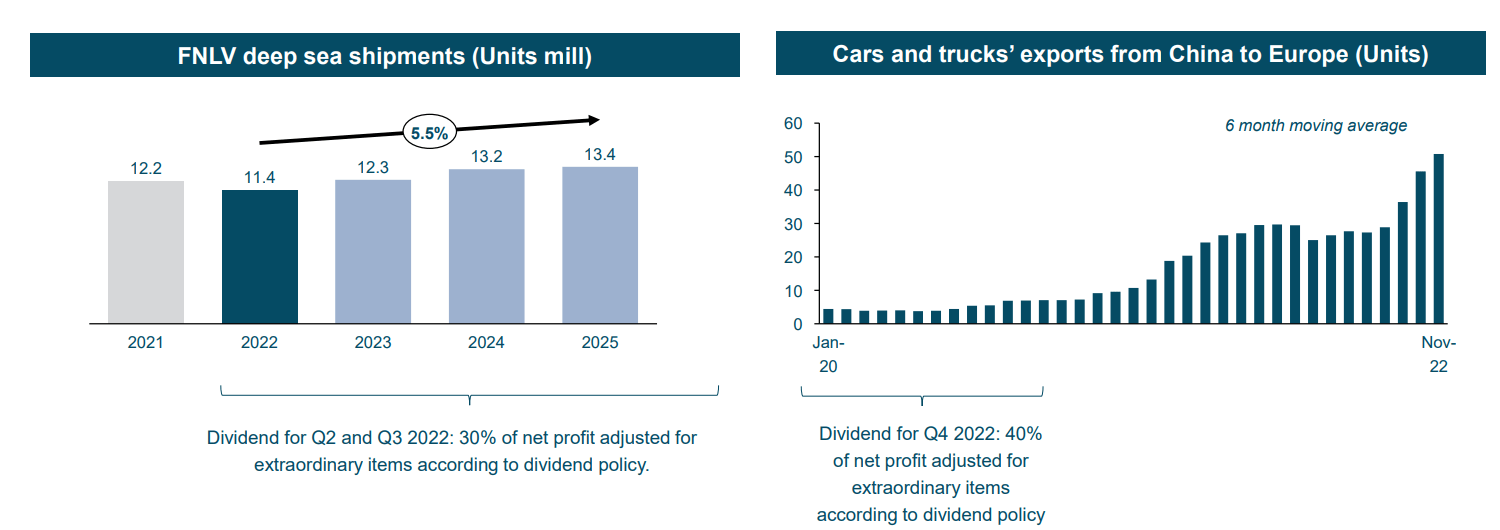

And although very few newbuilds will hit the water in 2023, quite a bit of additional tonnage will be delivered over the next half decade. The order book until the end of 2026 shows there will be a fleet capacity expansion of approximately 20% but as the expected CAGR for deep sea vehicle transportation is anticipated to come in at around 5-5.5%, it looks like the extra tonnage will simply absorb the demand increase while it will allow operators of older vessels to retire the oldest and least fuel-efficient vessels in their fleet.

{kind=link}

Investment thesis

I don’t have a position in Hoegh Autoliners just yet and several other investment opportunities popped up in the past few weeks due to the banking crisis. I am still very interested in Hoegh where the Maersk shipping company has a large minority stake (and Hoegh Autoliners is not a partnership like Hoegh LNG Partners).

While I acknowledge the fleet expansion will weigh on the charter rates, let’s not forget Hoegh is rapidly improving its balance sheet. The dividend is very generous but this still represents a payout ratio of just 40%. The net debt (excluding lease liabilities) decreased by approximately $140M and we can expect further debt reductions from the current level of $81M. The book value has increased by $262M during 2022 and currently stands at just over $5.5/share. And as Hoegh recently exercised another pre-existing option to acquire a vessel at a 40% discount to the current market value, there likely is more ‘hidden value’ on the balance sheet as market values exceed book values.

For further details see:

Hoegh Autoliners Is Almost Debt-Free, Trading At 2.5 Times Earnings