PKB - Homebuilders: This Bubble Could Pop

2023-05-22 10:00:00 ET

Summary

- Homebuilding stocks are outperforming the market due to a surge in demand for new homes and a shortage of housing supply.

- However, there are mounting risks, such as a potential shift in unemployment, that could negatively impact the housing market and make investing in homebuilding stocks less favorable in the long term.

- Concerns about the commercial real estate market and tightening lending conditions also raise concerns about the overall lending market and potential ripple effects on small businesses.

Introduction

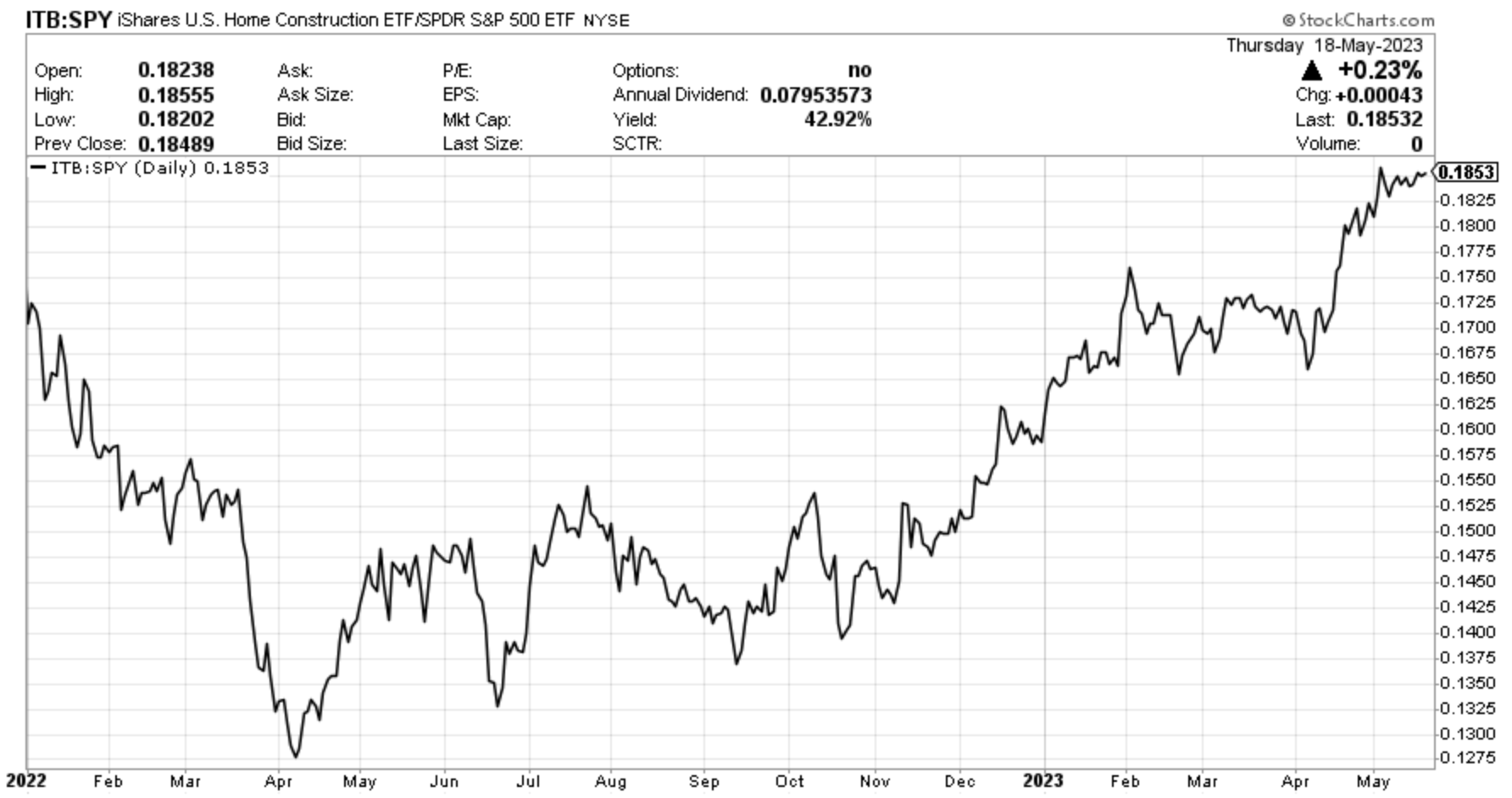

It's time to talk about housing and homebuilding. After last month's article on real estate , we're now shifting our focus to homebuilders and other related housing indicators. Why? Because homebuilding stocks are flying, outperforming the market and other housing-related investments by a mile, as displayed by the ratio between the iShares U.S. Home Construction ETF ( ITB ) and the S&P 500.

{kind=link}

Although there's a shortage of housing supply, the surge in demand for new homes is a result of people choosing not to sell their existing homes. Due to elevated interest rates, moving becomes less appealing, leading individuals to stay where they are.

However, it's important to note that this situation is showing signs of vulnerability. If economic growth weakens, unemployment could rise, prompting people to start selling their homes. Once this occurs, the market will be able to correct itself, potentially leading to a significant decline in home prices.

While I won't make a prediction of a Great Financial Crisis-style housing crash in this article, I want to highlight the unfavorable risk/reward of investing in homebuilding stocks and what this could mean for the bigger picture.

Homebuilding Is Where It's At

I like the ITB ETF for a number of reasons.

- It's the largest home construction-focused ETF, with close to $2 billion in assets under management.

- 67% of its assets are invested in homebuilders. It's not a pure-play homebuilding ETF, but it comes very close.

- It has 48 holdings and an expense ratio of 0.39%. While 0.39% isn't very low, ITB is a good way for investors to buy diversified homebuilding exposure.

All of these reasons explain why ITB is a great proxy for homebuilding stocks.

Looking at the chart below, we see that ITB has returned almost 40% over the past 12 months. Meanwhile, an ETF like the Invesco Dynamic Building & Construction ETF ( PKB ) with less homebuilding exposure returned 23%. Real estate stocks are down 11%. Regional banks, which are lenders of residential and commercial real estate, are down 33%. Stocks like Home Depot ( HD ), which cover housing-related retail, are somewhere in between.

I've often made the case that we're living in highly interesting times when it comes to macroeconomic developments. This certainly applies to housing and everything related to it.

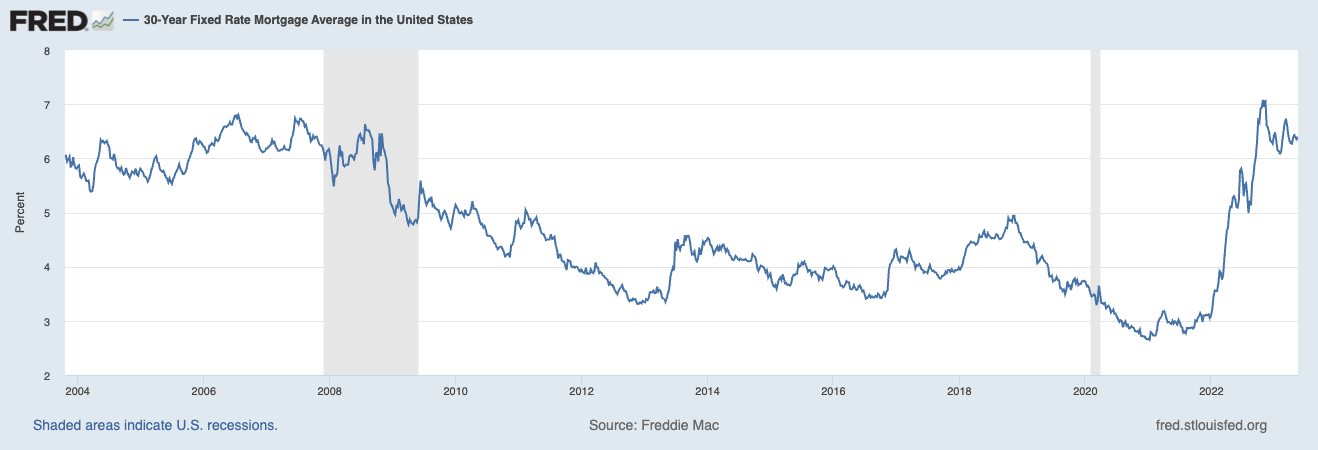

As reported by Bloomberg , the US housing market is experiencing a divide between existing and new homes. Existing homeowners are reluctant to sell due to their desire to retain low mortgage rates below 4% while borrowing costs have risen to a two-month high.

Federal Reserve Bank of St. Louis

{kind=link}

This unusual situation presents an opportunity for homebuilders in the new construction market. Builders have reported strong orders, exceeding expectations by 18% on average, despite mortgage rates above 7% and concerns about regional banks.

On May 16, the NAHB reported another surge in homebuilding sentiment, as displayed by the chart below.

NAHB

According to the NAHB (emphasis added):

New home construction is taking on an increased role in the marketplace because many home owners with loans well below current mortgage rates are electing to stay put , and this is keeping the supply of existing homes at a very low level .

[...] Lack of existing inventory continues to drive buyers to new construction.

[...] With limited available housing inventory , new construction will continue to be a significant part of prospective buyers' search in the quarters ahead.

As a result, new home sales now account for more than a third of total home sales. The pre-pandemic median was close to 15%.

Wall Street Journal

Adding to that, analysts predict further growth for builders in the coming years as they offer incentives, such as buying down mortgage rates from 6.5% to 5% or 5.5%, to help buyers afford homes.

While it needs to be seen how long that strategy lasts, it's certainly something that attracts potential buyers, as homebuyer housing payments are at an all-time high. Redfin data shows that mortgage payments based on a median asking price are at $2.6K per month, which is based on a 6.4% rate.

Redfin

Furthermore, so far, all of these assumptions are being confirmed. This is what the nation's largest homebuilder, D.R. Horton ( DHI ) said in its April earnings call :

Spring selling season is off to an encouraging start with our net sales orders increasing 73% sequentially from the first quarter. Despite higher mortgage rates and inflationary pressures , demand improved during the quarter due to normal seasonal factors, coupled with our use of incentives and pricing adjustments to adapt to changing market conditions. Although higher interest rates and economic uncertainty may persist for some time, the supply of both new and existing homes at affordable price points remains limited and demographics supporting housing demand remain favorable.

So far, so good.

The problem is that cracks are starting to appear.

Housing Risks Are Mounting

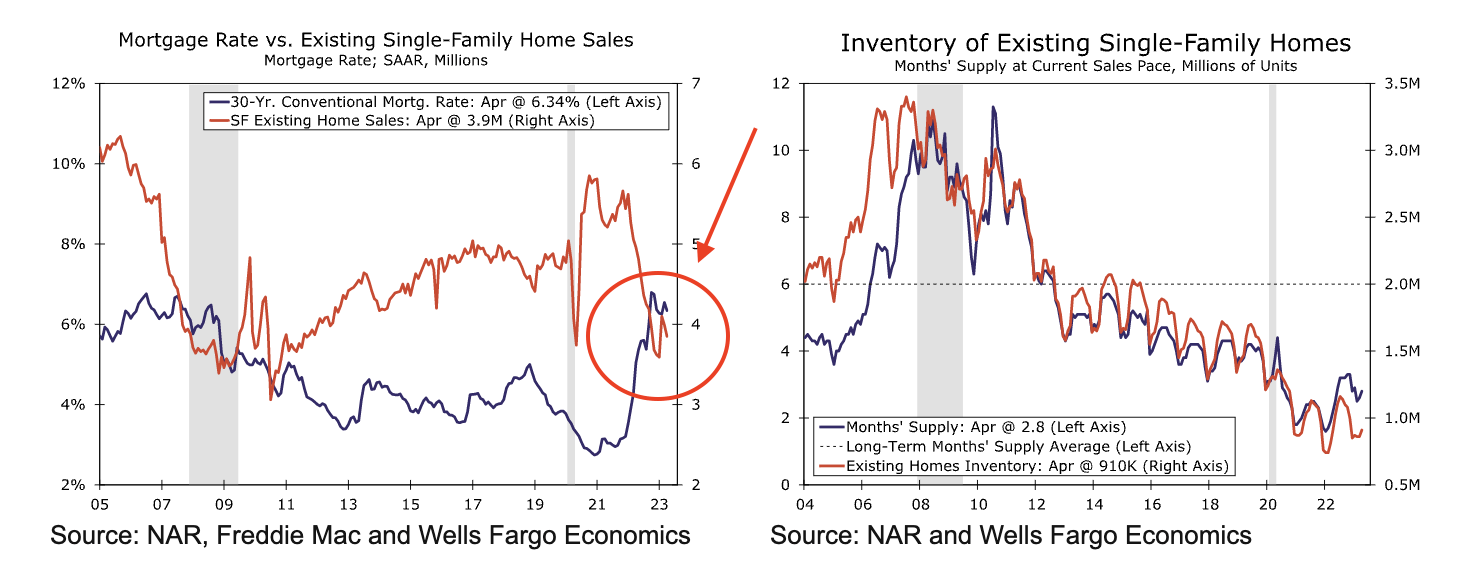

As healthy as homebuilder demand may be, demand for existing homes isn't great. Despite low inventory, higher rates are further damaging sales of existing homes. Wells Fargo ( WFC ) reported that higher mortgage rates in February and March likely put a dent in resale demand in April. After falling to 6.1% in late January, the average 30-year mortgage rate climbed back up to 6.7% by the first two weeks of March. Rates are currently still at these levels.

Wells Fargo (Author Annotations)

{kind=link}

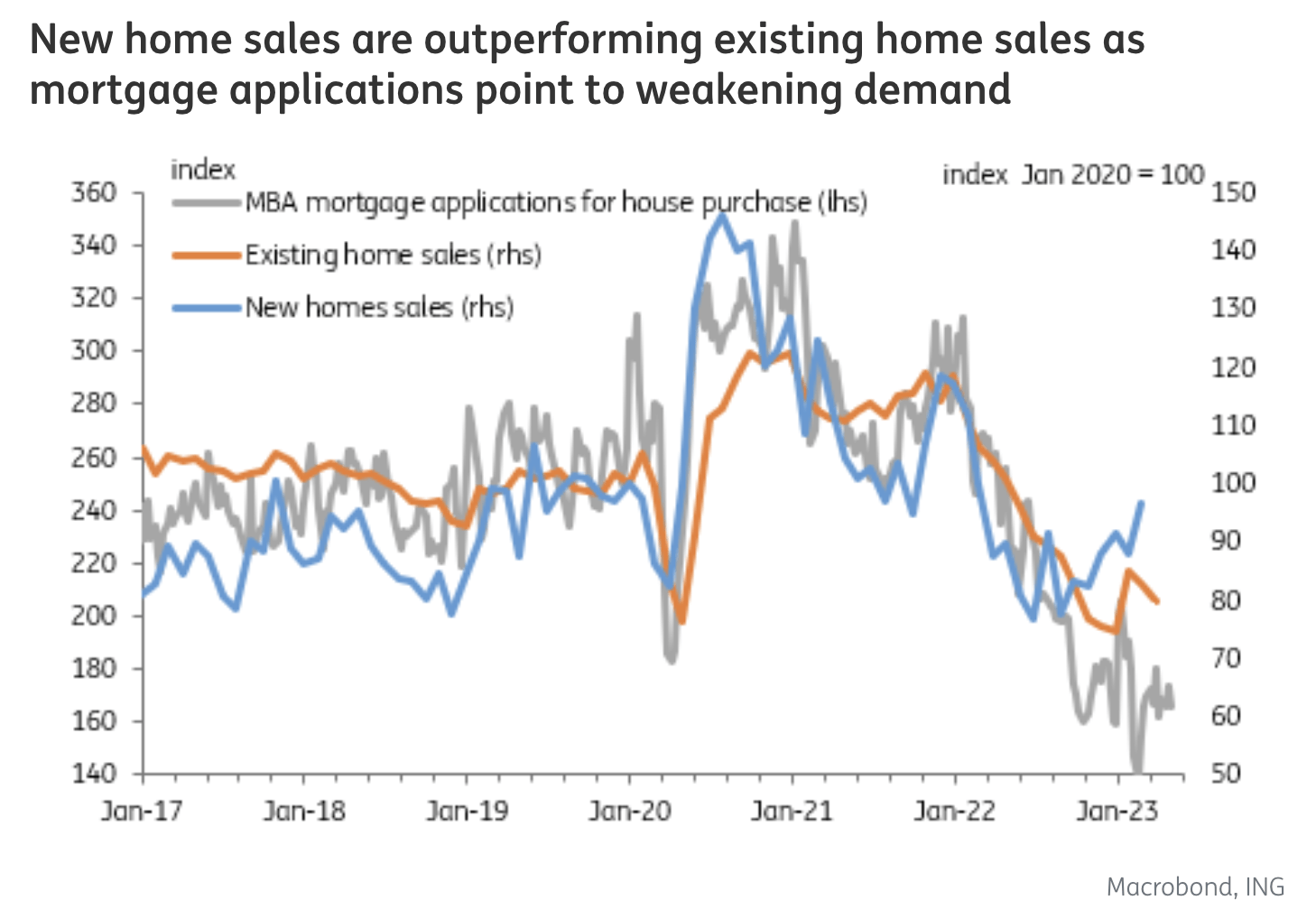

Hence, related to the first part of this article, we're seeing a widening gap between existing and new home sales. The chart below displays this widening gap, as well as the downside pressure provided by declining mortgage applications - caused by high rates.

{kind=link}

With this in mind, what could hurt homebuilders? It's not that I'm actively looking for reasons to be bearish. However, there are important developments to keep in mind that make the current situation a lot less bullish - at least from a longer-term risk/reward point-of-view.

According to ING , a potential shift in unemployment could have a significant impact on the US housing market. If the economy experiences a hard landing and unemployment begins to rise, it would lead to higher default rates and an increase in the number of homes available for sale.

Consequently, the combination of declining demand and rising supply would result in falling property prices.

The bank estimates that in order to bring house price-to-income ratios back to their long-term averages, a price decline of roughly 20%-25% would likely be necessary - unless there's a simultaneous increase in incomes, which would soften the decline a bit.

Additionally, the construction of new homes would likely (almost certainly) decline in such a scenario.

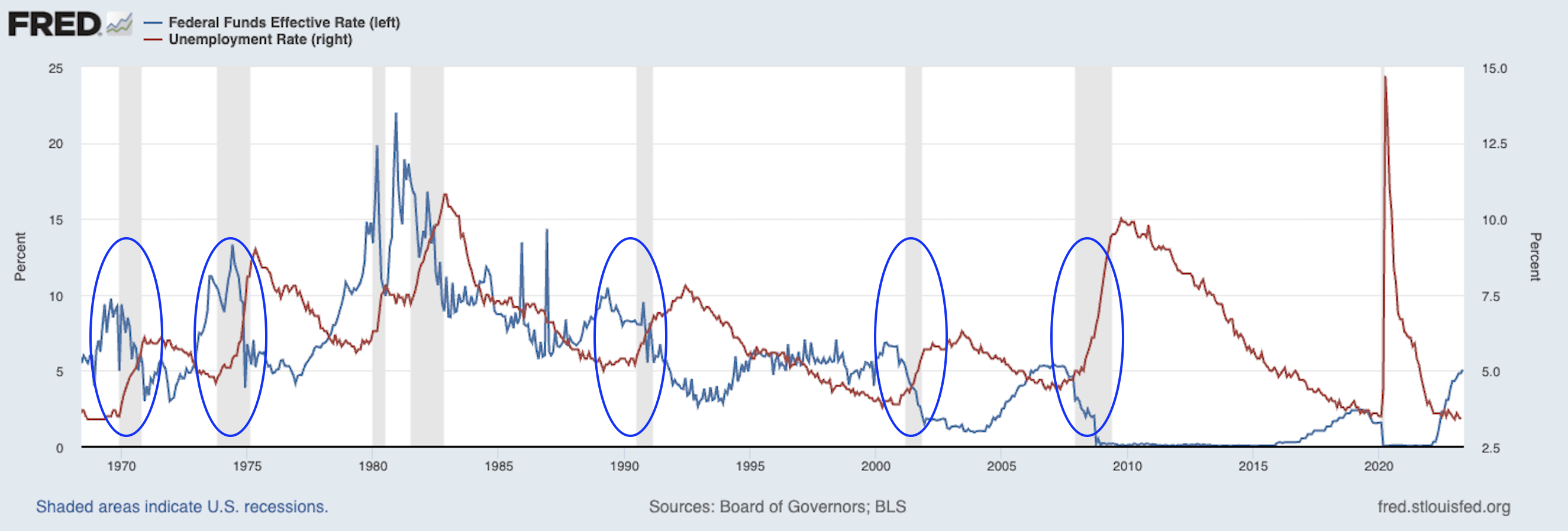

Right now, that's a major risk. Historically speaking, hiking cycles have led to recessions, which have caused unemployment to spike.

Federal Reserve Bank of St. Louis

{kind=link}

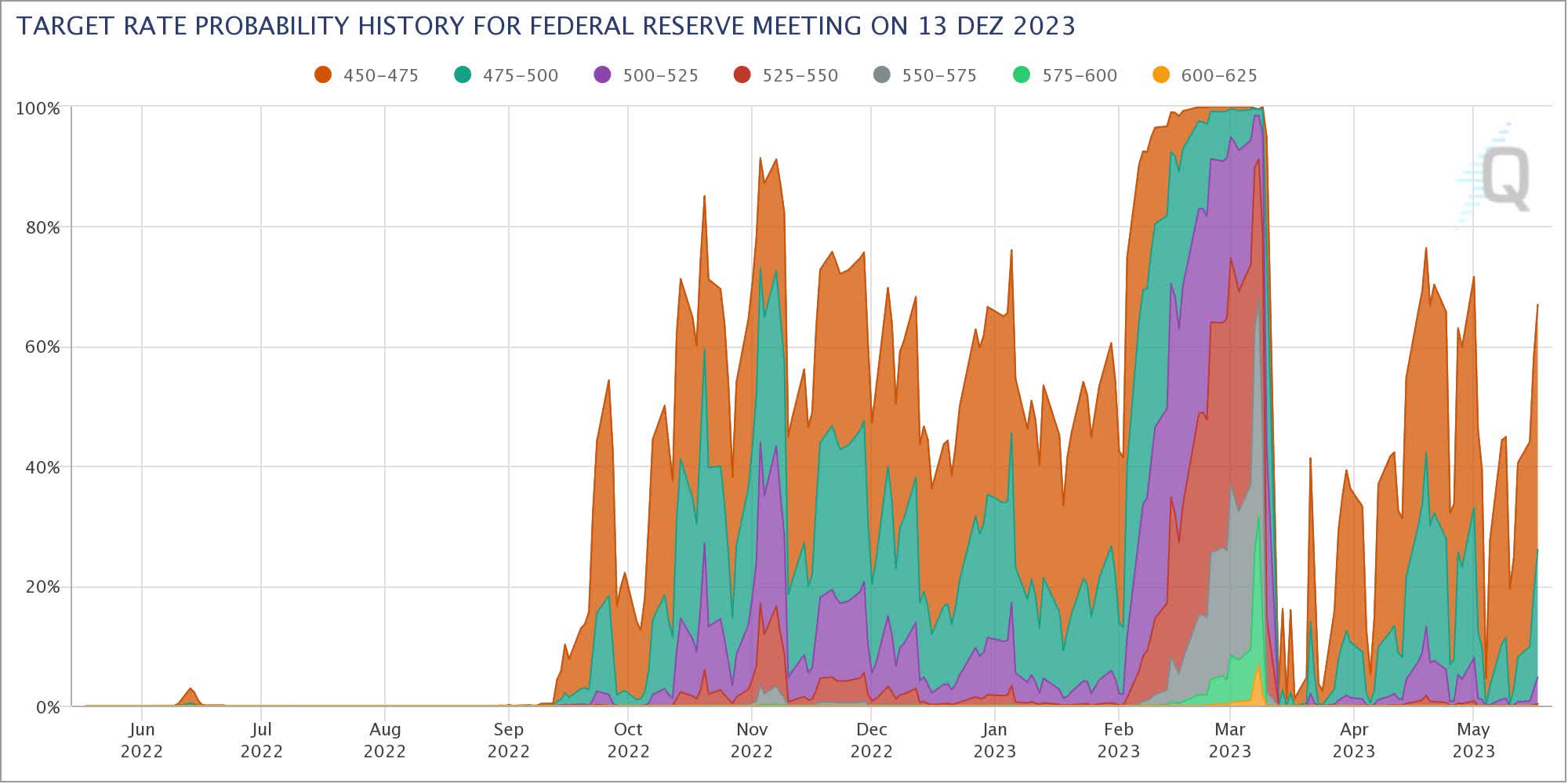

Currently, we're in one of the steepest hiking cycles in modern history. While the market is pricing in a Fed pause, it needs to be said that the market also is pricing in a slower rate-cutting cycle. The implied chances of a >4.50% Fed Funds Rate in December have risen to 60% again.

{kind=link}

This is happening despite weakening economic growth, as the Fed is expected to deal with both economic headwinds and sticky inflation. This makes it extremely likely that we get a scenario of rising unemployment, forcing the Fed to cut rates more aggressively at some point. It's also why insiders have told me that smart money (major institutions) are sitting on the sidelines. They're waiting for unemployment to rise. If that happens, rates will have to be cut. In that situation, private real estate buyers will be in a tough spot as high unemployment will keep them from benefiting from lower rates. That's when institutional players become major buyers.

It's also a scenario that would unleash the bearish scenario outlined by ING.

Furthermore, the risks extend beyond the residential sector. The Federal Reserve recently expressed concerns about the commercial real estate market due to the sharp rise in interest rates over the past 14 months. This increase in rates raises the possibility that refinancing commercial real estate loans could become challenging.

The somewhat blurry chart below shows increasing tightening in several segments.

The Daily Show

Related to this, the bank makes the case that the tightening lending conditions in the commercial real estate sector will also have ripple effects in other lending markets. Banks will become increasingly reluctant to lend in general.

{kind=link}

This situation is concerning because struggling businesses often turn into failing businesses when credit availability dries up. Small and regional banks account for more than 40% of all lending in the US, with a particular focus on small businesses outside major cities.

Therefore, the current situation raises troubling prospects. Large banks are unlikely to be able to compensate for the potential lending gap, and there's a risk of rising unemployment.

Takeaway

The surge in demand for new homes and the outperformance of homebuilding stocks are driven by a shortage of housing supply and homeowners choosing not to sell due to elevated interest rates.

While the current market conditions appear favorable for homebuilders, there are mounting risks that make the risk/reward of investing in homebuilding stocks less favorable in the long term. A potential shift in unemployment could have a significant impact on the housing market, causing higher default rates, increased supply, falling property prices, and a decline in new home construction.

The ongoing hiking cycle and the potential need for aggressive rate cuts in the future due to weakening economic growth could exacerbate these risks.

Additionally, concerns about the commercial real estate market and tightening lending conditions raise further concerns about the overall lending market and potential ripple effects on small businesses.

Hence, I believe that homebuilding stocks offer a very unfavorable risk/reward at current levels.

My strategy is to sit on my hands when dealing with homebuilders. However, I'm buying housing-related stocks that have already suffered. This includes real estate, consumer-focused stocks like Home Depot, and building material distributors like Carlisle ( CSL ), which I recently added to my portfolio.

The stock prices of these companies do not benefit from new home demand the way homebuilders do, which is why a lot more weakness has already been priced in.

So, long story short, I would be very careful when dealing with homebuilders at these levels. The situation is much more risky than it may appear at first sight.

For further details see:

Homebuilders: This Bubble Could Pop