HCMLF - Holcim: This Great Company Is Slowly Becoming More Attractive (Rating Upgrade)

2023-10-23 11:49:32 ET

Summary

- Holcim has shown strong performance and growth potential, with higher quality assets compared to its competitor Heidelberg.

- The company is considered one of the "greenest" concrete companies, which is an advantage in the ESG-focused market.

- Holcim is expanding in the US and expects net sales growth above 5% and organic EBIT growth above 10% for the year.

Dear readers/followers,

Few of my investments have been as successful this year as Holcim ( HCMLY ). By this I mean that the company has almost perfectly followed the trajectory implied by my stances over the past year or so. I started out with a bullish recommendation at the onset of 2023, which has outperformed the index to date - but I then went neutral, and those have underperformed the market, with the latest neutral recommendation seeing a double-digit decline in share price on the part of Holcim, more than 10% compared to the S&P500 which is down around 6.4%.

Seeking Alpha Holcim (Seeking Alpha)

This is an update on Holcim, compared to my latest article with a "HOLD" rating which you can find here.

In this article, I'll provide you with an update on the company, and why I am starting to keep a closer eye on the business here. Holcim, like any concrete business, is a play on the replacement value of its production assets. Like its competitors, this is where Holcim shines, and Holcim has a higher quality in its assets than competitor Heidelberg (HDELY) has.

I am "Long" Holcim, but I have not been adding for some time - the time may be coming for when this changes.

Here is why.

Holcim - The upside is slowly materializing for me

If you follow my work, you'll know that I'm one of the contributors not shy about telling you when I'm buying, but also when I am rotating. I have no fear of exiting a positive investment "too early", and whenever I go into an investment, I have an "exit" target as well, though sometimes those targets can be extremely lofty. This also means that I'm not shy when it comes to essentially ignoring businesses in favor of others due to their inherent valuation - or lack thereof.

Concrete investment is something that I consider fundamentally attractive because I don't see the technology going anywhere. For the foreseeable future, and likely for as long as I'll be around, I see this as timeless. These materials are easy to manufacture, but inefficient to transport.

This means that concrete production is going to be as close as possible to the end-users because you do not want to pay containers or ships or any sort of large-scale logistics to transport what amounts essentially to powder made up of limestone ore (and certain additives) for long distances.

You may not like Concrete - and indeed, the technology isn't exactly the ESG-friendliest sort of business, but it's hard to argue the timelessness or the demand for it.

However, Holcim has advantages here, because when it comes to ESG, Holcim is actually one of the "greenest" concrete companies around that you could invest in. This is naturally, quite an advantage.

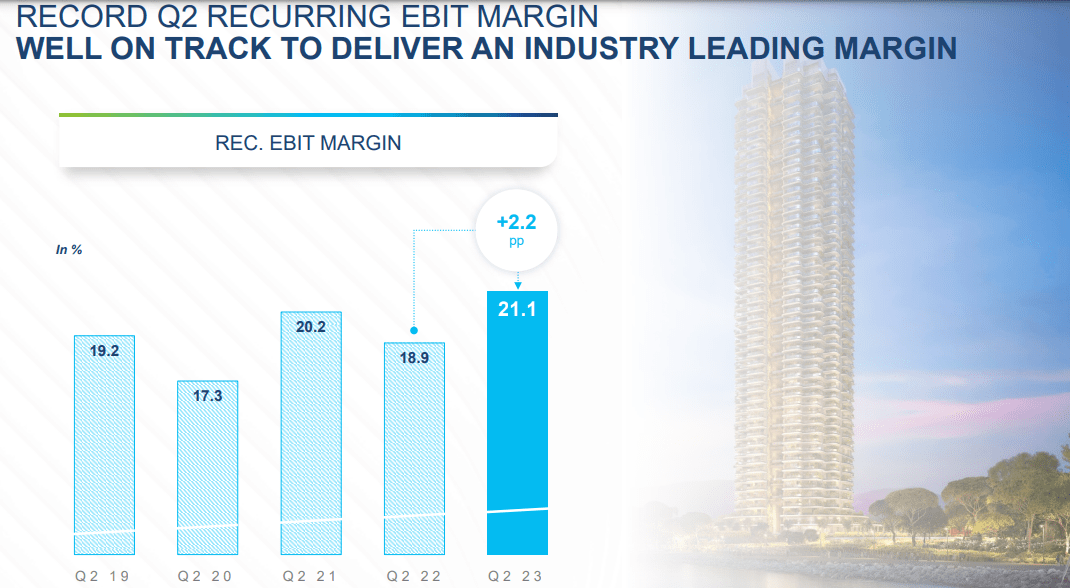

Also, despite what you see in the company's recent result trends, the company is actually doing better than you might expect. The latest results we have to consider are 2Q23 or half-year results, and the company saw over 7% net sales growth, over 13% recurring EBIT growth, and a record EPS, despite a complex infrastructure and industry situation.

In fact, Holcim's EBIT margin, that being the pre-tax margin, is now 21.1%, which is industry-leading. This is worth mentioning for sure.

{kind=link}

Holcim is also considered to be a very "hungry" business, by which I mean that it buys other concrete businesses at a rapid pace. In 1H23 alone, the company completed 18 value-accretive acquisitions through accelerated M&A executions, taking advantage of the current market environment and the uncertainty to strengthen its portfolio.

Holcim is expanding in the US, and is probably, as I see it, one of the best-structured concrete businesses to take advantage of an unstable market and capture growth. The company fully expects a 5%+ net sales growth for the year, and organic EBIT growth above 10%.

{kind=link}

I have historically been a far heavier investor in Heidelberg than I have been in Holcim. This has been due to the reversal potential in the former being far stronger than in the latter. That is, as I see it, no longer the case. Heidelberg has played its valuation card for now, and now I'm looking for a possibility to get deeper into Holcim.

The company continues to invest in capacities and products, as well as acquisitions, focusing on finding small and mid-sized local players that generate 5% or above in net sales growth per year over time, with a focus on EU and NA, trying to transact in mid-single digit EV/EBITDA multiples. The current environment makes this all the more possible, as proven by this half-year.

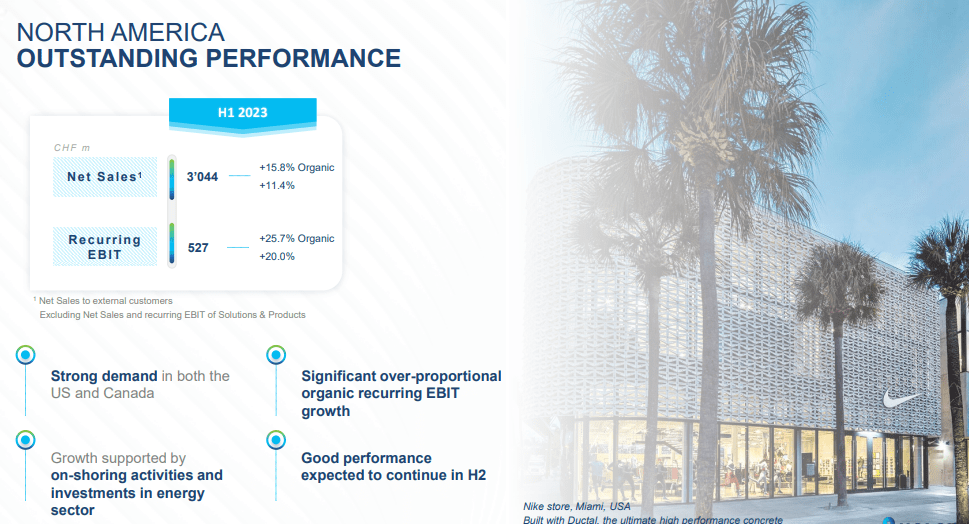

The company's attractive expansion in NA also continues, and the company is on track to generate 40% of the group sales from the geography in 2023E, which is a significant expansion in a relatively short time from a split that remains relatively EU heavy - but becoming more and more NA dominant.

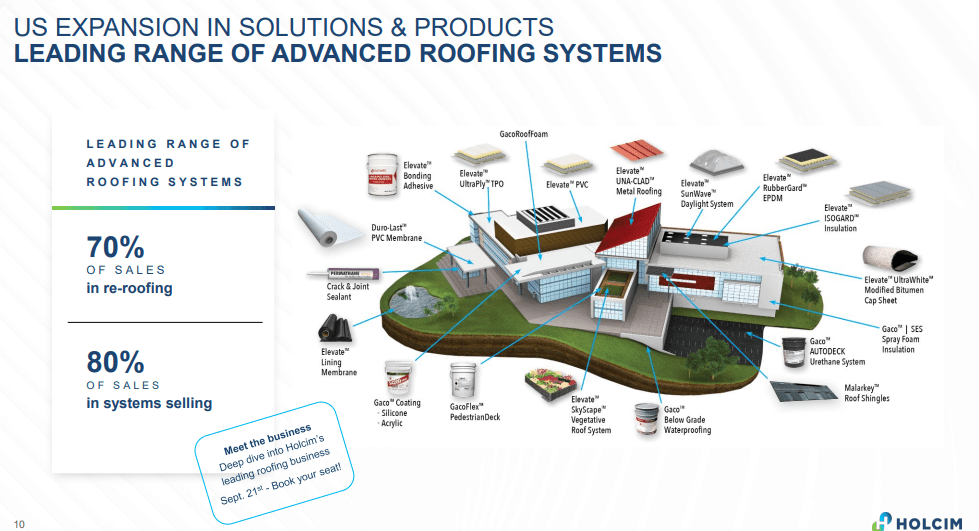

Heidelberg is better and larger in certain areas. Aggregates and ready-mix aren't somewhere where Holcim shines yet. But it's the leader in Cement, and it's the leader in commercial flat roofing, and compared even to Heidelberg, I believe Holcim now has the more attractive growth profile. The expansion in roofing and solutions has been remarkable to say the least, and Holcim now has a 20% market share across all US commercial flat roofing - that's a fifth of the entire market (Source: Holcim), as well as being #5 in residential roofing.

When it comes to this technology, the company does quite a lot.

{kind=link}

At the same time and despite this significant growth, Holcim has been able to actually cut down its CO2 on a per-million of net sales, by more than 18%. And this isn't across a 5-year period, this is one year. Since 2020, the company has cut Co2-per million by close to 40%, showcasing just how much is possible with the right mix of ambition and follow-through.

I'm typically not that interested in Co2-trends, as you may know, but in this case, the Co2 of a concrete company is directly tied to costs due to certain tariffs, especially in the EU. (more information in some of my earlier articles on Heidelberg).

The way that I view the most recent set of results is that we're seeing a discounting due to the risk-free rate rising significantly, and Holcim not really holding up in comparison to this. However, Holcim has reported excellent trends and good growth potential.

The only even somewhat declining sector turns out to be solutions & products, and this is not an overly large part of the company's overall mix. The highlights for the company by far outperform any problems here, with North America standing as a strong example of company outperformance.

{kind=link}

Even in Europe, where we've seen issues over the past few years with many companies, company trends are holding very strong, with good overall increases in profit, and a strong expected 2H for the company.

What was the reason for the weak half in Solutions & Products? Well, if you remember there were some very strong quarters before this due to stocking - these destockings and inventory rationalizations are now completed - so the company expects a full positive reversal for the sector in 2H. With continued positive expectations both in the core sectors and in solutions & products, I don't view much as "going wrong" when it comes to Holcim.

For that reason, let's move to valuation and see where we can start buying the company.

Holcim - A solid company with a good upside, at the right price

In my last article, I said "HOLD" until the company hits about 58 CHF per share. The company is currently trading at close to 55 CHF. That means per definition, the company is now a "BUY", and I am indeed changing my rating to "BUY" as of this piece.

Holcim has also clarified further portions of its growth trajectory. Not only am I going "BUY", I'm now raising my PT to 61 CHF to account for the better upside we now see in Holcim - and yes, this is despite the comparatively lower yield that the company offers. Remember, this company is BBB+ but now offers us less than 4.6% yield, which is below the going market rate.

But this is made up by significant growth potential.

Even if we assume that the company sticks to its 10x P/E that we currently have, and these forecasts materialize, you're getting 12.38% per year in growth, or almost 30% per year until 2025E. However, any upside beyond 13-15x P/E which would be closer to where the company "should" trade, then we're getting up to a 30% annualized, or 80% in around 2-3 years from this company - and that's massive for a BBB+ rated concrete business.

So, I say the time has come to be long Holcim. The company may go lower than we're seeing today - and then I'll add more. I'm now starting to establish a position here, and I believe you could do so as well.

Here is my going thesis for Holcim as of this latest report and update in October of 2023.

Thesis

- Holcim is one of the most qualitative and interesting cement companies in Europe - together with peers like Heidelberg, which I view as almost equally attractive. It has a, 4%+ yield, and a good set of fundamentals, even if there is a risk to some of its asset profiles.

- I'm raising my price target as of this article, now considering it a "BUY" with a long-term price target of 61 CHF/share.

- Remember the high level you should be looking at here. Any Cement company such as this is a play on Urbanization. The fundamental trends ongoing around the world speak in the long-term favor of companies like Holcim - and that's why I invest in them. At least, at the right overall level.

Remember, I'm all about:

- Buying undervalued - even if that undervaluation is slight and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

- If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

- If the company doesn't go into overvaluation but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

- I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them ( italicized ).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside that is high enough, based on earnings growth or multiple expansion/reversion.

I now see Holcim as cheap or as attractive enough to consider it a 'Buy' with a PT of 61 CHF/share.

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

For further details see:

Holcim: This Great Company Is Slowly Becoming More Attractive (Rating Upgrade)