HOFT - Hooker Furnishings: Strong Valuation Metrics Tempered By Potential Dividend Risk

2023-06-20 18:56:39 ET

Summary

- Hooker Furnishings shows potential for growth with efficient inventory management, a strong recovery in its hospitality division, and promising expansion initiatives.

- However, concerns arise from a decline in sales, softer demand, operational inefficiencies, and a questionable Dividend Safety Score.

- Despite indicators of undervaluation, the inherent risks call for a cautious investor approach and monitoring of future developments.

Thesis

This article provides an analysis of Hooker Furnishings (HOFT) by delving into its financial metrics, performance indicators, and growth strategies. While certain aspects like efficient inventory management, robust recovery in its hospitality division, and promising expansion initiatives suggest promising potential, significant concerns arise from a decline in sales, softer demand, operational inefficiencies, and a questionable Dividend Safety Score. Despite indicators of undervaluation, the inherent risks call for a cautious investor approach

Company Overview

Hooker Furnishings Corporation is a comprehensive player in the home furnishings industry, with a substantial portfolio that covers both residential and commercial markets. The company creates, produces, and markets furniture ranging from household items to hospitality and contract furniture.

Delving into its portfolio, Hooker's branded segment delivers various design categories, comprising home entertainment, home office, accent, dining, and bedroom furniture under the well-established Hooker Furniture brand. The Hooker Upholstery brand is the company's gateway into the imported upholstered furniture market. In their Home Meridian segment, the Accentrics Home brand offers a wide selection of home furnishings.

Additionally, it provides an array of furnishings, including bedroom, dining room, home office, and youth furniture, under the reputable Pulaski Furniture and Samuel Lawrence Furniture brands. The segment extends its reach into the leather motion upholstery market with the Prime Resources International brand. Notably, under the Samuel Lawrence Hospitality name, they design and supply furnishings specifically tailored for high-end hotels.

The HMidea brand focuses on ready-to-assemble furniture, catering to the growing demand for convenience in the home furnishing sector. Switching gears to the Domestic Upholstery segment, the company provides an impressive selection of motion and stationary leather furniture under the Bradington-Young brand. It also offers a range of upholstered furniture through the Sam Moore Furniture and Shenandoah Furniture brands, which target lifestyle specialty retailers.

Adding another feather to its cap, Hooker also supplies upscale senior living facilities with premium upholstered seating and casegoods under the H Contract brand, while its Lifestyle Brands name offers products for interior designers.

In terms of distribution, Hooker Furnishings has an extensive reach across North America, leveraging various channels from independent furniture stores and department stores to e-commerce platforms and warehouse clubs. Established in 1924, this long-running company stands as an indicator of its resilience and adaptability in meeting market changes. Headquartered in Martinsville, Virginia it has established strong roots and experience within its industry to remain successful over time.

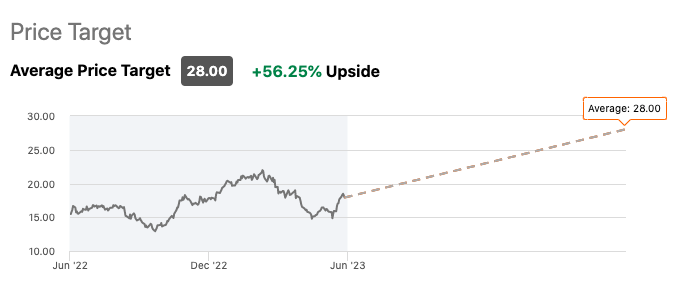

Expectations

Currently, there is only one "Strong Buy" Wall Street rating with a generous forecast for 50%+ upside potential.

{kind=link}

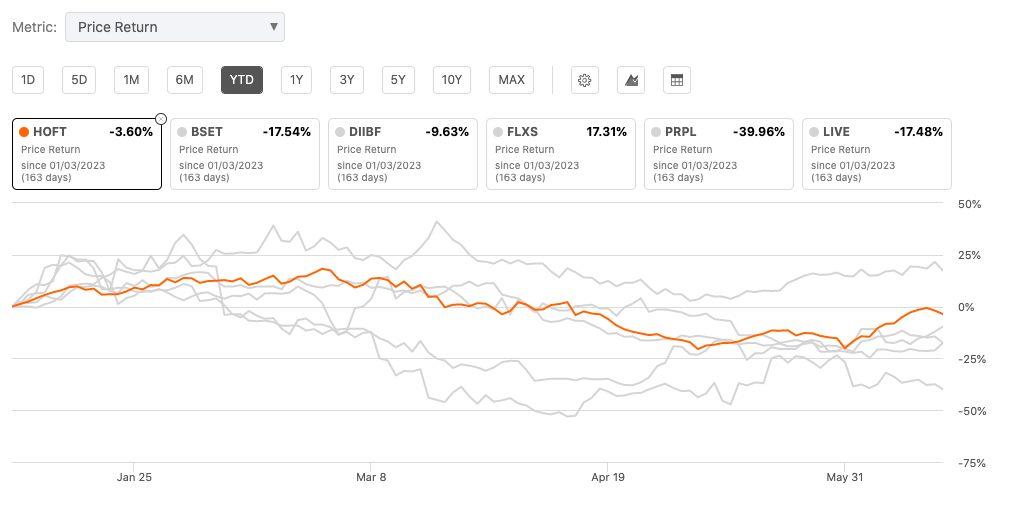

Performance

Performance-wise, Hooker Furnishings is slightly negative YTD (at the time of this writing), however, the bright spot being that it has outperformed the majority of its peers with the exception of FLXS.

{kind=link}

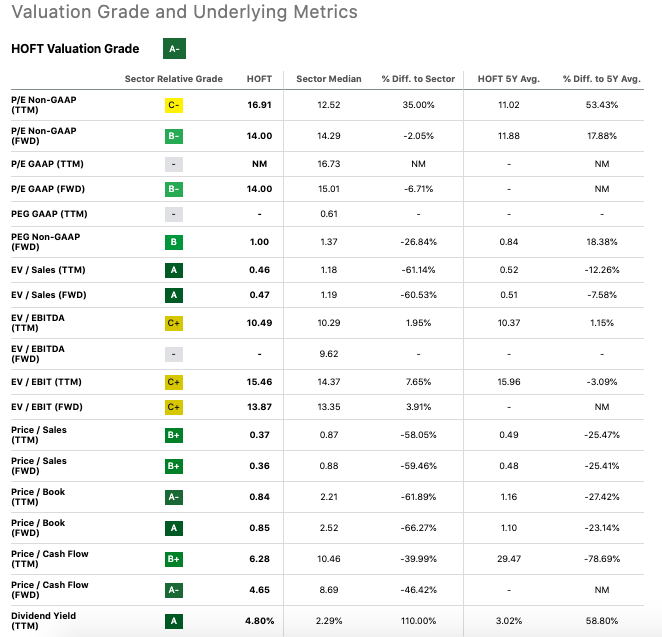

Valuation

Firstly, the valuation grade of A- (see below) indicates that the market generally perceives HOFT as relatively undervalued. While HOFT's forward and trailing non-GAAP P/E ratios are slightly above their respective five-year averages, this is somewhat offset by the fact that HOFT's forward P/E ratio is below the sector median, suggesting potential upside from a P/E perspective. That said, its GAAP P/E and EV/EBITDA ratios are not exactly shining stars in the mix, possibly indicating a bit of skepticism about the company's earnings quality or stability of cash flows.

{kind=link}

HOFT's forward non-GAAP PEG of 1.00, which compares favorably to the sector median, is a bullish sign, indicating the company's earnings growth could potentially justify its P/E multiple. However, the above five-year average PEG suggests the growth has become pricier than it has been historically, raising some caution.

The standout figures here are the valuation multiples based on sales, book value, and cash flow. HOFT has significantly lower Price/Sales, EV/Sales, Price/Book, and Price/Cash Flow ratios compared to the sector median and their respective five-year averages, indicating HOFT is undervalued on these metrics.

These attractive valuation multiples, coupled with a significant dividend yield (more on that below in "Risks & Headwinds) that's about double the sector median, make HOFT look quite appealing from an income perspective.

{kind=link}

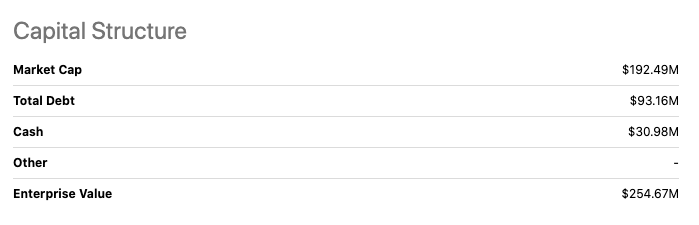

In terms of capital structure (see above), HOFT has a relatively small market cap of $192.49M. Its enterprise value is higher than its market cap due to the net debt on its balance sheet ($93.16M in total debt less $30.98M in cash). This moderately leveraged position implies that the company is using debt to finance its operations and investments, which could boost returns in a successful scenario, but also increase risk in a downturn.

In summary, while HOFT's P/E ratios and PEG ratio point to a fair-to-slightly high valuation relative to earnings, the company's Price/Sales, Price/Book, Price/Cash Flow multiples, and high dividend yield suggest a possible undervaluation

Q1 2024 Bullish Earnings Takeaways

First and foremost, let's look at Hooker Furnishings' inventory management strategy. It's clear that, despite facing a sales slowdown, the company has demonstrated proficient inventory management in aligning supply with demand. They have successfully navigated the delicate equilibrium of avoiding both overstocking and stockouts.

While it's true that inventory levels remain elevated beyond pre-pandemic figures, the strategic efforts to streamline inventory and synchronize it with present demand are evident and appear to be progressing effectively. Furthermore, it's worth underscoring the fact that the company hasn't been impacted by inventory obsolescence, which can potentially erode profits. This is a testament to their tactical management of inventory, ensuring the right products are available at the right time, thus mitigating the risk of unsellable, outdated stock.

Moving on to their hospitality division, there are compelling indicators of robust recovery. The division, identified as SLH, has charted an impressive performance with net sales doubling in comparison to the same period in the prior year. This uptick points to a strong revival in the hospitality sector following the COVID pandemic, suggesting a regained consumer confidence and spending potential in this area.

In terms of Hooker Furnishings' financial health, their cash position and dedication to shareholder returns are certainly commendable. At the close of the first quarter of fiscal 2024, the company maintained cash and cash equivalents amounting to $31 million. More significantly, Hooker Furnishings managed to generate $22 million in cash from its operations, proving their proficiency in converting business activities into cash, an integral determinant of financial stability.

At its core is an admirable commitment to shareholders. Through a share repurchase program, an estimated $20 million was returned directly back to shareholders - not only increasing shareholder value but also showing confidence in both itself and future prospects. Looking at future growth opportunities, there's an encouraging trend in incoming orders. The company reported a positive trajectory for consolidated incoming orders in May and June. This could potentially serve as a precursor to increased future sales, provided the company continues to deliver on customer expectations and market demands.

Finally, it's essential to note Hooker Furnishings' ongoing expansion initiatives. The company is proactively enhancing its visibility and expanding its reach within the market. The upcoming debuts of new showrooms in Atlanta and Las Vegas testify to their proactive market engagement strategy. By establishing a physical presence in key market areas, the company is likely to broaden its customer base and reinforce its brand presence, both of which could potentially translate into an increased market share and greater sales volume.

Risks & Headwinds

Analyzing Hooker Furnishings' recent results, the key point that immediately emerges is the significant decline in consolidated net sales, which have tumbled by 17%. This dip in sales seems to be driven primarily by the lower performance in the Home Meridian segment and the domestic upholstery segment. The cause behind this revenue contraction could be multifold, from changing consumer preferences to increased market competition, and it's certainly a pressing concern that could impact the company's financial outlook if not addressed in a timely and effective manner.

Further compounding these challenges is the softer demand observed in the current quarter. The company has been grappling with subdued consumer interest, which has necessitated an increase in discounting to stimulate sales. This approach, while effective in the short term, tends to compress profit margins and could potentially compromise the company's bottom line if the demand scenario doesn't improve.

Another factor raising eyebrows is the lower backlog for the Hooker Branded segment compared to the prior year. In my view, a lower backlog could serve as a potential warning sign, potentially indicating a reduction in future sales.

While it's noteworthy that the Home Meridian segment's operating loss improved in comparison to the previous year's first quarter, the fact remains that it is still in a loss-making position, reporting a $2.1 million operating loss. This implies that the segment is still grappling with efficiency or demand challenges, or potentially both, requiring strategic rethinking and operational improvements.

Digging deeper into the Home Meridian segment, the decrease in incoming orders and backlog could suggest further sales contraction on the horizon. The combination of reduced orders and a lower backlog is rarely a positive sign and is indicative of potential future difficulties.

The company is still navigating a few unresolved external factors such as the retail environment, fluctuations in ocean freight rates, and economic uncertainties. Each of these could pose a risk to the company's future performance. Ocean freight rates can directly impact their cost base, particularly for a company dealing in physical goods, and any global economic uncertainties could dampen consumer demand or create supply chain hiccups.

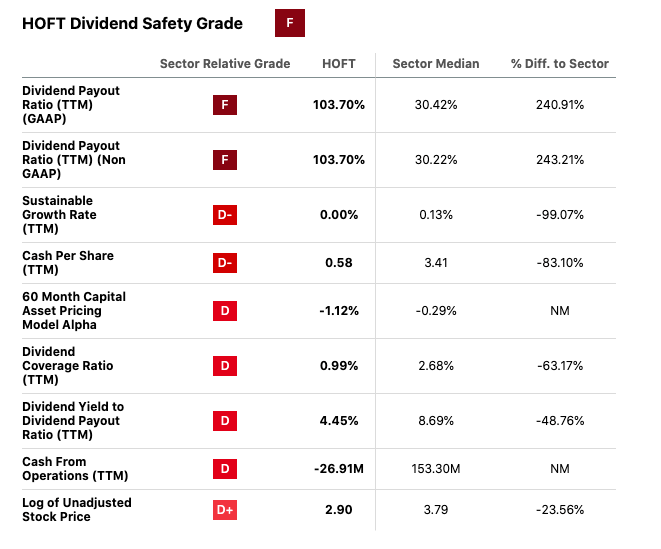

And finally, the Dividend Safety Score of F (see below) is an unmistakable red flag for those relying on HOFT's dividend for income. The fact that almost two-thirds of stocks with such a low score have historically cut their dividends implies that the chances of a similar action by HOFT are not non-trivial.

{kind=link}

The company's Dividend Payout Ratios (both GAAP and Non-GAAP) of 103.70% are substantially above the sector median and signal financial strain. In essence, HOFT is paying out more in dividends than it's earning, which is an unsustainable strategy in the long run. It either has to increase its earnings, reduce its dividend, or resort to its reserves or debt, which could have negative implications for its financial health and share price.

The Sustainable Growth Rate of 0.00% shows that, given its current return on equity and dividend payout ratio, the company's capacity for sustainable growth is virtually nil. This could mean a slowdown in expansion or development, which may further hamper its ability to improve its earnings and maintain its dividend.

Final Takeaway

Hooker Furnishings presents a mixed bag of financial indicators with some strong signals of potential upside and concerning signs of downside risk. Positive factors include proficient inventory management, robust recovery in the hospitality division, substantial shareholder returns, and promising expansion initiatives. However, a significant decline in sales, softer demand, operational inefficiencies, and a troubling Dividend Safety Score weigh down on the overall prospect. The analysis points to a potential undervaluation, yet given the potential risks, investors should hold the stock, monitor future developments closely, and seek potential improvement in earnings and sales to sustain the high dividend yield.

For further details see:

Hooker Furnishings: Strong Valuation Metrics Tempered By Potential Dividend Risk