HOMB - Home Bancshares Q2 Earnings: Strong Performance Amid Rising Concerns

2023-07-21 11:38:44 ET

Summary

- Home Bancshares, Inc. demonstrated resilience amid a challenging banking environment during Q2, surpassing revenue expectations with $474.87M and maintaining a solid earnings record.

- Despite its strong performance, the company faces significant challenges, including a decrease in deposit balances and potential squeeze on the net interest margin.

- I rate Home Bancshares stock as a "Hold," as it should successfully navigate its challenges but also faces considerable risk.

Thesis

Home Bancshares, Inc. (Conway, AR) ( HOMB ) has navigated a stormy banking environment by delivering financial services across diverse sectors. Despite the uncertainties, it remains resilient, reporting Q2 EPS of $0.51 and a revenue of $474.87M, surpassing expectations by $220.48M. However, in my analysis, I highlight significant challenges like a decrease in deposit balances and an imminent squeeze on the net interest margin. Therefore, even as Home Bancshares continues to display admirable strength, I believe it's vital to remain cautious and consider the potential risks, leading to my "Hold" rating on HOMB stock.

Company Profile

Home Bancshares, Inc., based in Conway, Arkansas, wears multiple hats in the finance sector. Primarily, it's the parent company to Centennial Bank, offering an array of financial services which are geared towards businesses, real estate players, and individual customers, among others.

Their offerings span from traditional banking to more specialized services. A closer look at their deposit products reveals a variety which includes everything from checking and savings accounts to money market accounts and certificates of deposit. Moreover, their loan portfolio is diversified, encapsulating everything from non-farm/non-residential real estate to consumer, agricultural, and commercial and industrial loans.

The company also operates in the insurance sector, underwriting policies for both commercial and personal lines, covering property, casualty, life, health, and employee benefits.

Home Bancshares Q2 2023 Earnings Highlights

In the turbulent sea of 2023's banking meltdown , Home Bancshares Q2 financial statements tell the tale of a resilient entity weathering its inaugural liquidity storm with a determined commitment to stability and strength. Amid potential revenue fallouts, Home Bancshares made an impressive stand, paying all uninsured deposits in full, thereby securing its berth among the country's most buoyant financial institutions.

Despite tapping into borrowing, Home Bancshares held its ground and sailed through the quarter, ensuring profitability and competitiveness. It remained moored within the top quartile of public banks in terms of profitability. The bank hit some rough waters when interest expenses surged ahead of income by $6.9 million, but it set its sights on smoother seas. According to management, by repricing nearly $760 million at a smidgen over 5% by year's end, they could add an estimated $5.7 million to the quarter's interest income.

Unfazed by the banking squall, Home Bancshares' management emphasized that they're geared towards generating new business securely and sustainably, anchored by its unwavering commitment to sound loan practices. Their yearly horizon targets roughly $400 million, and halfway through the year, they're holding a promising course with $208 million. Amid the banking crisis, the bank reiterated its commitment to maintaining a fortress balance sheet , demonstrating this by posting a solid earnings record of $105.3 million for the quarter.

Asset quality, a critical marker of stability, held firm with reserves standing at 2.01%. The numbers for non-performing loans and assets charted a positive course, showing an improvement over the quarter. The Return on Tangible Common Equity stood at an admirable 19.39%, and the CET1, leverage, and total risk-based capital ratios were all in the green.

Lastly, Home Bancshares also bought back 560,849 shares for roughly $11.8 million during the quarter, bringing the year-to-date total to 1.15 million shares for $25.3 million.

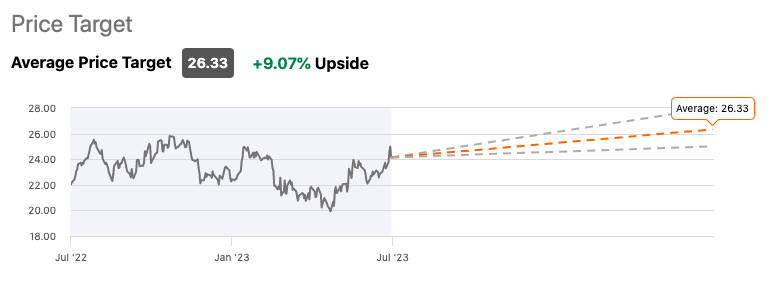

Expectations

Home Bancshares is covered by seven Wall Street analysts who have an average "Buy" rating on the company that amount to a +9.07% upside potential price target for its shares.

{kind=link}

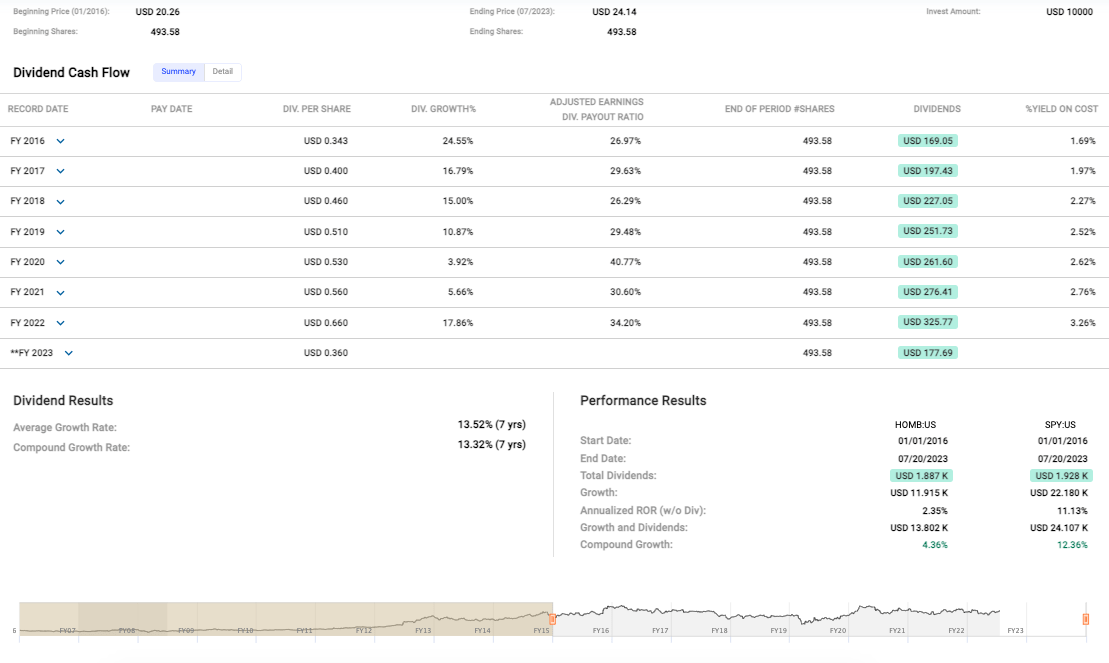

Performance

HOMB's stock performance in the medium term (from January 2016 to July 2023) has been a relatively steady but absolutely uninspiring ride up to $24.14 (note data below).

Home Bancshares Price Performance (Fast Graphs)

{kind=link}

Long-term investors like myself saw only an anemic compound annual growth rate of 2.35% without dividends, when compared with the far superior performance of S&P 500 Index (SP500), which saw 11.13% annualized returns during that same time frame. There's no sugarcoating it; HOMB has lagged behind significantly. However, one area where HOMB has shown promise is its dividend growth. From 2016 to 2022, they've maintained a fairly healthy dividend growth rate, averaging 13.52%.

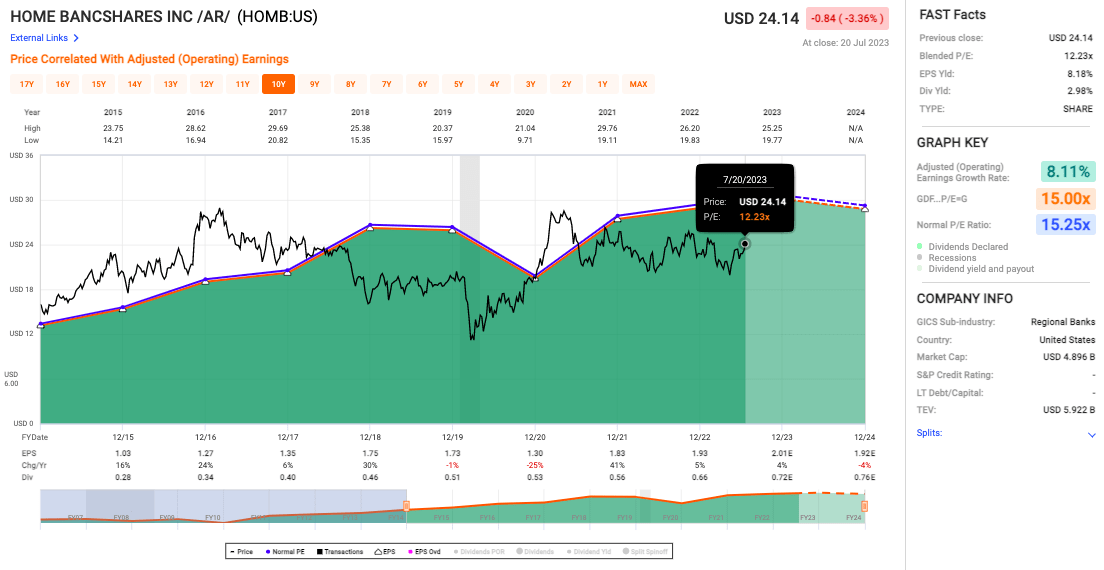

Valuation

The company’s blended P/E ratio, standing at 12.23x, is quite a bit below the average of the historical normal P/E ratio of 15.25x, indicating that the stock is currently undervalued relative to its historical trading multiples (note chart below). That being said, certain investors might see this as an opportunity to scoop up some shares at a discount relative to the company's earnings power.

{kind=link}

Risks & Headwinds

This quarter marks a stark period in the bank's history - arguably its most precarious one - that paints a rather sobering picture of the financial vulnerability the institution possesses, particularly in the face of external market disturbances. On the conference call , Chairman John Allison summed it up in one sentence:

This was the scariest 91 days of my banking career.

Author's side-note: Chairman John Allison's introductory comments, in my honest opinion, were a bit surprising and rare for a bank's conference call. Overall, the opening introduction set a tone of concern, frustration, and skepticism, highlighting the various problems he perceives in the current state of the United States and the language he used conveyed a mixture of pessimism, seriousness and sarcasm to deliver a critical commentary on the country's situation.

Moving on, if we extrapolate from this predicament, there's a clear risk that such instabilities might recurrently hamper the bank's future performance, potentially undermining its financial robustness and operational stability.

To fully comprehend the gravity of the situation, it's vital to probe the bank's financials. Specifically, the increased interest expense reported by the bank is indeed a glaring red flag. It has alarmingly outstripped interest income by approximately $6.9 million. This imbalance is far from a mere hiccup; it poses a significant threat to the bank's net interest margin and, consequentially, its overall profitability.

A more detailed examination of the bank's accounts reveals that deposit balances plummeted by a massive $449 million in the same period. The brunt of this significant exodus of funds was shouldered by its branches in Texas and Florida. This ongoing struggle to amass deposits could seriously undermine the bank's funding base, crippling its lending capacity and, consequently, its growth trajectory. This clearly implies that the bank needs to urgently devise strategies to staunch these outflows and restore its deposit growth.

If we zoom in on the net interest margin, it has contracted by 9 basis points during this tumultuous quarter. Additionally, there's a critical inverse relationship unfolding between deposit rate increases and earning asset yields. As an increase in both factors is anticipated, further pressure may be exerted upon bank profitability if these trends intensify further.

Looking ahead, the bank's outlook for the second half of the year appears to be gloomier than its already challenging first half. This anticipation indicates that there might be additional tribulations and adverse currents looming over its performance, which could further tighten the noose on its growth and profitability.

Final Takeaway

Despite the challenges faced by Home Bancshares amid the banking meltdown, the company demonstrated resilience with a solid earnings record and promising asset quality. They remain profitable and competitive, with plans to reprice a significant portion of their assets to improve interest income. Yet, my concern lies with increased interest expense, the decrease in deposit balances, and a potential squeeze on net interest margin.

Therefore, considering the overall turbulent banking environment and the company's mixed performance, I rate Home Bancshares, Inc. (Conway, AR) stock as a "Hold." Overall, there's potential for the bank to navigate these rough seas successfully, but the risks are also considerable.

For further details see:

Home Bancshares Q2 Earnings: Strong Performance Amid Rising Concerns