HLLY - Holley: Weak Company With Only Problems Ahead

2023-10-20 23:51:46 ET

Summary

- Holley’s revenue growth of +41% has been engineered with aggressive M&A, concealing mild organic growth.

- The company’s margins are a mess, with significant risk associated with what its normalized level will be. We consider operational and WC management to be extremely poor thus far.

- Holly’s balance sheet is a mess, with a ND/EBITDA ratio of 6.8x and an inability to generate sufficient FCF to conduct a meaningful deleveraging exercise.

- Holley’s quarterly performance has been disastrous, with Management committed to improving margins are all costs while revenue continues to sink.

- Holley is showing evidence of being undervalued, but we believe this does not sufficiently reflect the significant risks associated with its overall profile.

Investment thesis

Our current investment thesis is:

- Holley is an unattractive business in our view. The company has conducted unsustainable M&A and now has an untenable debt balance. We do not see solvency issues in the near term, but we see no clear route to reaching a sustainable level.

- Aside from this, Holley’s recent performance has been messy, with extreme margin volatility and aggressive cost-cutting by Management. Further, we are unconvinced by its current business model, with its small scale leaving the business susceptible to increased competition.

Company description

Holley Performance Products ( HLLY ) is a renowned American manufacturer of high-performance automotive aftermarket products. With a history dating back to 1903, Holley has become a leading player in the automotive performance industry, providing a diverse range of products catering to enthusiasts and professional racers alike.

Share price

Holley’s share price performance since its SPAC-led listing has been disastrous, losing over 50% of its value at a time when the wider market has struggled (only supported by a handful of tech firms). This does reflect financial weakness fundamentally, in conjunction with wider market sentiment.

Financial analysis

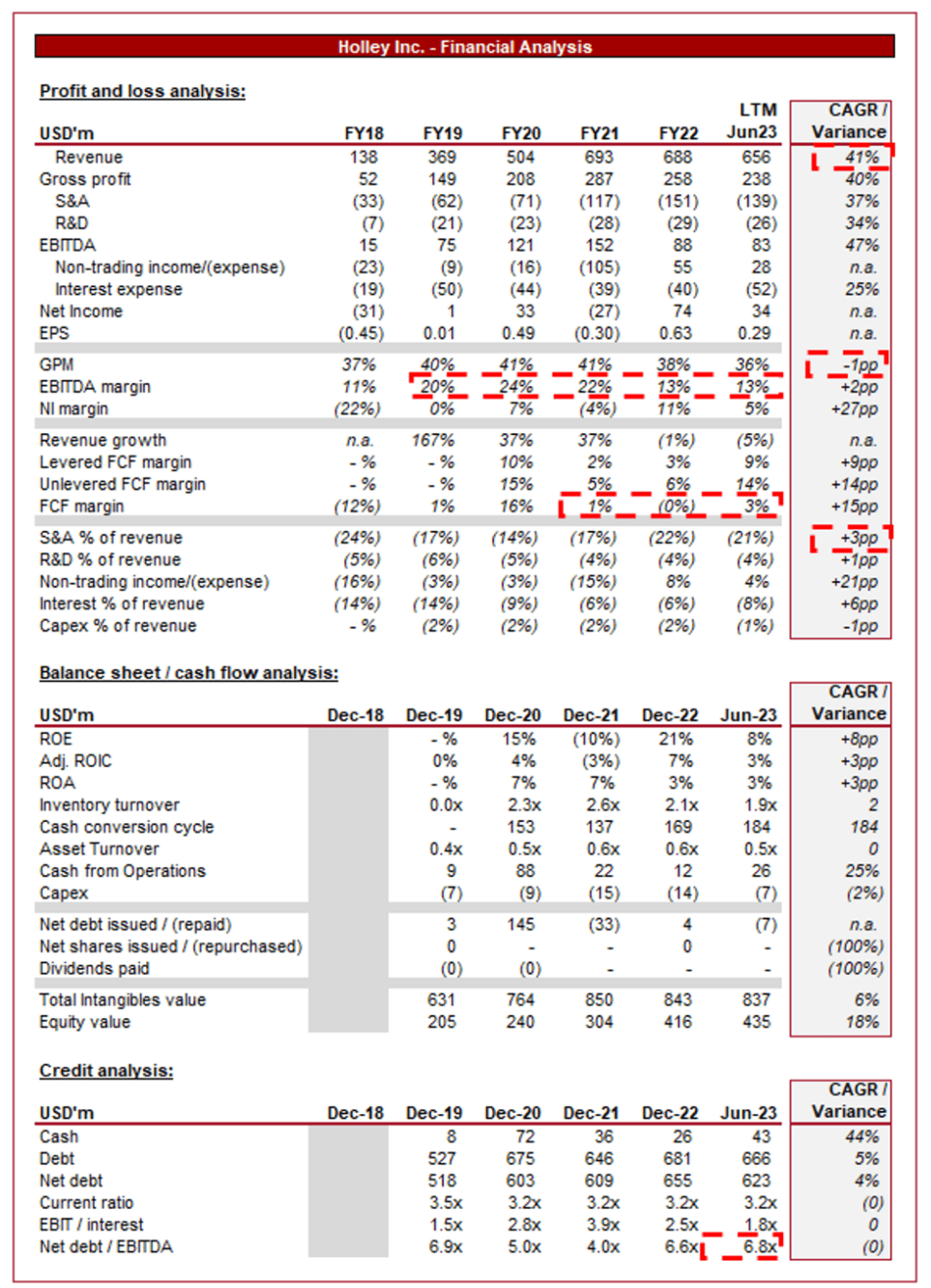

Holley's financials (Capital IQ)

{kind=link}

Presented above are Holley’s financial results.

Revenue & Commercial Factors

Holley’s revenue has grown substantially, with a CAGR of +41% in the last 4 years. This growth has been materially impacted by acquisitions, contributing to year-on-year volatility. EBITDA growth has exceeded this at +47%.

Business Model

Holley offers a wide range of performance products, including carburetors, fuel injection systems, exhaust systems, ignition components, and engine dress-up accessories. The company utilizes this diverse portfolio to cater to automotive enthusiasts and race teams, widening its customer base. Holley strongly leans into those seeking to personalize their vehicles.

Holley invests in R&D to drive continuous innovation to launch new and updated products. The company is seeking to enhance vehicle performance, fuel efficiency, and overall driving experience. The company has deep expertise in the segment, however, we question whether Holley is spending sufficiently to maintain its existing competitive advantage. This is partially due to the potential for under-funding, as R&D has fallen to 8% of revenue, but also as an absolute dollar value relative to significantly larger peers.

Holley has built a strong brand with a rich heritage in the automotive industry. Enthusiasts associate the brand with quality and performance, as well as a strong nostalgic feeling. This recognition has historically fostered customer trust and loyalty, allowing for repeat purchases and positive word-of-mouth marketing. We are concerned that the business is living off a heritage brand, lacking sufficient investment to push the brand beyond its niche.

Holley has an extensive distribution network that includes retailers, online platforms, and direct sales. This broad reach ensures its products are readily available to consumers worldwide, expanding its market presence and driving sales growth. The e-commerce segment is key as Holley can exploit its brand to drive superior economics by going direct to customers. Further, it allows customers to browse products, access technical information, and compare options.

Holley strategically acquires complementary businesses in the automotive aftermarket industry, accelerating this strategy in recent years in anticipation of its listing. These acquisitions not only expand its product offerings but also allow it to access new customers. The recent acquisitions have been a mixed bag thus far, with scale achieved but the company an operational mess. Management is currently switching focus to integration to address this.

Holley operates in the performance automotive aftermarket, a segment that has historically seen consistent demand, with less “lumpiness”. Enthusiasts and professional racers continually seek high-quality aftermarket upgrades and replacements, suggesting a reasonable level of underlying demand despite growth volatility.

The EV transition will likely be late to impact this segment of the industry given the enthusiast focus but it is impending nonetheless. We see minimal efforts to address this risk, with many products likely to see softening demand.

Finally, Holley faces stiff competition from significantly larger peers, with performance segments usually part of a larger OEM/Aftermarket producer. This allows them to benefit from economies of scale and shared competencies, a benefit Holley lacks. We see its brand as the key selling point but beyond this, we struggle to see the value proposition long-term as competition develops.

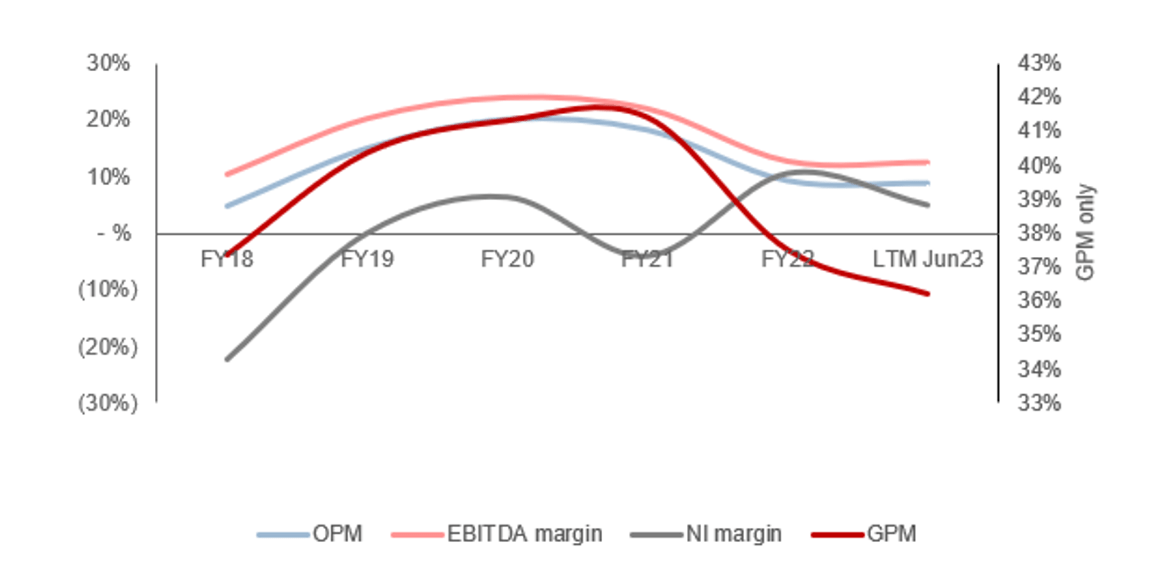

Margins

{kind=link}

Holley’s margins have been extremely volatile, with limited trading making it incredibly difficult for investors to assess what the normalized level of trading is. Broadly, industry trends imply macroeconomic conditions are contributing to inflationary pressures on the supply chain, as well as demand-side softening.

With these pressures unwinding, we suspect Holley can achieve a rapid improvement to an EBITDA level of 18-22%, although requires strong execution from Management which historical volatility implies may not be the case. Issues will come if Management seeks to universally cut costs, as Holley is known for its quality customer service. Further, the company must maintain, if not increase, its spending on innovation and marketing

Quarterly results

Holley’s recent performance has declined, with top-line revenue growth of (3.1)%, (14.3)%, (13.9)%, and (2.3)%. In conjunction with this, margins have materially deteriorated as we have observed, with two quarters of <10% EBITDA-M.

We attribute this to the current macroeconomic environment, with inflation and interest rates contributing to softening demand for its products. Consumers are experiencing an unprecedented attack on living costs, leading to reduced discretionary spending. This is having a knock-on effect on businesses, compounding the wider economic impact.

We are expecting conditions to worsen in the coming months, as the extended period of difficulty is leaving little room for maneuverability before conditions become untenable. Given Holley’s elasticity to weakening demand, we suspect this means greater struggles in the quarters to come.

Key takeaways from its most recent quarter are:

- Management appears solely focused on margin improvement following the significant dip in the prior year, with operational improvements and cost savings initiatives contributing to an Adj. EBITDA of 21.6%.

- There is a continued effort to streamline its operations, capturing synergies from recent acquisitions, and improving its supply chain and working capital management. The extent to which improvements have been achieved is impressive, although it makes us wonder what has been cut and how this will impact the long-term performance of the company.

- The company launched its Holley Sniper 2 EFI product line, a new product that is expected to generate renewed interest in the brand and reiterate its leading position within its community.

- Reduced inventory by $11.5m, although we question whether this is currently sufficient.

Balance sheet & Cash Flows

Holley’s balance sheet is bloated, with a ND/EBITDA ratio of 6.8x. This is significantly above a “healthy” level, with interest representing 8% of revenue and interest coverage of only 1.8x. The company has generated minimal FCF in the last few years (Avg. <$50m against a ND balance of ~$620m), which implies net deleveraging is going to be close to impossible in the coming years. Realistically, the company is hoping for rates to come down so it can perpetually refinance at better levels but this is unlikely. We believe this is a deal-breaking issue as it is likely irrecoverable.

Outlook

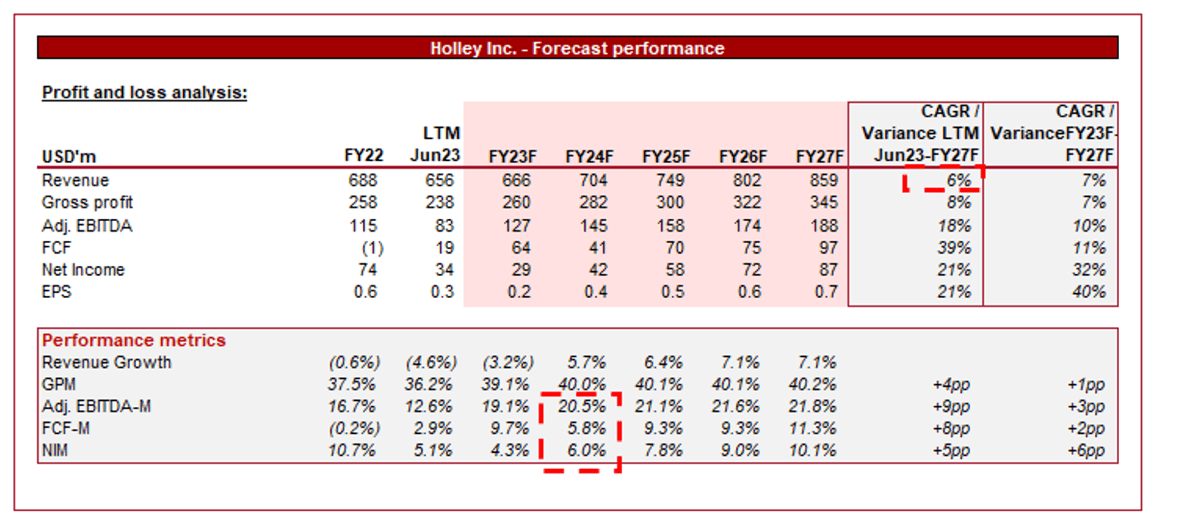

{kind=link}

Presented above is Wall Street's consensus view on the coming years.

Analysts are forecasting an improvement in growth, with a CAGR of 6% into FY26F. In conjunction with this, margins are expected to improve sequentially into FY24F before normalizing.

Given the limited historical trading at current market conditions, forecasts are inherently highly uncertain. We see very little in its niche business model to imply organic growth of ~6% is achievable, which means inorganic growth must be priced in. Further, we struggle to see margins normalizing at these elevated levels without competition offsetting.

Industry analysis

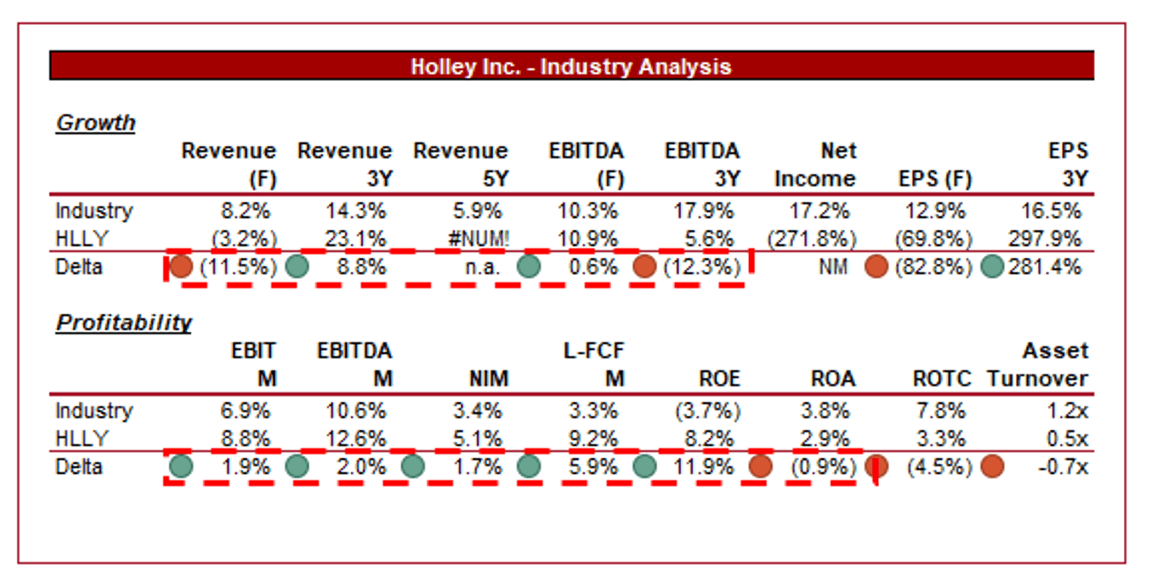

Auto Parts and Equipment Stocks (Seeking Alpha)

{kind=link}

Presented above is a comparison of Holley's growth and profitability to the average of its industry, as defined by Seeking Alpha (27 companies).

Holley performs surprisingly well relative to its peers. The company’s growth has outperformed its peers, although the vast majority of this is attributed to its M&A activity. When excluding this, the company’s organic growth is far less compelling.

This said, the company’s margins are genuinely superior to its peers, owing in part to its niche focus that allows for superior pricing relative to stock/generic products. This said, the company’s conversion of margins to FCF leaves much to be desired, reducing the value of these margins.

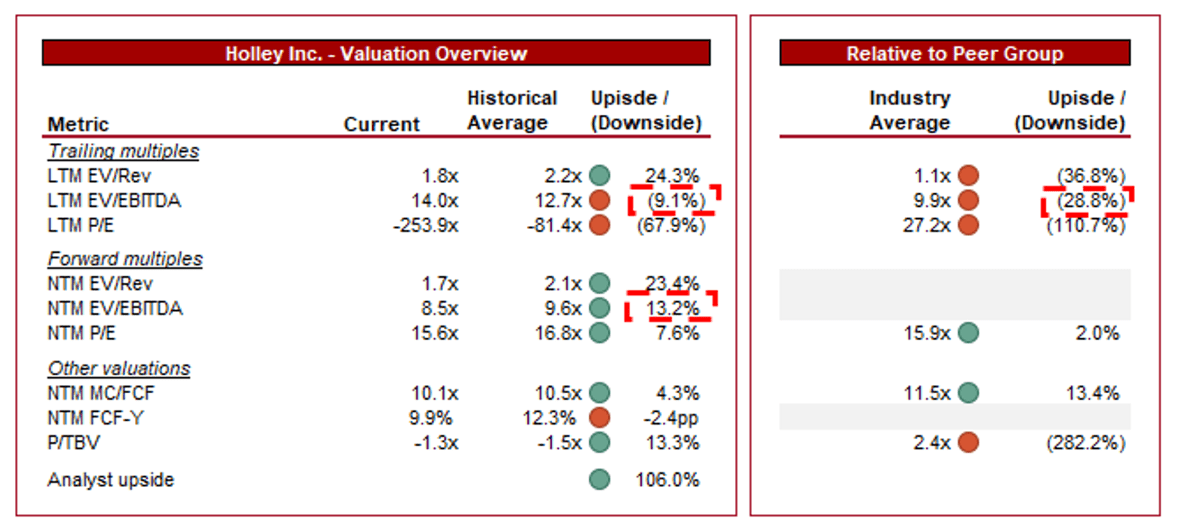

Valuation

{kind=link}

Holley is currently trading at 14x LTM EBITDA and 9x NTM EBITDA.

This current valuation represents a NTM FCF yield of 9.9%, which to some may appear extremely attractive. Our view is that most businesses trading about ~8% begin to have significant issues (markets do not price assets cheaply for no reason). Holley is on the higher end of the spectrum due to its debt balance and uncertain growth potential. For this reason, we would not consider ~10% to be attractive.

Further, Holley is trading at a ~29% premium to its peers on an LTM EBITDA basis and a ~13% discount on a FCF basis. We do not consider this premium to be justifiable in the slightest, with its FCF multiple inflated by WC unwind as Management seeks to aggressively unload stock. Although the company has margins on its side, that is its only advantage. The company lacks a true growth story and is not positioned for the EV transition in the way many of its peers are. Finally, only 3 businesses have a higher debt-to-equity ratio.

For this reason, we consider this stock overvalued and separately, faces headwinds that will likely cause share price pressure.

Key risks with our thesis

The risks to our current thesis are:

- Strategic partnerships to boost growth.

- Takeover by a larger peer seeking its margins and expertise.

- Efficient cost and WC management that will not compromise growth for superior FCF.

Final thoughts

Holley is financially and operationally a mess. The company has seen aggressive M&A, without sufficient forethought for the impact on the company subsequently. Integration efforts have been lacking and Holley is now irrecoverably burdened with debt. The only realistically way to deleverage is to grow EBITDA sufficiently to offset the ND balance, which appears unrealistically given its mediocre business model. We see very little positives with this business currently.

For further details see:

Holley: Weak Company With Only Problems Ahead