HLLY - Holley Shifts Into A Higher Gear (Rating Upgrade)

2023-08-12 04:54:08 ET

Summary

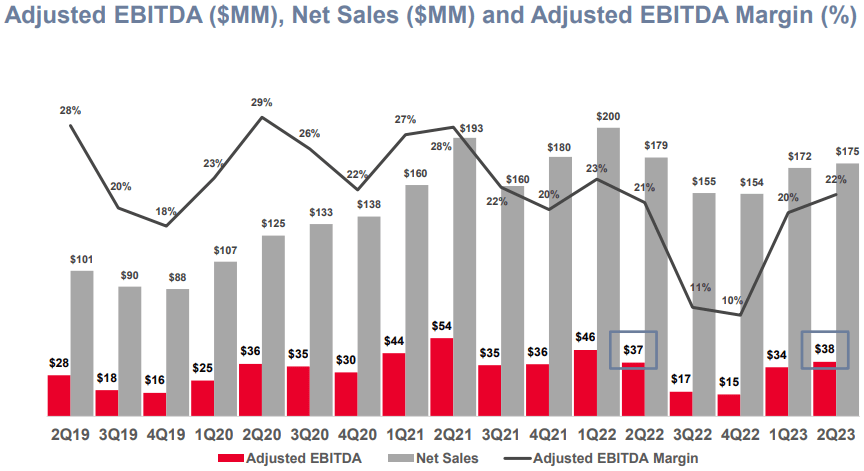

- Holley booked solid Q2 2023 results with orders for more than $180 million and an adjusted EBITDA margin of above 21%.

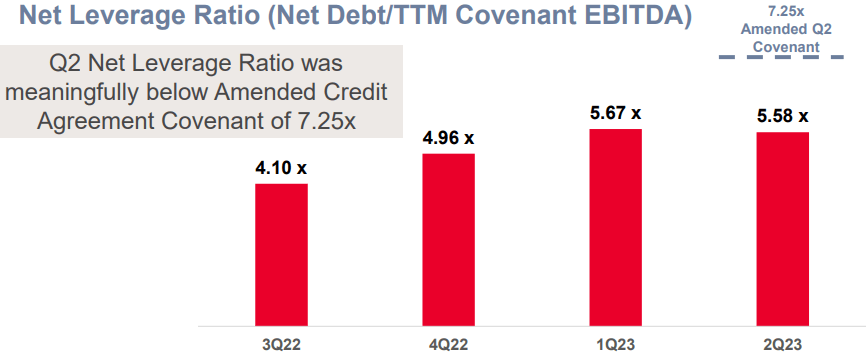

- In addition, Holley reduced its net debt by $28.8 million thanks to a much-improved free cash flow.

- In my view, the liquidity issues have dissipated thanks to the improving EBITDA, but the company doesn’t look cheap at an EV/adjusted EBITDA ratio of 14.3x.

- I think it could be best for risk-averse investors to avoid this stock.

Introduction

I've been closely following automotive parts maker Holley (HLLY) and my latest article on the company was released in May when I said that the 2023 outlook was disappointing and that I was concerned about the lack of progress on net debt reduction.

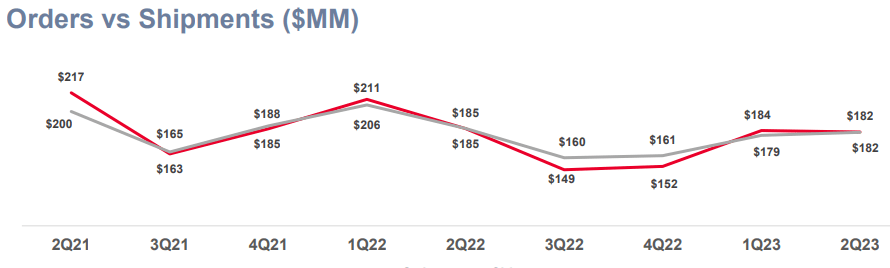

Well, Holley released its Q2 2023 financial results on August 10, and I think that they were strong as orders remained close to the levels of Q1 while the adjusted EBITDA margin surpassed 21% thanks to cost-cutting measures. In my view, Holley is on the right track and the solvency risk has decreased significantly but its stock is still not cheap. Let's review.

Overview of the Q2 2023 financial results

In case you're not familiar with Holley or my earlier coverage, here's a brief description of the business. The company was established in 1896 and is involved in the production of high-performance products for car and truck enthusiasts such as superchargers, fuel pumps, and engine tuners. Holley has dozens of brands, including Flowmaster, NOS, and MSD among others.

{kind=link}

The Holley family exited the business in 1968 and the company struggled during the Great Recession due to weak demand as it emerged from Chapter 11 bankruptcy twice in the span of just three years. In 2018, Holley was merged with Driven Performance Brands and got listed on the NYSE in July 2021 through a special-purpose acquisition company (SPAC) deal.

In my view, the main issue for Holley investors is that the car parts segment in which the company operates is highly cyclical - high performance parts for enthusiasts fall in the discretionary goods category and this market is therefore vulnerable to macroeconomic headwinds. The company's financial woes started again in Q2 2022 as supply chain disruptions and chip shortages hit the global economy and the situation got worse over the next few quarters as high inflation and de-stocking by customers negatively affected orders. This put Holley in a tough position from a liquidity standpoint as it had accumulated a net debt of over $600 million due to over a dozen acquisitions over the past years and falling EBITDA meant that it was getting close to breaching its debt covenants. Yet, it seems that the worst is behind Holley as it has managed to rake in orders of over $180 million for two consecutive quarters now, and with the adjusted EBITDA margin improving to 2021 levels, the net leverage ratio is retreating from the danger zone.

{kind=link}

{kind=link}

{kind=link}

Looking at the reasons for the strong order flow in Q2 2023, I think the key ones include the launch of 75 new products during the quarter (see slide 7 here ) as well as the increased marketing activity which included a 3-day event in Texas where Holley invited social media influencers, and YouTube celebrities with more than 29 million combined followers. In my view, the strong momentum is likely to carry through in Q3 with orders for that quarter remaining above $180 million.

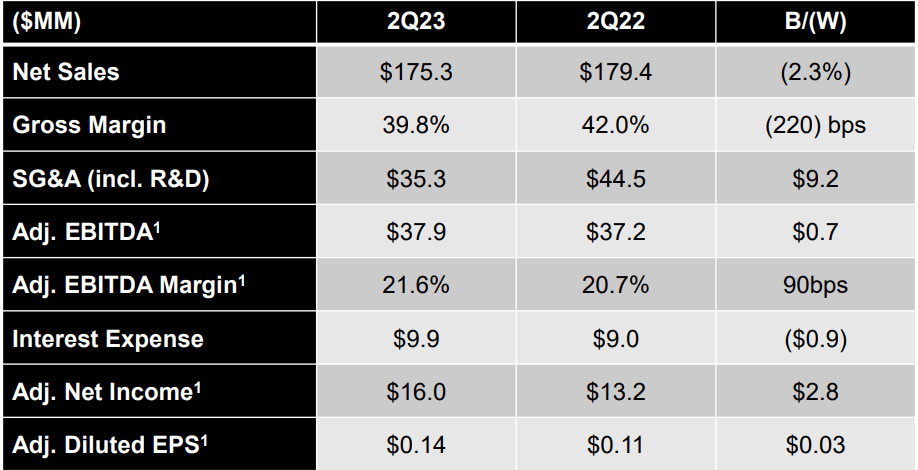

Looking at the Q2 2023 income statement, we can see that adjusted EBITDA surpassed the levels from a year earlier despite a slight decrease in revenues and lower gross margins and the main reason behind this was cost savings of about $11 million coming from cost-cutting measures initiated in late 2022 that included a decrease in the headcount, manufacturing efficiencies, and improvements in freight expenses.

{kind=link}

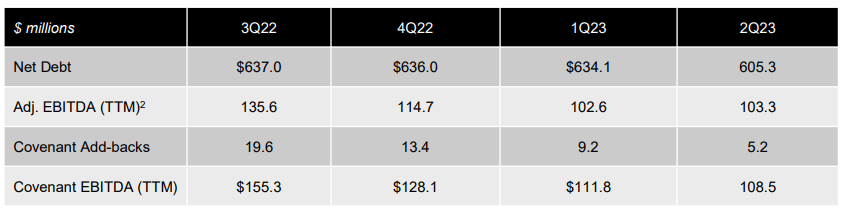

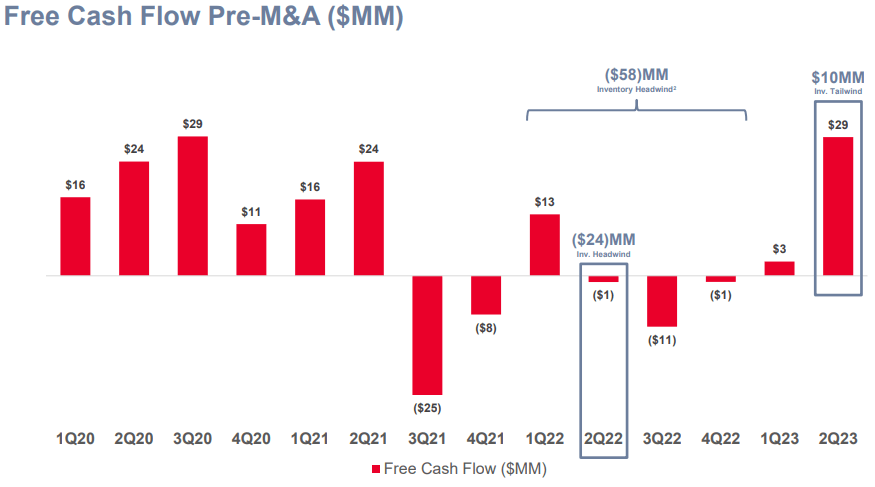

Yet, there is some seasonality in Holley's business, and I think that the adjusted EBITDA margin is likely to dip below 20% in the second half of 2023. Turning our attention to the balance sheet, I find it encouraging that the net debt decreased by $28.8 million quarter on quarter to $605.3 million. The company is finally making progress on reducing its debt load thanks to free cash flow soaring to $29 million as inventories were slashed by about $10 million. The latter had increased during the period of supply chain shortages and falling order flow.

{kind=link}

{kind=link}

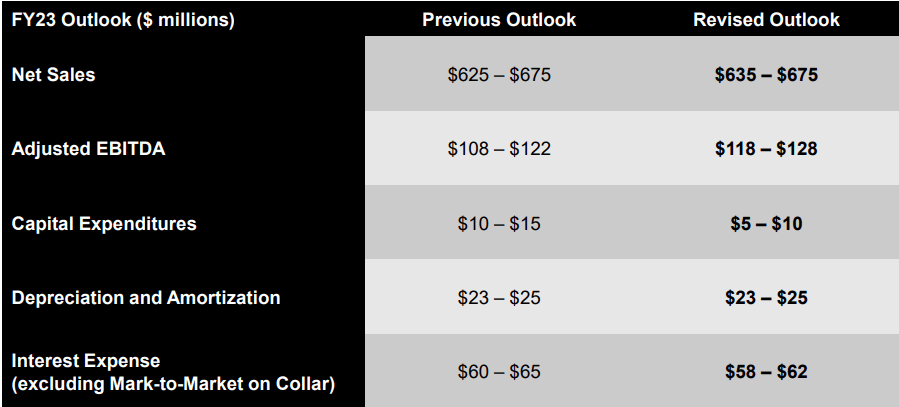

Following the strong Q2 2023 financial results, Holley has slightly improved its 2023 guidance and now expects to book adjusted EBITDA of between $118 million and $128 million for the year. This translates into an adjusted EBITDA margin of between 17.5% and 20.2% and reflects the seasonality of the business. In my view, the low end of the adjusted EBITDA target seems achievable, and the net sales forecast could be too conservative considering Holley would need to book revenues of just $288 million in the second part of the year to surpass the lower end. This is over $20 million below the net sales achieved in this period during the challenging 2022.

{kind=link}

Overall, I think that Holley delivered solid financial results for Q2 2023, but the stock doesn't look particularly cheap as of the time of writing, especially after the market capitalization soared by 19.65% to $871.2 million on August 10. The company now has an enterprise value (EV) of $1.48 billion and is trading at an EV/adjusted EBITDA ratio of 14.3x on a TTM basis. Even if we take the upper end of the 2023 outlook, the ratio will only drop to 11.5x and I think that this is a high level for a cyclical business with limited organic growth.

Investor takeaway

In 2022, Holley embarked on a cost-cutting program, and it seems that this is bearing fruit as the adjusted EBITDA margin topped 21% in Q2 2023. In addition, the order flow has stabilized, and the improved free cash flow enabled the company to reduce its net debt by almost $30 million during the quarter. I'm optimistic that Holley could keep the strong momentum going thanks to the high number of new product launches in Q2 and that the improved 2023 outlook seems achievable. While I think the liquidity issues have dissipated thanks to the improving EBITDA margins and my stance on the stock is no longer bearish, I think it could be best for risk-averse investors to avoid Holley as the EV/adjusted EBITDA ratio is still in the double digits on a TTM basis.

For further details see:

Holley Shifts Into A Higher Gear (Rating Upgrade)