RKT - Home Mortgage Industry Arbitrage - Buy MGIC Sell Rocket

2023-12-26 16:43:05 ET

Summary

- MGIC and Rocket Companies operate in different niches of the home mortgage business, with MGIC being a private mortgage insurer and Rocket being a mortgage banker.

- The valuations of MGIC and Rocket differ significantly, with investors being pessimistic about MGIC and optimistic about Rocket.

- The article argues that the valuation difference may not be justified, as MGIC is unlikely to experience substantially higher mortgage default claims payments and Rocket is unlikely to benefit from a surge in mortgage originations.

- My target prices suggest that MGIC is 30% undervalued and Rocket 50% overvalued.

Both MGIC and Rocket Companies are in the home mortgage business. But they differ in two important ways. One is their business models…

MGIC and Rocket are in different niches of the home mortgage business

MGIC is a private mortgage insurer, or PMI. For those of you not familiar with the PMI business, it starts with Fannie Mae and Freddie Mac, the dominant managers of U.S. home mortgage credit risk. By their charters, Fannie and Freddie are not allowed to buy mortgages with less than a 20% downpayment, unless the mortgage is “credit enhanced”. PMIs provide that credit enhancement, by insuring Fannie and Freddie against defaults of those low downpayment mortgages. If the insured loan defaults, the PMIs pay them a fixed claim payment. The PMIs receive insurance premiums paid by the borrower in exchange for taking that risk.

Rocket is a mortgage banker. Mortgage bankers have two operating functions. One is originating home mortgages, which requires:

- Finding customers looking to buy a home or refinance an existing mortgage.

- Underwriting the loan to ensure that it meets (primarily) Fannie Mae and Freddie Mac’s quality standards.

- Selling the loan to investors.

The other mortgage banking function is servicing the loan, which means collecting monthly mortgage payments and passing those payments on to investors.

Rocket claims that it is far more than a simple mortgage banker. I’ll address that claim below.

The second difference between the two companies is their valuations…

MGIC and Rocket are valued very differently

First, their price/book value ratios. Book values are useful valuation measures for most financial companies. Here are the ratios:

Company financial reports

Source: Company financial reports

Now their P/E ratios, using expected 2024 EPS

Seeking Alpha

Source: Seeking Alpha

Dramatic differences. Investors are pretty pessimistic about MGIC; its P/E ratio is less than half the market multiple. But investors are very optimistic about Rocket.

Is this huge valuation difference justified? If so, it requires some future combination of sharply lower MGIC earnings and/or sharply higher Rocket earnings. Let’s explore those possibilities.

Is MGIC about to incur substantially higher mortgage default claims payments? Highly unlikely

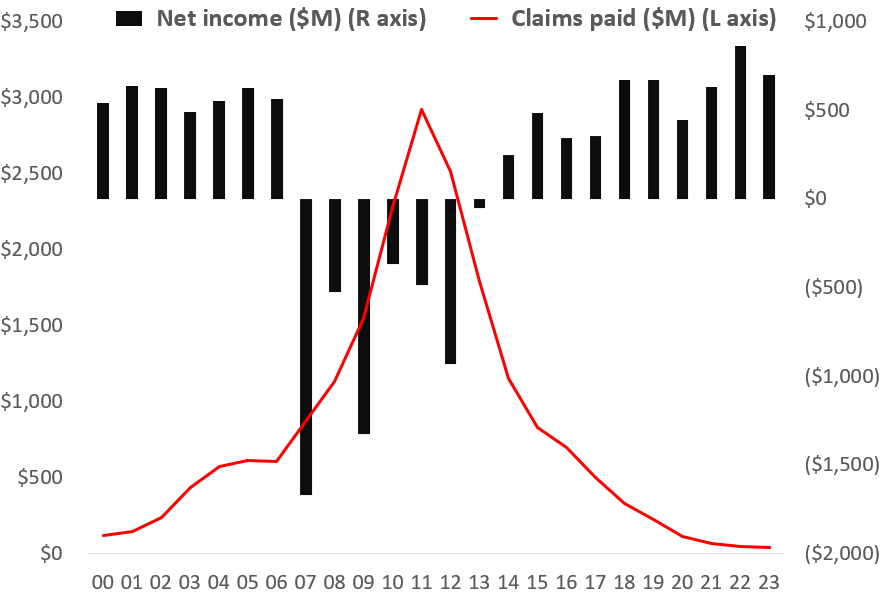

The major driver of MGIC’s earnings is its provision for claims payments, as shown by this earnings and claims payment history:

{kind=link}

Source: MGIC financial reports

The chart clearly shows that default costs soared during and following the ‘07/’08 Financial Crisis. So maybe the market is preparing for some version of that scenario.

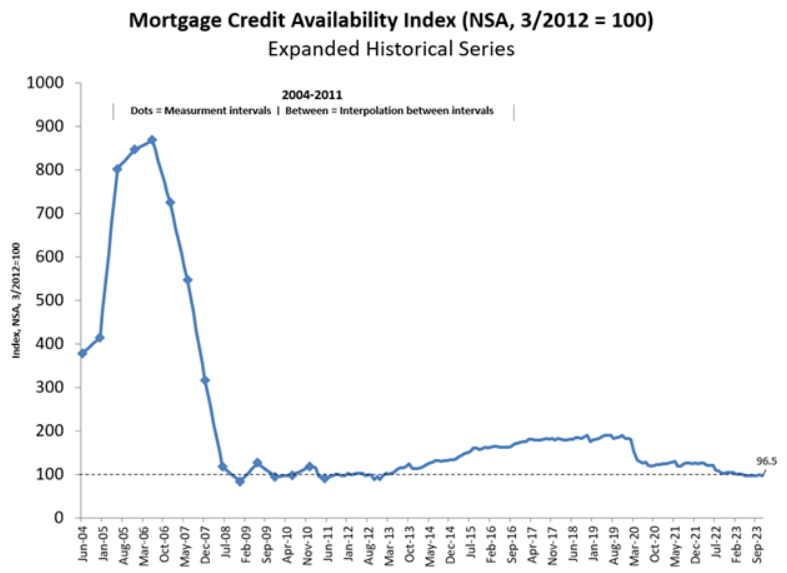

Another housing disaster is highly unlikely for the foreseeable future, for two reasons. First, the lending standards for MGIC and the entire mortgage credit world are dramatically better today, as shown here:

{kind=link}

Source: Mortgage Bankers Association

Better quality borrowers means fewer defaults.

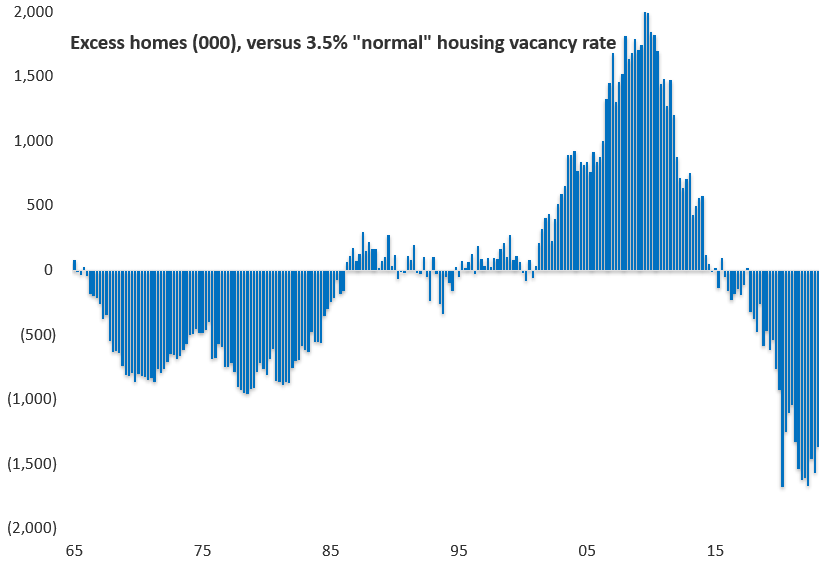

Second, single family housing moved from a major excess in ’07 to a serious shortage today:

{kind=link}

There is no better evidence that this housing shortage is powerful than the fact that despite a serious squeeze on housing affordability over the past two years (higher prices and higher interest rates), home prices are currently at record highs. Demand exceeding supply raises prices. Higher home prices both reduce defaults and cut the cost of those defaults.

Despite the conservative underwriting standards and the housing shortage, could MGIC’s claims payments soar anyway? Sure. All that is needed is a serious recession/depression. Not exactly a risk that the stock market is pricing in at present.

The more likely longer-term earnings trajectory for MGIC’s EPS is steady 5-7% growth from ’24, generated from some combination of insurance book growth and stock buybacks. An 8 P/E ratio seems pretty cheap for that outlook.

Is Rocket about to benefit from a surge in mortgage originations? Highly unlikely

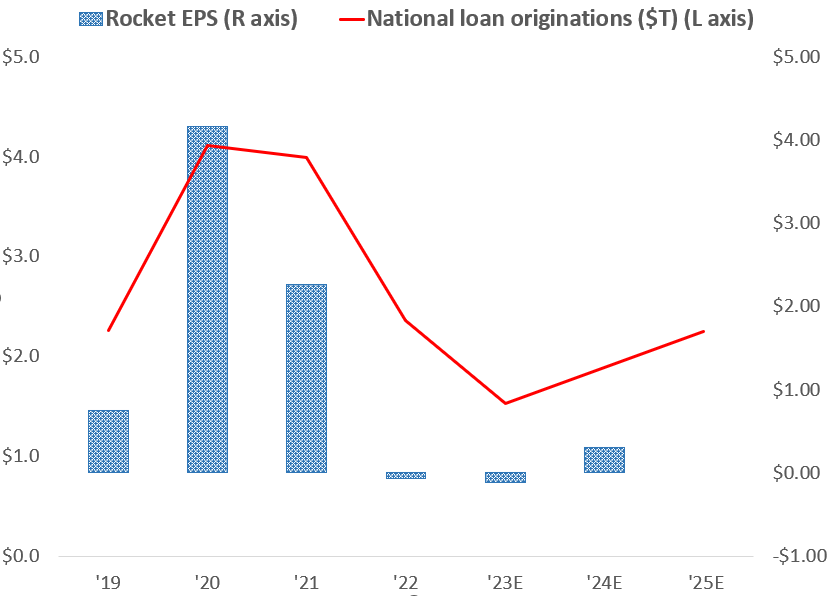

Like MGIC, Rocket’s earnings have a major driver – in this case, national home mortgage originations, as this chart shows:

Rocket financial reports, Fannie Mae

{kind=link}

Sources: Rocket financial reports , Fannie Mae

Mortgage origination volume explains over 80% of Rocket’s EPS moves, according to a regression analysis. So where is that volume heading? The chart above shows that Fannie Mae expects moderate improvement from particularly weak volume this year, but only to roughly the 2019 level. Rocket earned less than $1.00 a share pro forma that year; it was not yet public (It earned $1.34 billion in 2019, and had 1.8 billion shares after going public).

But what about the recent massive bond rally, that took the 10-year Treasury bond yield from 5.0% on October 18 to 3.9% today? Won’t that get home mortgage originations rocketing again? Investors sure think so – Rocket’s stock was $7.50 on October 18; it has nearly doubled since then.

An origination is surge is highly unlikely for Rocket, for two reasons:

1. A refinancing boom anywhere near 2021 is almost mathematically impossible. From 2015 to 2019, the 30-year fixed rate mortgage rate averaged 4%. Then post-COVID – from mid-2020 to late 2021 – an aggressive Federal Reserve kept the mortgage rate at 3% or below. During that period an astonishing $4.0 trillion of mortgages were refinanced, or nearly 40% of all mortgage debt outstanding. As a result, today “82% of homeowners have a mortgage rate below 5% and 62% have a rate below 4%, per Redfin. Notably, 24% of homeowners have a mortgage rate below 3%.” ( Yahoo Finance, June 14, 2023 )

The bond rally has taken the mortgage rate down to 6.7%. But it will have to drop below 5% to set off even modest refinancing activity.

2. Rocket is refi-centric. Rocket for some reason does not report the breakout of its loan originations between home purchases and refinancings. But another regression analysis – thank you Sir Francis Galton for inventing it – suggests that Rocket has an 11% share of national refinancing business, but only a 3% share of home mortgage originations. The likely reason is that Rocket is centralized, which makes it very efficient but not as effective at getting referrals from realtors and others when a home is sold. So for Rocket no refi boom means no earnings boom.

Another material refi boom will require mortgage rates to fall to 3% or less again. Which in turn will almost certainly require a major recession/depression to occur. Sound familiar?

Why then is the valuation gap between MGIC and Rocket so wide? The hype factor

I gave evidence above that the earnings both MGIC and Rocket are driven by single drivers – credit quality for MGIC and national home mortgage originations for Rocket. MGIC sticks to that story. For example, here are the opening remarks of MGIC’s CEO from its last earnings conference call :

“We continue to benefit from favorable credit trends, prudent risk management strategies, a disciplined approach to the market and the talent and dedication of our team.”

Not very sexy. And it recognizes the primacy of outside forces, not some special secret sauce the company supposedly has.

Rocket takes a different approach. It pitches itself as far more than a mortgage banker, as these quotes from its latest earnings presentation make clear:

“Building a technology giant.”

“Massive market opportunity. Rocket competes in some of the largest, most complex segments of the economy: mortgage, real estate, financial services. 20% of U.S. GDP. $5 trillion total addressable market.”

“Rocket is positioned to lead the digital transformation of our industries.”

“At Rocket, we have…a wealth of assets at our fingertips to leverage generative AI and revolutionize the homebuying and financing process…”

“Multiple drivers of growth.”

“The Rocket flywheel.”

You get the idea. Another company claiming that its disruptive technology will drive it to not only dominate its historic business niche but other related businesses. Just like SoFi, and Zillow and Redfin, and numerous other “fintechs”, no less than the well-funded existing major competitors. Investors clearly are willing to pay for this hype for FOMO on the next Google or Amazon. I am obviously a lot more skeptical.

So buy MGIC and sell Rocket

I expect MGIC’s P/E ratio to expand to at least 10 over the next few years as it delivers substantial amounts of its free cash flow to investors, as I described in this recent Seeking Alpha article . And I expect Rocket’s price-to-book value to drift down below 2 as the reality of no refi boom sinks in and the “disruptor” story fades. So target prices of $25 for MGIC (up 30%) and $10 for Rocket (down 30%).

Except if we get that economic depression. Then I’m wrong.

Editor's Note : This article was submitted as part of Seeking Alpha's Top 2024 Long/Short Pick investment competition , which runs through December 31. With cash prizes, this competition -- open to all contributors -- is one you don't want to miss. If you are interested in becoming a contributor and taking part in the competition, click here to find out more and submit your article today!

For further details see:

Home Mortgage Industry Arbitrage - Buy MGIC, Sell Rocket