HLLY - Holley: Attractive But Not The Best Prospect On The Market

Summary

- Holley has done well recently, but the picture this year is looking a lot less great for the firm.

- Shares do look cheap, and likely offer some upside potential for investors as a result.

- Having said that, there likely are better prospects that can be had at this moment that investors should consider too.

The automotive space is incredibly large. With the number of vehicles in the US alone nearing 290 million and that number almost certain to grow for the foreseeable future, this should not be any surprise. But of course, not every automobile is the same. And many automobiles, if not all, eventually need some parts in them replaced because of wear and tear. One company that's dedicated to providing aftermarket products for car and truck enthusiasts is Holley ( HLLY ). With its history dating back to 1903, the company is a fairly old one. And in the past three years, management has overseen some attractive growth. Most recent growth has been a bit weak, likely because of current market conditions. But given how affordable shares look today, the company could offer some nice upside for long-term, value-oriented investors.

A focus on aftermarket parts

As I mentioned already, Holley focuses on designing and selling high-performance automotive aftermarket products geared toward car and truck enthusiasts. The company produces products for a variety of automotive platforms and it provides them for sale through multiple types of distribution channels. Key brands that the company owns include its hallmark Holley and Holley EFI brands. The latter of these is the largest, accounting for 16% of the company's revenue. It focuses largely on electronic fuel injection technology. Other key brands include MSD (which focuses on electronics for the powertrain category), Simpson (Which focuses on motor sport safety products like helmets, head and neck restraints, seatbelts, firesuits, and more), Powerteq (which involves the production of exhaust, intakes, drivetrain, and engine tuning products and accessories), Accel (which focuses on performance fuel and ignition systems), and Flowmaster (with its emphasis on developing exhaust products).

It should prove useful to dig a bit deeper into where the company generates most of its revenue from. During its 2021 fiscal year, 46.8% of its revenue came from electronic systems. Mechanical systems came in second with 23.4% of revenue. Then we had exhaust products, accessories, and safety products, accounting for 11.1%, 9.2%, and 9.5%, respectively, of the company's revenue. Geographically speaking, the company is largely focused on the U.S. market. But this comes with a caveat. 97.4% of the company's revenue is attributed to its domestic operations. But this revenue is designated as domestic if the products in question were shipped from the US. So this does not track the end user, unfortunately. The rest of the revenue, meanwhile, comes from Italy.

{kind=link}

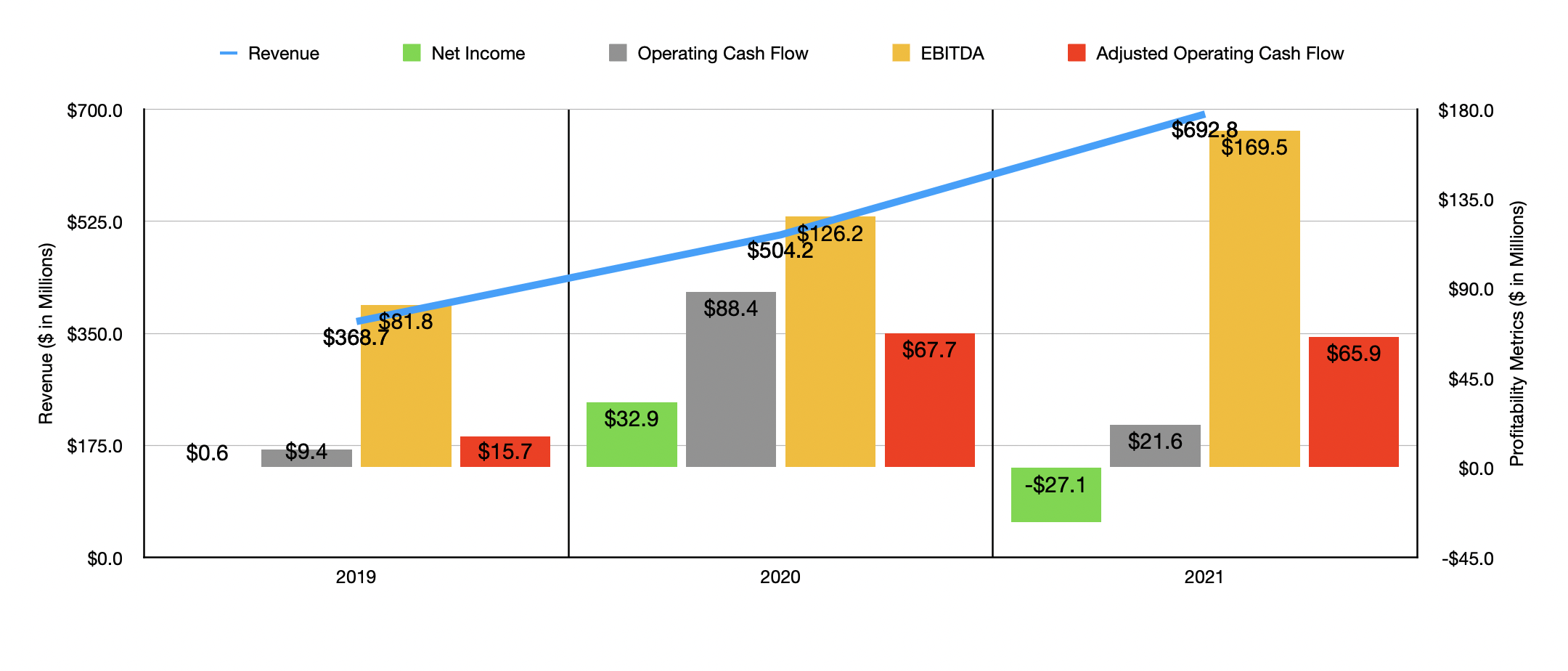

Over the past three years, the management team at Holley has done a great job growing the company's top line. Revenue rose from $368.7 million in 2019 to $692.8 million last year. This is not to say that all of the company's expansion has been organic. Between 2020 and 2021, for instance, the company's revenue grew by 37.4%. 61.7% of this revenue increase came from acquisitions the company had made. The rest came from strength in some of the company's core products, with electronics systems products revenue climbing by 25.1% while mechanical systems product revenue grew by 18.1%.

Profitability for the company, meanwhile, has been rather mixed. In 2019, net income totaled just $0.6 million. This jumped to $32.9 million in 2020 before the company turned to a loss of $27.1 million last year. Similar volatility has been seen with operating cash flow, with the metric going from $9.4 million in 2019 to $88.4 million in 2020 before dropping to $21.6 million last year. If we adjust for changes in working capital, however, the picture is not quite so bad. After rising from $15.7 million in 2019 to $67.7 million in 2020, cash flow dipped only slightly to $65.9 million last year. Meanwhile, EBITDA for the company has risen consistently, growing from $81.8 million in 2019 to $126.2 million in 2020. In 2021, it rose further to $169.5 million.

{kind=link}

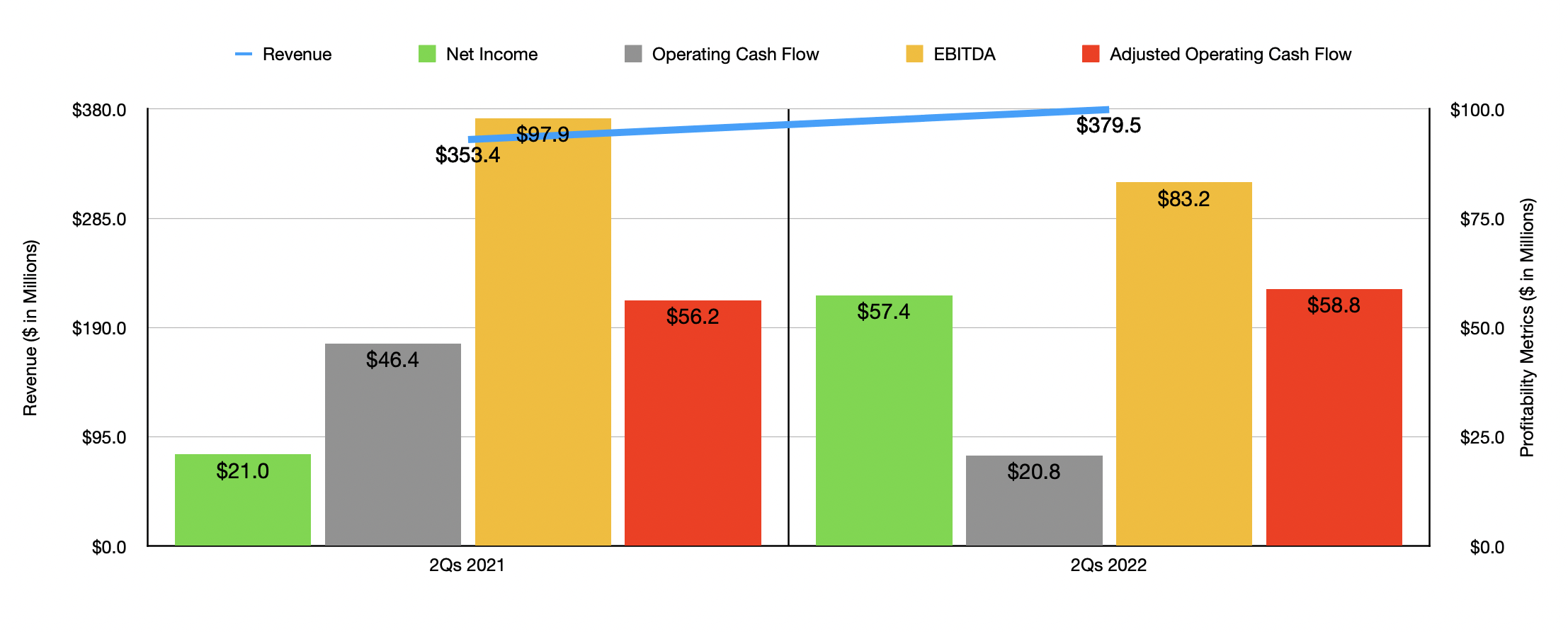

For the current fiscal year, how well the company is performing depends on how deep you look. If you look at just the first half of the year as a whole , the picture is fairly solid, with revenue climbing by 7.4% from $353.4 million to $379.5 million. Having said that, this view alone hides something rather negative. In the second quarter of the year alone, revenue came in at $179.4 million. That's 7% lower than the $193 million in revenue the company generated the same time last year. What's even worse is that this $13.6 million decline in revenue came even at a time when acquisitions added $9.4 million to the company's top line. Management attributed this largely to the impact associated with microchip shortages and other supply chain challenges that prevented the company from building and shipping many of its most popular products. They also said that some of the pain came from destocking from its resellers in response to the current economic environment, as well as from the softening of consumer demand. Lower unit volume impacted revenue in the second quarter to the tune of $37 million, net of a $14 million contribution associated with price increases.

{kind=link}

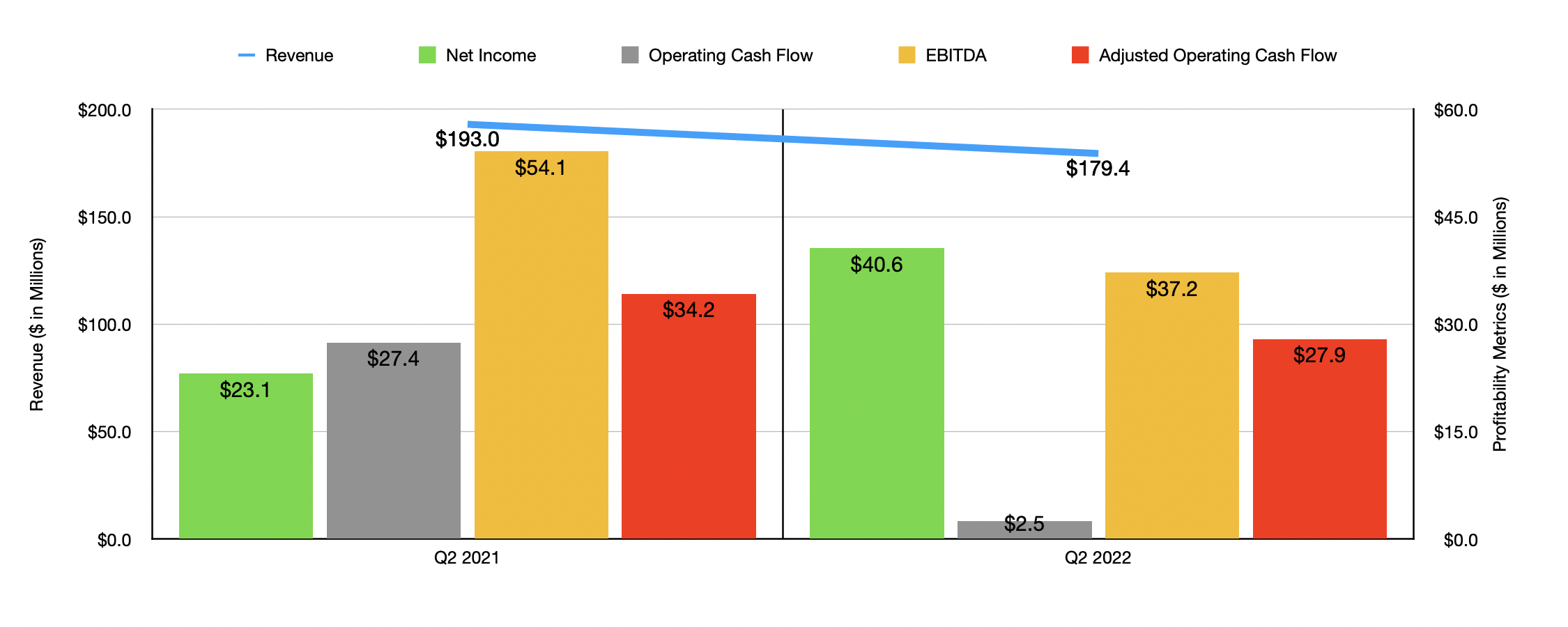

Just as we have seen some volatility on the top line, we have also seen some volatility on the bottom line this year. Net income skyrocketed from $21 million in the first half of 2021 to $57.4 million the same time this year. On the other hand, operating cash flow plunged from $46.4 million to $20.8 million. If we adjust for changes in working capital, however, it would have inched up from $56.2 million to $58.8 million. But at that same time, EBITDA for the company declined, dropping from $97.9 million to $83.2 million. Similar volatility can be seen by looking at the latest quarter alone, as can be seen in the chart above. Net income ultimately spiked in the latest quarter. But all other profitability metrics declined year over year, with the drop experienced by operating cash flow being the most severe.

{kind=link}

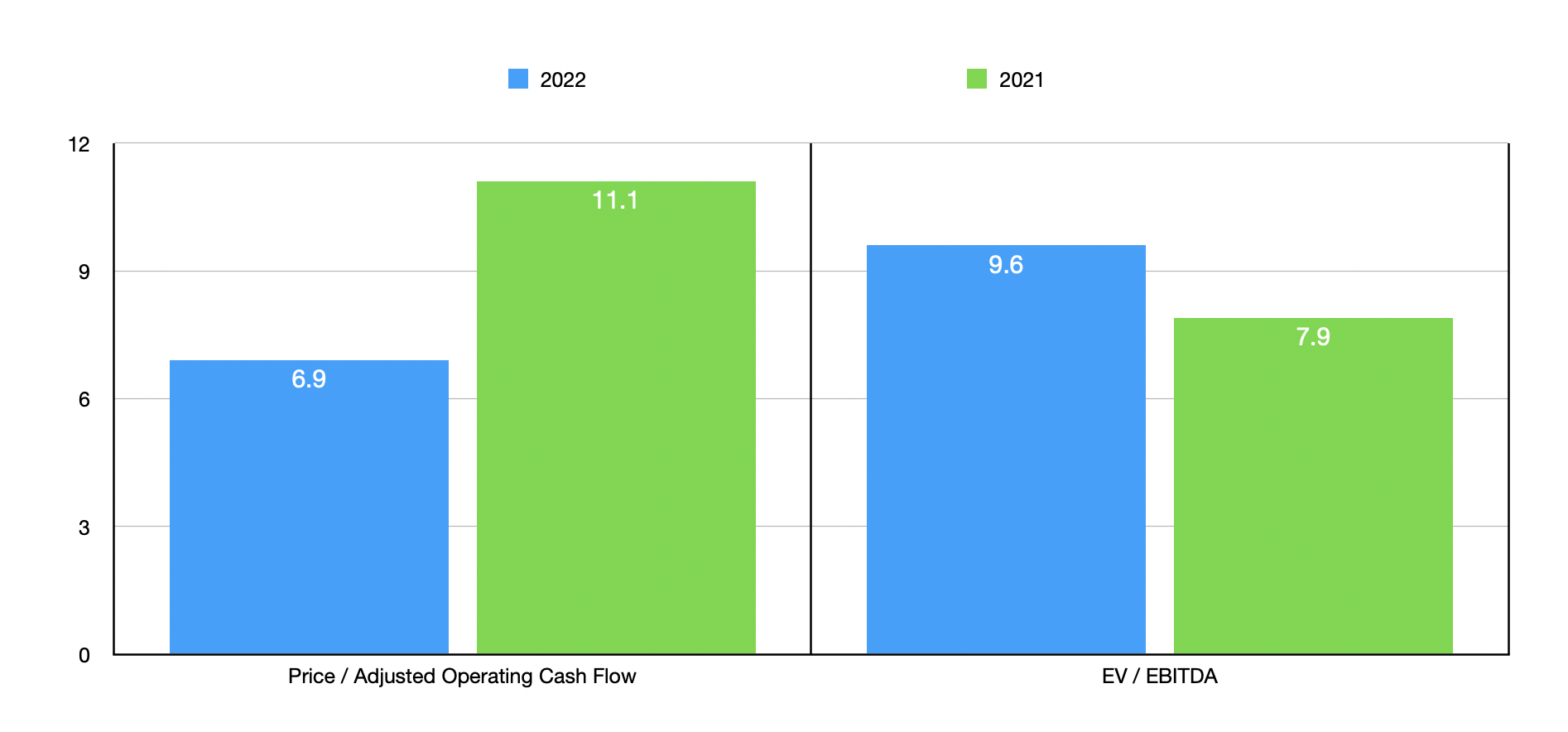

When it comes to the 2022 fiscal year as a whole, management expects revenue to come in at between $700 million and $725 million. Meanwhile, EBITDA for the company should decline, dropping to between $135 million and $145 million. If we take the midpoint there and strip out anticipated interest expense that management offered guidance on, we get a good proxy for adjusted operating cash flow. This metric should ultimately come out to $106 million. Using these figures, we can easily value the firm. The forward price to adjusted operating cash flow multiple should be 6.9. That's down from the 11.1 reading we get using 2021 results. The EV to EBITDA multiple, meanwhile, should climb from 7.9 to 9.6. As part of my analysis, I decided to compare the company to five similar firms. On a price to operating cash flow basis, only two of the five businesses had positive results, with multiples of 1.9 and 23.9, respectively. Our prospect was in the middle of the two. When it came to the EV to EBITDA approach, the range for the five firms was between 2.7 and 18.4. In this case, four of the five companies were cheaper than our prospect.

| Company |

| Price / Operating Cash Flow |

| EV / EBITDA |

| Holley |

| 6.9 |

| 9.6 |

| Standard Motor Products ( SMP ) |

| N/A |

| 8.5 |

| Modine Manufacturing Company ( MOD ) |

| 23.9 |

| 6.4 |

| Stoneridge ( SRI ) |

| N/A |

| 18.4 |

| Garrett Motion ( GTX ) |

| 1.9 |

| 2.7 |

| Motorcar Parts of America ( MPAA ) |

| N/A |

| 5.7 |

Takeaway

Right now, Holley is facing some pain because of microchip and other supply chain-related challenges. It's truly unclear how long this will last. Although revenue is expected to rise this year, it looks as though EBITDA will decline compared to last year. Having said that, shares of the business do still work cheap on an absolute basis, while they look mixed relative to similar firms. Just because of how cheap shares are and the company's historical track record of growth, I do think that it still warrants some upside potential, leading me to rate it a soft 'buy' at this time. But with that said, I do think that there might be better prospects we had right now.

For further details see:

Holley: Attractive, But Not The Best Prospect On The Market