HOMB - Home BancShares: Record Profits Depressed Multiples Deleveraging And Momentum

2023-07-27 10:36:59 ET

Summary

- Home BancShares has seen record revenues, EBIT and net income since 2014, with a debt/equity ratio down 74% from its peak in Q4-2015.

- The company has repurchased approximately $25m of shares this year. Meanwhile, multiples are depressed, with P/B, P/S, and P/E (quarterly) now sitting 56%, 51%, and 46% below their Q4-2016 peaks.

- The recent acquisition of LendingClub Bank's marine loan portfolio and Happy Bancshares could lead to additional revenue and customer base growth for the firm.

- Despite risks including a concentrated geographical presence and heightened regulatory requirements, Home's strong financials and upward price momentum present an opportunity for investors.

About

Home BancShares ( HOMB ) invests in locally managed community banks in the United States in regions including Florida, Texas, Alabama, and New York City. As their FY2022 10-K explains:

Since opening… we have acquired and integrated a total of 23 banks with locations in Arkansas, Florida, Texas and Alabama, including 18 banks since 2010, seven of which we acquired through Federal Deposit Insurance Corporation (“FDIC”) assisted Transactions.

… We believe many individuals and businesses prefer banking with a locally managed community bank capable of providing flexibility and quick decisions.

… Our operating goals focus on maintaining strong credit quality, increasing profitability, finding experienced bankers, and maintaining a “fortress” balance sheet.

Home’s revenues mostly consist of loan interest and service charges, and its main funding sources include deposits as well as borrowed funds from the Federal Home Loan Bank (“FHLB”).

Total assets in Q2-2023 amounted to $22.13b, per the Q2-2023 press release . The firm’s total amount of borrowed funds by the end of Q2-2023 was $701.5m, with $679.4m of that amount borrowed from FHLB. The company has substantial exposure to the commercial real estate market, which accounted for 56.3% of gross loans in FY2022.

Elevator Pitch

-

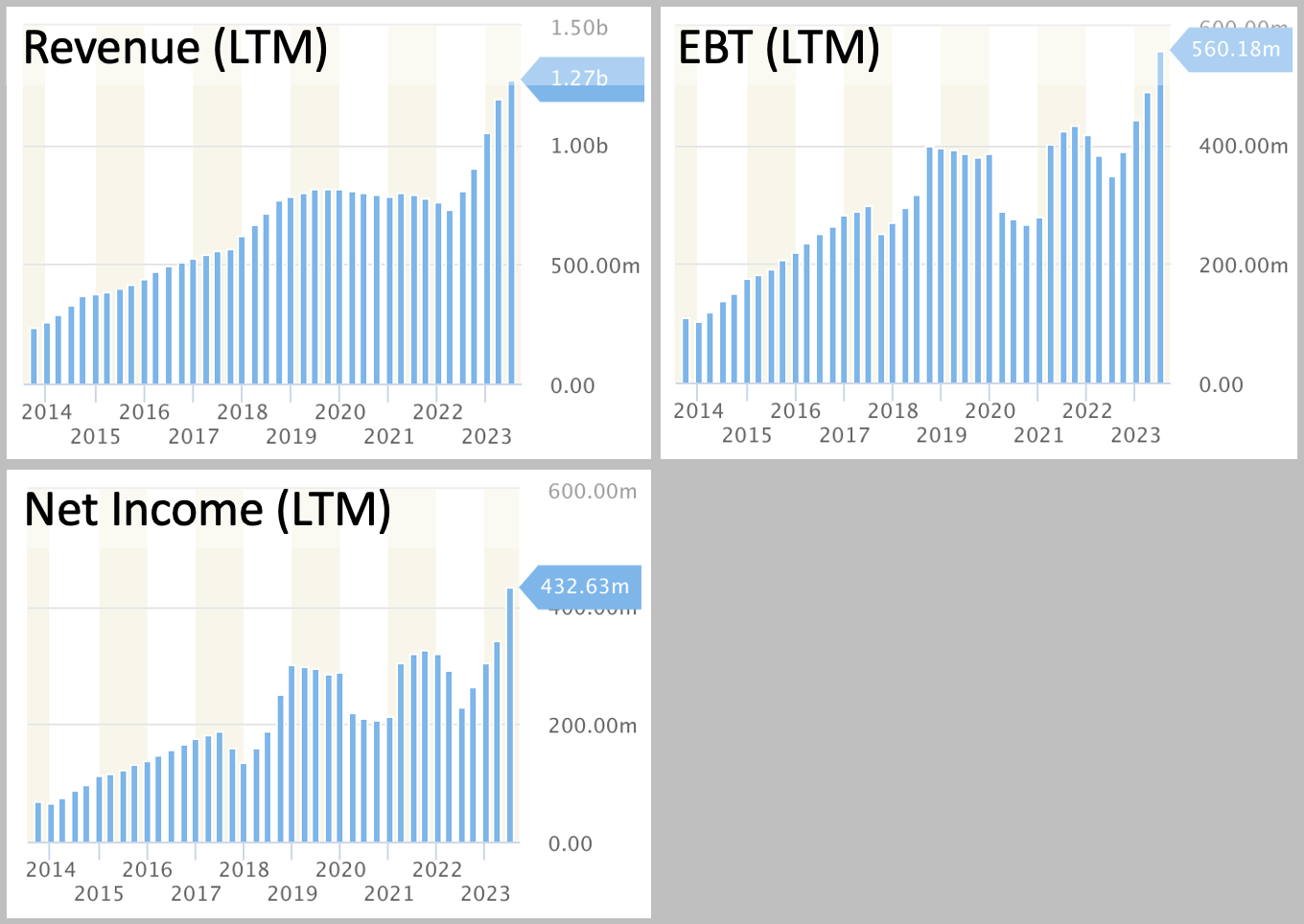

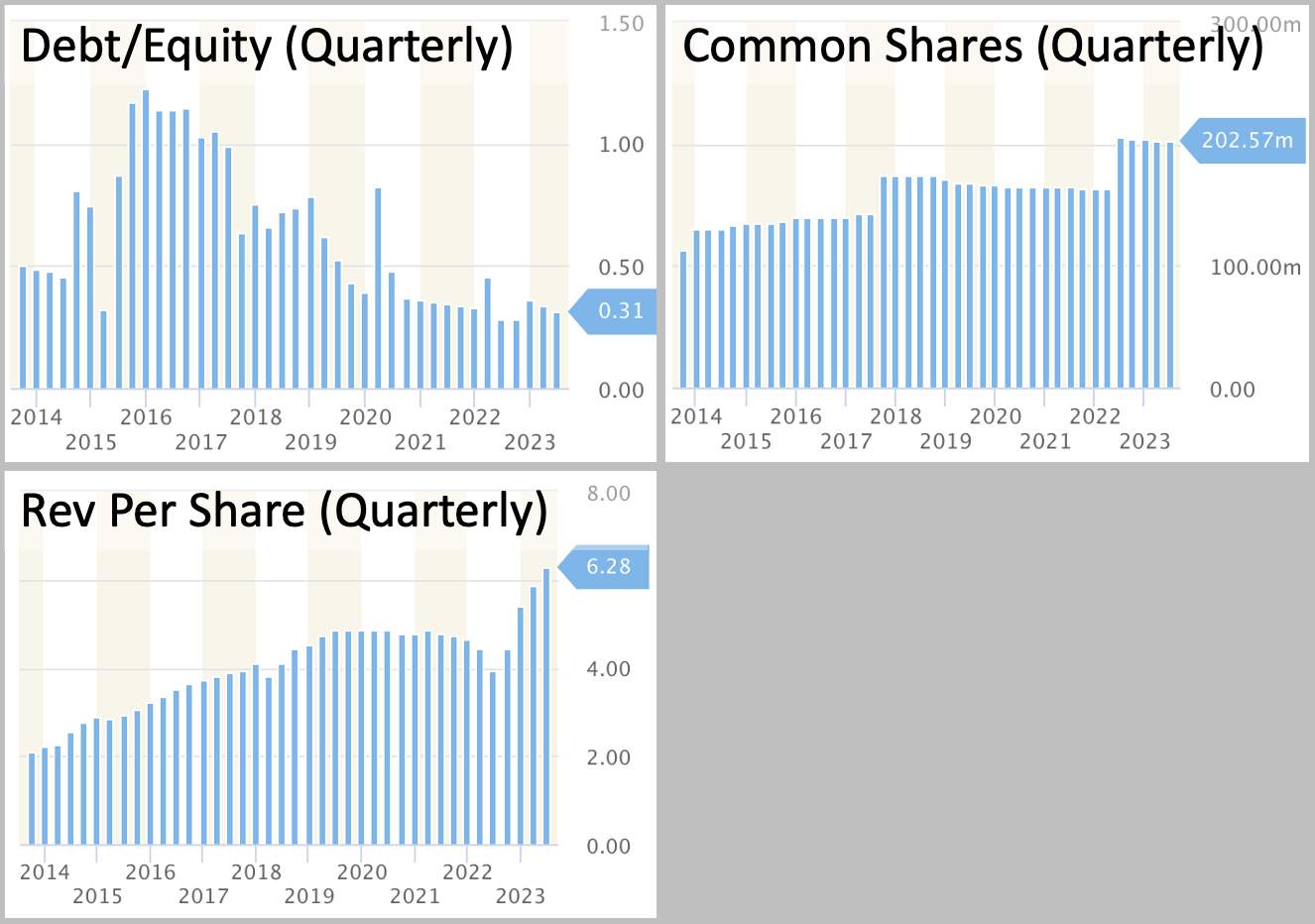

The company’s revenue (LTM, EBIT and net income (LTM) are at record highs since 2014. Its debt/equity ratio (quarterly) of 0.31 is down 74% from its peak in Q4-2015.

-

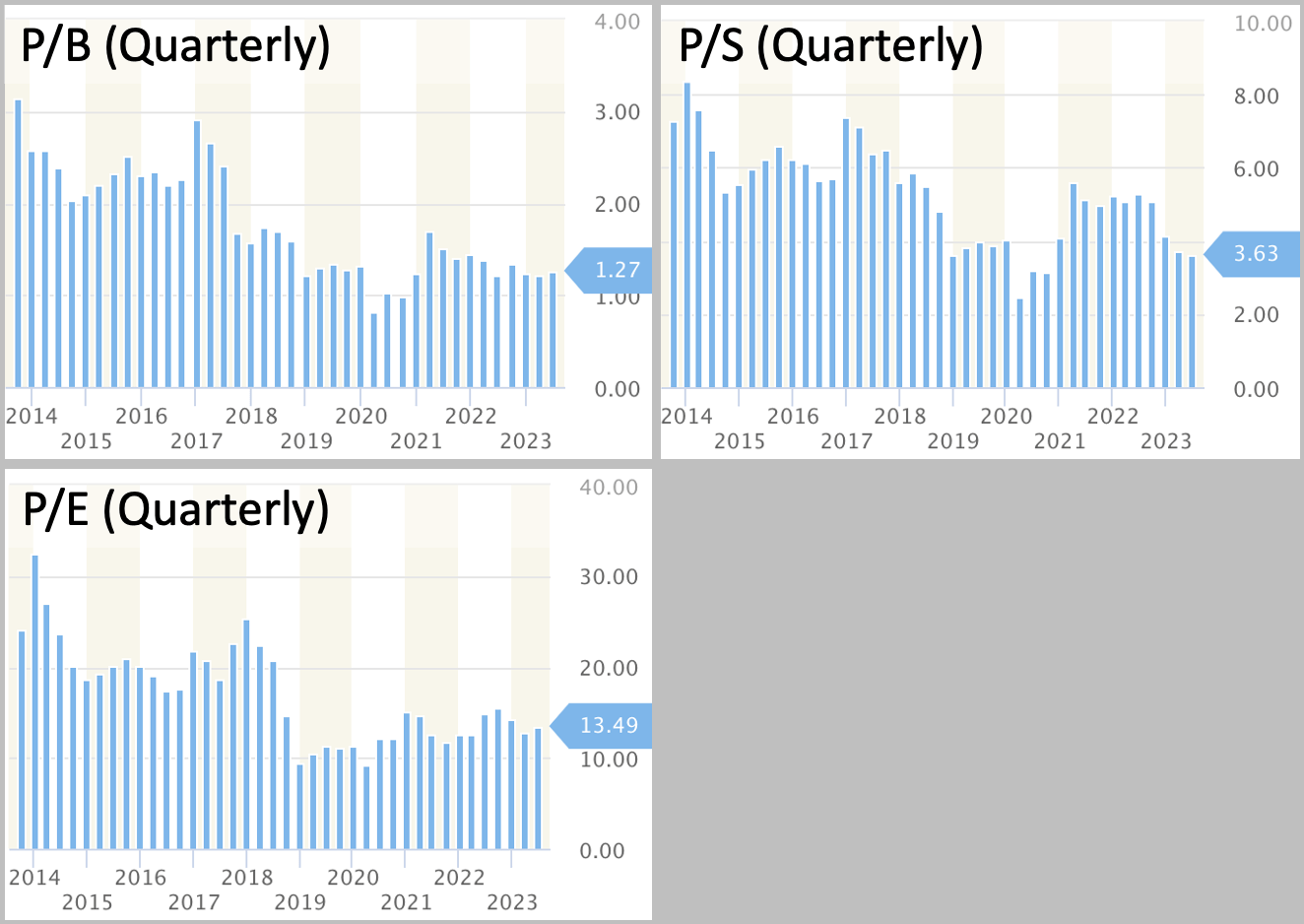

Home’s P/B, P/S, and P/E ratios (quarterly) are down 56%, 51%, and 46% from their Q4-2016 peaks, respectively. Its ROA ranks eighth among the top 200 exchange-traded U.S. banks for Q2-2023.

-

The firm has repurchased ~$25m of shares YTD.

-

Despite risks such as a concentrated geographical presence and heightened regulatory requirements, Home’s strong financials and upward price momentum present an interesting opportunity for investors.

Strong Financials

Revenue (LTM) is at a record high since 2014 and is up 57% year-over-year. EBIT, and net income are also at record highs since that time, based on data from StockRow .

{kind=link}

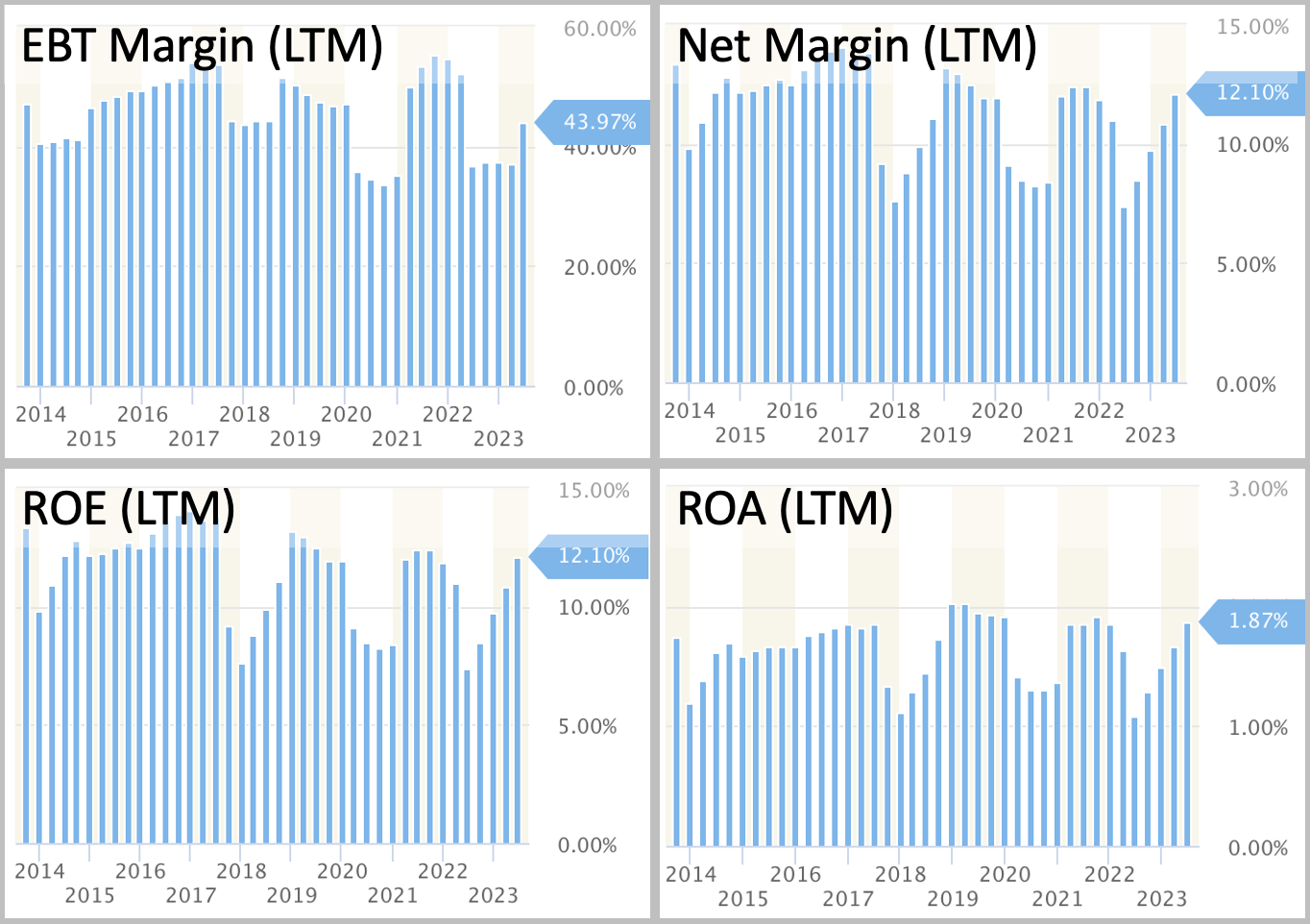

EBT margin (LTM) is above 40% and within its typical historical range. Net margin (LTM) has never dipped below 21% since Q3-2013; its current value of 33% is about 9% below its post-2014 peak, indicating room for potential expansion. ROE (LTM) is near the upper end of its historical range, though it has been downtrending slightly since 2014. It currently sits at ~12%.

{kind=link}

Home’s debt/equity ratio (quarterly) of 0.31 is close to a record low since 2014 and is down ~74% from its peak in Q4-2015. The firm’s number of common shares has been increasing since 2014 and is up 21% from Q2-2020, indicating a risk of dilution; however, per-share metrics such as revenue-per-share are still in uptrends in spite of this.

{kind=link}

Historically Cheap Multiples

The firm’s P/B ratio (quarterly) has been falling since 2016 and is down ~56% from its Q4-2016 peak, currently sitting at ~1.27. Its P/S and P/E ratios (quarterly) show a similar pattern, down about ~51% and ~46% from their Q4-2016 peaks, respectively.

{kind=link}

Strong Industry-Specific Metrics

In Q2-2023, common equity tier 1 (CET1) capital rose 0.8% compared to the same quarter last year and currently is at a solid level of 13.6%, per the firm’s recent press release . Net interest margin ((NIM)) was 0.6% higher than it was last year, now sitting at 4.28%. The firm’s return on average tangible common equity (ROTCE) of 19.3% is 16% higher than it was a year ago.

Home’s ratio of non-performing assets to total assets, 0.28%, was roughly unchanged compared to its value of 0.25% last year. The company has a strong liquidity position, with $4.9b net external liquidity available as of the most recent quarter.

Return on assets was higher in Q2-2023 compared to last year, rising from 0.26% to 1.9%. The firm estimates that its ROA ranks eighth among the top 200 exchange-traded U.S. banks for Q2-2023.

Home’s efficiency ratio in Q2-2023 was slightly (2%) below its value in the prior year and is now sitting at 44%.

Potential catalysts

In early February 2022, the firm acquired LendingClub Bank’s marine loan portfolio, which included $242m of yacht loans. About two months later, Home also acquired Happy Bancshares, which had about $6.69b in total assets and $5.86b of customer deposits. These acquisitions could lead to additional revenue and customer base growth down the line.

Management expressed disappointment in the firm’s elevated interest expenses in Q2-2023 and said it is taking action to address it. On the recent earnings call, the firm said it had about ~$760m to reprice at ~5% by the end of this year and that the firm might see an extra $5.7m boost to quarterly interest income, which may partially mitigate the impact of those elevated interest expenses.

The firm expects the number of potential deals to increase in the second half of the year compared to the first half, which they described as “a little bit slow,” and expressed some optimism about the environment for community banking deals:

…in the community bank footprint, we’re still seeing good opportunities. It’s hard to make some of the deals work... you gotta be looking at 45%, 50%, 55% equity in a lot of these deals to make them work. And there are people willing, in some cases, to do that. So we’re still seeing good opportunities. We actually had growth at the community bank level last quarte r.

In its 10-Q , the company said it plans on opening additional branches in the future if attractive opportunities emerge.

The company repurchased $11.8m of its shares in Q2-2023 and ~$13.5m in the prior quarter (590k shares with an average price ~$22.92).

Risks

Like other companies involved in regional banking, Home’s financials may worsen if economic conditions substantially deteriorate and/or if interest rates rise severely enough to offset the firm’s loan growth. Also, the firm relies on investment banks, brokers, and other financial institutions that could fail or experience instability. Events such as sudden macro changes or policy shifts could lead to instability in those institutions.

Home operates with stricter regulatory requirements since its total assets exceed $10b. This means its interchange fees for debit card transactions are capped (~$0.21 plus 5 basis points of the transaction plus a $0.01 fraud adjustment).

The firm has a fairly concentrated geographic presence and its results are highly dependent on local economic conditions.

A large part of Home’s loans could become under-collateralized if real estate prices significantly fall; about ~72% of the firm’s total loans were secured by real estate by the end of FY2022.

The company noted in its 10-K that its operations are adversely impacted by public health emergencies such as COVID-19, which forced the firm to recognize credit losses on its loan portfolio. Pandemics are hard to predict, and if the COVID-19 pandemic worsens or a new threat emerges, the firm’s results could suffer.

Execution

Buying a stock is a bet on where its price goes, not necessarily the fundamentals of the business. Since there is statistical evidence of trends in equity markets, investors who apply a scientific mindset may benefit from focusing on companies with trending share prices.

HOMB’s share price recently started an uptrend on May 15 and is up 16.5% since. The stock broke above its 200-day average (a popular trend indicator) on July 11, per finviz .

{kind=link}

Zooming out, the stock is sitting 14.5% below its peak values from 2017 and 2021 (both peaks were close to $28.20).

{kind=link}

It may be sensible to consider a bet on this stock only while the uptrend remains in play, perhaps by requiring that a simple trend signal is active; for example, requiring that price be above its rolling average (50, 100, 200-day, whichever has stronger evidence).

Bottom Line

Home’s record profits, long-term deleveraging, historically depressed multiples, and trending share price make it an interesting opportunity for investors. While its price continues to trend, the stock could be a reasonable bet for investors with a momentum-inspired strategy to consider.

For further details see:

Home BancShares: Record Profits, Depressed Multiples, Deleveraging, And Momentum