HOFT - Hooker Furnishings: A Good Opportunity For Long-Term Investors

2023-03-17 02:46:11 ET

Summary

- Net sales are stagnant as consumer demand is expected to slow down in the coming fiscal year.

- Despite recent improvements, profit margins remain depressed due to higher-than-usual freight costs.

- The balance sheet is weak, but high inventories will likely enable strong cash from operations in the coming quarters.

- The dividend is at risk of being cut due to the current headwinds.

- The current share price decline represents a good opportunity for long-term dividend investors with the ability to tolerate some risks in the short and medium term.

Investment thesis

Hooker Furnishings Corporation ( HOFT ) is in a relatively delicate position at the moment, and this is currently reflected in its share price, which is 61% below all-time highs. Inflationary pressures (especially higher-than-usual freight costs) are eroding profit margins while the company's net sales are expected to stay stagnant for the coming fiscal year due to weak consumer demand. Added to this is the risk of a (more or less) deep recession as a result of the recent interest rate hikes carried out by central banks with the aim of stabilizing current inflation rates, which are still very high.

But despite these headwinds and risks, I consider that this is a moment to consider the current pessimism as an opportunity for the long term because, although it is true that the dividend suffers from the possibility of being cut as a consequence of lower cash generation, it has been sustainable over the years while the current dividend yield (on cost) currently stands at over 4% at current share prices. Although the balance sheet is currently weak due to low cash and equivalents, I believe high inventories will likely allow the company to navigate current and potential headwinds and, in the long run, investors who have been confident in the company's future will enjoy a high dividend yield on cost or, failing that, high capital returns.

A brief overview of the company

Hooker Furnishings Corporation is a designer, manufacturer, importer, and seller of casegoods (wooden and metal furniture), leather furniture, fabric-upholstered furniture, and outdoor furniture for the residential, hospitality, and contract markets. The company also manufactures premium residential custom leather and custom fabric-upholstered furniture. The company was founded in 1924 and its market cap currently stands at ~$226 million, employing over 1,000 workers.

Hooker Furnishings (2021 Annual Report)

{kind=link}

The company operates under three main business segments: Hooker Branded, Home Meridian, and Domestic Upholstery. Under the Hooker Branded segment, which provided 33.8% of the company's total net sales in 2022, the company offers home entertainment, home office, accent, dining, and bedroom furniture in the upper-medium price points sold under the Hooker Furniture brand, as well as imported upholstered furniture targeted at the upper-medium price-range. Under the Home Meridian segment, which provided 47.0% of the company's net sales in 2022, the company owns a wider range of recognized furnishing brands, including Accentrics Home, Pulaski Furniture, Samuel Lawrence Furniture, Prime Resources International, Samuel Lawrence Hospitality, and HMidea. And lastly, under the Domestic Upholstery segment, which provided 17.2% of the company's total net sales in 2022, the company offers seating upscale motion and stationary leather furniture, upscale occasional chairs, settees, sofas, and sectional seating with an emphasis on cover-to-frame customization, as well as private label sectionals, modulars, sofas, chairs, ottomans, benches, beds and dining chairs in the upper-medium price points for lifestyle specialty retailers.

Currently, shares are trading at $20.49, which represents a 61.16% decline from all-time highs of $52.75 on December 06, 2017, and a 52.24% decline from recent highs of $42.90 on June 04, 2021. Such a price decline in a company that has successfully operated for a century may represent a good opportunity for those long-term dividend growth investors as the current dividend yield on cost starts from a fairly high point, but before jumping in, it's very important to understand why investors have punished the company so severely in recent years, as well as the risks associated.

First of all, I am going to make a brief summary of the latest acquisitions.

Recent acquisitions

In February 2016, the company acquired Home Meridian International for around $100 million. Part of the acquisition was financed with debt ($85 million), and another part with share issuances ($15 million). Thanks to this acquisition, the company's net sales more than doubled as it was a major one. Later, in September 2017, it acquired Shenandoah Furniture, a Valdese, North Carolina-based upholstery manufacturer, for $40 million.

And the latest acquisition took place in January 2022 when the company acquired Sunset West, a leading west coast-based manufacturer of outdoor furniture. With this acquisition, Hooker Furnishings entered the outdoor furniture segment, which is expected to grow at a CAGR of over 4% by 2028.

Net sales are expected to remain stagnant in the coming year

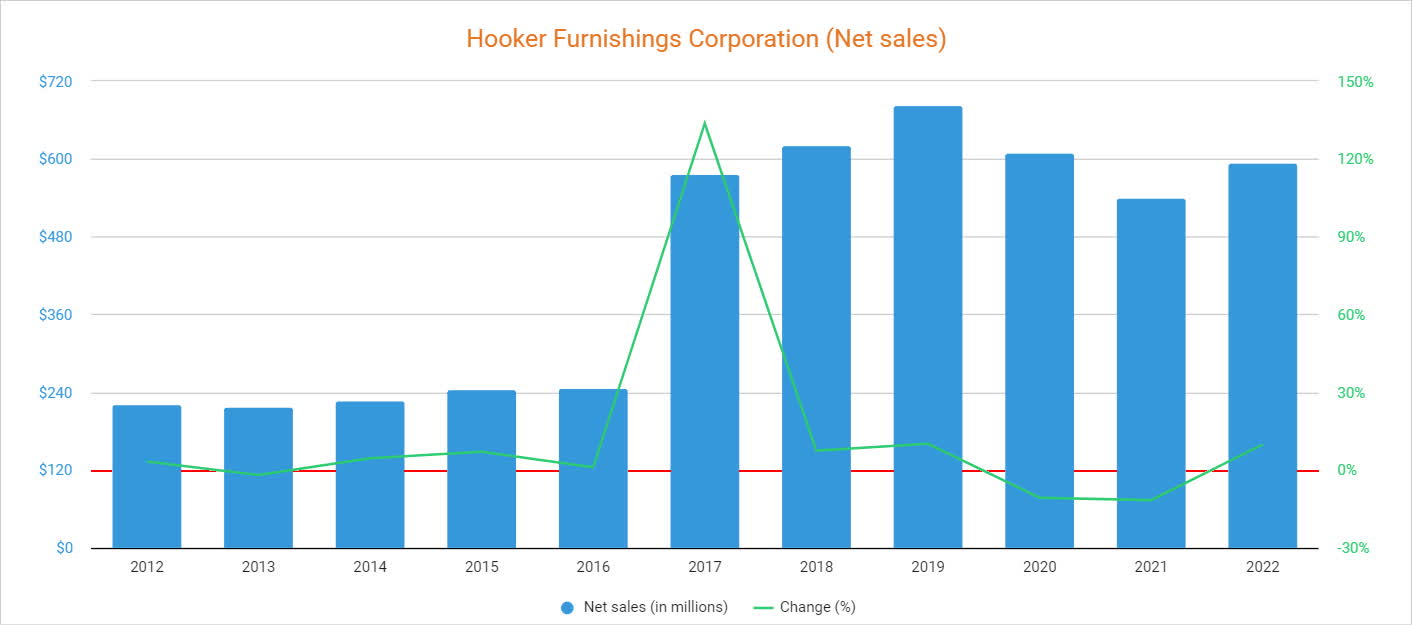

Net sales increased by 133.69% during fiscal 2017 thanks to the acquisition of Home Meridian, and by 7.52% in fiscal 2018 and 10.13% in fiscal 2019 thanks to the acquisition of Shenandoah Furniture, but softer retail activity caused a decline of 10.63% during fiscal 2020 and the coronavirus pandemic crisis another 11.58% decline in fiscal 2021. Nevertheless, net sales increased by 9.91% in fiscal 2022 as the restrictions derived from the coronavirus have been lifted. Still, the current trailing twelve months' net sales of $586.6 million represent a 1.18% decline compared to fiscal 2022 as demand has slowed down in recent quarters.

Hooker Furnishings Corporation net sales (10-K filings)

{kind=link}

In this regard, net sales declined by 9.55% year over year during the first quarter of fiscal 2023, by 5.91% during the second quarter, but increased by 13.60% during the third quarter boosted by the acquisition of Sunset West and increased demand in all the other domestic upholstery divisions, as well as higher net sales from Home Meridian. This means that while net sales have dropped significantly during the first half of fiscal 2023 they appear to be stabilizing during the second half and are estimated to remain flat in fiscal 2024.

The recent decline in the share price, coupled with a net sales rebound in fiscal 2022 and a stabilization in fiscal 2023, has caused a drop in the P/S ratio to 0.413, which means the company currently generates net sales of $2.42 for each dollar held in shares by investors, annually.

This ratio is 38.81% lower than the average of 0.675 during the past decade, and 73.34% lower than the peak of 1.549 reached during the first half of 2016, which means investors are placing less value on the company's net sales. This is explained, in my opinion, by five main factors that I will discuss throughout the article: two margin contractions since fiscal 2020, flat net sales forecasts for the coming fiscal year, a weaker balance sheet, increasing recessionary concerns, and a more risky dividend.

Margins are showing some signs of stabilization after a strong blow

The company used to enjoy gross profit margins of over 20% and EBITDA margins of almost 10% until fiscal 2020 when lower sales due to weaker retail activity caused a significant decline in volumes. Then, in fiscal 2021, the coronavirus pandemic outbreak caused another slump in volumes, and now profit margins are being eroded again due to inflationary pressures (especially higher freight costs).

Nevertheless, both gross profit and EBITDA margins have shown strong signs of improvement during the past quarter as they stood at 21.12% and 5.79%, respectively, despite higher salary and benefits costs and higher commission rates. This was possible thanks to higher net sales, the exit of unprofitable businesses at Home Meridian, and the mitigation of supply chain bottlenecks that were affecting the company for 2 years. In this regard, both gross profit and EBITDA margins will remain abnormally low as long as freight costs remain higher than usual.

The balance sheet is weak, but debt is widely manageable

The company borrowed $60 million for the Home Meridian acquisition in fiscal 2017 and another $12 million for the acquisition of Shenandoah in fiscal 2018, but successfully deleveraged the balance sheet by fiscal 2021. Now, long-term debt increased again to $25 million as cash acquisitions were $25.9 million during the first quarter of fiscal 2023 due to the acquisition of Sunset West.

Said debt is very low if we take into account interest expenses of $0.43 million during the past quarter vs. cash from operations of $7.3 million. But what makes the current debt load a virtually non-existent risk is very high inventories of $134 million vs. long-term debt of $24.6 million.

This means that the company has the ability to generate strong cash from operations in the coming quarters (despite lower profit margins) by reducing its inventory levels. In this regard, the management expects to reduce inventories by $25 million in the coming twelve months in order to reinforce the company's cash position, which is currently weak as cash and equivalents are very low at $6.51 million.

The dividend is not as safe as it used to be

The company enjoys a long-track history of dividend payments and raises. Following a stagnation in the quarterly dividend at $0.10 per share in the 2013-2015 period, dividend raises for seven consecutive years have more than doubled the dividend payout to $0.22 per share.

These raises, coupled with the current decline in the share price, have caused a spike in the dividend yield to 4.29%. Even so, it is very important to take into account that the dividend is at risk of being cut in the short and medium term as a consequence of current inflated freight costs. In this regard, I will present the company's cash payout ratio in the following table by calculating what percentage of the cash from operations has been allocated to the dividend and interest expenses over the years and, later, I will assess the current capacity of the company to sustain the current dividend payout.

| Year |

| 2014 |

| 2015 |

| 2016 |

| 2017 |

| 2018 |

| 2019 |

| 2020 |

| 2021 |

| 2022 |

| Cash from operations (in millions) |

| $5.70 |

| $22.77 |

| $23.04 |

| $31.24 |

| $27.75 |

| $9.66 |

| $41.43 |

| $68.26 |

| $19.21 |

| Dividends paid (in millions) |

| $4.30 |

| $4.31 |

| $4.32 |

| $4.85 |

| $5.82 |

| $6.71 |

| $7.21 |

| $7.84 |

| $8.82 |

| Interest expenses (in millions) |

| $0 |

| $0.05 |

| $0.06 |

| $0.95 |

| $1.25 |

| $1.45 |

| $1.24 |

| $0.54 |

| $0.11 |

| Cash payout ratio |

| 75.51% |

| 19.15% |

| 19.04% |

| 18.59% |

| 25.46% |

| 84.54% |

| 20.39% |

| 12.27% |

| 46.50% |

Historically, the company has allocated a relatively low portion of cash from operations to pay dividends and interest expenses (except for fiscal 2019 and, most likely, 2023). Currently, trailing twelve months' cash from operations stands at -$26.9 million, but inventories increased by $56 million and accounts receivable by $2.4 million during the same period while accounts payable increased by only $13.7 million. Furthermore, cash from operations was $7.3 million during the third quarter of fiscal 2023 while inventories increased by $2.8 million quarter-over-quarter, and accounts receivable declined by $5.7 million but accounts payable also declined by $6 million, which means the company is currently profitable thanks to recent margin improvements, but the dividend is at risk of being cut as profit margins have not yet fully recovered from higher freight rates and recessionary risks are a growing concern as a result of recent interest rate hikes.

Share buybacks are taking place as the management takes advantage of lower share prices

The number of shares outstanding increased by 6.70% during fiscal 2016 as a consequence of the Home Meridian acquisition, and by another $1.63% during fiscal 2017. Nevertheless, the total number of shares outstanding declined by 4.95% year over year during the past quarter as the company invested $10 million in share repurchases. More share repurchases are to be expected in the coming quarters as the management authorized up to $20 million in early 2022.

In this regard, the management seems to be taking advantage of the current fall in share prices in order to reduce the impact of the share dilution of recent years as inventories are high enough to maintain strong cash from operations in the coming quarters.

Risks worth mentioning

Overall, the situation for Hooker Furnishings is, in my opinion, not as dire as its share price might suggest, especially in the long term. Nevertheless, there are a series of risks in the short and medium term that I would like to highlight as I consider that it is very important to keep them in mind before deciding to invest in the company's shares.

- Higher than usual freight costs are eroding the company's profit margins, and will keep doing so for as long as inflationary pressures and supply chain issues continue to affect the global economy as the company largely depends on imports to fulfill the demand of its customer base.

- Recent interest rate hikes are raising the risk of a (more or less) deep recession, which could have a significant impact on consumer spending capacity. Also, lower consumer confidence, as well as declining purchasing power due to high inflation rates, could have a significant impact on home sales in the coming quarters.

- If profit margins do not stabilize soon as a result of inflated freight costs for a prolonged period, the dividend could be cut in order to preserve cash as, despite inventories being high at $134 million, cash and equivalents are very low at $6.5 million.

Conclusion

While it is true that the current situation for Hooker Furnishings is delicate due to supply chain issues and inflationary pressures, I believe that the future of the company in the long term is not as disastrous as its current share price suggests. The current margin contraction is directly linked to the macroeconomic context, which leads me to believe that these are actually temporary headwinds. The company has successfully operated for a century and, in my opinion, current cash from operations and inventories are enough to withstand current margin headwinds (and even a potential recession).

Therefore, I believe that long-term focused dividend investors should see the current share price as a good opportunity to obtain a high dividend yield on cost in the long term despite the risk of being cut in the short and medium term. We must always keep in mind that if the dividend is cut or even canceled and the management does not decide to restore it, investors can always obtain profits through capital gains once share prices reflect more optimism than the current one.

For further details see:

Hooker Furnishings: A Good Opportunity For Long-Term Investors