HOLX - Hologic: Post-Covid World Proving To Be A Nuisance On Profitability (Rating Downgrade)

2023-09-13 08:00:00 ET

Summary

- The latest investment findings suggest a revised rating of "hold" for Hologic, Inc.

- HOLX needs catalysts such as sales growth, higher profits, or valuation factors to drive its stock price higher.

- The company's COVID-era sales and profits are declining, and the rate of earnings produced on capital deployed has taken a hit.

- Net-net, revise to hold.

Investment briefing

In the last publication on Hologic, Inc. (HOLX), it was noted: "If new data arrives, to suggest [the rating] needs revising, it will be done...". Based on the latest investment findings, it would appear the data has changed in the short-term. This report will unpack the latest investment updates for HOLX, depicting why I've revised the rating to hold for now. HOLX needs a set of catalysts to price higher in my view, either (i) fundamental or economic catalysts [sales growth, higher profits on capital employed], (ii) sentimental changes, in revisions, technicals or options-data, or (iii) valuation factors.

The stock sells at 18.6x forward earnings and ~15x forward EBIT whilst offering up a 7% forward cash flow yield. Based on factors raised here, these may be on the higher end of the price matrix. Plus, HOLX's COVID-era sales/profits are diminishing sharply, despite higher capital intensity and asset heaviness. These are factors which likely contributed to HOLX selling lower this year in my view. (We should also take into account the potential distractions that HOLX's CEO's acceptance of Illumina (ILMN)'s chair of the board could cause. He has attempted to address any concerns about this, but it's still something that may weigh on investors' minds).

Readers of this channel will know we are investing in companies that will be rewarded or punished based on their long-term economic characteristics. As outlined here, this is a headwind for HOLX at present. Net-net, revise to hold.

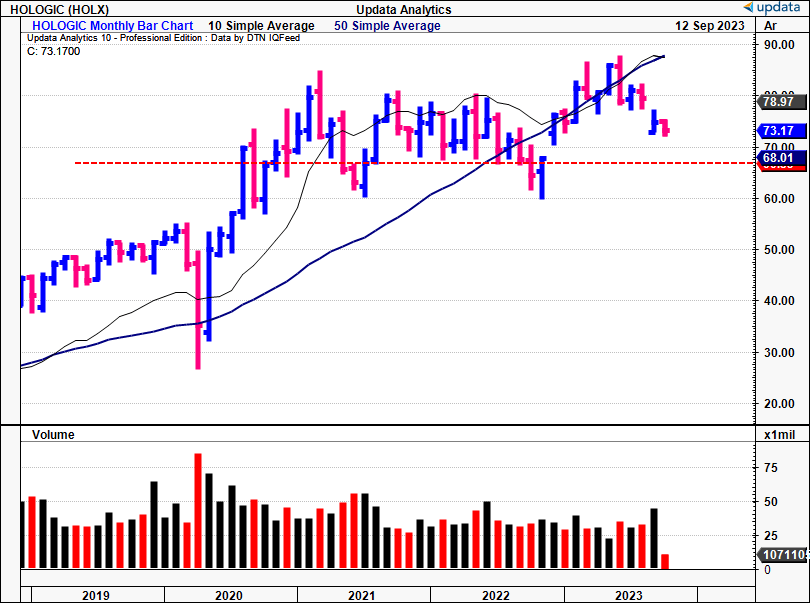

Figure 1. HOLX Monthly Returns, trading above 2020-'22 range

{kind=link}

Critical facts forming revised thesis

1. Review of latest numbers

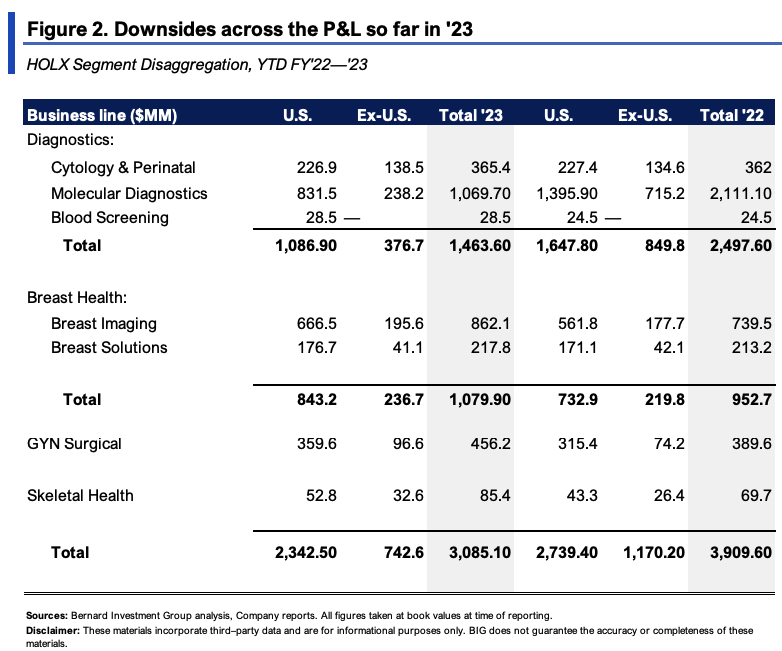

HOLX put up Q3 revenues of $984mm , which surpassed internal expectations [note: HOLX reported its Q3 FY'23 numbers in July, corresponding to Q2 CY 2023. For consistency and simplicity going forward, I'll be speaking in terms of Q3 unless otherwise stated]. It pulled this down to core EBITDA of $308mm, on earnings of earnings of $0.93/share. Momentum has been largely flat for the YTD, with downsides across the P&L [as seen in Figure 2]. Management raised full-year guidance ever so slightly to $3.995Bn-$4.035Bn in sales, calling for ~17% downside at the top. It is eyeing earnings of $3.87-$3.94 on this, around 35% YoY decline at the midpoint. It's already clipped $2.52Bn this year to date, so it expects $1.48Bn in turnover for Q4 to hit the upper end of forecasts.

Note: Not all revenues are shown, hence, "total" doesn't fully reflect the full set of revenues for the year. Only segment revenues are shown.

{kind=link}

Interesting trends were observed in the divisional breakdown of the quarter:

- The Diagnostics division led a decline of 21.3% in sales to $1.09Bn, but this was mainly due to lower COVID assay and ancillary revenues. Expect this normalization for the rest of '23. When excluding the COVID-factors, the division actually grew 11.8% YoY.

- Molecular Diagnostics (part of the diagnostics business), grew by ~13% during the Q3 (ex-COVID). It was down 22% YoY with all factors included. The Cytology and Perinatal business also had a good performance without COVID-sales, up ~10% YoY. But-and very importantly-I would thoroughly stress this level of growth may not be sustainable in the future. Management even advised "not to extrapolate this level of growth going forward to our Cytology and Perinatal segment" on the call.

- The breast health division booked quarterly revenues of $360.3mm, growing 27.5% from Q3 last year. This growth is particularly notable in my opinion because it builds on strong Q2 numbers and is good evidence of the demand building in this segment. I would state that last year was a difficult comps in breast health given the supply chain fiasco and the impact it had on lead times and so forth. But the increasing predictability of HOLX's semiconductor chip supply is a positive sign for breast health sales. Its surgical division put up Q3 revenues of $157.3mm, up c.15% YoY. Recent acquisitions to expand its laparoscopic footprint look to be paying off, based on these growth percentages. Management expects double-digit growth in surgical for FY'23.

- Lastly, the skeletal business did $27.1mm of business in the quarter, a robust 25% increase. So it would appear the breast health, skeletal, and surgical offerings would be the three business lines to keep watch of moving forward. In my view its diagnostics business will continue to be marred by the volatility in COVID-related sales.

Just quickly as well- HOLX produced quarterly OCF of ~$332mm, and finished the quarter with a cash balance of $2.77Bn on net leverage of 0.1x. Apart from this, it bought back 1.4mm shares worth $114mm. It has acquired 3.6mm shares this YTD, totaling $264mm. This certainly adds to the value proposition in my view.

2. Economic profitability, squashed earnings rate on capital deployed

One critical factor to consider when profiling HOLX is that its economic profitability has decreased since COVID-19 diminished. For example, pre-tax income dropped from $325mm in Q3 FY'22 to $286mm last quarter, 12% YoY decline.

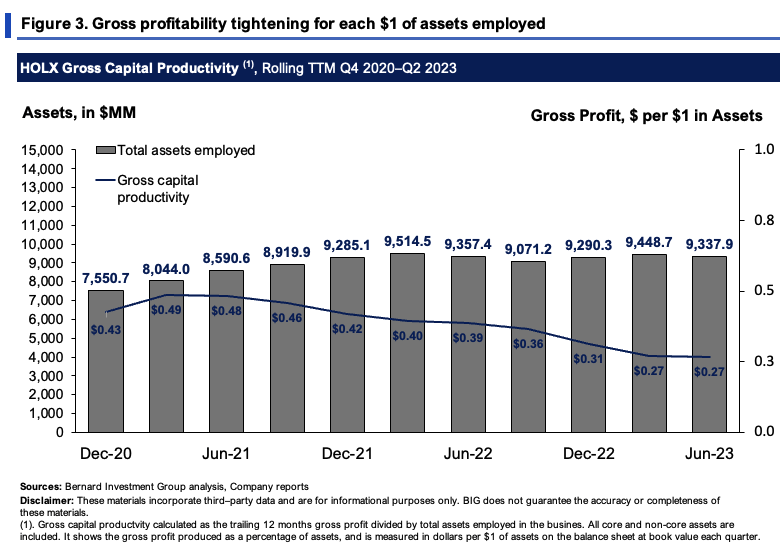

Gross margins-down from 77% in 2020 to 60.8% last quarter-are also a challenge to the investment debate. Moreover, as a function of assets employed to generate the profit, the picture is more bleak.

Figure 3 outlines this on a rolling TTM basis. It shows the gross profit earned on each $1 in assets employed (all core and non-core assets are included). Asset intensity is up $1.78Bn since 2020, but the gross profit produced on this is down $0.16 on the dollar to $0.27 for every $1 in assets. This is something HOLX needs to improve drastically in my view.

{kind=link}

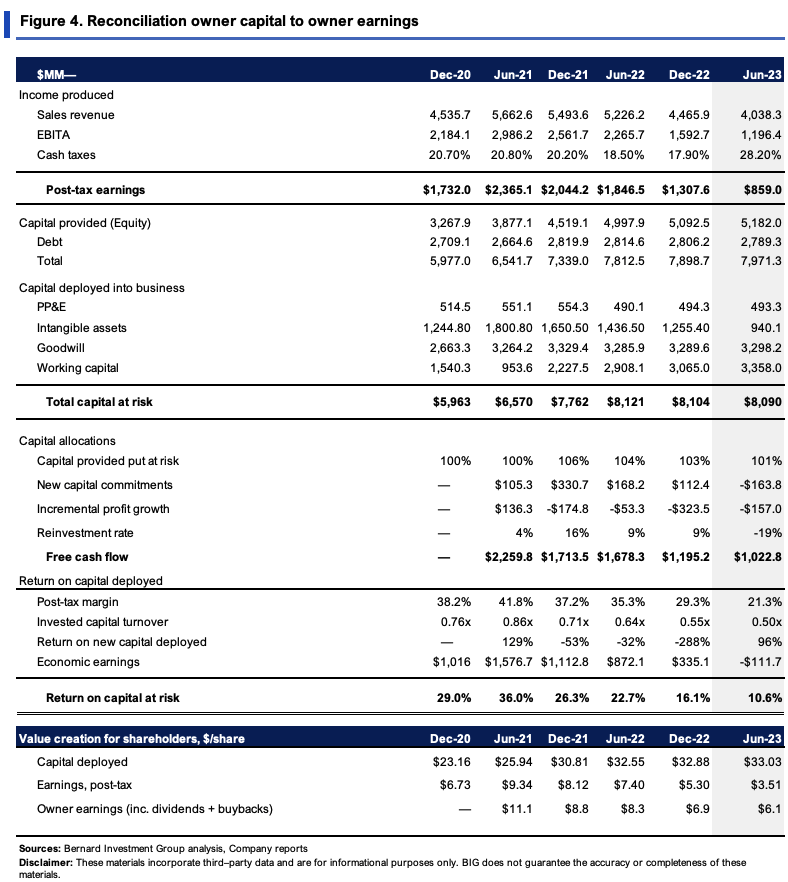

Despite the extra income generated from all its COVID-19 sales, the bulk of it hasn't been reinvested into the business yet-deployed into growth initiatives, increasing capacity and so forth. With about $30-40mm in CapEx per quarter and nothing added to intangibles, it's earning ~$860mm in trailing NOPAT on $8.1Bn of capital at risk, a return on capital of ~10%. This is below our required rate of return, discussed later.

These business returns aren't value-additive in my view, and that's been reflected in HOLX's equity stock this year so far. On a per-share basis, you're looking at $33/share invested to produce $3.50/share in trailing post-tax earnings. Post-tax margins and capital turnover are also decreasing back to the longer-term range as well.

So it's really the buybacks that are adding the most value here, bringing the owner earnings to $6.10/share last period, despite producing $3.51/share or 10.6% earnings rate on capital.

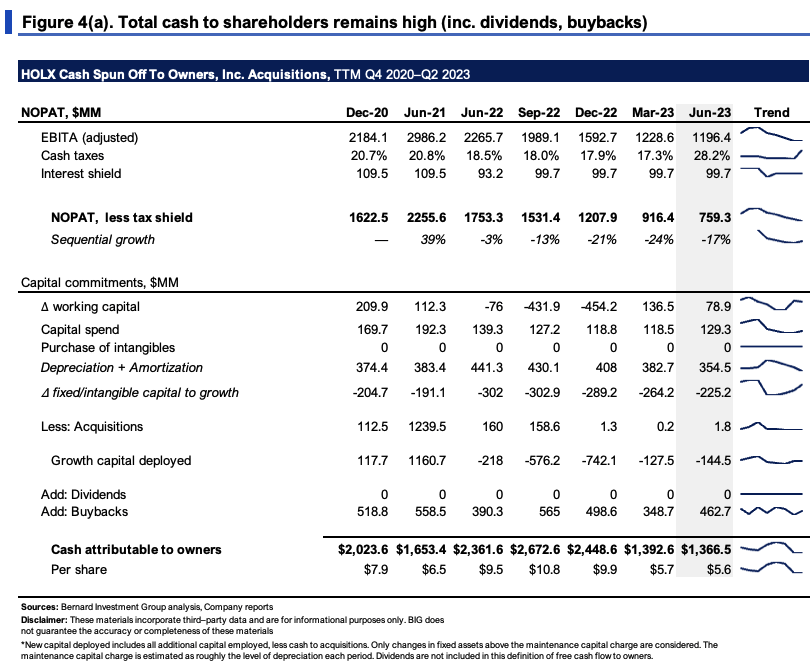

{kind=link}

You see the buyback point reflected in Figure 4(a) as well, which shows a slightly different orientation of NOPAT, investments, and FCF. This time, when calculating new capital deployed, we take into account any additional capital invested minus any cash used for acquisitions. Only changes in fixed assets that exceed the maintenance capital charge are considered 'growth investment' here, which is estimated to be approximately equivalent to the depreciation charge each period. Buybacks are also factored into this calculation of FCF to owners. Further, NOPAT is taken net of the tax shield afforded by interest payments. So we're looking at the deleveraged level of investment toward growth and checking FCF based on this.

Here, you can see the large divestments to growth capital inflecting positively on cash flows-but there's no value add. FCFs are also down off FY'20 highs from $2Bn to $1.36Bn. Without the buybacks, it booked $903mm in owner earnings, all the above factors included in the calculus.

{kind=link}

We can think of the market and its long-term averages as a competing rate of return. Long-term market averages are around 10-12% (take 12% here), which we'll call the market return on capital . To produce outsized returns over time, companies should produce business returns higher than the market return on capital. The question is: in whose hands is investor capital more valuable-in our hands, just riding the benchmark, or, in HOLX's hands?

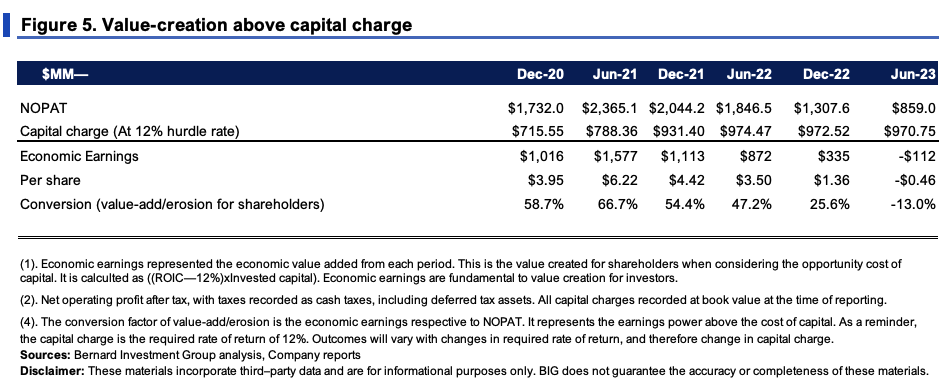

Currently, it's more valuable in our hands. Why? Because HOLX didn't outpace the market return on capital on its investments in 2023-for the first time in around 2.5 years mind you. To quantify this, Figure 5 outlines the economic earnings HOLX threw off from 2020 to 2023 so far. It then compares this to the NOPAT produced. Economic earnings are calculated as a function of the ROIC, less the 12% hurdle rate, multiplied by the invested capital.

The 'capital charge' is the required rate of return of 12% applied to the capital employed by HOLX, $970mm last period (8,090x0.12 = $970). A positive number for economic earnings is fundamental in the value creation of corporations. It shows the amount of profit generated above the required rate of return. If you're required return is 10%, you'd need HOLX to spin off at least $809mm in post-tax earnings to create value above this rate ($8,090x0.1 = $809). At 15%, $1.2Bn, and so on. We use 12%, as mentioned earlier. Any number above (or below) these stipulated rates are considered economic earnings (or losses), and signify the surplus return (loss) above the hurdle rate.

What shows is that, from 2020-2022, the conversion factor was tremendously high for HOLX. From 2020-2021 it was around 47%-58% of NOPAT, producing >$1Bn in surplus earnings on capital at risk each period. From 2022 onwards, the numbers have shrunk, and were negative $112mm last period, or negative 13% to NOPAT. The market pays exquisitely focal attention to these kinds of economics. So it would make sense why HOLX sells lower in H2 FY'23.

{kind=link}

3. Value drivers and expected valuation

- Critical value drivers

So we've discussed the headwinds HOLX is working through and what's likely caused the selloff in its equity value this year. The question is what to expect going forward, and what kind of expectations make sense at HOLX's current market values.

Figure 6 shows the key value drivers for the company these last 3 years. Operating margin looks to be the major growth lever. NWC is actually a 365% increase, but is shown negative here as it is taken as a percentage of the change in revenue. Every new $1 in revenues also came with $0.04 in fixed assets, with M&A numbers adding 22% of value over this time too.

BIG Insights

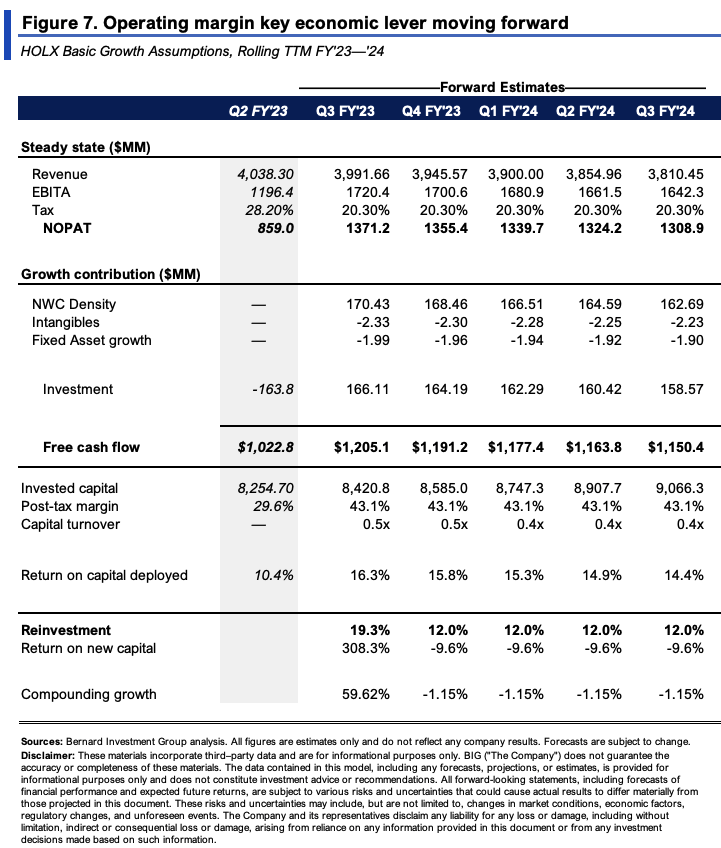

As a simple exercise, I looked at what HOLX could produce if it were to continue at its current trajectory. Inputs from Figure 6 are included and the outputs are shown in Figure 7. Presume HOLX continued at its steady-state level of operations (basically what it's doing now).

You're looking at revenues paring back to $3.8Bn over the next year, with pre-tax earnings following suit. I'd foresee ~$160-$165mm in investment each quarter, in-line with historical averages.

The company could still spin off $1.1-$1.2Bn in free cash flow, and ratchet up NOPAT margins to the 40% range, returning 14-15% on the capital required to run the business. The problem I have here is this could cumulate to a 4.6% reduction in intrinsic value over this time. You can see the capital intensity potentially increasing, with profits earned on this capital decreasing.

{kind=link}

- Valuation

Of course, these figures may change over time. But based on HOLX's current market cap of $17.83Bn, the market expects $2-$2.14Bn in pre-tax earnings from HOLX in the next 24-36 months if discounting at the market return on capital of 12% (2,140/0.12 = 17,830).

Comparing the company's EV of $17.8Bn to the earnings produced on capital deployed is fruitful here. Both show returns for HOLX-business returns and market returns on investment. As shown in Figure 8, comparisons of both numbers show forward earnings power may well be priced in at HOLX's current EV. In a perfect world, I'd like an EV/IC >3x with ROIC/hurdle rat >1.5x.

BIG Insights

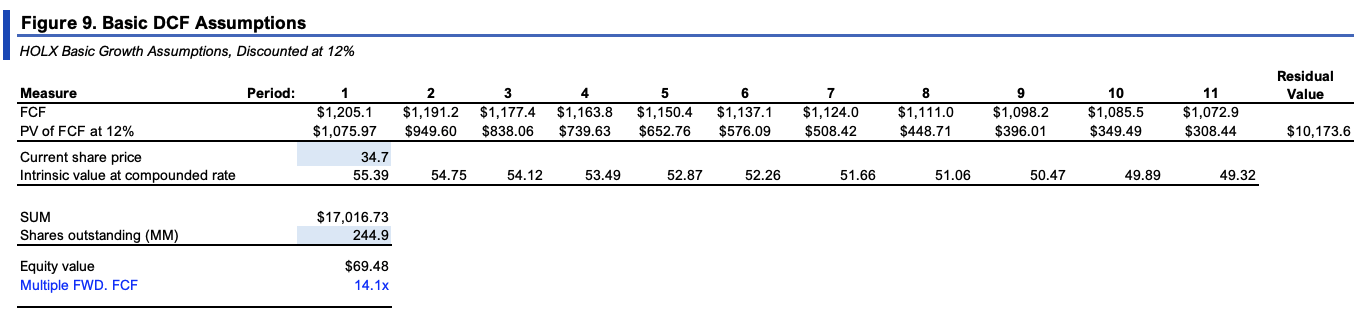

Extending the projections made in Figure 7 out to FY'28 and discounting back at 12% gets you to ~$17Bn in market value and ~$70/share, below where HOLX sells today. This supports a neutral view in my opinion.

{kind=link}

In short

HOLX is a long-term holding for the long account. But decisions on additional allocations and capital protection also have to be factored in, as always. On this premise, I am advocating to hold off allocating to HOLX for now, both as an initial holding and for those already long of it. The stock isn't a short candidate by any means. But it has some work to do emerging out of the COVID era, and the market has some time to digest the company's outlook downstream. Net-net, I revise HOLX to a hold for now.

For further details see:

Hologic: Post-Covid World Proving To Be A Nuisance On Profitability (Rating Downgrade)