HLLY - Holley: Strong Q3 2023 Results And Significant Debt Reduction (Rating Upgrade)

2023-11-15 03:28:57 ET

Summary

- Holley’s net sales rose by 1.1% in Q3 2023 while the adjusted EBITDA margin soared to 19% thanks to cost savings.

- Also, free cash flow came in at $21.7 million and Holley slashed its net debt by $20.9 million during the quarter.

- In my view, the recent selloff has created a good buying opportunity as the EV/adjusted EBITDA ratio is 8.2x based on the midpoint of the 2023 guidance.

Introduction

I’ve written a total of six articles on SA about Holley (HLLY), the latest of which was in August when I said that the Q2 2023 financial results were strong but that the company was still not cheap.

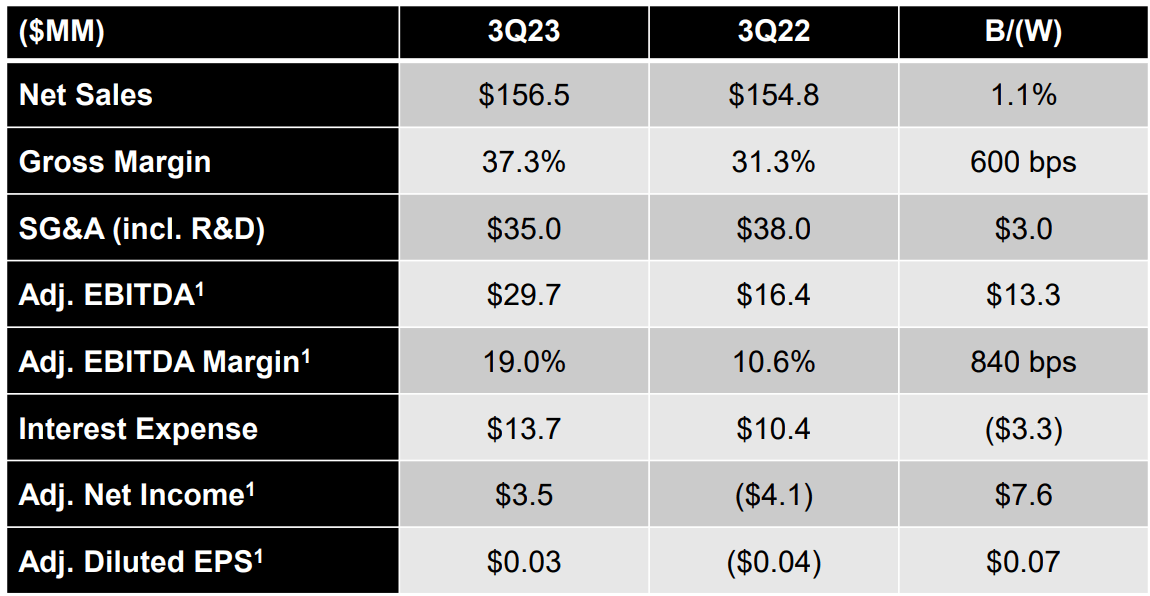

On November 8, Holley released its results for Q3 2023, and it was another solid quarter as net sales growth got back into positive territory while adjusted EBITDA soared by over 80% year on year to $29.7 million. In addition, the company strengthened its balance sheet as free cash flow of $21.7 million allowed it to cut its net debt by $20.9 million during the quarter. Considering the outlook for the business is improving and the market capitalization of Holley has decreased by 52.9% since my previous article, I now feel comfortable upgrading my rating on the stock to a speculative buy. Let’s review.

Overview of the Q3 2023 financial results

If you aren't familiar with the company or my earlier coverage, here's a brief description of the business. Holley focuses on the manufacturing and sale of high-performance products for car and truck enthusiasts such as superchargers, fuel pumps, and engine tuners and is a successor to a company of the same name founded in 1896 that entered into Chapter 11 bankruptcy during the Great Recession. As high performance car parts fall into the discretionary goods category, this is a business that is vulnerable to changes in the macroeconomic cycle.

{kind=link}

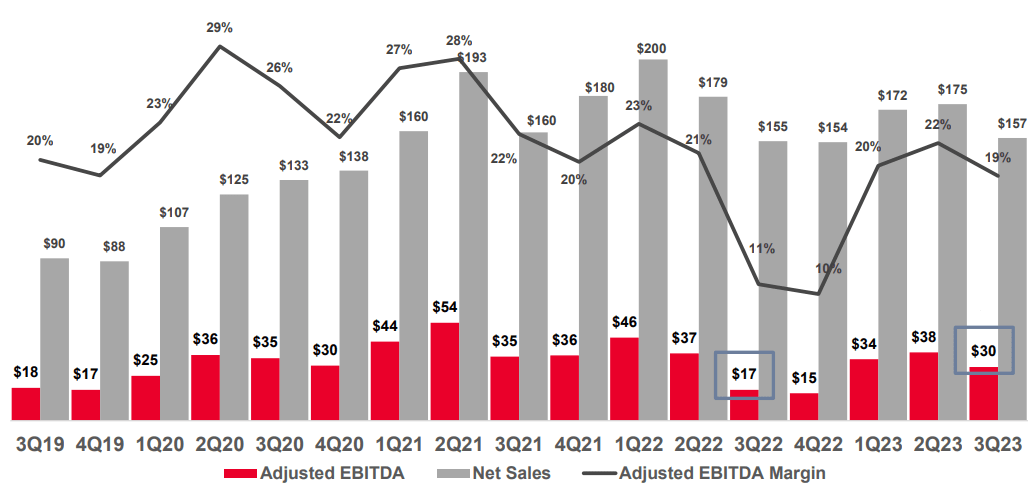

In 2021, Holley listed on the NYSE through a merger with a special-purpose acquisition company (SPAC) and its financials started suffering from supply chain disruptions and chip shortages in Q2 2022 which were followed by woes brought by inflation and de-stocking by customers. Holley embarked on a cost-cutting plan in late 2022 that is focused on a lower headcount, manufacturing efficiencies as well as improvements in freight expenses. The aim is to achieve annualized cost savings of $35 million and I’m encouraged by the progress it has achieved. Holley reported $10.4 million of year-over-year savings in the Q3 2023 which puts it on track to reach its cost savings goal in 2023.

Looking at the Q3 2023 financial results, net sales growth is back in positive territory as Holley reduced past due orders sequentially by $8.1 million. In addition, the adjusted EBITDA margin improved to 19% thanks to the cost-saving measures while adjusted net income was back into the black.

{kind=link}

{kind=link}

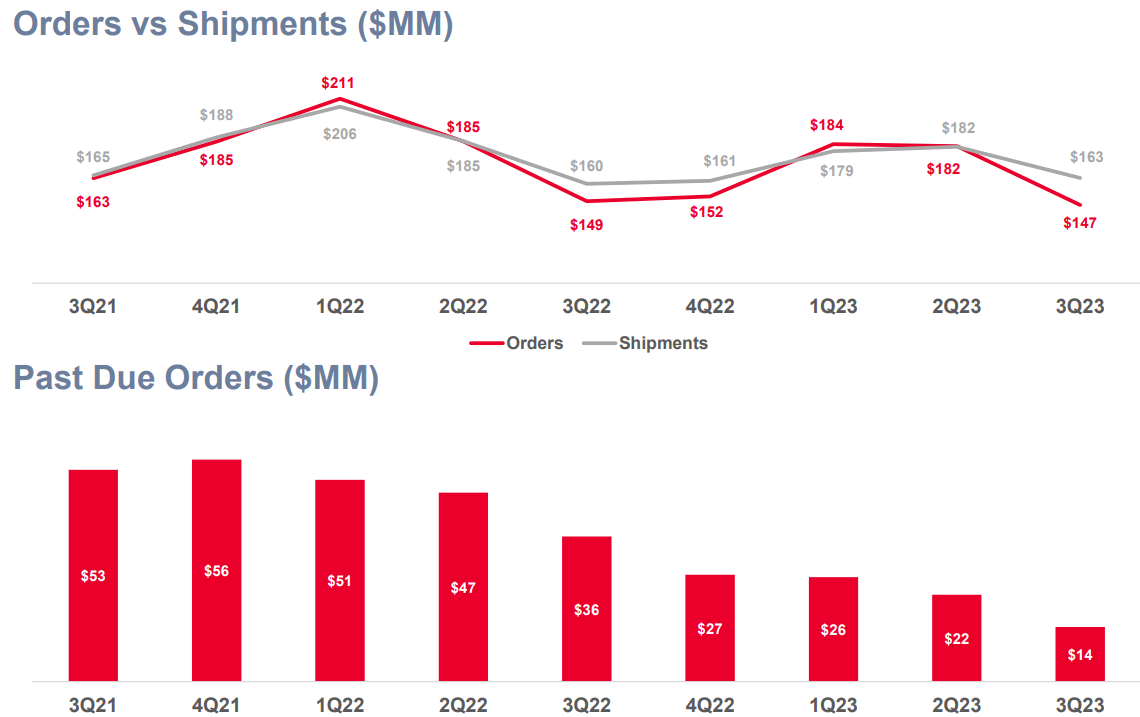

That being said, I’m concerned that orders were just $147 million for the quarter. Considering Holley launched 75 new products in Q2 (see slide 7 here ) and another 67 new products in Q3 (see slide 6 here ) I was expecting orders to be strong. Instead, we got a number that was weaker than even the one from Q3 2022. Yet, it’s worth noting that Q3 is usually Holley’s weakest period for orders due to seasonality. I’m hopeful we’ll see an improvement in Q4 as the company said during its Q3 2023 earnings call that it plans to be more intently focused on order growth trends for its near-term performance.

{kind=link}

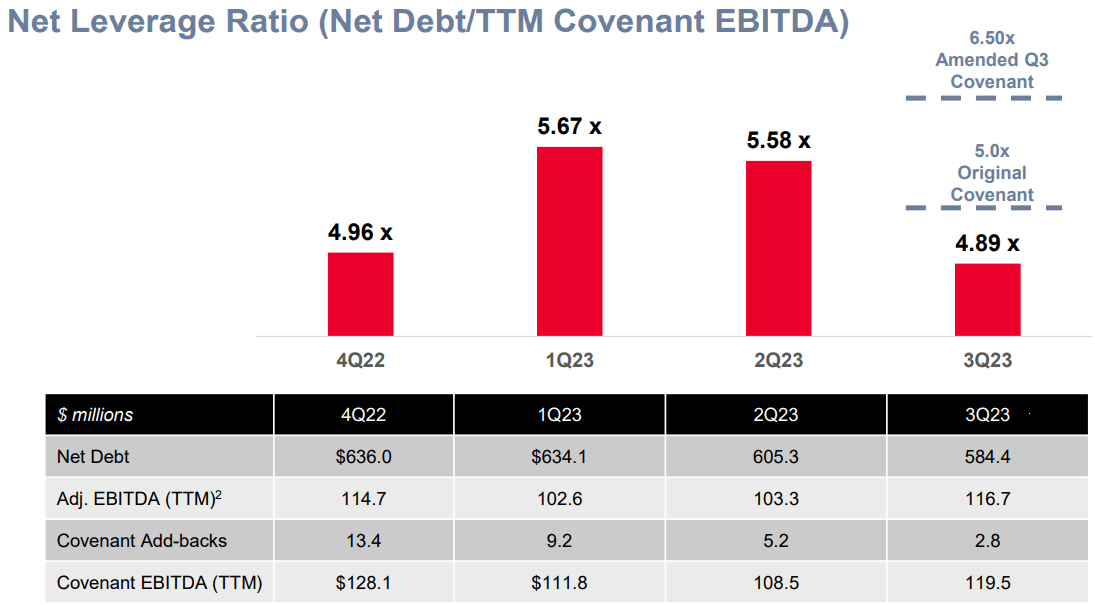

Looking at the balance sheet, net debt went down to $584.4 million at the end of September from $605.3 million a quarter earlier as free cash flow came in at $21.7 million in Q3 2023. As adjusted EBITDA continues to grow, Holley's net leverage ratio is now well below the debt covenant levels. I’m optimistic that net debt could decrease by some $20 million in Q4 2023 as the company continues to focus on strengthening its balance sheet.

{kind=link}

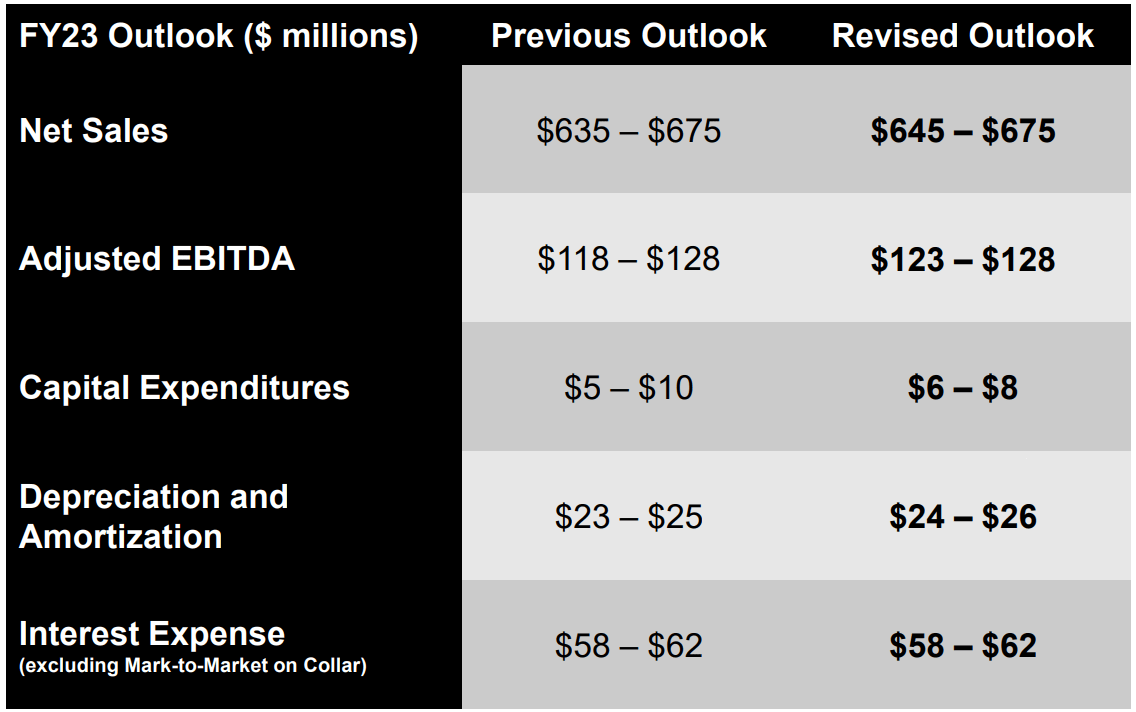

Looking at what to expect for the future, Holley revised its outlook for 2023 upwards once again and now forecasts net sales of $645 million and $675 million and adjusted EBITDA of between $123 million and $128 million. While adjusted EBITDA usually dips in the last quarter of the year due to holiday promotions, I’m encouraged that the guidance suggests it should see a significant improvement compared to Q4 2022.

{kind=link}

Looking at the valuation, Holley has an enterprise value of $1.03 billion as of the time of writing and is trading at an EV/adjusted EBITDA ratio of 8.8x on a TTM basis. Using the midpoint of the 2023 adjusted EBITDA guidance, the ratio drops to 8.2x. While this is a cyclical business, I’m encouraged by Holley’s financial performance during a period of high interest rates, and I think the company should be trading at about 10x EV/adjusted EBITDA. Holley's sales are growing once again, the adjusted EBITDA margin is close to 20% thanks to cost-cutting measures, and the net leverage ratio is now below Q4 2022 levels.

Turning our attention to the downside risks, I think the major one is that high interest rates could put pressure on orders in Q4, particularly during the holiday season in December. Holley’s past due orders were just $14 million in September and a low level of new orders could thus lead to a decrease in net sales as well as margins due to a loss of economies of scale. Looking further ahead, I’m concerned that even if sales in remain unaffected by high interest rates in 2024, growth is likely to be limited due to the lack of M&A as the company remains focused on reducing its net debt.

Investor takeaway

Holley’s net sales are growing once again, and its adjusted EBITDA margin has improved significantly this year as the company is on track to achieve annualized cost savings of around $35 million. Also, the free cash flow for the quarter was above $20 million, which allowed the company to reduce its debt and improve its net leverage ratio. In my view, the selloff over the past few months has created a good buying opportunity as the EV/adjusted EBITDA ratio is now in the single digits. That being said, I’m concerned that orders were low in Q3 and that the net leverage ratio is still pretty high.

For further details see:

Holley: Strong Q3 2023 Results And Significant Debt Reduction (Rating Upgrade)