HCMLF - Holcim: Less Optimism About Real Estate We Are Now Neutral

2023-08-06 00:20:44 ET

Summary

- We lower our estimates on Holcim on the back of a real estate slowdown.

- The Solutions & Products division reported a negative sales and earnings trajectory.

- Holcim is now trading in line with our EV/EBITDA target multiple. The company looks pricey, and we move our rating to a neutral one.

Since 2022, Holcim ([[HCMLF]], [[HCMLY]]) has been Mare Evidence Lab's top pick. Our buy rating was supported by favorable tailwinds such as 1) higher government infrastructure spending (both in the USA as well as in the EU), 2) supportive acquisitions to diversify Holcim's business with a Multiple Arbitrage opportunity thanks To Firestone ((USA)) and Durolast ((EU)) acquisitions, and 3) a solid balance sheet with lower volatility thanks to disinvestment in emerging markets. Including Holcim's generous dividend, we reached a total return of almost 45%, outperforming the S&P 500. While we believe the company is moving in the right direction, we are also concerned about the Concrete, Cement, and Ready-mix segments. In addition, for the first time, the Solutions & Products division Q2 top-line sales dropped by 9%, and the core operating profit declined by -23%.

As a reminder, in our 2025 estimates, we anticipated how the Holcim revenue forecast was driven by the Solutions & Products division. We explained how " this was a segment that offers an above-market growth rate with lower cyclicality compared to the commercial real estate. " This was one of Mare Evidence Lab's supportive critical investment thesis and an earnings growth driver in the total company's EBIT development. We now believe that Holcim's valuation looks full, and so we are rating the company with an equal weight valuation of CHF 62 per share vs. our previous valuation of CHF 67 per share ($14.5 in ADR).

{kind=link}

Mare Past Analysis

Here at the Lab, we are cautious about the Real Estate sector. We believe the industry is moving toward cyclical headwinds with higher interest rates, lower access to credit, and declining GDP estimates. In the USA, 10/20% of the workforce is still not back in the office from the pre-pandemic level. In detail, the sector encompasses various end-market such as commercial, residential, retail, and industrial properties. As we all know, real estate is a significant driver of every country's economy and directly impacts various industries. Holcim is one of the largest global cement, concrete, and aggregate producers, directly linked to the real estate market performances.

Q2 results

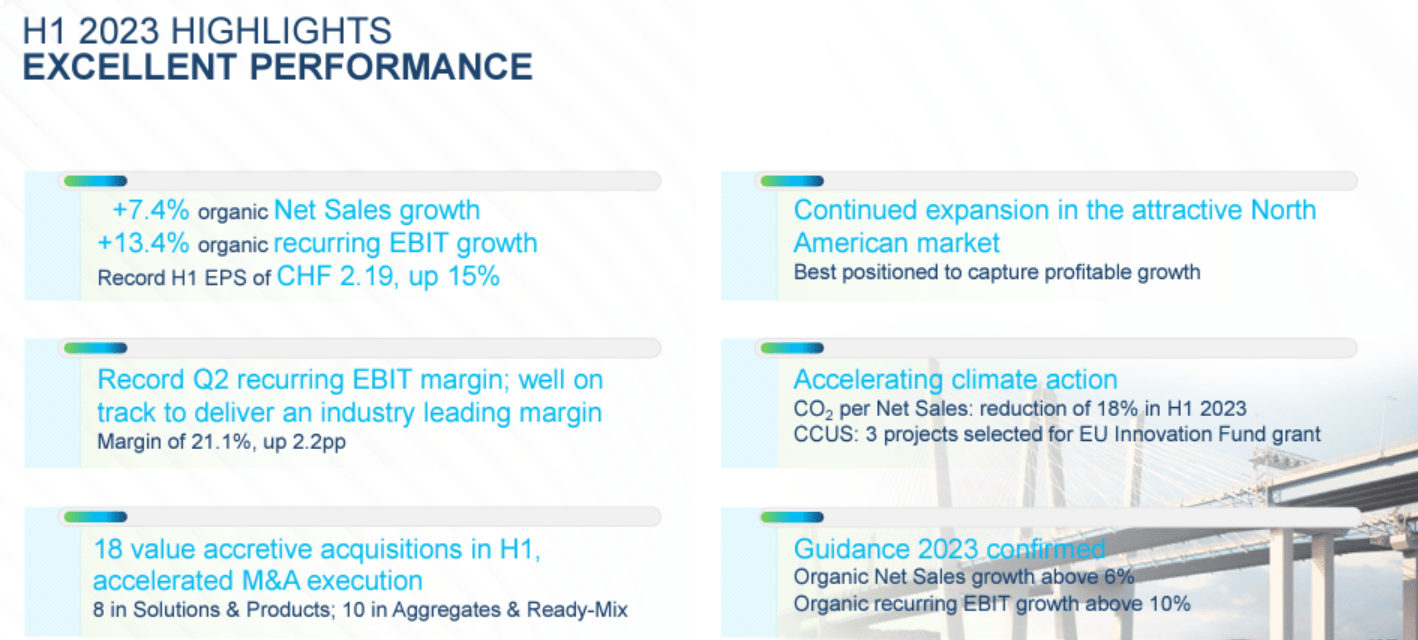

All in all, Q2 results were decent. Q2 top-line sales increased on a like-for-like basis by 7%, with a recurring core operating profit up by 13.9% to CHF 1.55 billion. Cross-checking Wall Street estimates, the company's EBIT margin misses slightly the EBIT growth. On a reported basis, sales and operating profits were down due to India disposal and negative currency evolution. Going down to the P&L analysis, net profit fell by 2% to CHF 1.28 billion. The company's positive benefit was from lower interest charges and Holcim adj. EPS increased by +3.7% to CHF 2.22. The ongoing share buybacks also supported this.

{kind=link}

Holcim Q2 Financials in a Snap

Source: Holcim Q2 results presentation

Changes in Estimates

- Net debt was higher than expected, reaching CHF 11.1 billion versus our H1 forecast of CHF 10.7 billion. In our assumption, we anticipate an ongoing de-leverage with net debt of CHF 7.8 billion at year-end (previously, it was estimated at CHF 7.6 billion);

-

The company is now guiding 6% turnover growth with a plus 10% on recurring EBIT growth. Our estimates previously forecasted an EBIT margin growth of plus 12.5%. For this reason, Holcim now foresees a 2023 core operating profit margin of 16%, and we align with the company's management. Before, we anticipated an H2 2023 EBIT margin of 17.4%;

- The company decided to re-segment this quarter and is now splitting out the Solutions & Products division. Despite a marked improvement compared to Q1, clients' de-stocking activities are not over. This division reported sales were down by 9%, and also the core operating profit significantly declined;

- Considering the disposal activities, we are guiding sales of CHF 27 billion for the current year with an EBIT of 16.5%.

Conclusion and Valuation

Considering the H1 results, we believe that Wall Street analysts will likely price lower earnings, and we might see modest downgrades, mainly if the roofing division will not perform in H2. Here at the Lab, we decided to leave our EV/EBITDA multiple unchanged , which is set at 6.5x and higher than competitors thanks to Holcim's roofing earnings diversification and higher profitability. For this reason, we arrived at a target valuation of CHF 62 per share. The company is currently trading with an EV/EBITDA of 6.6x. Therefore, we are now neutral on the next twelve-month visible period. Downside risks include raw material inflationary pressure, negative FX evolution, changes in regulation, especially at the ESG level, rising interest rate, and real estate slowdown.

For further details see:

Holcim: Less Optimism About Real Estate, We Are Now Neutral