HOLX - Hologic: A Superb Steward Of Capital Offsets Top-Line Risks

2023-04-19 00:53:35 ET

Summary

- Hologic is a long-term cash compounder with an attractive value proposition.

- Here I demonstrate the firm's strengths going forward.

- Despite top-line pressures, findings show the firm's business economics are exceptional and can throw off large piles of cash to shareholders.

- Net-net, I reiterate buy at $173, revealing tremendous upside potential.

Investment Summary

After a polished 1st FY'22 quarter the bullish case for Hologic, Inc. (NASDAQ: HOLX ) has only strengthened in my opinion and I therefore reaffirm my buy rating on HOLX stock. I had reiterated my buy thesis in January this year, and since the latest firm's latest numbers, I believe there is tremendous value to be unlocked in this name.

As a reminder, I have been bullish on HOLX since November 2020. By dismantling the growth/value axis from an intelligent investors' perspective in the January publication, I advocated the company deserves to trade at high market multiples. As evidence, it boasts:

- Competitive strengths in its diagnostics and surgical businesses;

- Superb returns on capital at wide spread above the cost of capital;

- Ability to generate long-term economic profits for shareholders.

If you want profitability, operating leverage, and a low-volatility, long-term compounder, HOLX is one selective opportunity currently on the table, in my informed opinion.

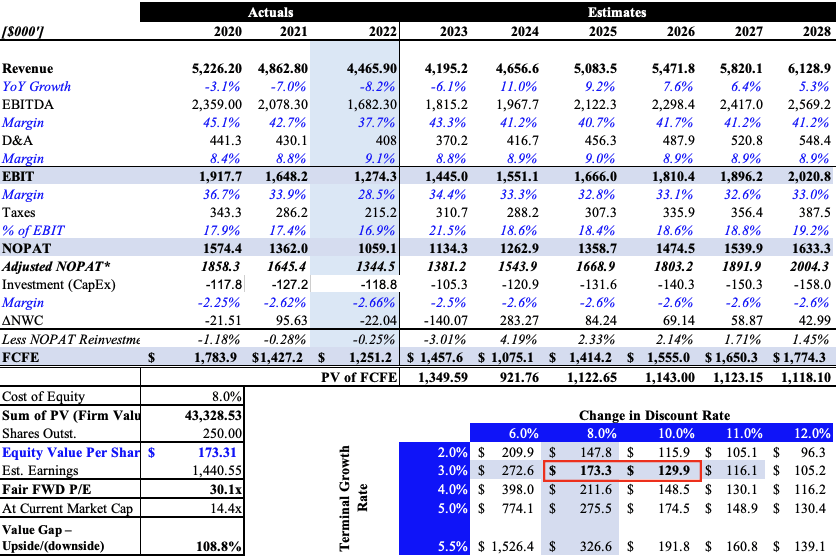

It is expected the company will see a pullback in revenue in FY'23. I think this is fair, and forecast a 6% YoY decline at the top. Yet, I am certainly not concerned. HOLX is a cash-generating machine with business economics that others can only strive for. Here I will show how the firm continues to be a long-term cash compounder with multiple avenues of investment to generate future shareholder value.

Despite the revenue downside, I believe this diagnostics behemoth can generate $1.4Bn in operating income and grow earnings by 20% in FY'23, to throw off $1.4Bn in free cash flow to shareholders this year. If my numbers are correct, expect the firm to expand ROE 7 points to 34% and drive 34% return on incremental capital over the next 3 years. This is now a company with far lighter capital requirements to maintain and grow operations. As such, the returns on capital could be stellar and generate equally as strong returns for shareholders.

As I will demonstrate, the earnings power and operating leverage HOLX possesses are simply too reflexive to ignore. It is therefore a steal priced at 17x EBIT and 22x non-GAAP earnings. My forward-looking assumptions have the stock priced at $173 or 30x P/E on a market capitalization of $43.2Bn. Net-net, I reiterate HOLX as a buy.

Fig. 1 – HOLX stock price performance since October 2022

Data: Updata

HOLX a tremendous generator of cash

The last two years have been filled with ups and downs throughout HOLX's operations. On a trailing 12 month basis, at quarterly intervals from FY'20, revenues peaked in March of 2021, and have been lumpy since.

Despite the obvious top-line pressures, after reading the bullish points below, I am sure the strengths of HOLX's business economics will be abundantly clear for investors to reason by.

One, the firm booked $560mm in diagnostics turnover in Q1 FY'23 annual results [a $2.24Bn run rate]. This was a 41% YoY decline. I am not concerned by these numbers though – ex-Covid revenue, organic diagnostics sales climbed nearly 16%. The differential was expected, given the obvious Covid rebound. Diminishing Covid revenues are actually good thing, 1) because they are lower margin segment, and 2) due to the inventory mark downs in Covid-related PPE and diagnostics.

It's important, therefore, to think in first principles – revenue downsides have been expected. Hence, capital intensity/productivity, profitability and cash flow that are the most important numbers to gauge.

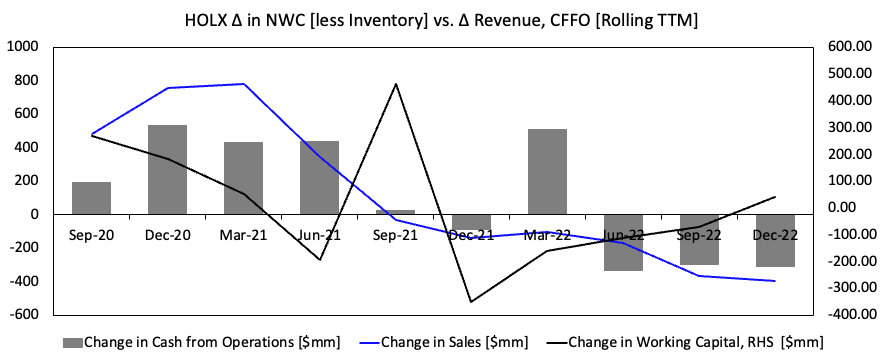

In that vein, consider the following points [observed in Figure 2, Figure 3]:

- As revenue has crept lower, HOLX kept cash collection high and didn't see cash flows crimp until Q4 FY'21.

- This is evidenced from favourable changes accounts receivable, providing more cash to the firm.

- It generated $1.8Bn in trailing cash from its operations during Q1 FY'23, and with negligible Covid-related receivables this year, I project HOLX to generate $1.6Bn in CFFO, driving to $1.8Bn in FY'24. This is $800mm–$1Bn above its pre-pandemic range.

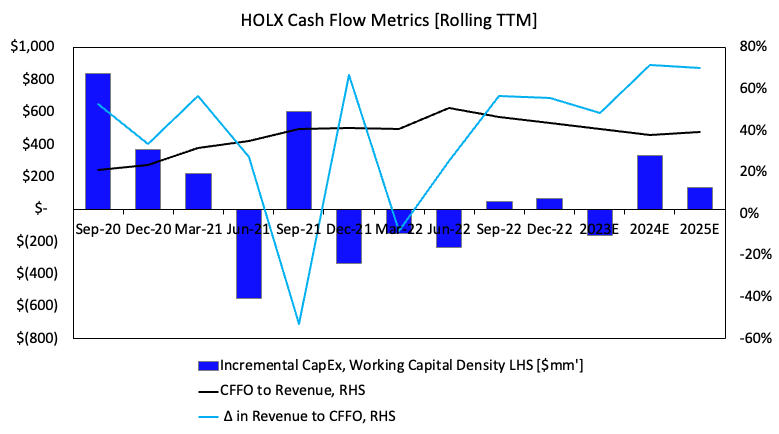

Two, the percentage of CFFO to revenues has also been increasing since FY'20, and could remain at c.40% or turnover over the coming periods – more than double pre-Covid times. Further, measuring the change in revenue related to CFFO, it averaged above 50% in this time, and my numbers indicate this could stretch to >60% by FY'25. Revenues are heavily backed by cash, therefore.

Fig. 2

{kind=link}

Fig. 3

{kind=link}

Three, HOLX possesses tremendous operating leverage. This is positive to owner earnings looking ahead. The firm has averaged 2x–2.6x operating leverage since FY'18 and FY'20, (on both an annual and TTM basis respectively), [Figure 4]. Meaning that, with a 6.1% YoY decline in revenue this year, my forecasts still expect the firm to generate $1.4Bn in operating income on a 34% margin. Quarterly OpEx was relatively flat at $340mm in Q1 FY'23, and I project annual OpEx to remain flat at $1.39Bn this year as well, and the firm could generate $1.1–$1.2Bn in post-tax earnings on these assumptions.

Fig. 4

Data: Author, HOLX 10-Qs

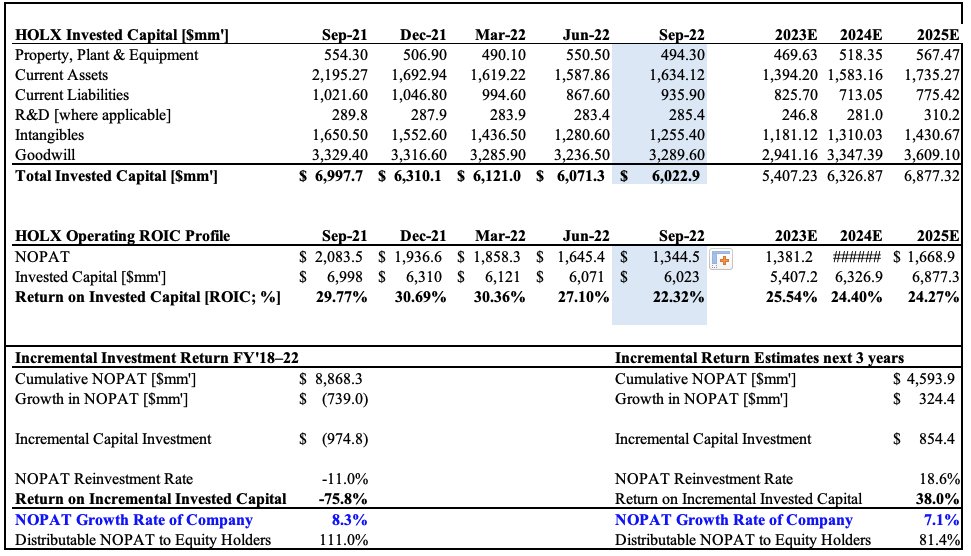

Four, as investors, we want to buy companies that quickly and boldly reinvest capital toward value-creating growth. The best companies can generate the same high return on invested capital ("ROIC") and reinvest greater amounts each year. This is precisely where HOLX excels.

With the pullback in Covid-related turnover, HOLX has done a terrific job in reducing capital requirements to maintain its existing level of operations. In other words, capital productivity is likely to increase. Incremental CapEx and NWC density are below pandemic ranges [Figure 4], resulting in a more capital efficient company. Meaning, HOLX can throw off piles of cash to shareholders. This could generate $1.45Bn in free cash to shareholders/owner earnings in FY'23 in my estimation [Figure 7].

A few points to emphasise this:

- Over the last 3 years, HOLX has consistently generated 20–25% TTM ROIC each quarter since FY'20.

- This, as incremental the level of capital invested increased >$500mm over the same period.

- Looking ahead, the capital density is lighter, yet estimates point to HOLX generating $4.5Bn of cumulative NOPAT into FY'25, with an additional $324mm on the top of FY'22 [Figure 5].

- But, it is projected to invest another net $850mm, or net $283mm per year on average, hitting $6.8Bn in total capital invested in FY'25.

- This equates to a consistent 24–25% return on capital whilst the amount of capital invested is increasing.

- This is an incremental return of 14–17% per year as well.

- At an 8% hurdle rate (HOLX current WACC), there is immense economic profit to be pulled from this company [Figure 6].

The return on the incremental capital equates to 38% over the three years with my numbers, after reinvesting 18% of post-tax earnings. Hence, HOLX can reinvest at 18% for a 38% return. These are exceptional outputs that tell me HOLX is primed to ratchet up capital productivity in the periods to come.

Fig. 5

{kind=link}

Here we have firm that could invest an additional net average $283mm in new capital over the next 3 years, and generate 20–25% return on principle per annum:

- $1.35Bn profit off $5.4Bn in invested capital,

- $1.57Bn profit off $6.3Bn, then

- $1.7Bn profit off $6.8Bn in FY'25 (should my numbers be correct),

- And so on.

To demonstrate how important I believe this is to HOLX trading at higher multiples, I've plotted the forecasted owner earnings, i.e., FCF less frictional costs [reinvestments for maintenance and growth] against the projected net earnings from FY'20 out to FY'25E. You can observe the ?100% conversion of owner earnings from reported earnings in each year, a trend I envision to continue.

There simply is no better form of business economics to generate shareholder value in my estimation.

Profits don't have to be put back into the business. HOLX is a firm that has multiple investment opportunities to generate c.20-25% return, meaning will likely be doing so in my opinion. Hence, three things:

- HOLX will explore multiple growth opportunities, and the track record speaks for itself.

- The capital HOLX allocates each year provides surplus cash that can be reinvested into growth, versus the bulk of profits.

- Thereby preserving cash to shareholders.

This is exactly the kind of business I want to be in.

Fig. 5a

Data: Author, HOLX 10-Qs

Fig. 6

Data: Author, HOLX 10-Qs

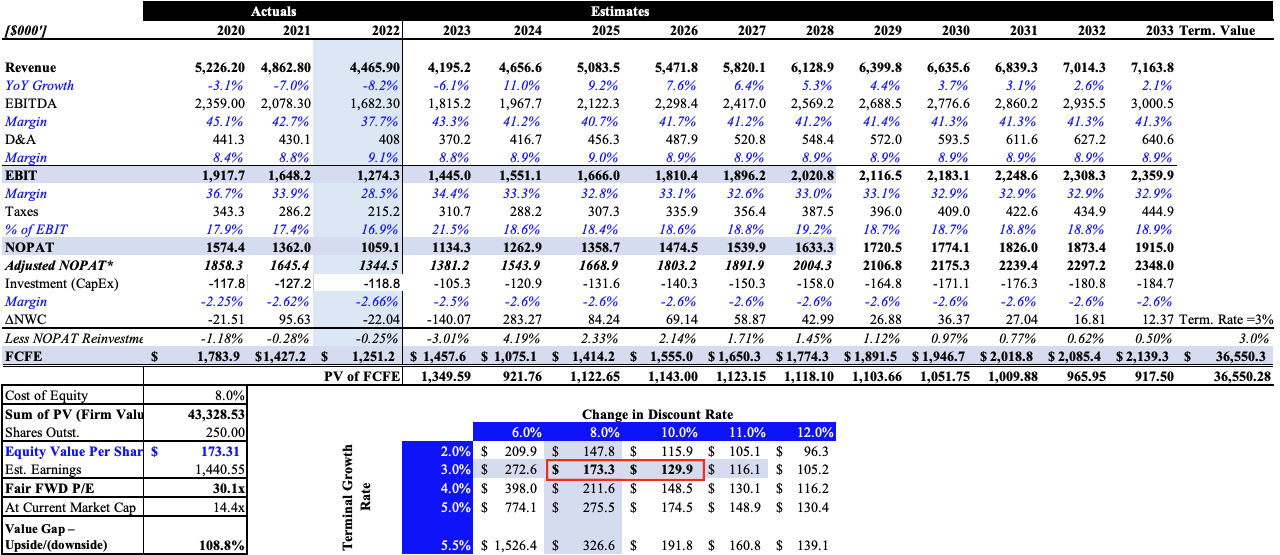

Valuation and conclusion

It is borderline offensive to see the market value HOLX at just 22x forward earnings and 17x EBIT. Given the superb economics of its capital allocation and capital productivity, the market is severely undervaluing the stock at these multiples in my opinion.

I have mentioned the firm could throw off $1.45Bn in owner earnings this year. This, underlined by a thinner NWC density and smaller incremental CapEx versus years prior. Hence, there is more cash available for shareholders. I also project to see incremental returns on capital and grow revenues in-line with long-term ranges in the years to come.

My conclusions on HOLX's valuation are therefore as follows [Figure 7]:

- Projecting the owner earnings and discounting these at 8% values HOLX at $43.3Bn, otherwise $173 per share, nearly double market value.

- At the current market cap, the market has priced the firm at 14x my FY'23 estimated earnings.

- This pales in comparison to my numbers that show it fairly valued at 30x forward earnings.

- Baking in further risk with a 10% hurdle rate, the stock is valued at $130 with these outputs [see: sensitivity table in Figure 7].

Hence, I am buying HOLX at any multiple below this, and the current 22x earnings looks deliciously cheap given these forward estimates.

Fig. 7

{kind=link}

Consequently, I firmly believe there is tremendous value yet to be extracted from HOLX over the mid-term. If the growth and ROIC assumptions presented here are 80% correct, this points to strong earnings growth and profitability for the company, which investors could reward very handsomely.

In summary:

- HOLX is drifting away from its Covid-related growth percentages.

- Given the firm's operating leverage, increases in revenue should translate to strong turns in operating income.

- In terms of economic profitability, HOLX's capital productivity, smaller NWC base and business economics could see it generate 20–25% ROIC (and above the hurdle rate) as it invests into new growth capital.

- This would throw off large piles off cash to owner earnings and create substantial value for shareholders looking ahead.

Net-net, I believe the firm is valued fairly at $173 or 30x forward earnings, but also see value up to the $130 mark depending on the hurdle rate used. Reiterate buy.

Appendix 1: HOLX Long-term P&L, owner earnings forecasts

{kind=link}

For further details see:

Hologic: A Superb Steward Of Capital, Offsets Top-Line Risks