BA - Honeywell: Good Near-Term And Long-Term Growth Prospects

2023-10-18 14:13:47 ET

Summary

- Honeywell's revenue growth is expected to benefit from a healthy backlog and easing supply chain challenges.

- Strong demand in the Aerospace and Performance Material and Technologies segments will contribute to the company's growth.

- Honeywell's margin outlook is favorable, with benefits from pricing actions, productivity gains, and volume leverage.

Investment Thesis

Honeywell International’s ( HON ) revenue growth should benefit from a healthy backlog and easing supply chain challenges, which should improve backlog-to-sales conversion. In addition, the company should also benefit from strong demand in the Aerospace, and Performance Material and Technologies segments. In the long run, the company's growth is poised to benefit from megatrends like automation, sustainability, and growing demand in the aerospace market. The margin outlook is also favorable with benefits from pricing actions, productivity gains, and volume leverage. The valuation is lower than historical averages and looks attractive at current levels.

Revenue Analysis and Outlook

Honeywell has posted low-to-mid single-digit growth in recent quarters with strength in the Aerospace and Performance Material and Technologies segment more than offsetting weakness in the Safety and Productivity Solutions segment. In the second quarter of 2023, the company posted a 2% Y/Y increase in net sales to $9.146 billion led by a 3% Y/Y increase in organic sales. The increase in organic sales was attributed to double-digit organic sales growth in commercial aerospace, process solutions, and UOP businesses. Forex headwinds negatively impacted net sales by 1%.

HON’s Historical Revenue Growth (Company Data, GS Analytics Research)

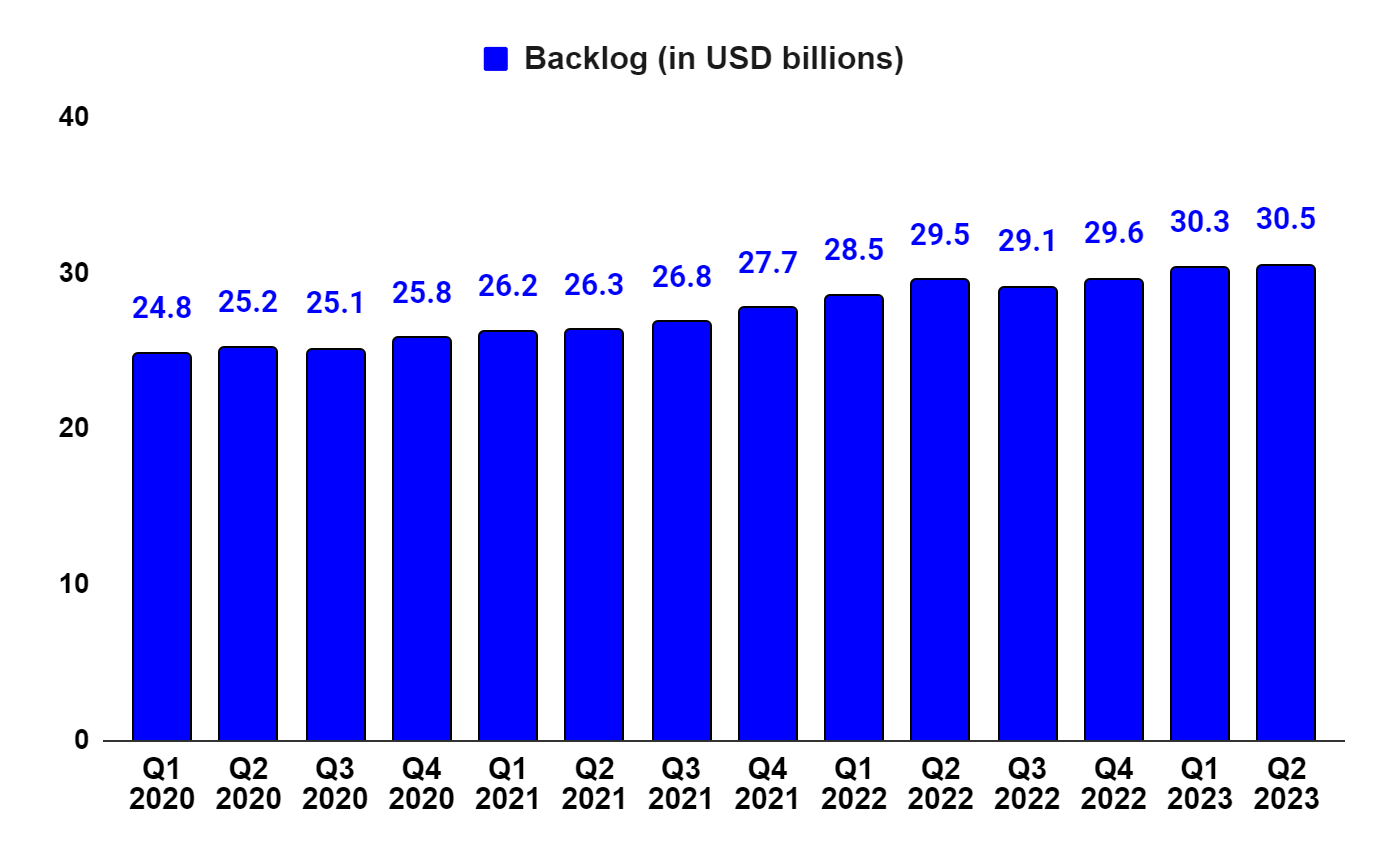

Looking forward, I am optimistic about Honeywell’s growth prospects. The company reported 4% Y/Y in backlog last quarter which increased to $30.5 billion. This increased backlog coupled with easing supply chain constraints, which should improve backlog to sales conversion, bodes well for the company’s near-term growth.

HON’s Historical Backlog Growth (Company Data, GS Analytics Research)

{kind=link}

The end market outlook also remains positive. The company’s Aerospace end-market is benefitting from the increase in flight hours, resulting in solid aftermarket demand. The original equipment sales are also improving as build rates increase at both Boeing ( BA ) and Airbus ( EADSF )( EADSY ). The supply chain disruptions have impacted production over the last couple of years but with sequential improvement in the supply chain environment, the company sales should benefit. The demand drivers for defense and space business also remain solid with the rising geopolitical tensions resulting in increased emphasis on defense spending across the world.

In the Performance Material and Technological business, which is exposed to the energy and specialty chemical market, the backlog remains healthy and the company is seeing robust demand for petrochemicals and refining catalysts. This business also has long-term drivers in the form of transition towards renewable energy and sustainability trends. Honeywell is well positioned to capture this trend with a full suite of biofuel technologies, process and separation technologies for CCUS (Carbon Capture, Usage, and Storage) and Hydrogen, and a leading position in sustainable refrigerants and electronic material.

The near-term outlook for the Honeywell Building Technologies segment outlook is somewhat mixed. This business is exposed to the non-residential end market. While the backlog in this segment is healthy, the slower-than-anticipated return-to-office trend is impacting demand from corporate customers. The demand from institutional clients in verticals like education is strong though thanks to government stimulus programs that are incentivising spending on upgrading HVAC systems. The long-term outlook for this segment is good given its exposure to energy efficiency and sustainability megatrends. I expect flattish sales in the back half for this business with improvement in FY24 and beyond.

The company's Safety and Productivity Solutions (SPS) business has been under pressure for the past few quarters after strong FY20 and FY21 sales growth. One specific area of weakness in this business is warehouse automation work. During the Covid period, there was a good deal of investment in warehouses due to rising e-commerce sales. However, this trend has reversed with the economy reopening and has impacted the segment sales in recent quarters. The company has also seen some softness in demand for short-cycle products due to macro uncertainty. However, the demand for services has remained healthy. According to management , the company's SPS portfolio is “bouncing on the bottom of the cycle.” While the timing of recovery in this business is hard to predict, the sales decline should end next year based on easing comparisons and for FY24 this business can deliver flattish sales.

The company is focusing on capitalizing on three megatrends for driving medium to long-term growth - Automation, Future of Aviation, and Energy transition. The recent trend towards reshoring coupled with the high cost of labor and labor shortages in the U.S. are expected to drive a multi-year growth in Automation investments. The reprioritization of defense spending across the globe due to rising geopolitical tensions, investment in drones as well as space technologies, and growth in global flying passengers is expected to drive good growth in the Aviation market. Further, the focus on sustainability as well as energy security is driving investment in the energy market (especially renewables) and Honeywell is well-positioned to benefit from it.

The company has recently announced a change in its business segments to align them better toward these megatrends.

HON’s Reorganized Reporting Structure Effective Beginning First Quarter 2024 (Company’s Presentation)

This segment realignment improves the clarity around the company's growth drivers and I expect Honeywell to further strengthen its portfolio around these megatrends through M&A in the future.

Overall, in the near term, strong growth in Aerospace coupled with good growth in Performance Materials and Technologies and flattish sales in Building Technologies should more than offset weakness in the Safety and Productivity Solutions (SPS) business and drive growth. As the company sees easing comps in the SPS business starting next year and benefits from the megatrends discussed above, its growth rate should further accelerate in FY24. So, I am optimistic about the company's growth prospects.

Margin Analysis and Outlook

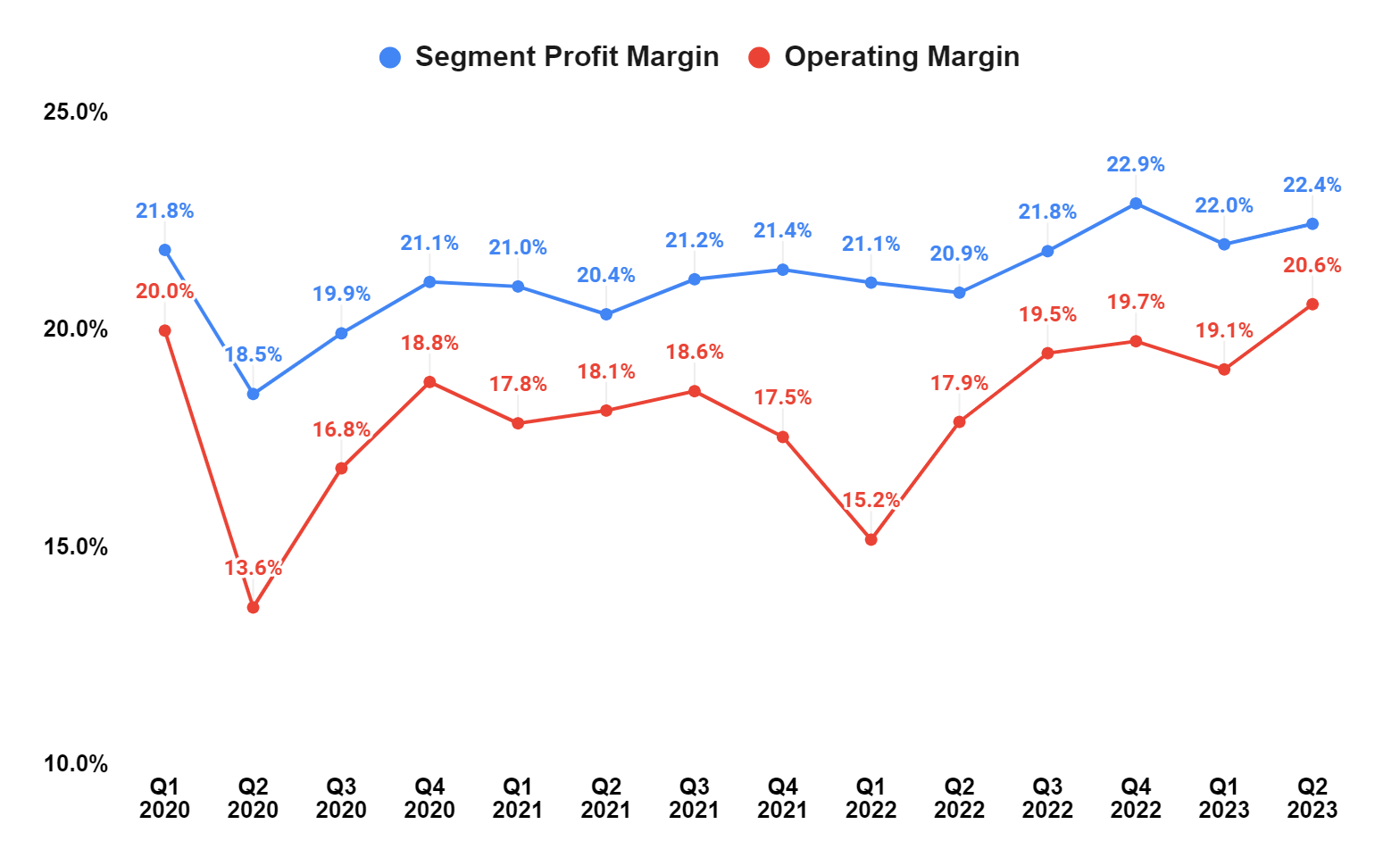

In Q2 2023, the company’s operating margin improved by 270 bps Y/Y to 20.6% and the total segment margin improved by 150 bps Y/Y to 22.4%. In terms of the segments, the Aerospace segment margin expanded by 120 bps Y/Y helped by volume leverage. Despite the decline in net sales, the HBT margin increased by 200 bps Y/Y and the SPS margin increased by 410 bps attributed to a pricing increase and productivity actions. However, the PMT segment margin declined 60 bps Y/Y due to challenges in the advanced materials business due to disruption at one of its production facilities. Margin expansion in the Aerospace, HBT, and SPS segments more than offset the lower PMT segment’s margin and resulted in a Y/Y increase in the total segment profit margin for the company.

HON’s Segment Profit margin and Operating margin (Company Data, GS Analytics Research)

{kind=link}

HON’s Segment Wise Profit margin (Company Data, GS Analytics Research)

{kind=link}

Looking forward, I expect the company's margin to continue benefiting from price actions. The company's investment in Honeywell Digital has enabled it to implement surgical pricing actions for specific product lines and improve price/cost and I expect it to be a driver for margin expansion in the future as well. The company should also benefit from productivity improvement and volume leverage from growing sales.

Valuation and Conclusion

Honeywell is trading at 20.36x FY23 consensus EPS estimate of $9.15 and 18.54x FY24 consensus EPS estimate of $10.05. This is a discount versus the company’s 5-year historical forward P/E of 22.71x.

I like the company’s good long-term growth prospects given its exposure to megatrends like automation, sustainability, and growing aerospace demand. The company has also done a good job in terms of improving margins and I expect continued benefit from pricing actions, productivity initiatives, and volume leverage. The stock’s lower-than-historical valuation looks attractive and I believe, as the decline in SPS business sales ends due to easing comparisons next year and the company's growth continues to benefit from megatrends, HON stock’s valuation can see a re-rating. Hence I have a buy rating on Honeywell.

For further details see:

Honeywell: Good Near-Term And Long-Term Growth Prospects