HBNC - Horizon Bancorp: More Stability Than The Previous Quarter

2023-08-11 11:03:37 ET

Summary

- Horizon Bancorp's stock price has increased by 60% over the last three months.

- The banking industry is showing signs of recovery, with a decrease in bank failures and renewed confidence.

- Horizon Bancorp's deposits have declined for two consecutive quarters, but the cost of deposits remains relatively low compared to peers.

Since May 2023, Horizon Bancorp's ( HBNC ) price per share has increased by as much as 60 percent, yet the all-time high of $23.80 is still a long way off. 2023 has certainly not been an easy year for the entire banking industry, but the impression is that a glimmer of hope has been kindled in recent months. The long-awaited recession may not arrive, which is reviving cyclical sectors such as banking.

Overall, Horizon Bancorp's Q2 2023 did not include any positive surprises, but at the same time it was not as disastrous as predicted a few months ago in the midst of the banking crisis. At least for now, fortunately, bank failures have stopped and confidence is coming back.

Deposits and borrowings

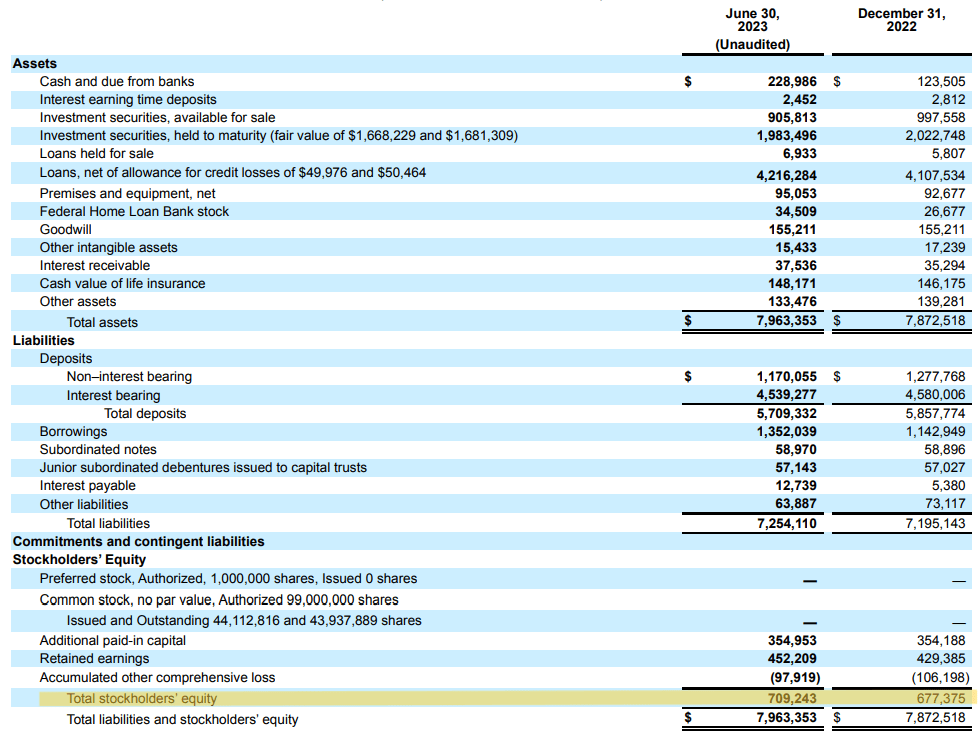

This is the second quarter in a row that average total deposits have declined and currently stand at about $5.6 billion. Since the Fed started with the rapid increase in interest rates, Horizon Bancorp has been forced to increase the yield on its deposits, otherwise it would have risked a mass exodus of its customers.

{kind=link}

The current average cost of total deposits is not that high, 1.35 percent versus 0.11 percent last year. This is a pretty good figure overall if compared to peers, but also if compared to the increase in the average yield on total loans. The latter, have had an increase of 43 basis points more than the cost of deposits since Q1, 2022.

The problem here lies in the growth in nominal terms rather than the percentage change in costs. In fact, average total deposits have not exceeded $5.9 billion for about two and a half years. Moreover, a further reduction in deposits is expected in the next quarter, albeit to a smaller magnitude than that seen in this quarter.

It is also likely that upward pressure on the cost of deposits may increase in the second half of 2023, but for now, CFO Mark Secor prefers to wait for better economic environments to attract new customers who might increase deposits. There is no rush to raise capital by offering higher interest rates than competitors; this would negatively affect margins.

There's still going to be some pressure. And as we start to get a little more clarity on rates and the potential pausing of the increases, I think we feel like we're going to be able to determine where those deposit pricing is going to end up and be able to manage that. And we said, we have the excess liquidity, and we don't have to chase every rate right now and be able to be a little more strategic in what we're going to be putting on, on the books for funding.

In other words, the current loan-to-deposit ratio of 75% combined with $100 million in excess cash allow Horizon Bancorp to have a flexible financial structure that does not currently require expensive funds.

{kind=link}

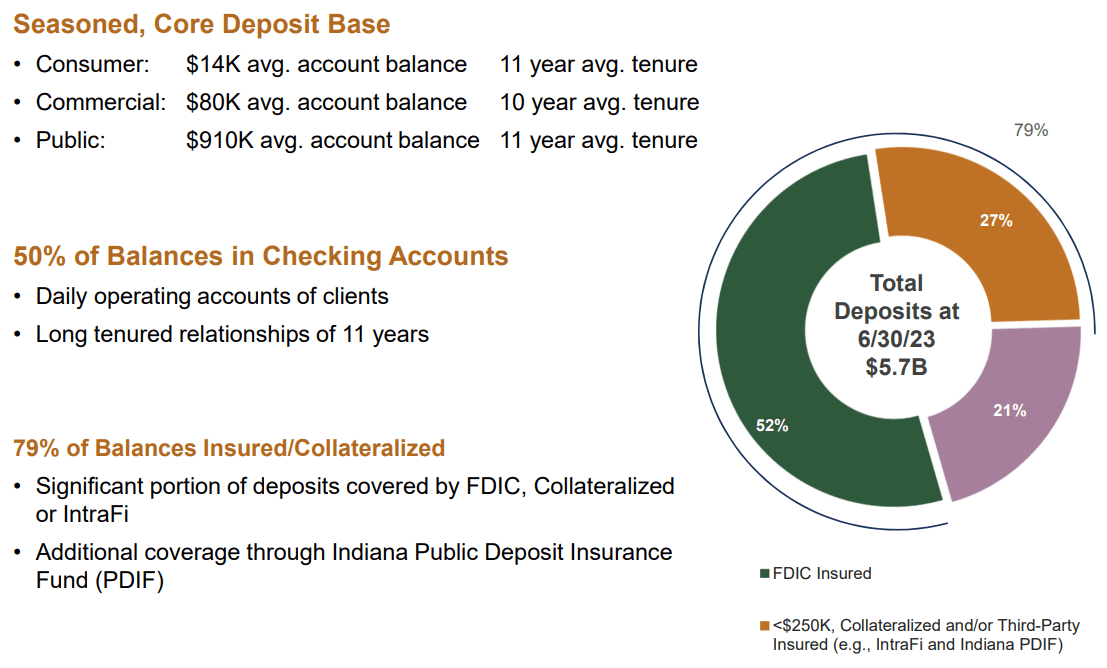

In addition, only 21% of deposits are not currently covered by the FDIC or other types of insurance.

Finally, regarding the use of borrowings in order to increase funds available, it is unlikely to happen in the coming quarters. Borrowing will be relatively flat because management is satisfied with current funds and does not want to worsen the net interest margin.

Loans and investment portfolio

Total loan growth in H1 2023 was rather sluggish, only 2.60%. This was a predictable result since at current rates it benefits very little for companies and households to take on debt. However, according to management the second half will be different, and the expected growth is between 6-8%.

{kind=link}

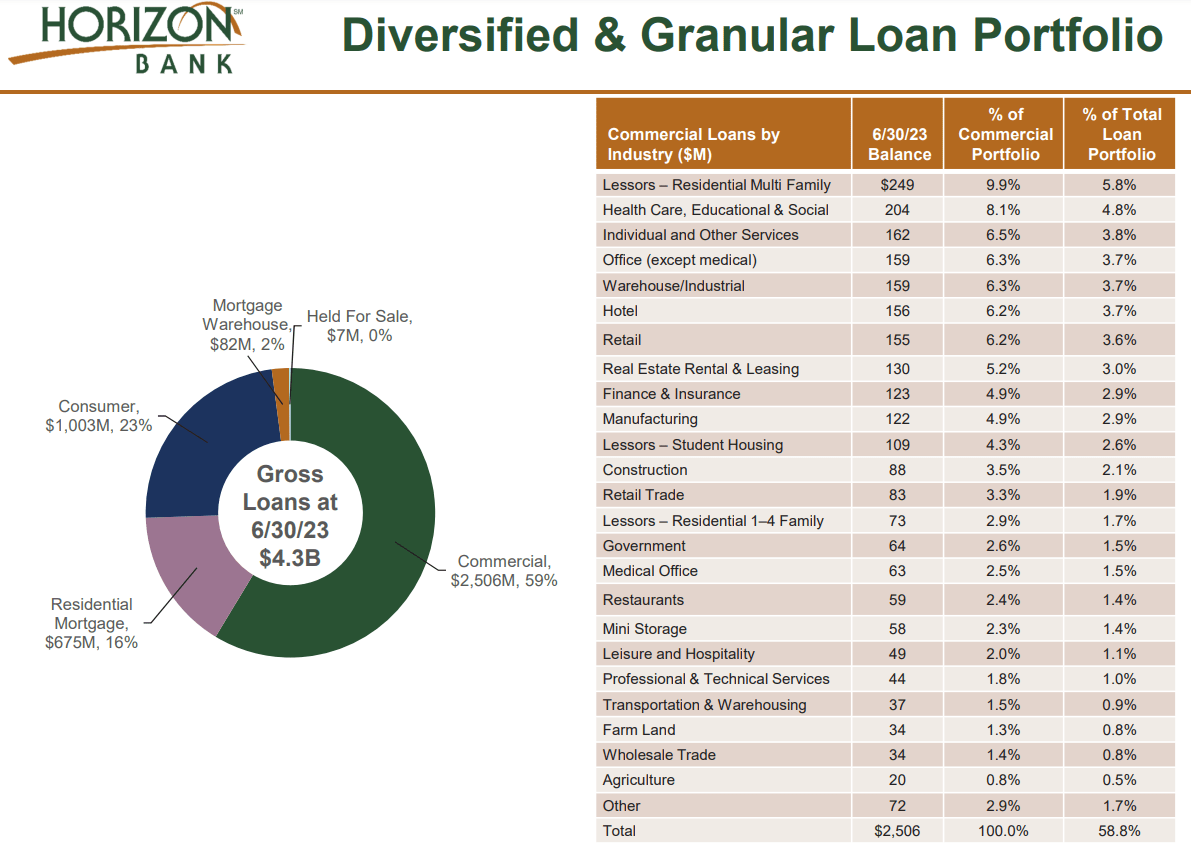

The main problem regarding the loan portfolio is the strong exposure to commercial loans, about 59% of the loan portfolio. Certainly they are not all directed to one market, there is a good diversification, but all are dependent on the performance of the business cycle. After months of recession concerns, the Fed has changed its opinion, which might reassure Horizon Bancorp's shareholders, but on the other hand the main leading indicators signal the exact opposite.

{kind=link}

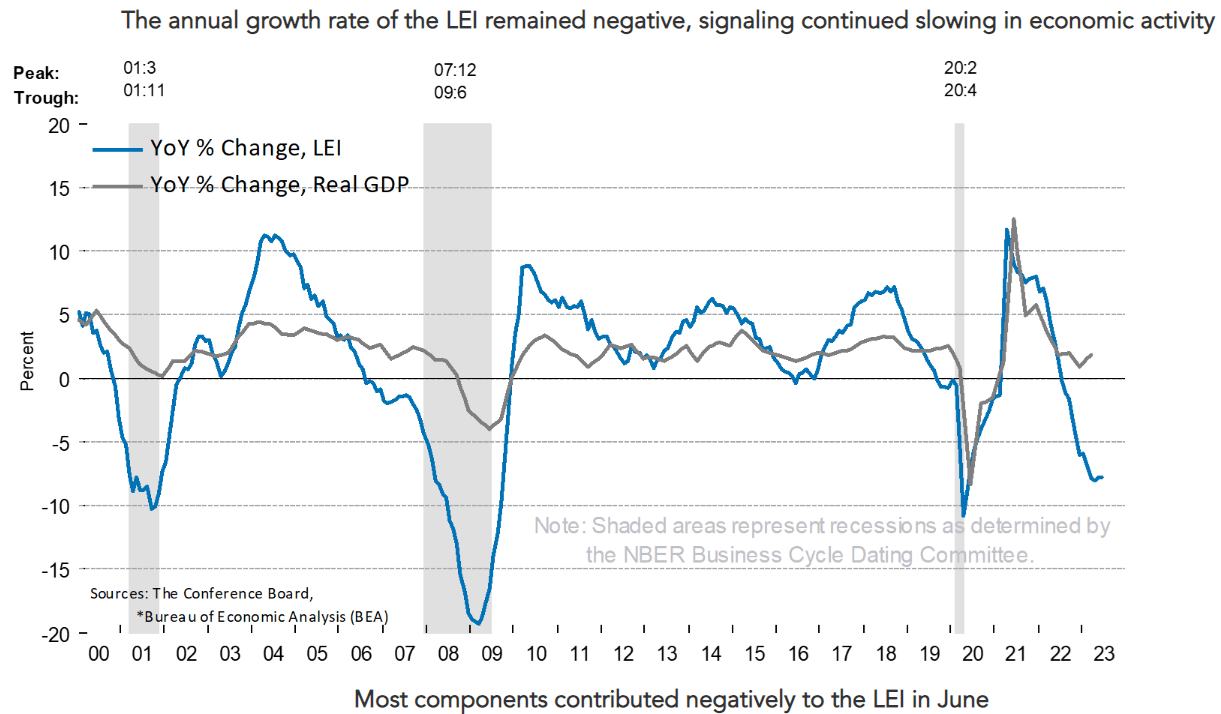

The Leading Economic Index has almost reached a level of -10, which is the threshold touched in the past three recessions. In other words, although the Fed brings positivity to the markets, on the other hand, many doubts remain about the future performance of the U.S. economy. In the event of a recession, all banks will be hit hard, but those with heavy exposure to commercial lending may get the worst of it. A business is more likely to be insolvent than a family that has taken out a mortgage on the house in which they live.

{kind=link}

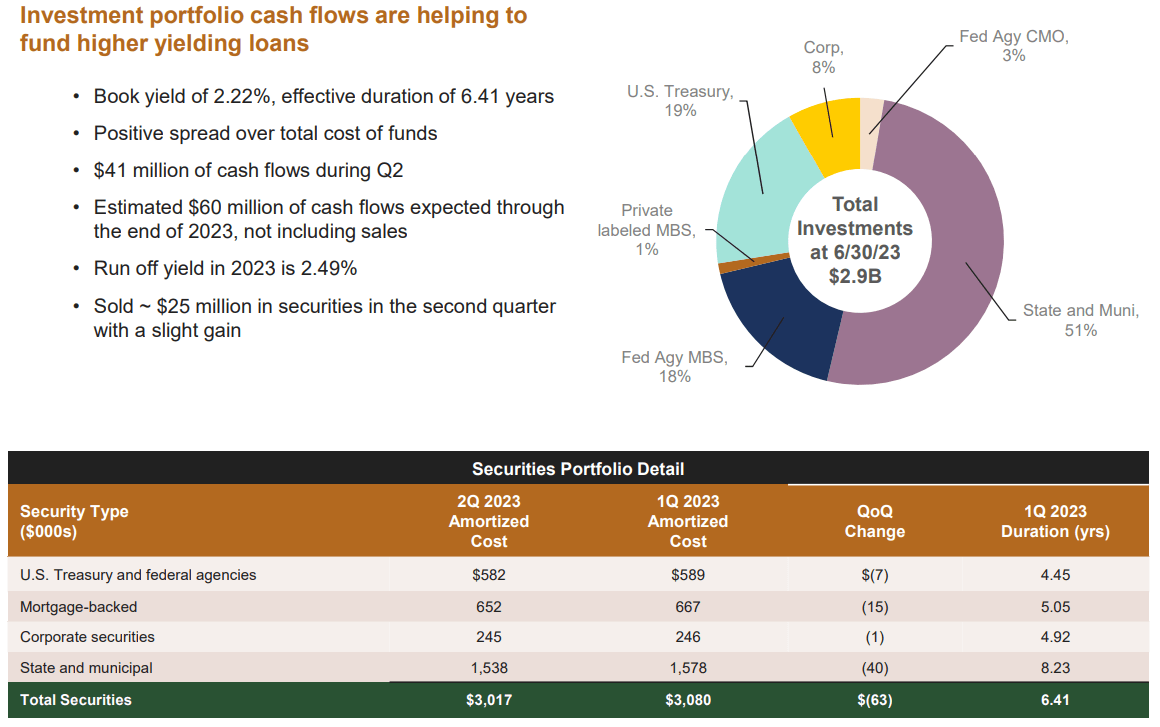

Regarding the loan portfolio, Horizon Bancorp's strategy is similar to that of many of its competitors, which is to put the purchase of securities on the back burner. Cash flows of $60 million are expected by the end of 2023 and will probably be used to provide new loans at current rates.

In addition, securities worth $25 million were sold at a slight profit this quarter. During the conference call, CFO Mark Secor hinted that the company's intention is to sell more securities to have more capital on hand, but the current yield curve is holding back this decision. Unrealized losses on AFS securities are still too high - about 14% of equity - and they want to avoid materializing them: better to wait for the right time to do so. Should interest rates decline, these unrealized losses would decrease, and at that point I expect that the securities portfolio will be lightened.

Finally, I would like to briefly discuss the buyback.

{kind=link}

In Q2 2023, the CFO did not appear opposed to the buyback scenario, but wanted to point out that it is a matter of secondary importance. In recent quarters the priority has been to grow the TCE ratio, and that has not been easy since unrealized losses were piling up: the buyback would have increased the downward pressure on equity even more. Now there seems to be good financial stability again, but a clearer picture of future interest rate trends will be sought before purchasing treasury stock. In any case, the current dividend yield of 5.13% is in my opinion high enough to compensate for the absence of the buybacks.

Conclusion

After a significantly negative first half of 2023, Horizon Bancorp has regained some stability with rising equity and a still relatively low cost of deposits. The second half of 2023 is likely to see more loan growth, financed by cash flows obtained from the investment portfolio. As for the latter, efforts will be made to lighten it by taking full advantage of yield curve movements.

The current Price/Book Value of 0.77x is definitely lower than the historical average of the last 10 years of 1.24x, which could be a sign of undervaluation. In any case, I prefer to rate this bank as a hold, since I remain doubtful about its high exposure to commercial loans as well as the rather low net interest margin: only 2.68% versus 3.26% for its competitors.

For further details see:

Horizon Bancorp: More Stability Than The Previous Quarter