HEP - Holly Energy Partners: Fundamentals Keep Strengthening Despite Market Noise

2023-03-31 06:38:21 ET

Summary

- Holly Energy Partners ended 2022 with stronger financial performance in the fourth quarter.

- In fact, their operating cash flow set a new record, which provides momentum going forward into 2023.

- They continue deleveraging, and excitingly, management clearly articulated that higher distributions are likely forthcoming later in 2023.

- Despite the recent turbulence within capital markets and talk of a recession, their cash flow performance is resilient and should not see any significant impact.

- Thankfully, this should not derail their prospects for higher distributions, and thus given their high circa 8% yield, I believe that maintaining my strong buy rating is appropriate.

Introduction

Early in 2023, it seemed that the scene was set for higher distributions for the unitholders of Holly Energy Partners, L.P. (HEP), as my previous article discussed. Whilst yet to eventuate, the prospects are growing stronger after management more clearly articulated that such a move should be forthcoming, likely later in 2023. The last month saw turbulence in capital markets with banks collapsing, which may concern some investors but after consideration, thankfully their fundamentals keep strengthening despite market noise and thus, this does not derail the prospects for higher distributions.

Coverage Summary & Ratings

Since many readers are likely short on time, the table below provides a brief summary and ratings for the primary criteria assessed. If interested, this Google Document provides information regarding my rating system and importantly, links to my library of equivalent analyses that share a comparable approach to enhance cross-investment comparability.

Author

Detailed Analysis

{kind=link}

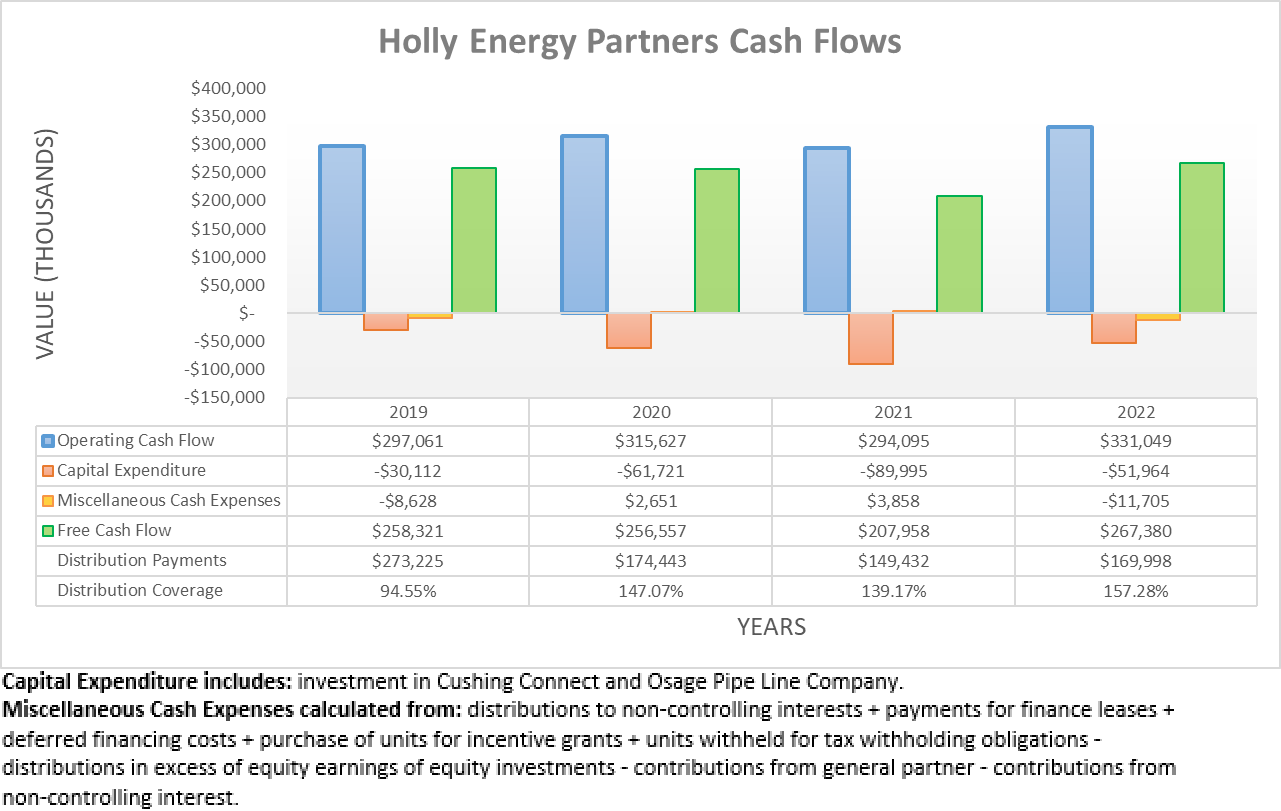

After seeing their cash flow performance improving throughout the third quarter of 2022, it was positive to see this continuing throughout the fourth quarter. Despite being weighed down earlier in the year due to higher turnaround expenditure as my previous analysis discussed, their operating cash flow still closed out the year at a new record of $331m, which represents an impressive increase of almost 13% year-on-year versus their previous result of $294.1m during 2021, as their Sinclair acquisition bears fruit. Once subtracting their capital expenditure of $52m and accompanying miscellaneous cash expenses of $11.7m as listed beneath the above graph, they generated $267.4m of free cash flow during 2022. Given their distribution payments of $170m, this provided strong distribution coverage of 157.28%, which sees plenty of scope to fund higher distributions going forwards into 2023.

{kind=link}

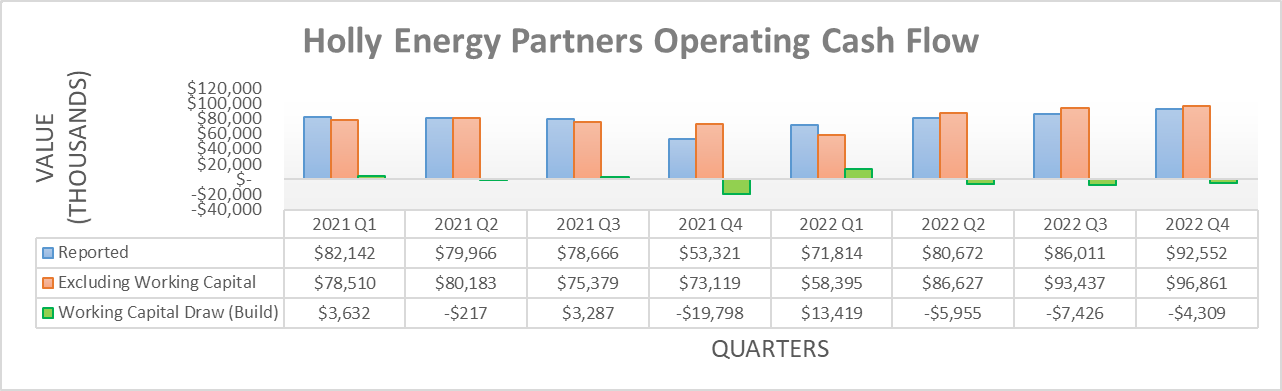

Upon looking at their operating cash flow from a quarterly perspective, it more clearly shows the fourth quarter of 2022 enjoyed stronger financial performance. Apart from their reported result landing at $92.6m that set a new record, their underlying result of $96.9m that excludes working capital movements also set a new record and therefore, provides momentum going forwards into 2023.

When conducting the previous analysis, their guidance for 2023 had just been released and based upon my estimations given their low capital expenditure forecast of only $37.5m at the midpoint, I foresaw very strong distribution coverage of almost 200%. Subsequently, there have been no changes to their guidance and thus the only new risk stems from the recent market turbulence coming on the back of banks collapsing, which in turn heightens risks of a recession or at minimum, weaker economic conditions.

Thankfully as a midstream subsidiary of HF Sinclair (DINO), they are detached from short-term economic conditions. The best example was during the severe downturn of 2020 whereby their operating cash flow was so resilient to the economic conditions that it even increased year-on-year to $315.6m versus its previous result of $297.1m during 2019. If their operating cash flow can defy what was arguably the worse headwind in decades without dipping, even a recession during 2023 should not cause any significant impact to their cash flow performance nor derail my previous estimations. If anything, their stronger financial performance during the fourth quarter of 2022 makes it more likely for my previous estimations to be exceeded.

Since they stand to generate ample excess free cash flow after distribution payments going forwards into 2023 given their prospects for very strong distribution coverage, it naturally circles around to the question of higher distributions that my previous analysis suspected would be forthcoming. Whilst so far, their distributions remain unchanged, the prospects are growing stronger with such a move being more clearly articulated, likely later in 2023, as per the commentary from management included below.

So fair to say incremental cash return is top of mind for us. And as we approach our leverage target over the next couple of quarters, we'll communicate what we're going to do in terms of incremental cash return to shareholders."

- Holly Energy Partners Q4 2022 Conference Call.

{kind=link}

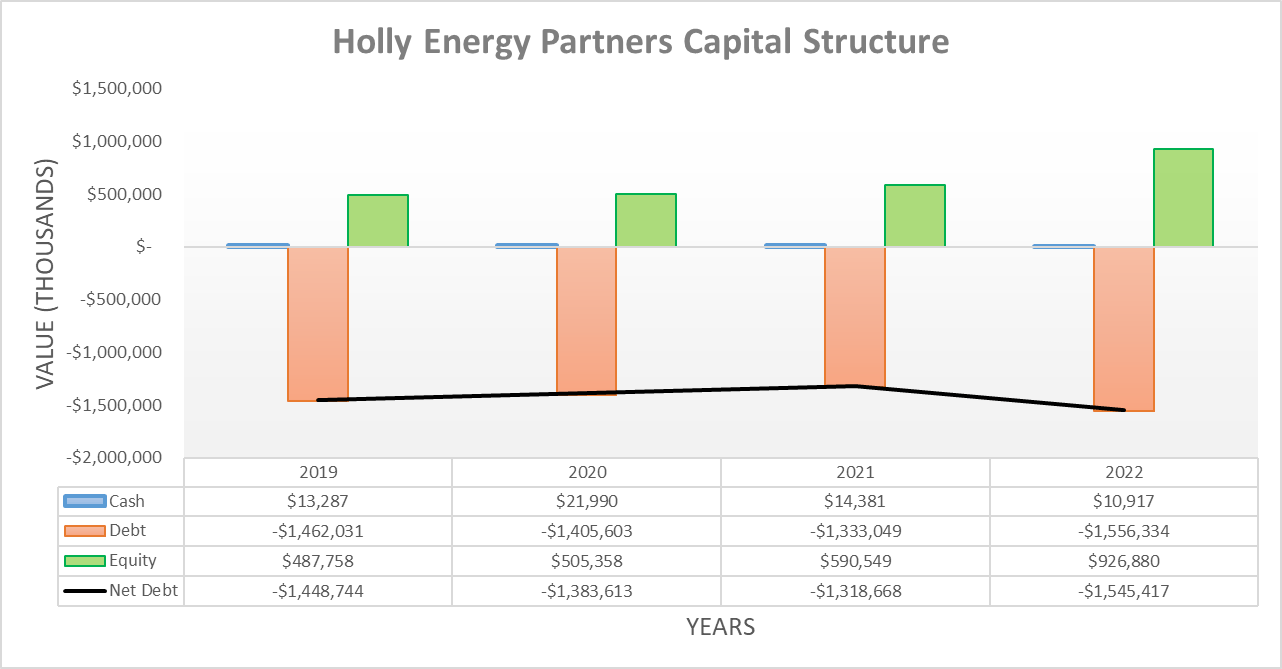

Thanks to their strong cash flow performance during the fourth quarter of 2022, their net debt continued trending lower as was evident when conducting the previous analysis. As a result, it now sits at $1.545b and thus represents a slight decrease versus its previous level of $1.578b following the third quarter. Whilst it ended 2022 around 17% higher versus its previous level of $1.319b where it ended 2021, this was due to their Sinclair acquisition during the first quarter of 2022, which my earlier article discussed in detail for anyone interested. Despite the possibility of further capital market turbulence, there are still no reasons to expect their net debt to stop trending lower going forwards into 2023 thanks to their aforementioned resilient cash flow performance and ample excess free cash flow after distribution payments. Although the extent will depend upon the timing and magnitude of their likely forthcoming higher distributions.

{kind=link}

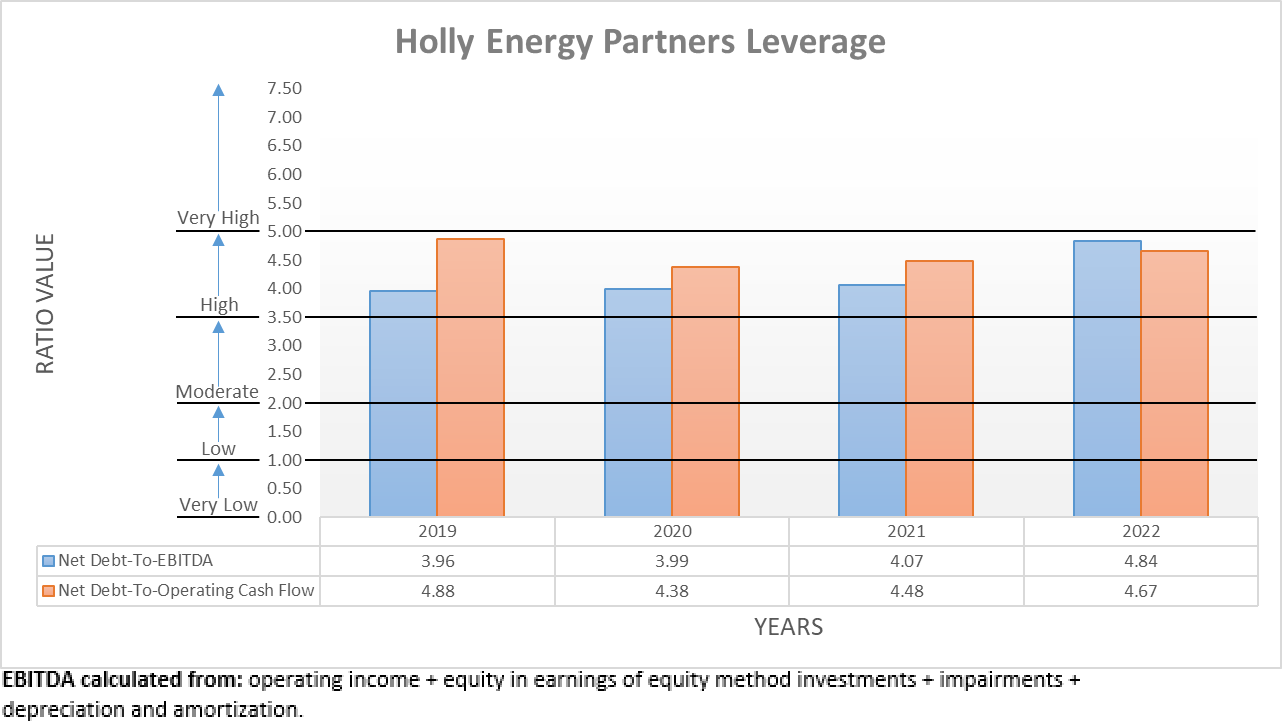

When lower net debt is combined with stronger financial performance during the fourth quarter of 2022, deleveraging is unavoidable with their net debt-to-EBITDA sliding down to 4.84 versus its previous result of 5.19 following the third quarter. Meanwhile, their accompanying net debt-to-operating cash flow also enjoyed a similar change, thereby sliding down to 4.67 versus 4.96 across these same two points in time, respectively. As a result, this now sees both of their results beneath the threshold of 5.01 for the very high territory and thus within the high territory of between 3.51 and 5.00. On the surface, this might still sound concerning to some investors but thankfully, their aforementioned resilient cash flow performance means their leverage cannot derail their prospects for higher distributions going forwards into 2023, especially as their net debt should decrease in tandem.

{kind=link}

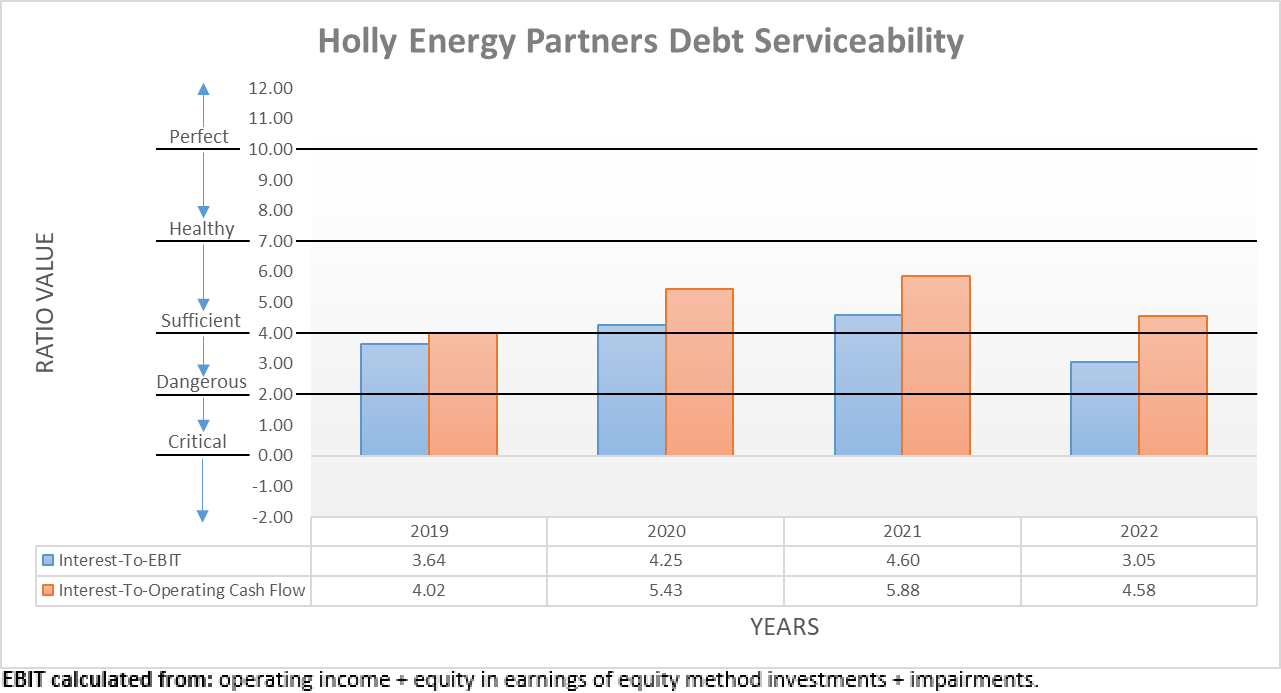

Similar to their leverage, their debt serviceability also improved during the fourth quarter of 2022 on the back of their fundamentals strengthening. As a result, their interest coverage is now 3.05 when compared against their EBIT versus their previous result of 2.70 following the third quarter, which is within the range that I consider sufficient. If compared against their operating cash flow, their interest coverage also improved with respective results of 4.58 versus 4.19 across these same two points in time and despite these being noticeably better and thus within the range that I consider healthy, I prefer to judge on the worse side.

Going forwards into 2023, this should continue improving alongside their leverage as their net debt is reduced, namely via repaying some of the $668m of drawings under their credit facility that carries a variable interest rate, unlike the remainder of their debt. Since this only amounts to circa 43% of their total debt of $1.556b, they are only partially exposed to higher interest rates if monetary policy continues tightening.

{kind=link}

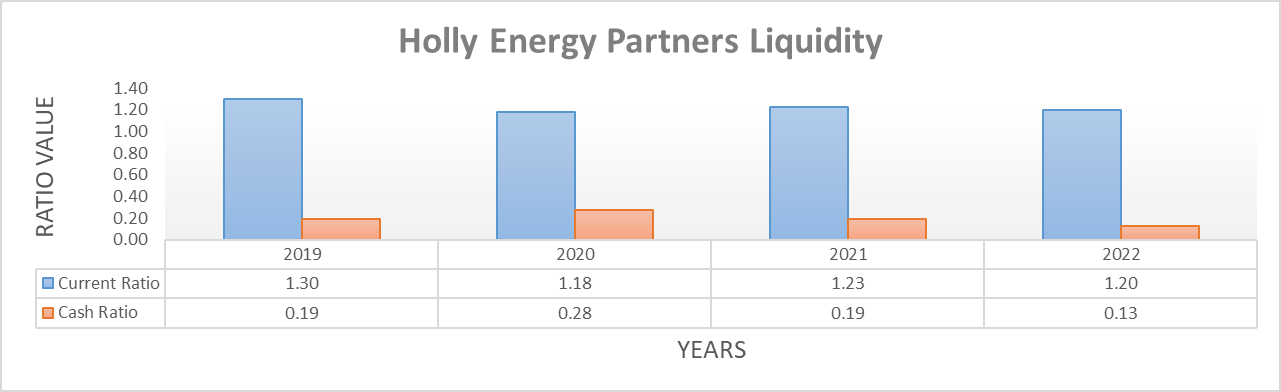

When it comes to liquidity, it remains strong following the fourth quarter of 2022 with their current ratio at 1.20 and equally as importantly, their cash ratio at 0.13. Even though leverage and debt serviceability are important in the medium to long-term, I feel that liquidity is actually more important ugh in the short-term, especially given the last month saw banks collapsing.

Whilst the situation is now calmer, risks remain but thankfully, as they generate ample excess free cash flow after distribution payments they are a net contributor to capital markets given their cash inflows outpace their accompanying outflows. When combined with no debt maturities until July 2025, it effectively isolates the company from the banking crisis as much as possible. Normally, it is not necessarily problematic to require access to capital markets but if the banking crisis were to reassume whilst monetary policy remains tight, access could be difficult and thus by extension, it could have otherwise created risks for their distributions.

Conclusion

Even though the recent banking crisis brought turbulence into capital markets, thankfully their resilient cash flow performance makes this nothing more than market noise. Furthermore, they ended 2022 with record-setting operating cash flow that provides momentum heading into 2023, whilst they continue deleveraging thanks to ample excess free cash flow after distribution payments. Now that management more clearly articulated that higher distributions should be forthcoming, it appears their fundamentals keep strengthening and thus I believe that my strong buy rating is appropriate.

Notes: Unless specified otherwise, all figures in this article were taken from Holly Energy Partners' SEC filings , all calculated figures were performed by the author.

For further details see:

Holly Energy Partners: Fundamentals Keep Strengthening Despite Market Noise