HLLY - Holley: Decent Q1 2023 Results But Underwhelming Outlook (Rating Upgrade)

2023-05-26 04:34:53 ET

Summary

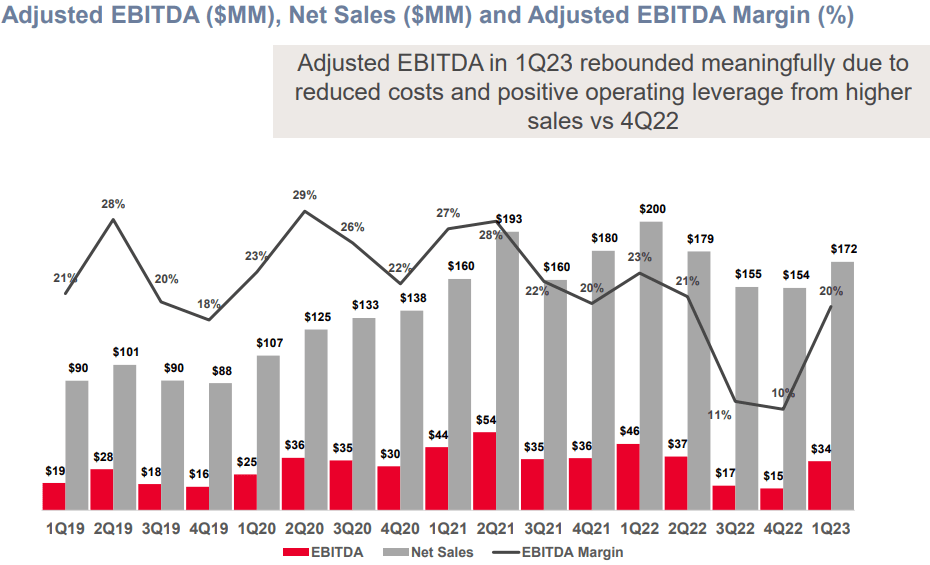

- With sales rising in Q1 2023 and Holley implementing cost-cutting measures, the gross profit and adjusted EBITDA soared by 43.3% and 124.5% quarter on quarter.

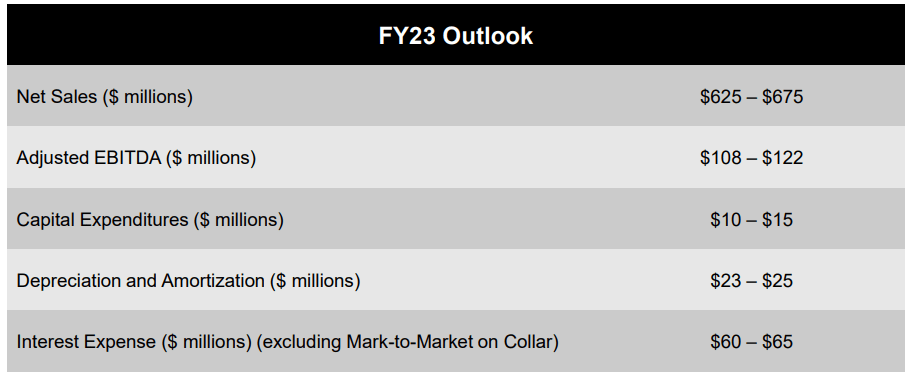

- However, quarterly sales and adjusted EBITDA should fall in the coming months according to the 2023 outlook and HLLY could breach its consolidated net leverage ratio financial covenant soon.

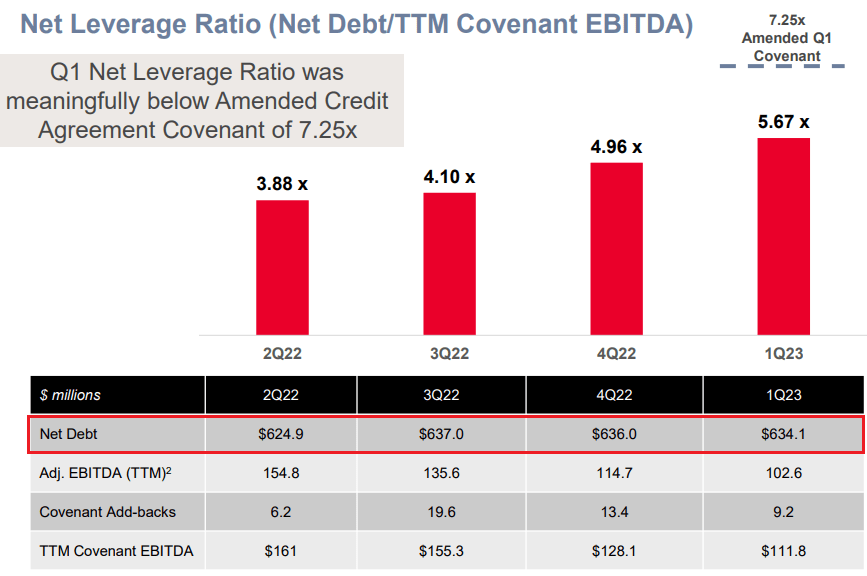

- Holley has been unable to bring down its net debt and the consolidated net leverage ratio financial covenant level declines to 5.75x in Q4 2023.

- In my view, risk-averse investors should avoid this stock.

Introduction

I’ve written four articles on SA about U.S. high-performance automotive parts maker Holley (NYSE: HLLY ), the latest of which was in February when I said that the financial situation of the company was getting precarious and there could be significant stock dilution or another bankruptcy in the cards if something didn’t change dramatically.

Well, in early March Holley announced that it plans to start cutting costs and that it reached a deal with its lenders to amend a covenant of its credit facility. It seems that the risk of insolvency has diminished significantly in the near term and the cost-cutting measures are starting to bear fruit as the adjusted EBITDA margin doubled quarter on quarter in Q1 2023 to 19.7%. In addition, orders are improving, and Holley is in the black once again. That being said, I’m concerned about the lack of progress on slashing net debt, and I think that the 2023 outlook is disappointing. Holley expects to book adjusted EBITDA of $108 million to $122 million for the year, which is slightly above the TTM rate, and this suggests that the financial results for the next few quarters are likely to deteriorate. Let’s review.

Overview of the Q1 2023 results

In case you're not familiar with Holley or my earlier coverage, here's a short description of the business. The company manufactures and sells high-performance products for car and truck enthusiasts such as carburetors, exhaust headers, superchargers, engine tuners, mufflers, and transmissions. It has locations across North America, Canada, Italy, and China and its brands include Flowmaster, NOS, Scott Drake, Accel, and MSD among others.

{kind=link}

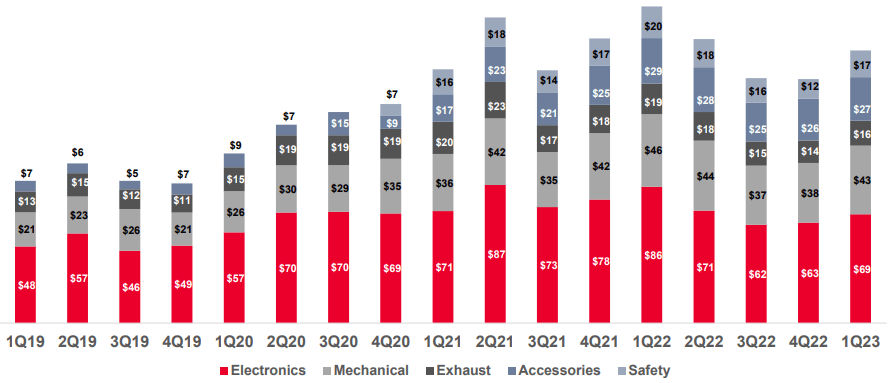

In 2021, Holley was listed on the NYSE and one of its main selling points back then was that demand for its products was sticky as 82% of all car and truck enthusiasts see budgets on parts as recurring expenses (slide 13 here ). I have doubts about this idea considering the company had a tough time during the Great Recession. In 2010, Holley emerged from Chapter 11 bankruptcy for the second time in three years as sales slumped by 19.5% year on year to $90.2 million in 2009. The financial results for 2022 were disappointing too due to chip shortages, supply chain disruptions as well as pressure on demand for discretionary goods in the USA due to high inflation. Yet, I was surprised to see net sales improved by 11.7% quarter on quarter to $172.2 million in Q1 2023 as Holley managed to improve chip supply.

{kind=link}

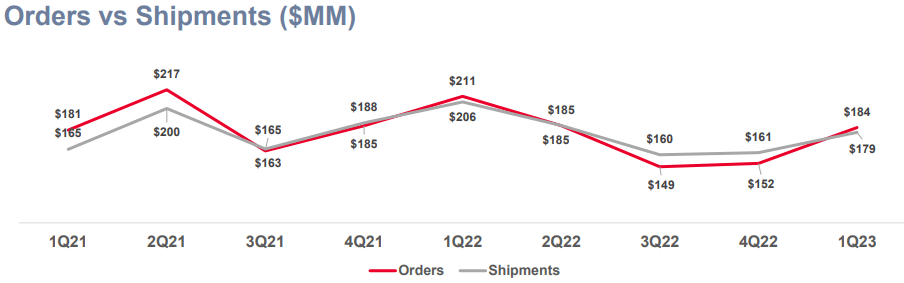

As you can see, there was a sequential improvement in net sales across all product categories and I think that revenues could continue to grow in Q2 2023 as new orders are growing once again. Orders in the electronics category seem to be particularly strong as Holley mentioned during its Q1 2023 earnings call that they outpace its ability to supply.

{kind=link}

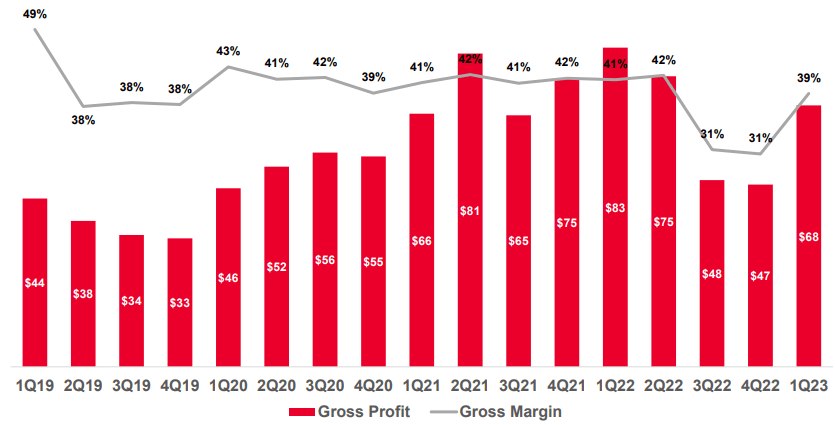

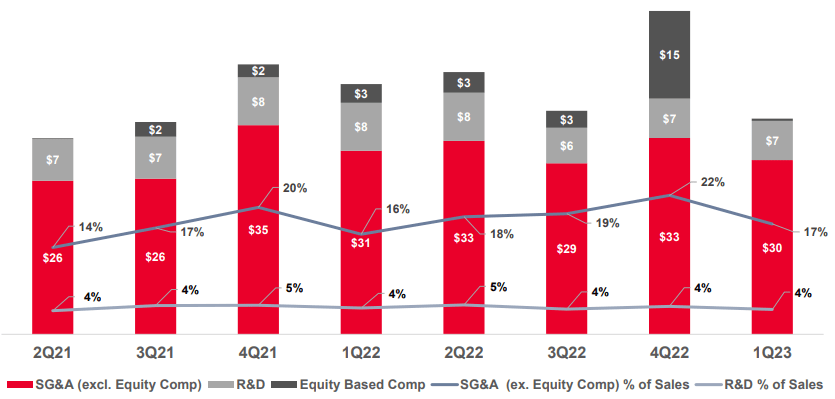

During Q1 2023, Holley focused on optimizing its distribution network with an emphasis on reducing complexity in its facilities and slashing inventories. The company also limited SG&A expenses and combined with higher sales and the lack of non-cash product rationalization charges, gross profit and adjusted EBITDA soared by 43.3% and 124.5% quarter on quarter, respectively. The gross margin is now at 39.3% and I think it could cross the 40% mark in Q2 2023 thanks to economies of scale as sales continue to rise. In addition, Holley mentioned at its Q1 2023 earnings call that it plans to accelerate the synergy capture from recent acquisitions and achieve $3 million to $3.5 million of cost synergies during the year.

{kind=link}

{kind=link}

{kind=link}

Despite the positive developments, I’m worried about Holley’s debt situation. Sure, the company amended the terms on its credit facility in March thus raising the consolidated net leverage ratio financial covenant level to 7.25x from 5x which significantly reduces insolvency risk. However, the net debt level barely decreased in Q1 2023 and the weighted average interest rate on the borrowings under the credit facility had risen to 8.7% as of April 2 (page 16 here ).

{kind=link}

The operating cash flow is insufficient to pay down debt considering interest expenses for 2023 are expected to come in at $60 million to $65 million in 2023 and taking into account that the consolidated net leverage ratio financial covenant level declines to 5.75x in Q4 2023, the risk of insolvency or significant stock dilution is still high. I don’t expect the net leverage ratio to improve much in the near future as Holley’s outlook for 2023 includes adjusted EBITDA of $108 million to $122 million, which isn’t much better than the TTM numbers for Q1 2023. Overall, I find the outlook for the full year underwhelming as it suggests that there won’t be much improvement in the financial results of Holley over the remainder of the year. I expect quarterly sales and adjusted EBITDA to fall in Q3 and Q4.

{kind=link}

Overall, I continue to be bearish on Holley’s stock but I’m upgrading my rating to Sell due to the improved liquidity situation in the short term thanks to the debt renegotiation as well as the decent Q1 2023 financial results. In my view, short selling seems viable as I expect the share price could be under pressure over the coming months due to deteriorating financial results. Data from Fintel shows that the short borrow fee rate stands at just 0.79% as of the time of writing. However, the short interest is 7.88% of the float and it takes over 10 days to cover so price volatility risk is high. It could be best for risk-averse investors to avoid this stock.

Investor takeaway

The market valuation of Holley has increased by over 50% since my previous article and I think the main reason for this is the improvement of financial results as well as the renegotiation of debts. However, it seems that the quarterly sales and adjusted EBITDA will decline soon once again and considering Holley has been unable to bring down its net debt, the consolidated net leverage ratio financial covenant level of 5.75x could be breached in late 2023 and the risk of insolvency or significant stock dilution remains high.

For further details see:

Holley: Decent Q1 2023 Results But Underwhelming Outlook (Rating Upgrade)