HCMLF - Holcim: Concrete Upside In Concrete But Beware Valuation

2023-07-13 23:01:48 ET

Summary

- I sold my stake in Heidelberg after the share price reached my target of €75/share, despite believing in its long-term potential.

- I believe that Holcim, like Heidelberg, has reached a peak for the time being, despite giving it a neutral hold rating previously.

- I suggest that there are better investment opportunities in the market than waiting for these concrete companies to realize more upside.

Dear readers,

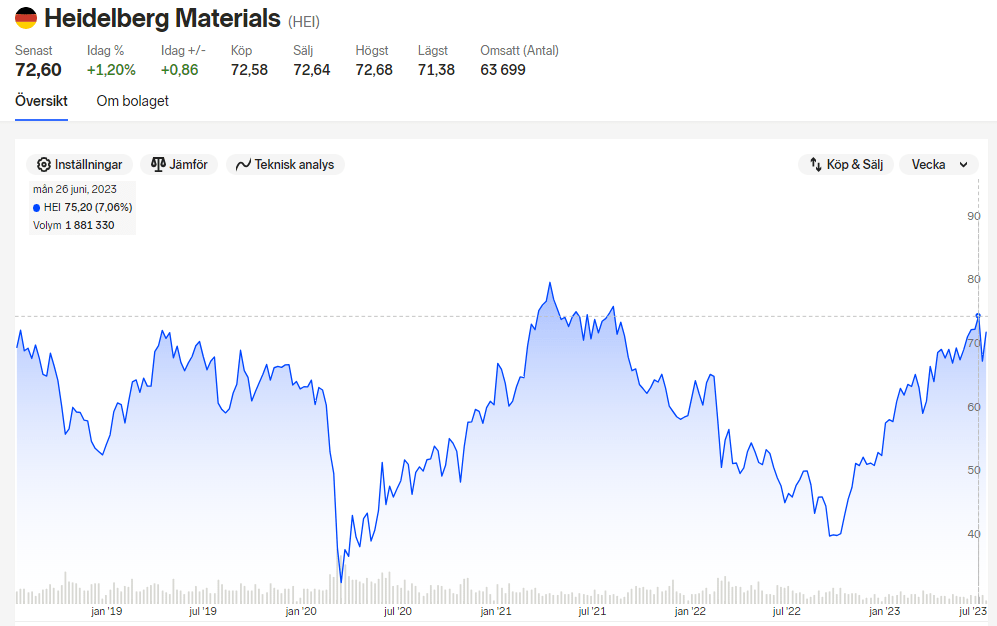

In this article, I'll update you on the advantages and potential of investing in concrete, specifically Holcim ( OTCPK:HCMLY ). I'm a big-time investor in Concrete - or at least I was until Heidelberg Materials ( OTCPK:HDELY ) breached the €75/share native price target - which is where I sold the last of my stake in the company. You can see the current share price of that company there.

{kind=link}

The reason why I sold concrete, and Heidelberg, is not because it's a bad business or I don't see more potential long-term upside, but because I invested at just over €40/share on average, which means that I managed to eke out a very impressive RoR in a very short time - and there are better potentials on the market than waiting for Heidelberg to realize even more of its upside.

I say this, because the same, or much of the same, happens to be true for Holcim. Since I wrote about Holcim last and gave you my neutral "HOLD" rating, the company has barely broken even. The S&P is up almost 8.5% since April - Holcim isn't even up 1%.

Holcim RoR (Seeking Alpha)

Much like Heidelberg, because we're talking about an industry here, Holcim has, I believe, reached what it's able to reach for the time being, and I see better alternatives elsewhere.

I want to crystallize this opinion for you in this article, and make sure you understand where it is coming from.

Let's get going.

Holcim - It's a good time for some profit rotation

If you follow my work, you'll know that I'm one of the contributors not shy about telling you when I'm buying, but also when I am rotating. I have no fear of exiting a positive investment "too early", and whenever I go into an investment, I have an "exit" target as well, though sometimes those targets can be extremely lofty.

I like investing in Concrete/aggregates because it's a very timeless sort of investment, and I don't think the segment or the companies in the segment are going anywhere. Their business models are relatively simple to understand. The companies provide products and services that do not do well if they need to be transported long distances, so it's a relatively simple cycle, provided you understand some of the influences.

Holcim has a very different asset/portfolio profile from Heidelberg. I would characterize it as more "qualitative" than what we see in Heidelberg because Heidelberg is influenced by its purchase of ItalCementi. On the other hand, Holcim cannot produce as cheaply as Heidelberg, but what it produces comes at a cheaper CO2 tax.

Generally speaking though, Holcim and Heidelberg have fairly different earnings and revenue profiles. If one company goes up in a quarter, it's likely the other will as well.

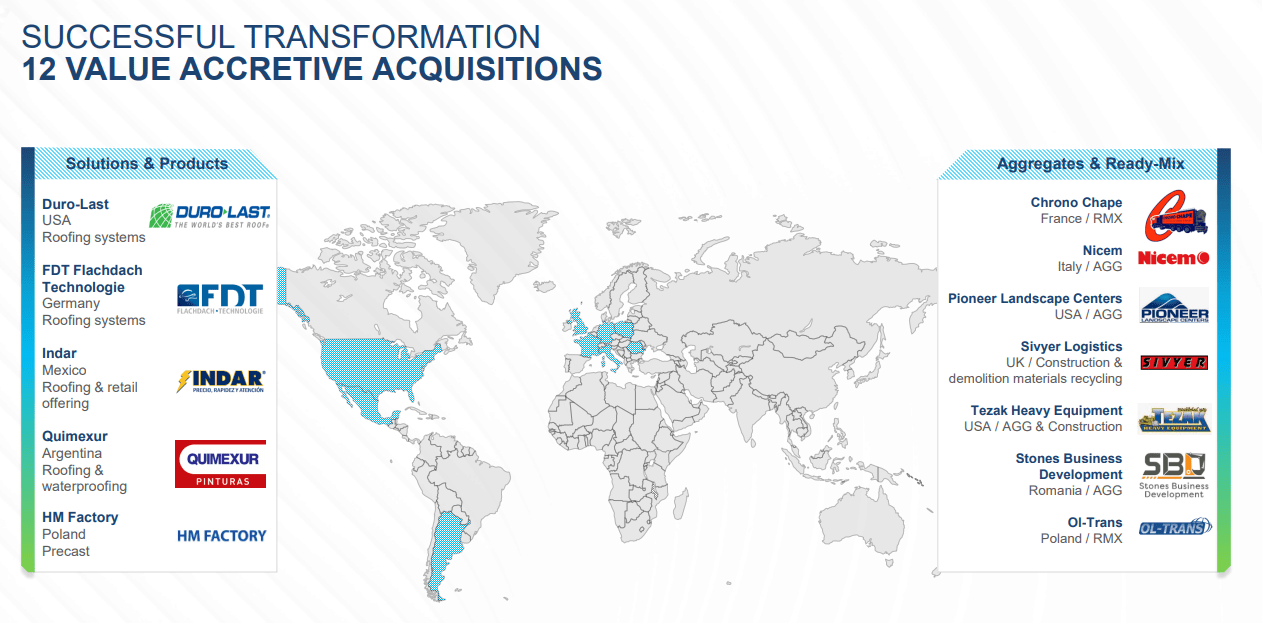

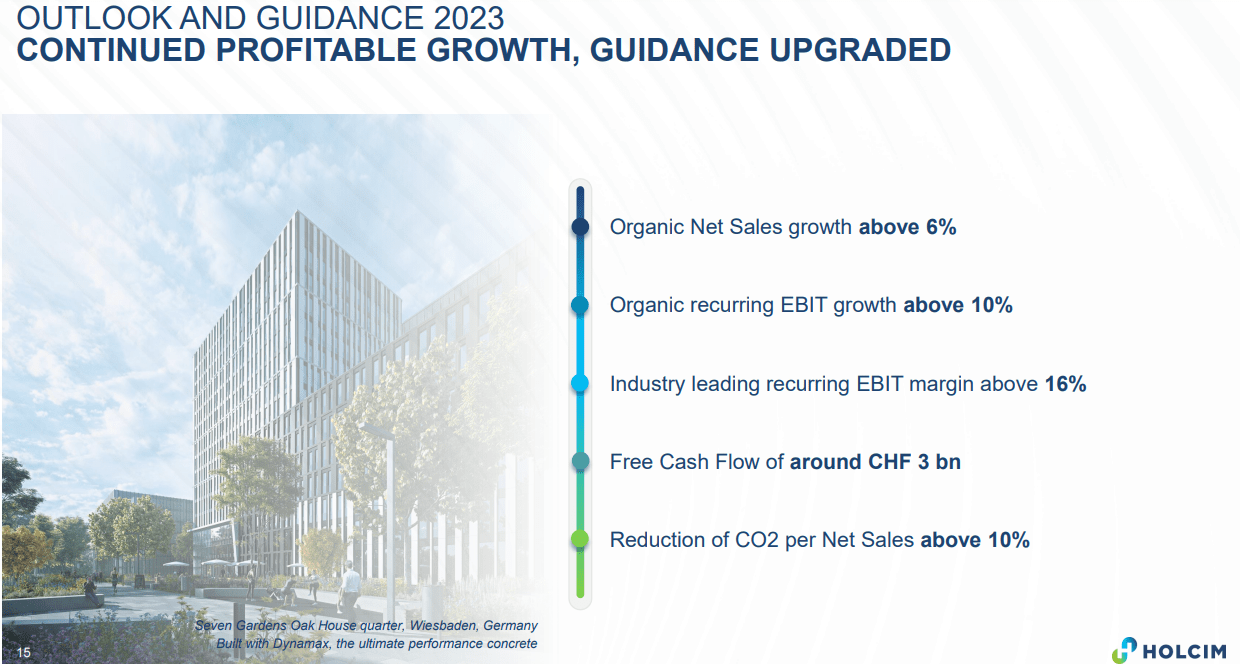

So too in 1Q23. In the trading update, the company saw a strong start to the year with organic sales growth of 8%, EBIT growth of 12% and 12 attractive M&A's. Holcim remains one of the most climate-aligned concrete companies in the sector, and they also upgraded their 2023E guidance.

Here are some of the new names that Holcim added to its portfolio.

{kind=link}

Overall, the company with the exception of its Argentina exposure, has a markedly different risk profile geographically than Heidelberg as well, which has more exposure to APAC. The company is also a near-leader in global net-zero carbon concrete.

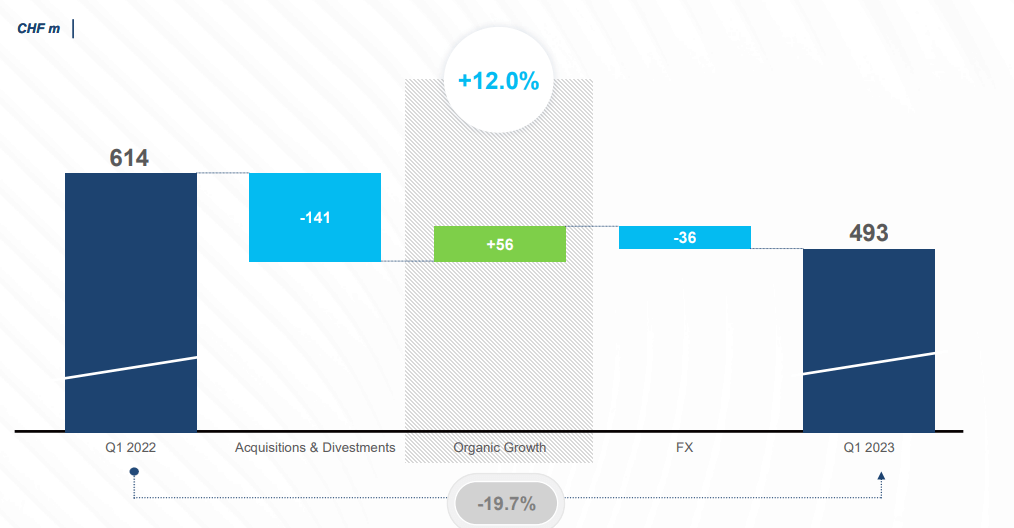

Despite the company's organic growth in terms of EBIT, the actual EBIT itself was lower than in 1Q22 - but this is due to company divestments and acquisitions that have not yet started to add to the company's sales. YoY the actual number is almost a 20% decline, as seen below.

{kind=link}

Nonetheless, positives include excellent regional growth in NA, LATAM, EU and Africa/ME. Demand is continually strong, with most impacts coming from the roofing segment. The company's orderbook though, is well-filled. LATAM saw its 11th consecutive quarter of profitability, driven by Mexico, Colombia and Argentina with good projects and pipelines. Even anemic Europe saw strong performance, with margin expansion driven by non-commoditized high-value solutions, the same thing that Heidelberg is trying to focus more and more on. Africa and Middle East were excellent as well though, seeing significant margin expansion, a significant increase in alternative fuels, and a recovery in China visible overall.

There wasn't much negative to be said for Holcim for the quarter, and this is driving what is a good level and outlook for the company's full-year guidance.

{kind=link}

The issue for the company isn't quality or results - the issue for Holcim is valuation, which we'll get into in a bit here.

What I want to say is that with a near-40% gross margin, Holcim is really one of the highest-quality, highest-margin, and lowest debt (1.9x to EBITDA on a net debt basis) concrete businesses around. It's also Swiss, which I see as another distinct advantage. Its current dividend yield of around 4.2% is in no way bad and is actually at a 2-year high despite its valuation. The company's only negative trends that I could see from a high level are the issuing of long-term debt and an ROIC that's still lower than the average weighted cost of capital. but if you follow my articles on concrete companies, you'll know the calculations for the replacement value of existing assets, and why some of these calculations, given the replacement value, do not really make sense. It's the reason Heidelberg and Holcim are acquiring, rather than building new assets (or part of them, at least).

What we want to look at when it comes to Holcim going forward are really macro-level trends. The company, despite difficulties in part of the US markets, expects positive results in roofing. It's a complicated market, due to the company over the past few years seeing a shortage in specific feedstock, namely a plasticizer that's led to disruptions in supply. This has led to overstocking at the contractor level, as most simply bought what they could, knowing there was a disruption. This is now what's normalizing - still, results are expected to remain in the positive range for the company.

1Q is always the smallest quarter from the year - so the company's guidance update is actually worth noting here, and look at whether it's based on volume or margins (i.e. pricing). The company is on a positive cost-over-price basis in every single region, with costs peaking (as with Heidelberg) sometime during 3Q last year due to energy pricing, among other things. The takeaway I take from management commentary when it comes to this is that it is a mix of margin recovery from highs, as well as strong demand across multiple geographies.

The burden from the Ukraine war is nothing small - and there is inflation as well as a persisting higher cost of energy, and the European green deal, which puts export volumes at risk (not just for Holcim, but for all companies impacted by it).

CapEx is another thing we want to keep our eyes on. The current plan is 2B CHF planned on a forward basis. In this context, the investments in sustainability actually have very impressive returns in Europe due to the political and taxation landscape - which means we can already guide for how margins are going to increase in Europe once these are online. The EU has a huge decarbonization system with Carbon credits, and once Holcim fulfills this, it's a question of how quickly the margins will increase.

I have good expectations for the company's bottom line going forward, but at the same time, here are the issues I currently see for Holcim.

Valuation for Holcim - It's not all that great, unfortunately

You may like Holcim here, but unfortunately, there is a decent amount of downside to the stock. Given that the company is set to grow earnings no more than 2-3% per year in the next few years, you're betting, if you invest, on a quick realization of margin improvements as a result of the company's green investments. I believe these will take more time. The company currently trades at about 11.3x P/E. This is not "high" per se, but it's also above where the company has been most times for at least the past 5 years. Yes, the earnings profile is improving -but still.

The company is BBB+ rated, and it there's one concrete company between Heidelberg and Holcim that I would allow for a premium, it's Holcim without a doubt. But Heidelberg is (or was) a lot cheaper.

And, to be frank, I don't believe Holcim to be worth 16x Normalized P/E, which is what you'd want to look at to see outsized returns for the company here.

Analysts and valuation models for the company are fairly split, but I can see and showcase some of the uncertainty here. 20 analysts follow Holcim based on current trends and work price targets starting at 48 to 78.5 CHF with an average for the native HOLN ticker of 63.4 CHF. That's also 13 CHF higher than only 6 months ago - which I don't view as valid.

Working off projected FCF, P/S numbers in a segment context, graham number (square root of 22.5 times the multiplied value of the company's EPS and BVPS - a very conservative/defensive investment valuation method) and Peter Lynch fair-value formula, you get averages pointing to a PT of 50-53 CHF. Given where the company currently trades today, that would actually imply a modest overvaluation. It's not clear-cut to me - there's potential for the company to go higher - but it could certainly go lower as well, based simply on the headwinds and potentials here.

That's probably why 14 out of 20 analysts are at "HOLD", "SELL" or equivalent ratings and only 5 are at "BUY". It's for that reason, mixed with my own conservative view of the entire sector, that I say that anything above 55 CHF is too much for the business here.

I went "HOLD" before on Holcim with a conservative PT of 52 CHF - I'm not changing this at this time, and consider this company to be too expensive here as well.

Thesis

- Holcim is one of the most qualitative and interesting cement companies in Europe - together with peers like Heidelberg, which I view as almost equally attractive. It has a, 4%+ yield, and a good set of fundamentals, even if there is a risk to some of its asset profile.

- I no longer see Holcim as a "BUY" - and for this company, I'm saying it's at 58 in terms of PT, making it a "HOLD".

- Remember the high level you should be looking at here. Any Cement company such as this is a play on Urbanization. The fundamental trends ongoing around the world speak in the long-term favor of companies like Holcim - and that's why I invest in them. At least, at the right overall level.

Remember, I'm all about:

- Buying undervalued - even if that undervaluation is slight and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

- If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

- If the company doesn't go into overvaluation but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

- I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them ( italicized ).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside that is high enough, based on earnings growth or multiple expansion/reversion.

I don't see Holcim as cheap or as attractive enough to consider it a 'Buy' at over 58 CHF. It's a "HOLD" here.

For further details see:

Holcim: Concrete Upside In Concrete, But Beware Valuation