HOLX - Hologic: An Underappreciated Gem With A Bright Future

Summary

- Price action for HOLX has remained stagnant for the last two years, but underlying business metrics have remained strong.

- Hologic has put the cash windfall from COVID to good use with recent acquisitions that can boost future growth and diversify earnings across different segments.

- Current pessimism about the stock price is short-term thinking at its finest; the best opportunities are hidden in such situations.

Investment Case

Underscored by the recent earnings, Hologic's ( HOLX ) business has remained strong despite a slowdown in COVID-19-related business as the core revenue is diversified within Diagnostics and across Surgical franchises. "Growth through acquisitions (inorganic growth)" is a widely used strategy of using excess cash to acquire companies which would serve to boost the company's growth in the years following the acquisitions. For Hologic, this inorganic growth strategy has entered a new iteration, and although near-term revenues are forecasted to trend down due to a decline in the COVID-19-related sales, barring any missteps, the acquisitions should serve the company well over the long term.

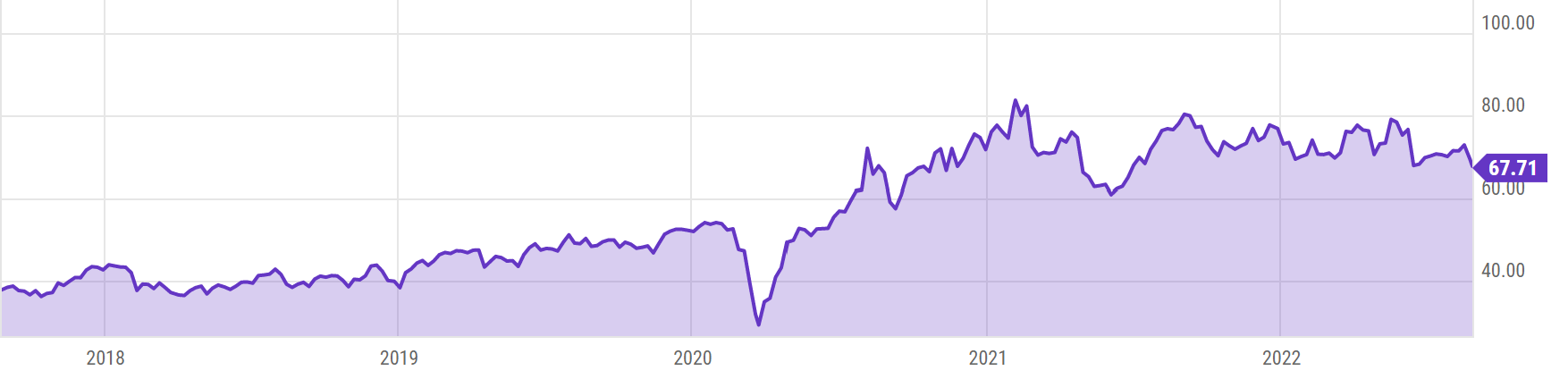

Stock Price Action

5 Year Price Action (Y charts)

{kind=link}

The stock has climbed an impressive 76% over the last five years but has remained largely flat over the last two years. The biggest gain in the stock price came in the late 2020 and early 2021 which was the result of the market reacting favorably for the strength shown by the company's diagnostics segment from COVID-19 related business. Since then, stock has exhibited a 18% drawdown from its peak and remained mostly flat for the last two years. This could be attributed to the fact of COVID-19 induced growth being over and the market being unsure of the source of future growth. In such situations, there are a few questions I ask myself. What has the company done with this cash windfall? How efficient is the company in replacing its COVID-19 revenues? How well is the revenue diversified in the absence of COVID-19-related revenues? Has the market overlooked a case for future growth?

Unpacking the full investment case

Hologic is a medical technology company that currently operates across four segments - Diagnostics, Breast Health, GYN Surgical and Skeletal Health. Over the last decade the company has been able to offer a wide array of premium diagnostics products, medical imaging systems, and surgical products primarily focused on improving women’s health. The snapshot below is a quick representation of the wide portfolio of products offered by the company.

{kind=link}

Focus on women's health

Hologic has been making women's health as one of the primary focus of their business over the last decade. In breast health alone the company offers 31 different products geared mostly towards breast cancer care and another 22 products focused on gynecological health. More recently the company started "Hologic Global Women's Health Index" a multiyear initiative on a global scale which will serve as a key input for the company to answer some of the most pressing questions in women's health. The data could also aid the company to develop the next wave of products and/or improve business related to women's health all over the world.

Revenue History and Cash Utilization

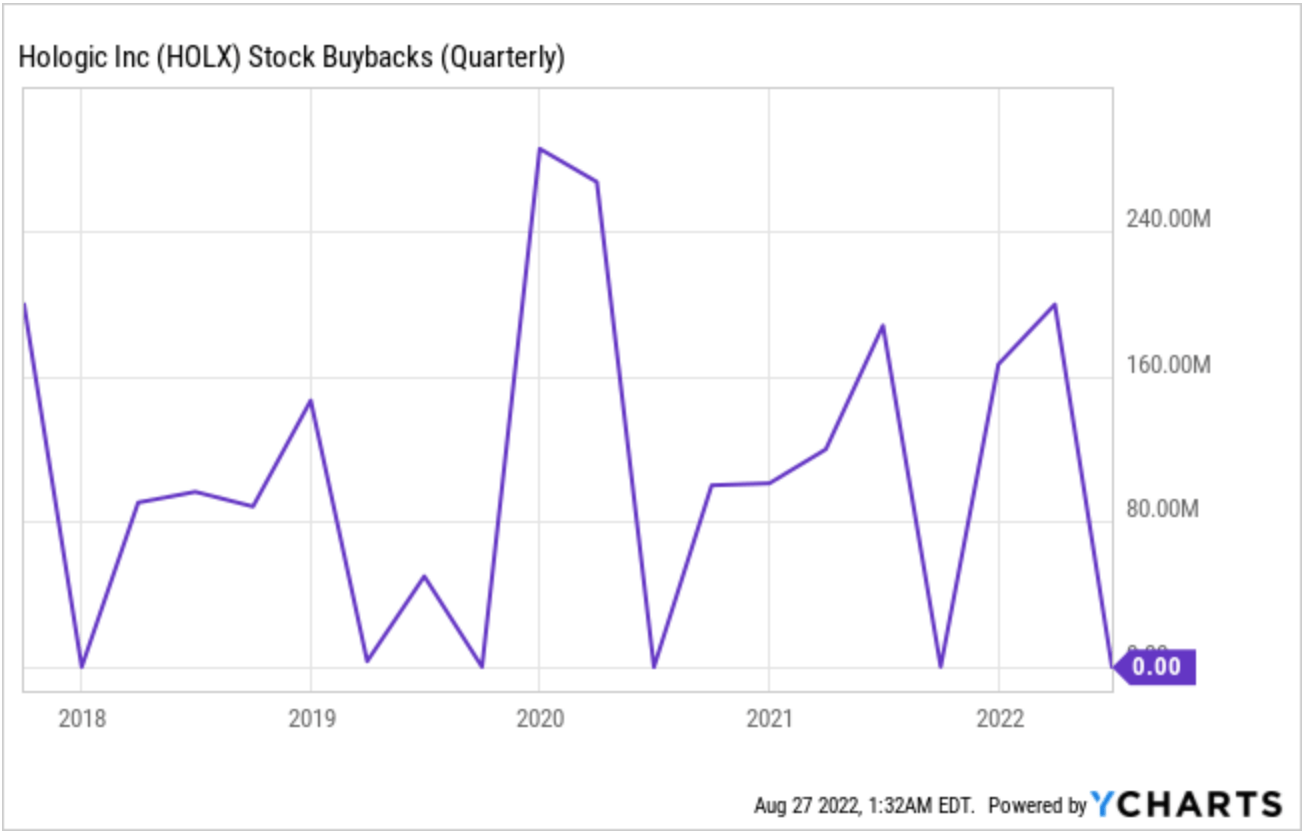

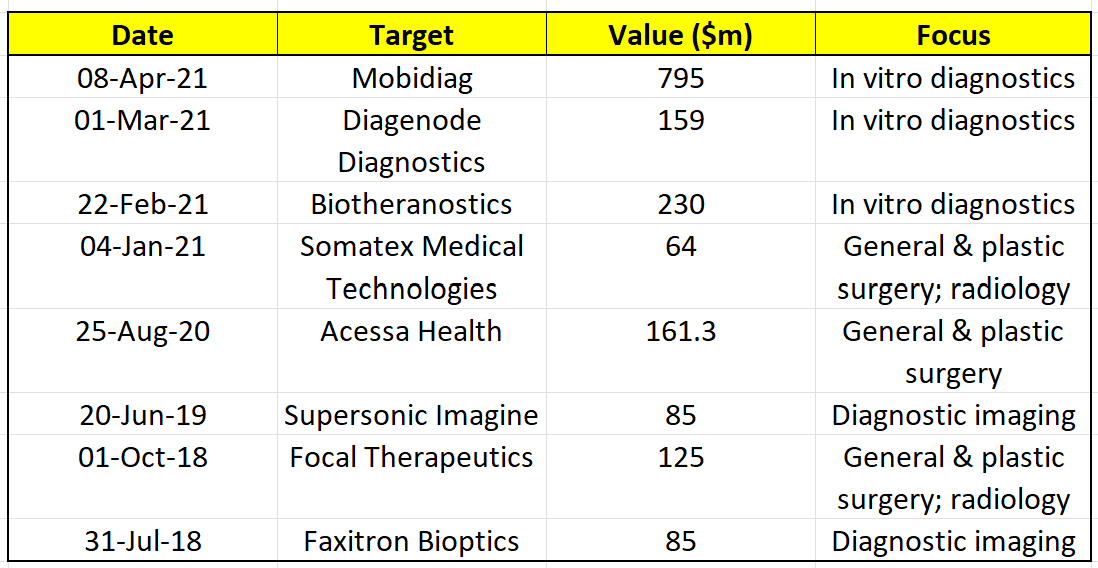

Average revenue growth from 2015 - 2019 stood at 6%. During fiscal 2020, COVID-19 impacted sales from two of its segments (Breast Health and GYN Surgical) but this was greatly offset by the boost in revenues that came from SARS-CoV-2 tests in the diagnostics division and this trend continued well into 2021. As a result, for FY 2020 and 2021, growth in revenues came in at 12% and 46% respectively. Management has put its cash to work in these two years primarily through stock buybacks ($850M+) and acquisitions ($1.2B+). The goal of each acquisition is to drive the topline growth while diversifying the core business.

Stock Buyback - 5Year History (YCharts)

{kind=link}

Acquisitions (>$50M) - 5Year History (Company data collected by Author)

{kind=link}

2022

For all quarters of 2022, the boost in the cash flows and revenues provided by COVID-19 understandably started to decline. However, an important thing to note is that the company not only sells tests for COVID-19 but also diagnostic systems (Panther) that processes these tests. The advantage here comes from the fact that these systems can also be used to process a broad menu of non-COVID tests. The installed base of Panther systems grew over 75% during the pandemic and over 250 systems were placed so far for fiscal 2022. This will drive the next wave of future growth as COVID got these systems foot in the door but they will be continued to be used for other testing purposes. The company has seen further evidence that most of their customers (?90%) use the systems for at least one other test.

For Q1 2022 , QoQ Revenue decreased by 8.6% but excluding revenue from COVID-19, organic revenue for the quarter grew by 9% (excluding COVID-19, growth was observed across all of company's core segments)

For Q2 2022 , QoQ Revenue decreased by 6.6% compared to the prior year period which was expected due to decreased sales of the company's COVID-19 diagnostic tests. Excluding revenue from COVID-19, the company showed growth in certain segments and mostly failed in Breast Health segment due to two main reasons -

- Semiconductor chip shortages

- Dip in the utilization of healthcare early in the quarter due to COVID-19 Omicron variant

For Q3 2022 , QoQ Revenue further declined by 14.2% again due to decreased sales of the company's COVID-19 diagnostic tests. Excluding the revenue from COVID-19, company showed growth in certain segments and mostly failed in Breast Health segment primarily due to semiconductor chip shortages. Global revenue for acquired businesses showed significant growth for the comparable quarter and will be included in organic revenue guidance starting a year after the acquisition. The earnings observed so far in fiscal 2022 have demonstrated that the company is slowly but surely replacing its COVID-19 revenues and the acquisitions will further ensure that growth is well diversified across all of its segments.

Is this a good time to get in?

To answer this question, I have used levered discounted cash flow analysis. Step I - Forecasting our cash flows for the next five years, I have used the guidance provided by the management for fiscal 2022. Management projects revenue to drop about 15% but expects cashflows to remain strong. The revenue drop is to continue on to 2023 as the COVID-19 test related business is more than likely to drop off completely. This will be met with the acquisitions beginning to make a significant impact on top line growth. So let us assume a revenue drop of 12% going into 2023 and we arrive at a revenue of $4.2B. In fact, if we had removed COVID-19-related revenue growth from 2020 and compounded revenue annually at a rate of 6-7%, we would have arrived at a similar number for 2023 (7% is the average revenue growth for the five years prior to 2020). From 2024 onwards let us again project a growth rate of 6% (5 - 7% is the projected long-term organic growth rate given by management).

Operating Cash flow as a percentage of revenues is expected to remain strong for 2022 (we will also use what we have learnt from the first three quarters of 2022 and assume that the number will at least remain the same for 2022) and take the average rate of the last five years for projecting this beyond 2022. For capital expenditure we will assume the average rate of last five years (-3.44%) until 2026.

FCF Projection (Author's projection using company data)

{kind=link}

Step II - Next step is to find our Weighted average cost of capital. We are setting a value of 3.25% for our risk-free rate (current 30Y treasury yield ) and our Market Risk Premium comes out to be 4.05% (Market Risk Premium = 30Y real returns of the stock market - risk free rate) (7.3% - 3.25%) giving us ((WACC)) at 6.73.

WACC (Company data and Author's Calculations)

Step III - Plugging this number ((WACC)) for our Free Cash Flow build-up gives us the sum of present value of the leveraged Free Cash Flow at $6.12B.

FCF Buildup (Company data and Author's Calculations)

{kind=link}

Step IV - Calculating the Terminal value using growth in perpetuity method with Long-term growth rate at 2% gives the present value of terminal value.

Present Value of Terminal Value (Author's Calculations)

Step V - At the final step, we calculate the intrinsic value and compare this against the current market price. The gap (-32%) we observe indicates to us that this stock is undervalued and there is a very strong case for buying at these levels.

Intrinsic Value (Company data and Author's Calculation)

For valuation analysis, I have used Levered DCF model, as this is done after the company has met its financial obligations and shows how much operating cash flow a business has to expand (From a continued future profitability standpoint we have also seen the company's pattern of using its cash to fund acquisitions to expand into new areas). In our analysis, we have been conservative in our revenue growth rate and OCF growth while forecasting our cash flows (Step I). Management in the past few quarters has been able to beat its own forecast and going forward the topline growth may come well above what we have included in our calculations. This would only increase the intrinsic value and make our buy case stronger. On the flip side, any missteps from the company that affects the topline growth can adversely impact our intrinsic value thereby making our buy case weaker. Also, for calculating Market Risk Premium in Step II, we have used 30Y real returns until 2021. A continued downturn in the stock market would push our Market Risk Premium lower which would again increase the intrinsic value. On the flip side, a continued downturn in the stock market may come at the cost of tightening monetary policy (increases Risk-Free rate) which would decrease our intrinsic valuation on the stock making the buy case weaker.

Risks/Challenges

When it comes to the biggest challenges for this company I remember the oft repeated quote - "The worst enemy you can meet is yourself". Let me explain. The company has played the acquisition playbook several times throughout its history and there have been instances where these have led to disastrous outcomes. The most recent example of this being the acquisition of Cynosure which it purchased in early 2017 for $1.7B in cash. The unit underperformed and greatly missed its forecasted sales which led to Hologic getting rid of the unit in 2019 for $205M. Rewinding to 2012, Hologic acquired Gen-Probe for $3.75B. This acquisition was expected to increase EPS the following year and accelerate Hologic's growth rates. None of the management's expectations came true which led to a $1.1B goodwill impairment charge recorded in 2013.

It could be a real possibility that the recent acquisitions made by Hologic would not play out as expected and lead to a write down of the acquired business. Also, management could put more of its cash to work to acquire more businesses which again may not play out as expected. In any of these situations, the expected growth in business that could counter the decline in revenues in 2022 and 2023 may not materialize which could put our thesis into question.

Closing Thoughts

Hologic's main focus of business is women's health and with the decline of COVID-19, their base business strengthens. The rise of COVID-19 was serendipitous as the company was able to answer the world's needs for highly reliable molecular COVID-19 testing which greatly strengthened the company for the future. From the company's Q2 release -

Our performance is a direct result of the planning and investments we made throughout the pandemic to strategically strengthen our business. We are a stronger Hologic through portfolio diversification, the addition of multiple growth drivers into our franchises and continued growth in our international businesses..

In terms of total addressable market for women's health, there are over 3.9 billion women in the world with a fraction of this in the United States (170 million), which is Hologic's largest market today. Hologic's technology has the opportunity to impact more lives around the world.

With such a strong financial position, management's history of strategic use of cash and a bright future, Hologic feels like an underappreciated gem at its present valuation. In the coming weeks, I will be initiating a long position in HOLX and hope to benefit from its performance in the future.

For further details see:

Hologic: An Underappreciated Gem With A Bright Future