HDELY - Holcim: I Like Heidelberg More But Holcim Is Safer

Summary

- Holcim, together with Vicat and other concrete/aggregate plays in Europe, are the main alternatives to the giant that is HeidelbergCement, now known as Heidelberg Materials.

- The company has a better (by that meaning more modern, less emerging-market focused) asset base but also a smaller one. Still, some call Holcim safer than Heidelberg.

- I own and I like Holcim - but I like Heidelberg more.

- Here is my 2023 thesis for Holcim.

Dear readers/followers,

I've covered Holcim ( HCMLY ) before, and I will continue to do so. Substantial amounts of my investment portfolio are, after all, found in the basic materials space, and this definitely includes concrete/aggregates, which in turn also includes Holcim.

Holcim is a Swiss business - and that always gives a sort of air of quality - because who doesn't like Swiss businesses? Holcim is not problem-free - like its peers, it suffers from carbon costs and taxes, and it's not immune to operational challenges, but it also has a number of upsides not found in every one of its peers.

Since I last wrote about Holcim, the company has climbed faster than Heidelberg ( HDELY ). My Heidelberg position is up more because my cost basis is better, but Holcim has seen substantial 25%+ market outperformance.

It's a good example of why you should ignore naysayers when it comes to Europe, or why investing here at the right valuation should definitely "be done".

Holcim Article (Holcim Article)

Holcim - things look good going into 2023

Surprisingly, my work on Holcim has gone both underfollowed and underappreciated. I understand that coverage on EU businesses are a minor sort of thing here on SA, but it's still interesting when buying several businesses like Holcim has outperformed the market by double-digits, while much-covered work on massive companies resulting in negative double-digit RoR gets much more attention.

It's my hope that I can rectify this by pointing out again, just how good Holcim is, much like its peers.

Holcim is a multinational concrete/aggregate company. It has tens of thousands of employees and presences around the globe - scale is the only way to make this sort of thing work. Scale, scale, scale. If you don't have scale in this business, you can pretty much forget profit in today's market - that's how "bad" it is.

Holcim is what became of LafargeHolcim, a company that resulted from a merger of Lafarge and Holcim back in 2015. This combined merger at this time was one of the largest in cement ever. The company later changed its name to Holcim Limited.

Annual company sales are approaching 30B CHF, and the current market cap is more than that. The company's yield is currently 4.24%, and it trades at a P/E of 12.17x. This is higher than Heidelberg, but there's also the higher safety and quality that some argue the company has.

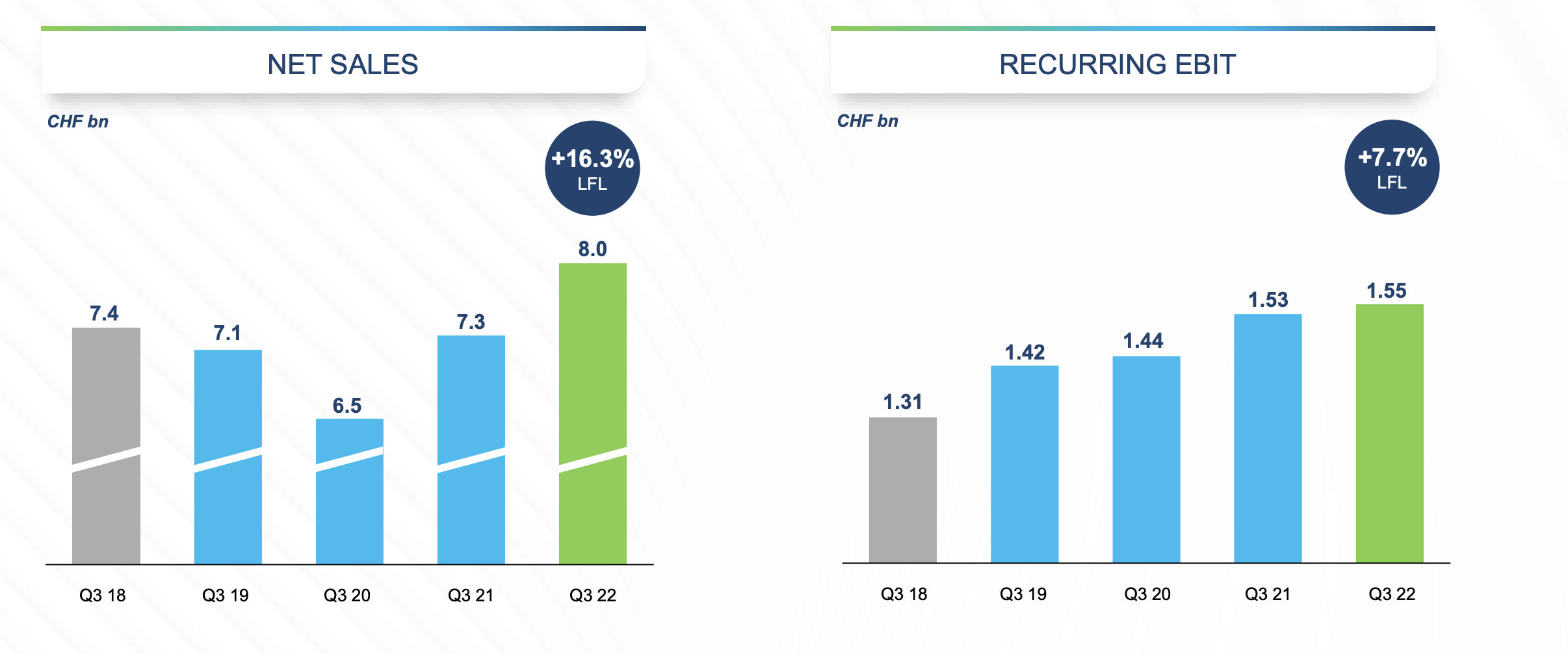

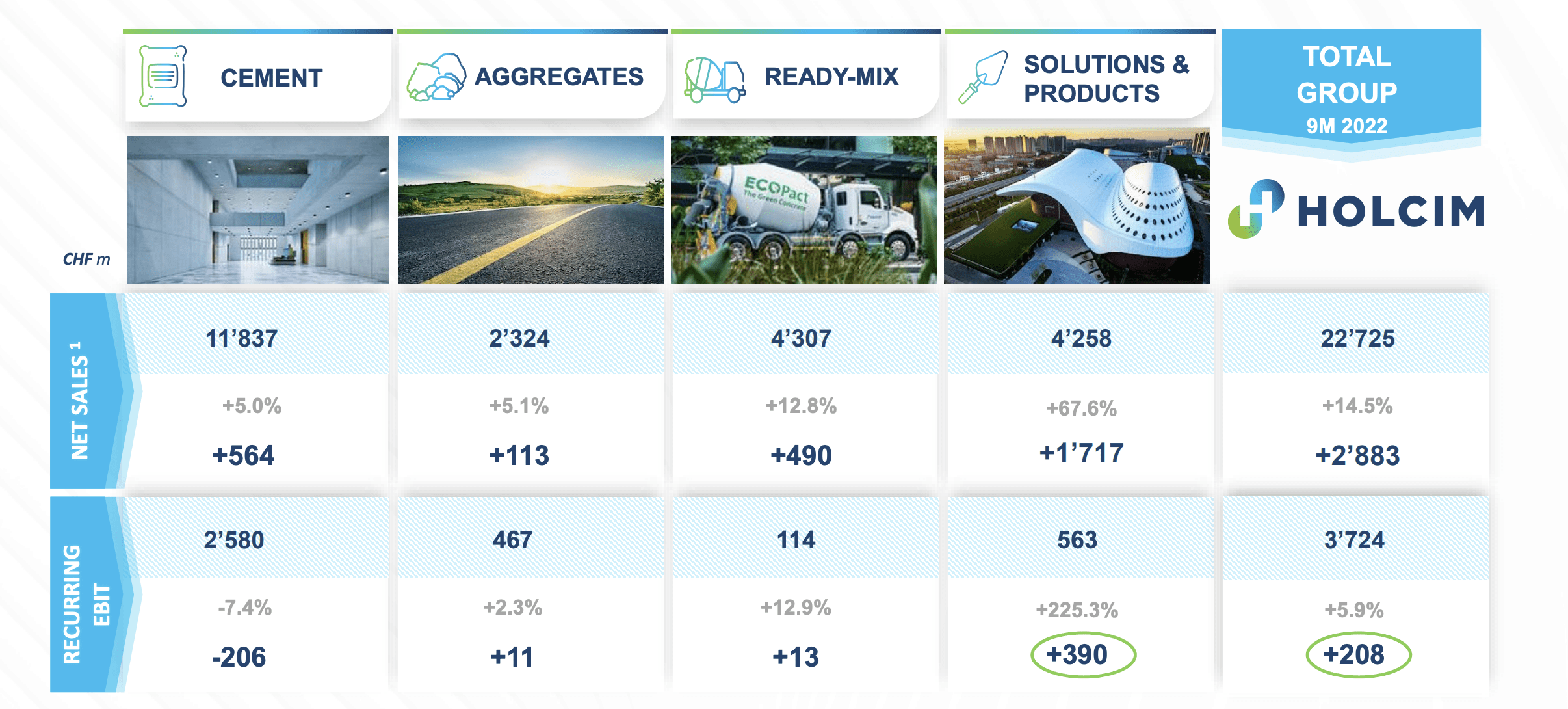

Holcim is a play on quality. It delivers a more stable performance than Heidelberg but also has a lower potential RoR going forward. Where Holcim shines is safe growth. The company saw net sales increases in the double digits, and EBIT increases as well - other concrete businesses are struggling with earnings.

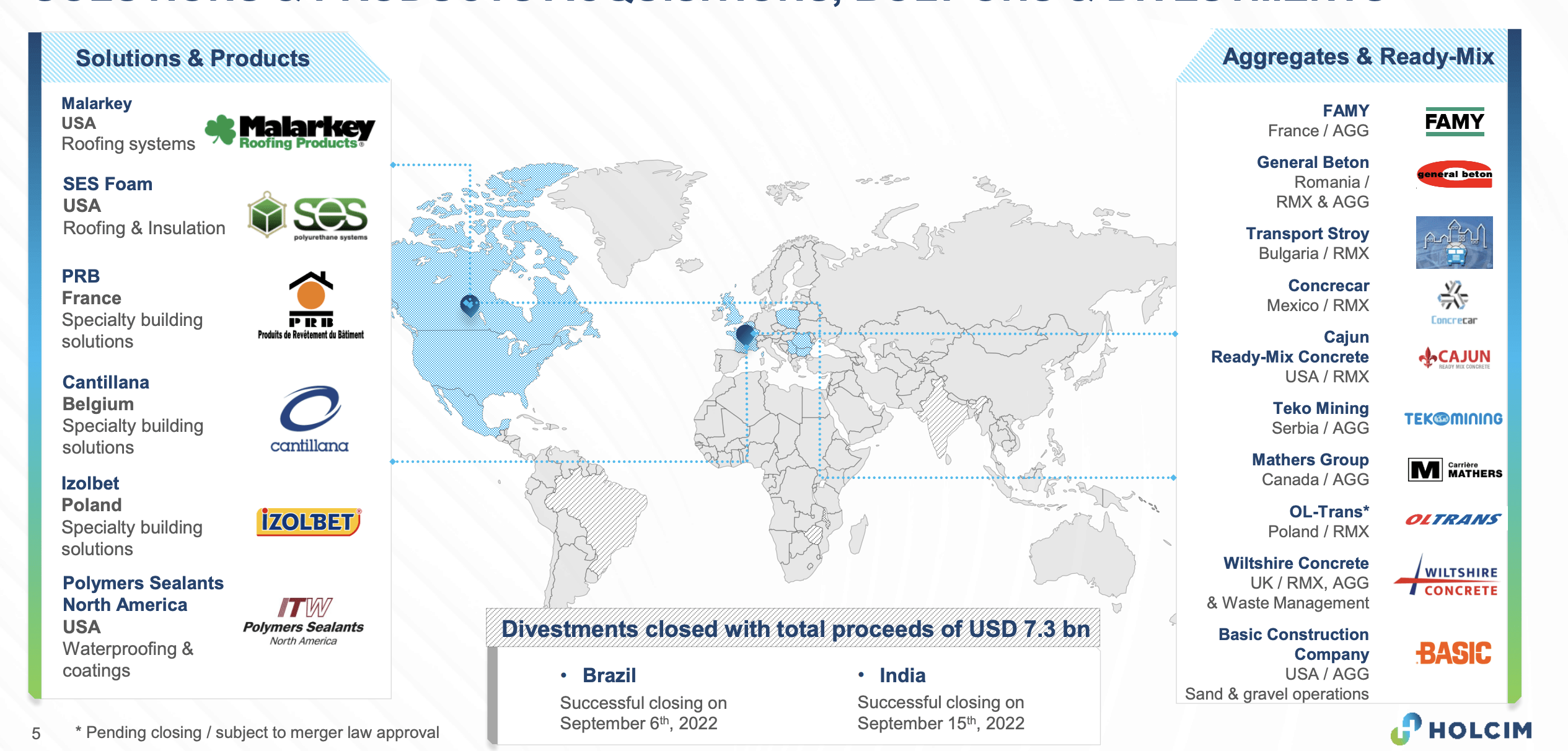

Holcim is currently transforming its portfolio, with M&A continually ongoing. 4 M&As for Solutions & products are signed, and another 10 bolt-ons for Aggregates and Ready-mix. Unlike Heidelberg, Holcim is moving away from what many concrete guys would consider the growth markets of the future - emerging markets like Brazil and India. I understand the volatility in these markets that might lead Holcim to do this, and that's also why I both own Heidelberg and Holcim - I want EM exposure, but I also like safety.

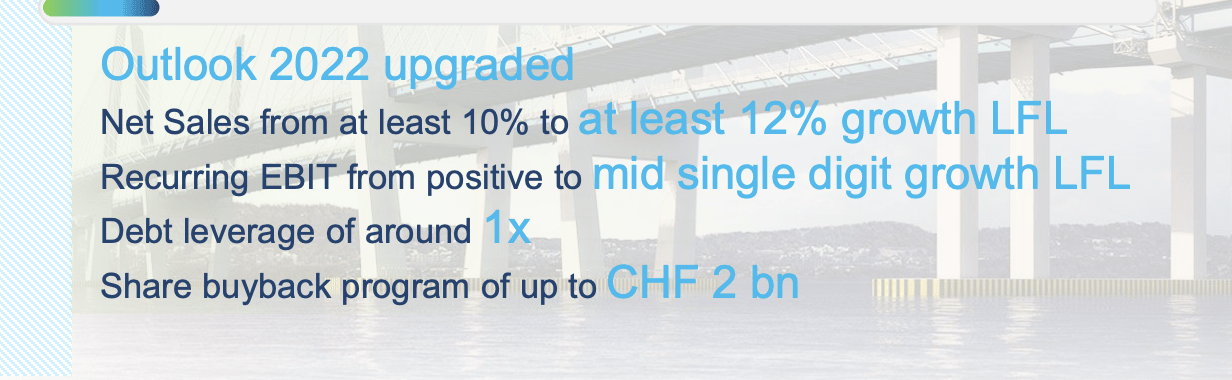

The company's 2022E outlook updated in 3Q22 mirrors the quality this company delivers.

{kind=link}

And if we were to look at the company's recent sales, and high-level pre-tax profit, there is a case to be made that Holcim is currently "better" than Heidelberg.

{kind=link}

I won't argue that Holcim is currently in a better position than Heidelberg - they are - but this is also because much of Heidelberg's business is still "percolating". We're in incubation there, with an upside that could see the company's share price potentially double in the next few years. The same, I believe, cannot be said for Holcim.

Nonetheless, Holcim manages one of the most attractive Concrete portfolios in the entire world. I've been looking at Heidelberg for Post-Ukraine-war upside, and I'm also looking at Holcim for the same deal.

{kind=link}

Holcim, due to not being carbon-dragged by ItaliCementi (which Heidelberg is) is ahead in its work in terms of transformation. The company's current cash conversion cycle is better, and it has less capital intensity. It's also far higher on ESG at this time, with many products like Facade, Insulation, Tile Adhesives and Roofing already brought-to-market, while HeidelbergCement is still mostly more in "basic" products.

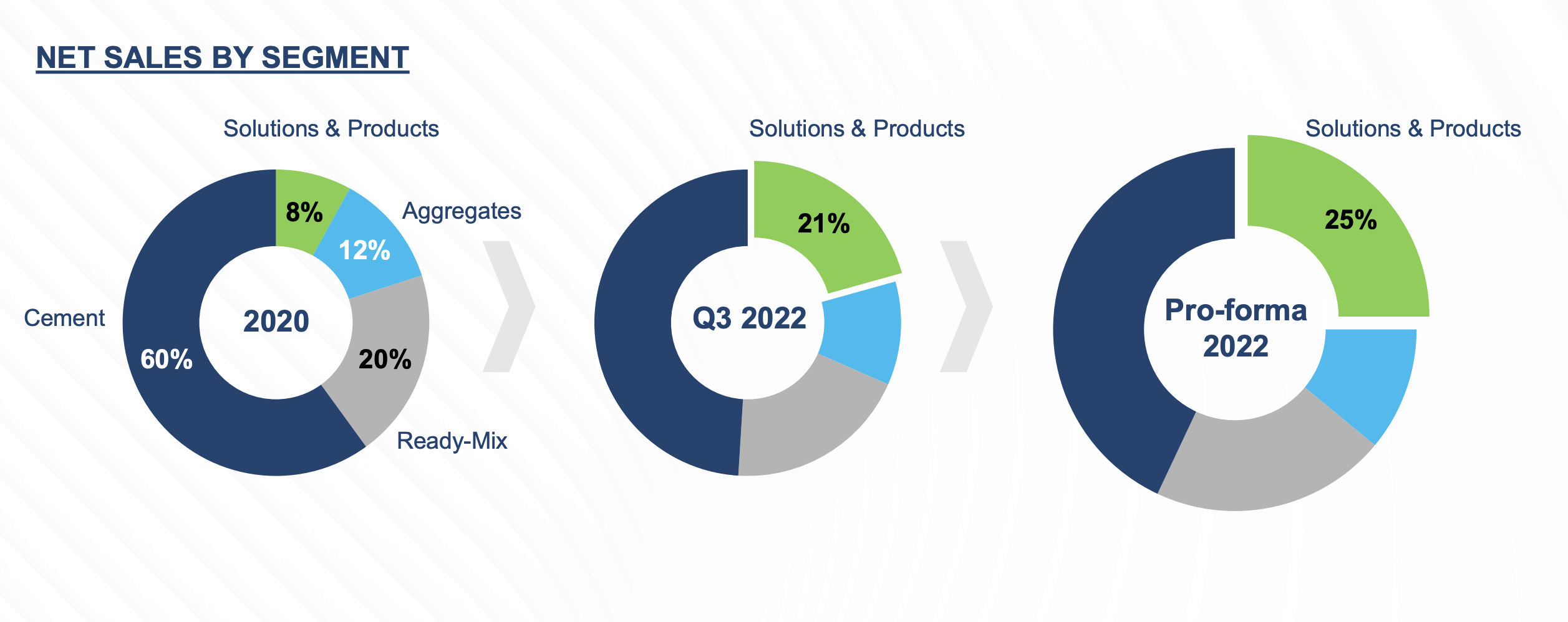

Take a look at the company's Solutions/products growth, and you'll be able to see what the company is aiming for, and the fact that it's currently working well.

{kind=link}

Holcim seems like a concrete company that's done everything "right", and indeed, I wouldn't argue much against this. But it's also, as we'll see in a little while, a company that's more or less reached its valuation where I believe it could go.

Remember, most cement production has been value-destructive for a very long time. I mean that on a ROCE (NOPAT+lease exp*(1-tax)/ net capital employed percentage) basis, the company is below its weighted average cost of capital ((WACC)) of around an average of 7.5-8%. ROCE is lower than 6% and has only recently climbed up closer toward the WACC, compressing the spread. Holcim had this issue much less than HeidelbergCement. As before, I won't invest in a cement company when ROCE is above WACC because it implies we're in an asset high-utilization portion of the cycle. The resulting implication is that when things turn back down, the stock will fall - and your returns go south.

Holcim, the way things are going, are going dangerously high in terms of their valuation. No matter how they dress things up or mix other products in, at its heart, it's still 75%+ a cement, aggregate, and ready-mix company. While its solutions are driving profitable growth, it does not make them immune from the trends on the market - as we see in the cement margins that we're currently playing with.

{kind=link}

The company may be transforming at breakneck speeds, but time will tell if this is advantageous (moving out of LATAM), and gaining much more of an NA focus, going from 24% to 40% NA in Pro-forma 2022. Like Heidelberg, the company focuses much on its sales and volume growth, but its leaving LATAM behind (for the most part), does not take away from its challenges in other areas.

China anyone? Because APAC is seeing massive lockdown and inflation impacts, resulting in negative price over cost and a full -53.9% EBIT drop. Much of the negatives are being weighed up by Holcim's pushes into Solutions, but we cannot let the negatives or risk being "paved over" here.

The company is buying back and has a very strong balance sheet, a good dividend, and solid fundamentals overall. I have no worries here with regard to Holcim, and that is why I am keeping my shares at this time.

However, this is also where we start running into some "math problems" and other problems. Let's remember a couple of things in the "risk" portion of the company.

Previous/partially current management was positive about their Lafarge/Holcim M&A. This proved to be flawed, on several levels. The comparative lower margins and profits at Lafarge, coupled with higher leverage as well, proved to be one of the most value-destructive mergers in the sub-sector ever recorded.

The combined company has been at a disadvantage because of this. Furthermore, initial management targets of cost-savings, cumulative FCF, and CapEx as well as supposed high dividend increases over time proved to be little more than dreams. Management didn't account for downside risk. The risk is that we're seeing similar trends with these latest moves, where they essentially overfocus/quickly shift to products and solutions, and leaving entire geographies behind, divesting decades' worth of asset investments at below-replacement prices. This is the entire reason why cement companies are attractive, to some extent.

Let's look at what the main problem is here at the moment though.

Holcim is starting to look fully valued after a 25%+ outperformance

As before, valuing Holcim is similar to valuing HeidelbergCement.

I'm still applying a sales growth rate of close to GDP with EBITDA heavily impacted by increased CapEx due to things like Carbon costs (they're up 200% in 2021 alone), and energy costs rising, it's not fair or accurate (in my mind) to expect a whole lot of growth out of Holcim. This also really hasn't materialized. Some growth, sure - but not as much as out of peers. DCF is still looking conservative, with a 1-2% sales growth expectation, and I'm not changing that to reflect any changes due to the portfolio re-orientation that the company is doing.

S&P Global calls for valuation ranges of 38 CHF up to 64 CHF, coming to a current average of 52 CHF. This is a significant impairment compared to the previous valuation targets for the company, which were essentially 10 CHF higher. This also means that at current share prices, the company is 0.9% overvalued, or we can simply call it "fair value" here.

I apply a 10% discount to Holcim for some of the risks mentioned here, but I still consider weighing these at fairly heavy amounts. My previous price target, conservative, for Holcim, was 60 CHF. I'm shifting it somewhat here. I believe the move upwards for Holcim together with its portfolio shift, and compared to peers, a group which includes Heidelberg, Taiwan Cement, Vicat, Vulcan and other materials companies, shows the premium Holcim is demanding to other cement companies. Holcim native is at 11.9x NTM P/E, Heidelberg is below 8x, with Anchui Cement at around 9.8x, and ancillary CRH PLC at around 12x. Given the premiumization of the company, I would argue that Holcim is starting to look more and more fully valued.

I'm not shifting my PT here. I don't shift my PTs, due to how they are calculated unless something material has changed in the company. Nothing I've seen in 3Q22 is anything I have not previously accounted for or commented on. I'm not a fan of the company deciding to leave India or Brazil. I like their focus, but I worry about their degree of refocusing - I believe Heidelberg is handling this more qualitatively, and the way Lafarge and Holcim merged gives me some ground to stand on, in terms of my thesis.

Here is my current thesis for Holcim.

Thesis

- Holcim is one of the most qualitative and interesting cement companies in Europe - together with peers like Heidelberg. The company is solid enough to have beaten the market by 25% since I wrote about it last. It has a high, 4%+ yield, and a good set of fundamentals.

- However, the climb means that the company is more and more fully-valued in context to the overall sector. Holcim is more qualitative in terms of its assets than Heidelberg, but Heidelberg has significantly more growth potential.

- I still see Holcim as a "BUY", but I see HeidelbergCement as the company with a significantly higher upside here.

- Remember the high level you should be looking at here. Any Cement company such as this is a play on Urbanization. The fundamental trends ongoing around the world speak in the long-term favor of companies like Holcim - and that's why I invest in them. Very long term, just making sure that I'm buying them at the "right" time of the cycle.

- PT for Holcim is 60 CHF - that makes it a "BUY".

Remember, I'm all about:

- Buying undervalued - even if that undervaluation is slight and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

- If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

- If the company doesn't go into overvaluation but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

- I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them ( italicized ).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside that is high enough, based on earnings growth or multiple expansion/reversion.

The one problem is that the company is no longer cheap - aside from this, Holcim is still a "BUY".

For further details see:

Holcim: I Like Heidelberg More, But Holcim Is Safer