HCMLY - Holcim: Upside In Concrete Long-Term But Near-Term Problems

2023-04-20 00:28:00 ET

Summary

- The concrete/aggregate industry has seen some very good results in the past few years. Holcim results are up by over 40% in a single year in adjusted EPS.

- However, this outperformance and the exuberance masks potential near-term problems. 2023E earnings are likely to go lower, and there is reason to be careful.

- I'll show you why I'm cautious about Holcim and other Concrete businesses, and am close to considering this one a 'Hold', not a 'Buy'.

Dear readers/followers,

By this time, you know that I'm a big investor in things Concrete and aggregates - with major investments in companies like Heidelberg Materials ( HDELY ) but also Holcim ( HCMLY ). I like these companies - because their business models are relatively simple to understand. The companies provide products and services that do not do well if they need to be transported long distances. They also have asset efficiency and profitability problems due to energy costs and the dirtiness of the assets in context. But at heart, these companies provide something that's not only necessary, but it's also crucial for almost every part of the infrastructure.

So, doing away with Concrete is not something I view as realistic at any one time in the near future. These companies provide a very decent yield, a good safety - at least if you're willing and able to "ride the rapids" of this company's and the sector's ups and downs - because it's volatile.

Updating on Holcim

What I like about Holcim - except not being able to trade it natively given issues with the Swiss Stock Exchange - is mostly everything. Holcim has a different asset profile than Heidelberg, somewhat newer here. In exchange, it can't (yet) produce as cheaply as Heidelberg is currently able to do, and Heidelberg has, frankly, a somewhat better set of fundamentals.

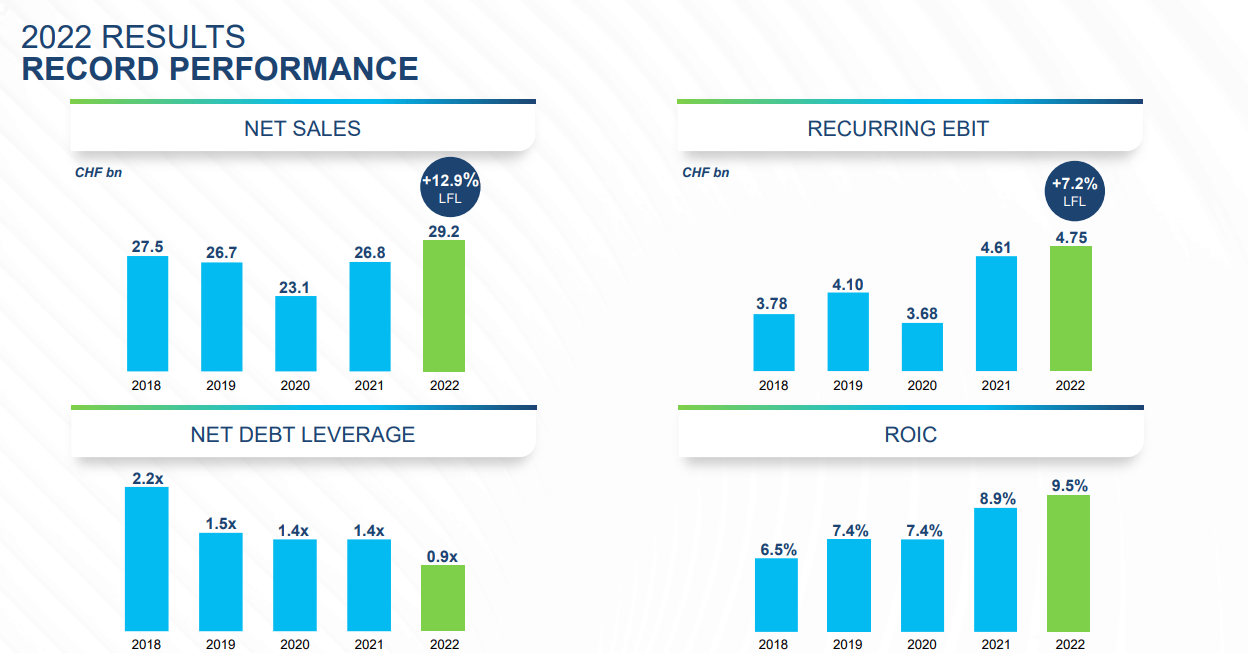

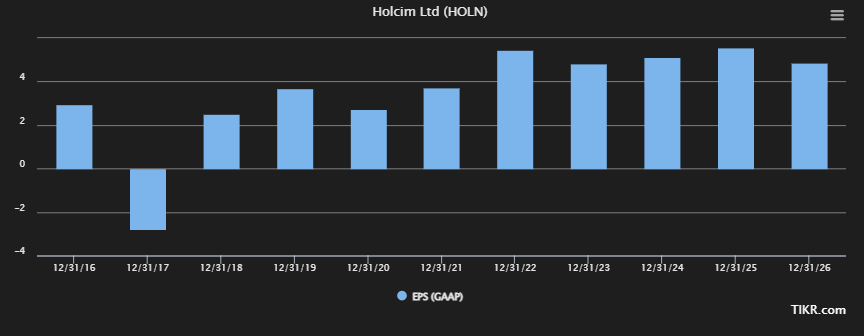

The company both had record or superb 2022 performances. What worked for Heidelberg also worked for Holcim. The company recorded record net sales of nearly 30B CHF, a 13% LFL YoY growth, and recurring EBIT of close to 5B CHF, up 7.2%. EPS grew by more than 20%, and ROIC inched up to 9.5%. The company's outlook for 2023 is somewhat more positive than HeidelbergCement - the company expects further growth (I do not), and movement forward in its transformation (which I agree with).

{kind=link}

Like Heidelberg, Holcim is trying to inch close to a Solutions/products-oriented sales mix. This transformation is going well. 19% of net sales are now coming from these sectors, and the company also managed an expansion into NA, which at this time represents 35% of the group's sales. Holcim also managed 6 value-accreditive M&As, and some good bolt-ons as well, which all resulted in the bottom line of accelerating its Co2 output in terms of net sales by 21%.

Concrete companies like Holcim need to be focusing on exactly this, because of the way Co2 in the EU is going to be taxed going forward. That's also one of Holcim's advantages - it's in a better Co2 position compared to HeidelbergCement, which through its Italcementi M&A has a whole host of somewhat dubiously-attractive producing assets.

Much of the company's assets, compared to Heidelberg, aren't yet "shining". As I said, its peer Heidelberg is not only equally fundamentally safe, but it's also more profitable and at a similar valuation in terms of overall appeal. That could make it a relatively easy choice which of the companies is more attractive here - but Holcim is more future-proof when looking at its assets.

Holcim, in many ways, is considered "less" qualitative than HeidelbergCement for its near-term earnings potential. What's more, an Altman-Z score check shows us that Holcim is considered in distress. While this method really isn't considered indicative to forecast bankruptcies anymore, a poor Altman-Z score is not positive, and this one is currently 1.69. Also, unlike HeidelbergCement, Holcim has had a few more negative and challenging years.

{kind=link}

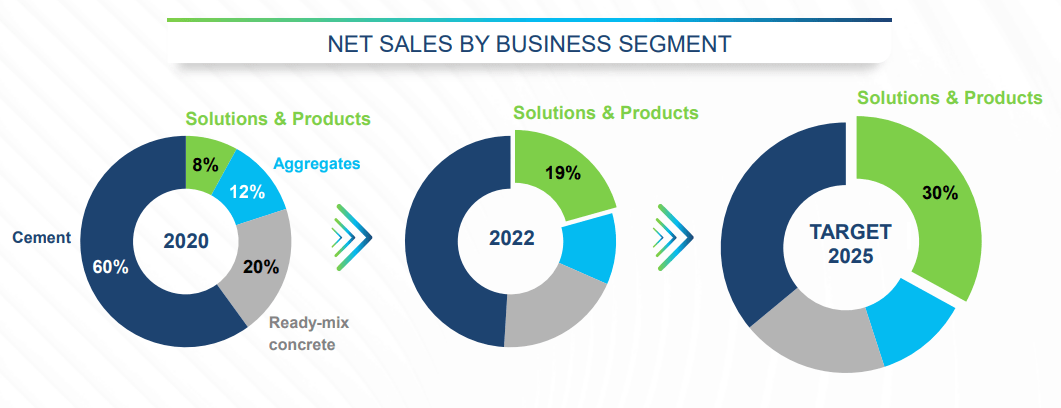

However, Holcim's upside going forward is clear. Just look at the mix development for the company in only a few years.

{kind=link}

Holcim is set to become one of the most diversified and appealingly mixed businesses in this segment within only a few years - and this is not a small thing. This includes things like roofing, insulation, tile adhesives, and facade products, such as wall systems. Advantages here in this segment?

A few.

{kind=link}

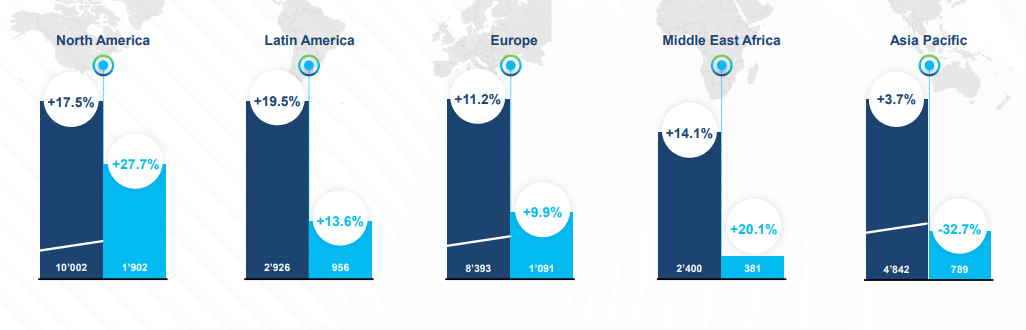

What's more, Holcim is actively targeting to become more NA-centric. In 2019, 23% of sales were NA - now it's 37%, with a 40%+ target in only a few years. Whenever a company like this does this sort of shift, there are some significant risks - so we want to keep a clear focus on quarterly results for any sort of troubles or challenges. So far, and in 2022, no real indications of any major troubles. All segments were up, and NA especially saw outstanding performance due to the ongoing transformation.

{kind=link}

FCF was at record levels for the year, and while we're not at a net cash position, the company's debt is down from around 10B to 6B CHF - vastly improved. The company also took the opportunity to increase the dividend to 2.5 CHF/share, which comes to a very impressive 14% increase. That's significantly higher than Heidelberg and other peers in the sector for this year. This payout is also not subject to Swiss withholding tax , because it's paid out of the company's foreign capital contribution reserve.

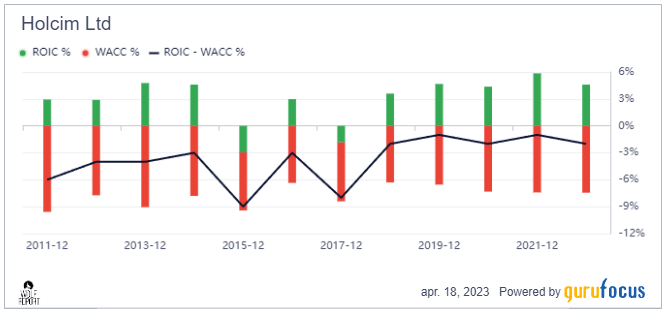

In my last article, I made it clear that I like Heidelberg more - but Holcim is safer. Remember, most cement production has been value-destructive for a very long time. I mean that on a ROCE (NOPAT+lease exp*(1-tax)/ net capital employed percentage) basis, the company is below its weighted average cost of capital [WACC] of around an average of 7.5-8%. Look at the company's profitability development - once again, Heidelberg is slightly better here.

{kind=link}

The main problem about Holcim is that the company, when it M&A'ed with Lafarge, was positive about this prospect, much like Heidelberg with Italcementi. Unlike the latter, Lafarge margins were lower, and the company's leverage was higher - and this proved to be a very value-destructive merger. This is something Holcim is still battling with, and I expect the next few quarters and 1-2 years to continue that trend. In my last article, I called Holcim to be essentially fully valued.

This has worsened materially since that article because macro has changed somewhat - and my expectations for Holcim are now different.

Like Heidelberg, this means that while I see some continued upside, I would be cautious.

Holcim - The upside is limited

So, my stance for Holcim is that the company is essentially fully valued here. How so?

A few reasons. First off, because I believe Holcim is likely to see significant earnings pressure on top of what the company is already seeing in its profitability. Earnings going into 2023E are expected to drop close to double digits. In terms of pure share price, the company hasn't been valued this highly for close to a decade. Even if Holcim is seeing improved earnings levels compared to 2016 and thereabouts, this doesn't equate to the company trading at a significantly higher multiple. Historically, Holcim has traded at a high premium - close to 19x. For a cement/aggregate company with the troubles brought on by Lafarge, I don't believe this to be justified. Even more, I don't believe it to be justified for a business that's expected to grow no more than 2-3% on average for the next 2-3 years.

I'm still applying a sales growth rate of close to GDP with EBITDA heavily impacted by increased CapEx due to things like Carbon costs (they're up 200% in 2021 alone and are expected to grow further), as well as rising overall energy cost. I said so in my last article, that beyond 2022, it's not fair to expect a whole lot of growth out of this - or indeed, any of the cement companies out there.

DCF is still looking conservative, with a 1-2% sales growth expectation, and I'm not changing that to reflect any changes due to the portfolio re-orientation that the company is doing. If we use an EPS DCF with the assumption of 2-3% growth for 10 years, and 1-2% with the terminal rate using a reverse DCF model, we get an implied share price range of 50-55 CHF. The company is currently trading at 58.4 CHF.

S&P Global analysts are slightly more positive about the company. From a low of 49 CHF to 78 CHF on the high side, we have an average of 61 CHF, up from around 50 CHF at year-end 2022. Out of 19 analysts, only 5 have a "BUY" rating. There isn't a whole lot of conviction to be had here - and that is understandable.

Much like with HeidelbergCement, I expect the company's earnings to be relatively flat, with the 2022 level not being achieved until 2025 or 2026. Until then, earnings are more likely to be volatile - and S&P Global and other analysts are sharing that forecast.

{kind=link}

I apply a 10% discount to Holcim for some of the risks mentioned here, but I still consider weighing these at fairly heavy amounts. My previous price target, given in early 2023, conservative, for Holcim, was 60 CHF. I'm not only shifting my stance here, but I'm also shifting my PT to account for this slightly higher risk. it's now 58 CHF, which means I'm lowering it to around 11-12x normalized P/E.

In terms of market cap, Holcim is far larger than Heidelberg. Other companies in the same segment include CRH plc (CRH), Vulcan (VMC), Martin Marietta ( MLM ), Grasim (GRSXY), and others. While Holcim has a higher overall asset quality and brings with it a better exposure mix than Heidelberg, Heidelberg is a lot more predictable as a business. It is volatile but doesn't see the same sort of volatility as Holcim does. Holcim's push towards diversification is more intent than Heidelberg, and it's based on the assumption that this sort of mix is more favorable in the long term.

That might be the case - but that doesn't mean Heidelberg or its higher Cement-focused business is somehow less attractive. I'm also somewhat leery of Holcim management, which has an unfortunate history of overpromising and underperforming - both in results and shareholder returns over time, even cutting or lowering the payout at several times in the past 20 years. It's delivered yield, but not as much as some other businesses. The latest management moves might turn out to be the latest in such a move, specifically the overfocus/quick shift to products and solutions, and leaving entire geographies behind, divesting decades' worth of asset investments at below-replacement prices. And these below-replacement prices are my problem here because building these assets is very expensive - and their ownership of legacy assets is the entire reason why cement companies are attractive, to some extent.

It is how I've outperformed with HeidelbergCement, and why my thesis is the following here.

Thesis

- Holcim is one of the most qualitative and interesting cement companies in Europe - together with peers like Heidelberg, which I view as almost equally attractive. It has a, 4%+ yield, and a good set of fundamentals, even if there is a risk to some of its asset profile.

- I no longer see Holcim as a "BUY" - and for this company, I'm saying it's at 58 in terms of PT, making it a "HOLD".

- Remember the high level you should be looking at here. Any Cement company such as this is a play on Urbanization. The fundamental trends ongoing around the world speak in the long-term favor of companies like Holcim - and that's why I invest in them. At least, at the right overall level.

Remember, I'm all about:

- Buying undervalued - even if that undervaluation is slight and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

- If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

- If the company doesn't go into overvaluation but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

- I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them ( italicized ).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside that is high enough, based on earnings growth or multiple expansion/reversion.

I no longer see Holcim as cheap or as attractive enough to consider it a 'Buy' at over 58 CHF. It's a 'Hold', if barely.

For further details see:

Holcim: Upside In Concrete Long-Term, But Near-Term Problems