HCMLF - Holcim: A Construction Materials Powerhouse With A Roll-Up Strategy

2024-01-14 10:40:00 ET

Summary

- Holcim is a Swiss company that has used M&A to consolidate the cement industry and unlock economies of scale.

- Despite a decrease in reported revenue, Holcim has improved margins and organic performance.

- Holcim has pursued a significant amount of M&A, particularly in the construction supply market, and anticipates further growth in the US.

Introduction

Holcim ( OTCPK:HCMLF ) ( OTCPK:HCMLY ) is one of the largest cement and building materials producers in the world. As a Swiss company, it has used a shrewd M&A strategy to consolidate a rather fragmented market and this enabled the company to unlock economies of scale and synergy benefits. In other recent articles, I had a look at its smaller competitors Titan Cement ( OTC:TTCIF ) and Buzzi ( OTCPK:BZZUF ), with the latter trading at just 4 times EBITDA .

{kind=link}

Holcim is a Swiss company and reports its financial results in Swiss Francs and I will use the CHF as base currency in this article. I will focus on the company’s Swiss listing. The average daily volume in Switzerland, where Holcim is trading with HOLN as its ticker symbol , is roughly 1.1M shares per day. The company has been buying back its own shares in the past few years and its current share count is approximately 572M shares for a market cap of almost 37B CHF.

All is fine in the cement industry, and Holcim is posting impressive results on an underlying basis

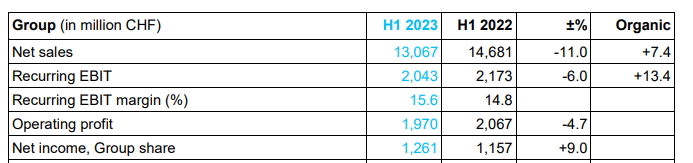

Holcim is a Swiss company, and as such, it reports its financial results in Swiss Francs. While that's a highly sought-after currency during volatile times, the strengthening Swiss Franc makes Holcim’s financial results very difficult to compare to the results of other periods. As the table below shows you, the company reported an 11% revenue decrease in the first semester of 2023 although its organic revenue growth exceeded 7% .

{kind=link}

And the margins clearly improved. Even when expressed in Swiss Francs, the 11% revenue decrease resulted in an EBIT decrease of just 6%. And looking at the organic performance, the 7.4% revenue increase happened hand in hand with an EBIT increase of in excess of 13%.

We see a similar – but improving – performance in the first nine months of the year . The reported revenue came in about 10% lower compared to the first nine months of last year but the impact on the EBIT remained limited to just 2.2%. And on an organic basis, the recurring EBIT actually grew by almost 14%.

{kind=link}

Unfortunately, Holcim only provides detailed financial statements every semester so the Q3 trading update definitely isn’t as detailed as those six-month updates. That’s why it does make sense for me to initially look back at the H1 2023 results before plugging in the data from the more recent trading updates.

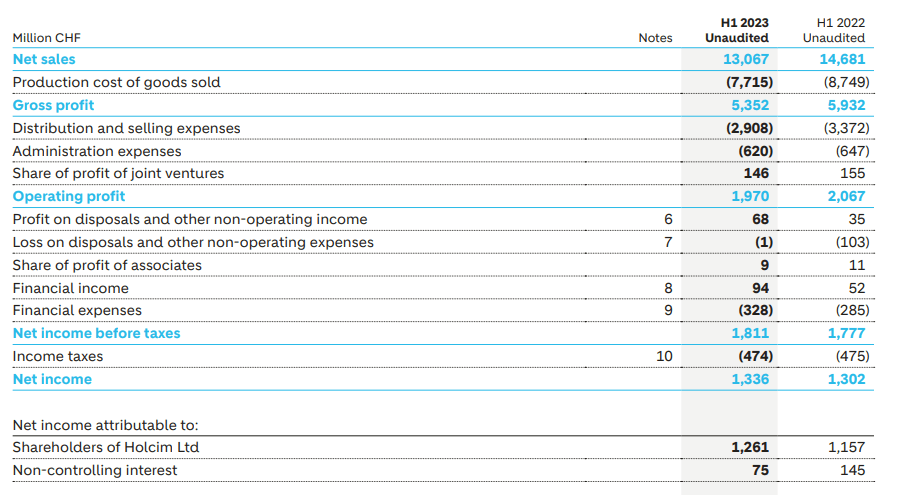

As you can see below, the company reported a total revenue of 13.1B CHF, which resulted in a gross profit of 5.35B CHF and an operating profit of 1.97B CHF . Both elements are lower than the result in the same period in the preceding year.

{kind=link}

That being said, Holcim was able to record a higher pre-tax profit mainly due to a higher profit on disposals and non-operating income and a lower loss on disposals compared to a year ago. This helped the company to publish a net profit of 1.34B EUR, which is about 2.5% higher than the 1.3B CHF in H1 2022. But there’s more. A higher proportion of the total earnings was attributable to the shareholders of Holcim as the total net income attributable to non-controlling interests fell by almost 50%. This means that about 1.26B CHF of the reported net income was attributable to Holcim’s shareholders resulting in an EPS of 2.19 CHF.

The cash flow statement also explains why I'm quite confident in Holcim’s future. The company reported an operating cash flow of 930M CHF but this includes a 1.46B CHF investment in the working capital position (mainly an increase in the receivables). However, the reported result also underestimates the total amount of taxes due by about 130M CHF while we should also deduct the 56M CHF paid to non-controlling interests as a dividend while the 174M CHF in lease payments also should be deducted.

{kind=link}

This subsequently results in an adjusted operating cash flow of 2.03B CHF. The total capex was 730M CHF resulting in a net free cash flow of approximately 1.3B CHF. That’s in line with the reported net income.

Holcim used the incoming cash flow to pursue M&A. A lot of M&A. The cash flow statement above shows Holcim spent 1.77B CHF on acquisitions which pretty much is the entire free cash flow generated during the first semester. The company is mainly focusing on the very fragmented construction supply market as the 1.77B CHF spent on acquisitions resulted in the acquisition of 18 companies. Holcim is very serious about its leadership position in North America as it already is No. 1 in cement and the number five in aggregates and ready-mix concrete. It anticipates a growth level of 5% per year in the 2023-2026 period in the US.

{kind=link}

Although the company did not provide any details on its acquisitions in Q3, Holcim acquired three other companies during the third quarter. A slower M&A pace, and this will likely allow the balance sheet to catch a breath.

At the end of June, Holcim had about 3.65B CHF in cash (I'm excluding the long-term financial investments and assets from this equation) while the balance sheet contained 1.04B in current financial liabilities as well as 13.8B CHF in long-term financial liabilities for a total net debt of approximately 11B CHF. That’s less than 2 times the EBITDA, even after the acquisitions, so that’s fine with me. Also keep in mind the high investment level in its working capital position is having a negative impact on the net debt position.

Investment thesis

When Holcim published its Q3 trading update, it also increased its anticipated EBIT margin. Whereas the company initially guided for an EBIT margin of in excess of 16%, it has hiked this guidance to in excess of 17% for FY 2023 on the back of a 17.9% recurring EBIT margin in the first nine months of the year. The company also provided a free cash flow guidance of 3B CHF but I’m waiting to see what the impact of the working capital changes is on that result.

I currently have no position in Holcim, but I like the strong cash flows, the focus on roofing and its desire to act as a consolidator in a rather fragmented market.

For further details see:

Holcim: A Construction Materials Powerhouse With A Roll-Up Strategy