HNHPF - Hon Hai Precision: Shining Through The Volatility

Summary

- Hon Hai delivered resilient Q2 numbers, as its supply chain resilience shines through.

- Forward guidance has been raised as well, signaling management's confidence in the outlook.

- With the stock trading at a very reasonable valuation relative to its growth potential, Hon Hai is a worthy defensive consideration for any investor's portfolio.

Hon Hai Precision ( HNHAF ), the leading global provider of electronics manufacturing services ((EMS)), appears on track to realize its 3+3 strategy, boosted by strategic alliances and accretive investments into building out its electric vehicle ((EV)) business. As things stand, management's EV guidance remains at a massive NT$1 trillion in sales and ~5% of global EV share by 2025, and given its progress thus far (new project win from Monarch Tractor and the production ramp-up of Lordstown's ( RIDE ) Endurance), I am positive about Hon Hai's prospects in entering and potentially reshaping the industry. The near-term guidance also calls for potential new customer wins from conventional auto OEMs and start-ups, as well as potential margin improvements in the coming quarters - prime re-rating catalysts for the stock, in my view.

Net, the current 11-12x P/E valuation seems very reasonable given Hon Hai's defensiveness (largely the result of its robust global logistics network), which should allow it to ride out any operating challenges unscathed. Plus, the improving earnings quality in its core business, as well as the long-term optionality from its new business initiatives, add to the compelling investment case.

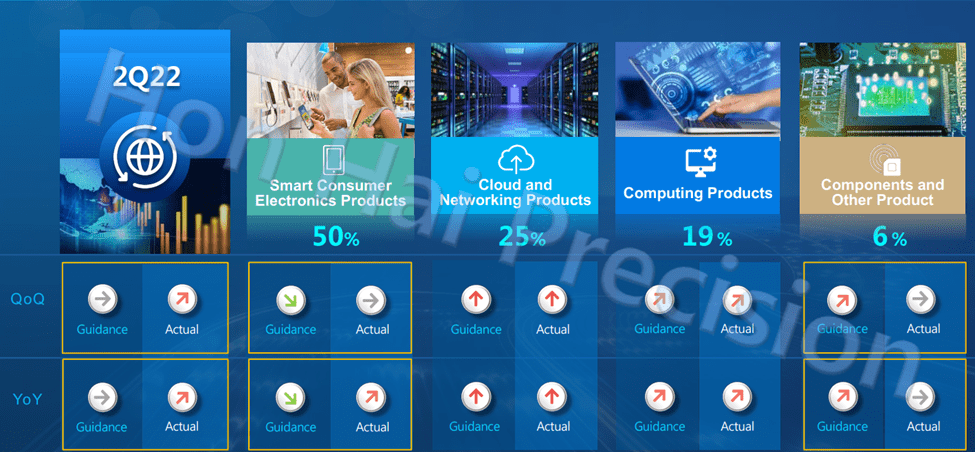

Q2 2022 Yields Solid P&L Numbers

Hon Hai's latest quarterly report showed revenue came in well ahead of consensus on strong cloud demand and share gains in the PC category, while gross margins also expanded ~40bps QoQ on product mix benefits (i.e., a higher contribution from components and cloud services), driving H1 2022 gross margins to a solid 6.2%. As a result, even with lower non-operating gains due to financial asset valuation losses this quarter, net earnings still came in strongly.

{kind=link}

In addition to the product mix upgrade benefits shining through, the strong execution despite COVID restrictions in China was impressive. Hon Hai's logistics advantage played a key role in its resilience - the company's ability to use more in-house components for manufacturing and secure logistics meant it could fulfill orders through the disruptions, supporting its continued growth and margin expansion. Yet, the extent of its margin outperformance relative to Foxconn subsidiary, Foxconn Industrial Internet, which saw margin contraction in Q2, was a major surprise. Most likely, Hon Hai benefited from a substitution effect as a result of its supply chain resilience - in contrast, operational disruptions during the China lockdowns crippled many of its assembly peers' production. It remains unclear how much of the order gains will 'stick' in the coming quarters, though, so I suspect the company could see some moderation in the coming quarters.

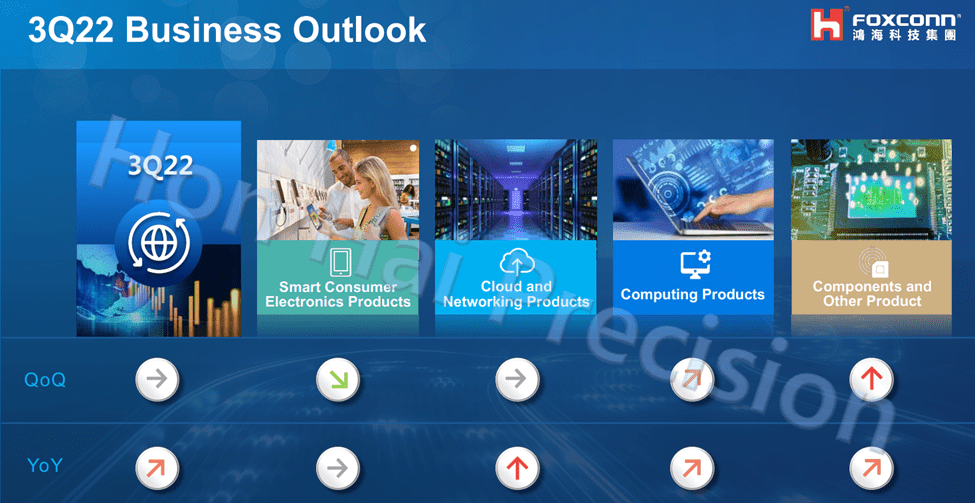

Further Improvements Expected In Q3 2022 Outlook

The Q3 2022 guidance of flat sales QoQ (on a higher base) or +7% YoY has been reiterated, while H2 2022 margins are expected to be up relative to 1H22 levels. Key near-term drivers include growth in computing products and components contribution (vs. the ~10% of FY21 revenues), although cloud and networking sales are set to be flattish QoQ and consumer products down QoQ on the iPhone transition. Of note, management also addressed its increased inventory on hand, citing limited risks given these are backed by customer demand. With further product mix improvements expected (mainly components and cloud services related) and process optimization efforts also in the pipeline, gross margin looks set to expand down the line further. Management also committed to continuing to drive a higher quality product mix in coming years, so expect more upside to current estimates.

{kind=link}

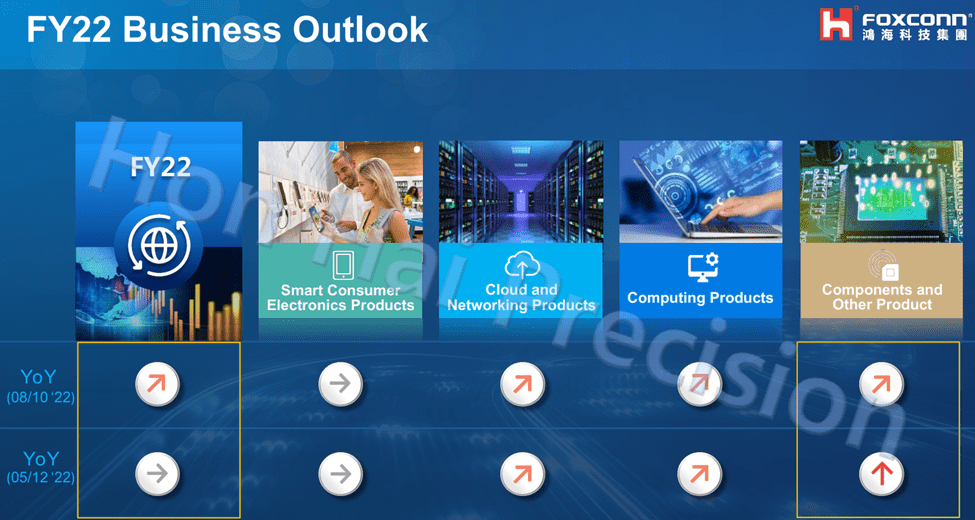

Beyond the next quarter, management also revised up its full-year guidance from flattish YoY (previously guided in May) to up YoY. Specifically, the updated revenue growth guidance implies +10% YoY growth at the midpoint and a strong 13% YoY revenue increase in Q4 2022 (an acceleration relative to the +7% YoY in Q3 2022). This comes despite a slight downward revision in the "component and others" segment growth this year, given some of the components produced during the China lockdowns were allocated elsewhere (mainly its own consumer products). Still, the strong guidance highlights management's confidence in the outlook in the face of market concerns about consumer weakness in the back half of the year. Given its strategic shift toward high-end products and its proven capability to serve as a stable supply source during market volatility, I feel comfortable underwriting the stronger outlook as well.

Over the mid-term, the FY25 gross margin target was also maintained at 10%, although there could be incremental upside from its cost optimization and product mix upgrade initiatives, as well as its planned EV business expansion. The latter offers massive optionality to earnings, in my view, with Hon Hai's target for NT$1tn (or $33bn) of high-margin revenue contribution by 2025 remaining intact.

{kind=link}

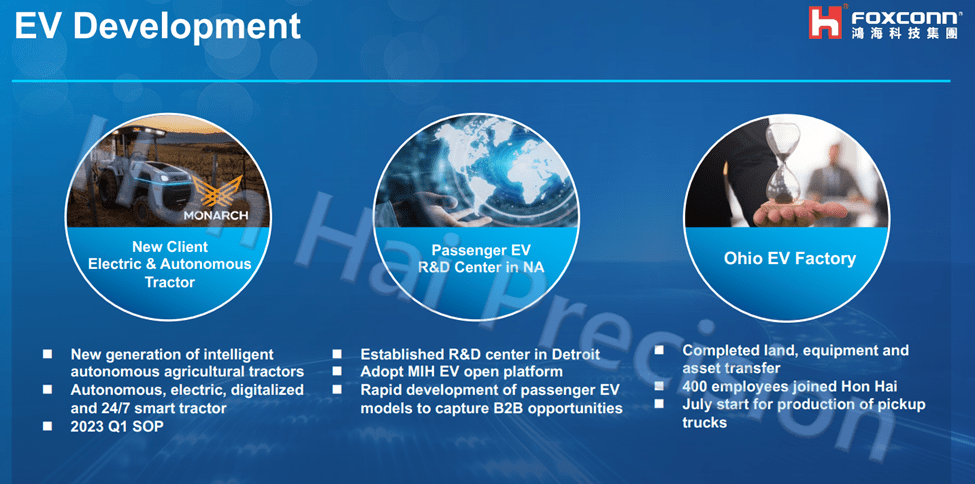

On Track For EV Expansion

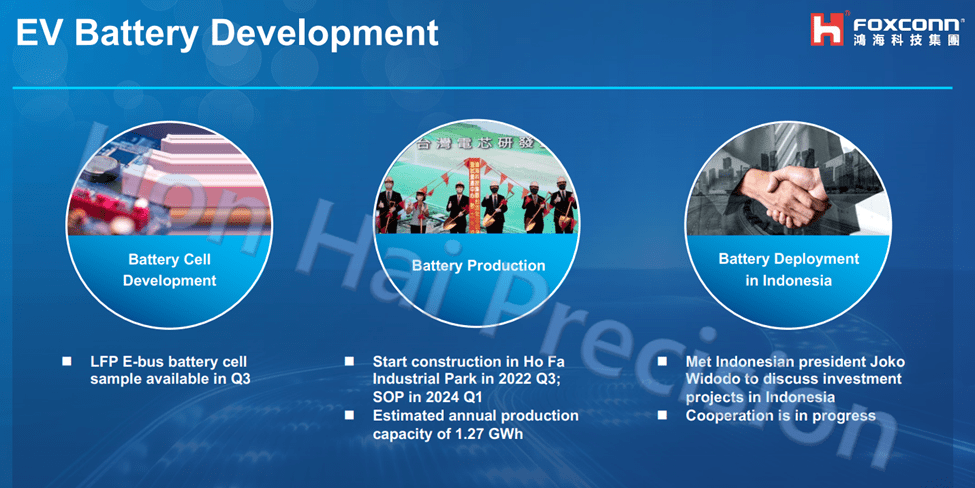

Over the mid to long run, EV remains the key growth initiative. Hon Hai's planned EV development is broad-based, spanning not only assembly but also components such as semiconductors and batteries (note lithium iron phosphate battery production in Taiwan is slated to start in Q1 2024 with a planned capacity of ~1.3GWh). Thus far, the company's traction has been positive - production of Lordstown's pick-up trucks is set for July, while the mass production of Monarch Tractor's electric tractors and battery packs will begin in Q1 2023 at the Ohio site (500k-600k units of annual capacity). These new production orders should significantly ramp up utilization at the Ohio facility ahead of the mass production of Fisker's ( FSR ) passenger cars in 2024, which is set to be a key earnings driver as well.

{kind=link}

Going forward, the target for ~5% market share and ~40% vertical integration (focused on battery and semiconductors) remains intact as Hon Hai looks to hit its 10% gross margin target by 2025. While this seemed ambitious initially, I suspect these numbers could prove conservative down the line, given the ongoing supply chain challenges that have emphasized Hon Hai's best-in-class supply chain capabilities. Plus, Hon Hai's EV business adds a different business model to the industry - by outsourcing design and manufacturing to Hon Hai, clients get to expand into new markets quickly and focus on branding and marketing, while the broader industry gains from lower entry barriers.

Beyond 2022/2023, which will focus mainly on commercial EVs with smaller volume/revenue contributions, 2024 will be the key year for the business as the mass production of passenger EVs by Fisker kicks off. Other key milestones to watch include the start of mass production at the Thailand production base (150k units/year of capacity), as well as progress on the EV battery and LiDAR (i.e., remote sensing) fronts.

{kind=link}

Shining Through The Volatility

Hon Hai's solid Q2 2022 results and updated guidance confirm what most investors already knew - this is a company with robust operational capabilities, well-positioned to weather any end-demand headwinds and supply chain volatilities. The margin profile is not only defensive on account of its best-in-class supply chain management and component sourcing capabilities but also offers ample room for upside as management renews its focus on driving operational efficiency. Importantly, these core competencies will prove invaluable in a highly volatile market, driving stable P&L gains through a potential macro downcycle.

Meanwhile, Hon Hai's execution of its EV strategy has also yielded several key milestones already, and its mid-term targets remain well within reach. On balance, I see room for a valuation re-rate from the current 11-12x P/E, as the company's competitive positioning shines through the volatility, while successful execution of new business opportunities adds incremental optionality to the investment case.

For further details see:

Hon Hai Precision: Shining Through The Volatility