HRL - Hormel: A Mini Spam Bubble Becomes Less Expensive

Summary

- We had a dour outlook for Hormel two years back.

- Extreme valuation alongside expected headwinds led to a forecasting of negative 20 to negative 50% total returns over 10 years.

- We update our thesis.

We generally don't have many Strong Sell ratings in the consumer staples space. But the bubble of 2020-2021 produced extreme valuations on multiple fronts, including in the staples sector. Our notable call there included Clorox ( CLX ) where we did not expect investors to break even within a decade (or even two). Hormel Corporation ( HRL ) was the other one. When we first wrote about it about two years back, we had the following conclusion,

At the end of the day, it is a valuation call, but we have a very high degree of certainty here because Hormel is in the 99th percentile across every valuation. Sure, you can compare Hormel to a 10-year Treasury note or even Bitcoin and say "Hormel is better". But that is the fastest way to the poor house. We expect negative 10-year returns and even a 50% drop from here would hardly be unexpected to us.

Source: Hormel, A Mini Spam Bubble

Unlike the Clorox call, Hormel was a mixed bag. Total return was negative 1.19% over two years (yea!) and Hormel underperformed the Consumer Staples ( XLP ) sector by over 21%.

But we expected worse, much worse. So while the call worked, we look at where things did not pan out as expected.

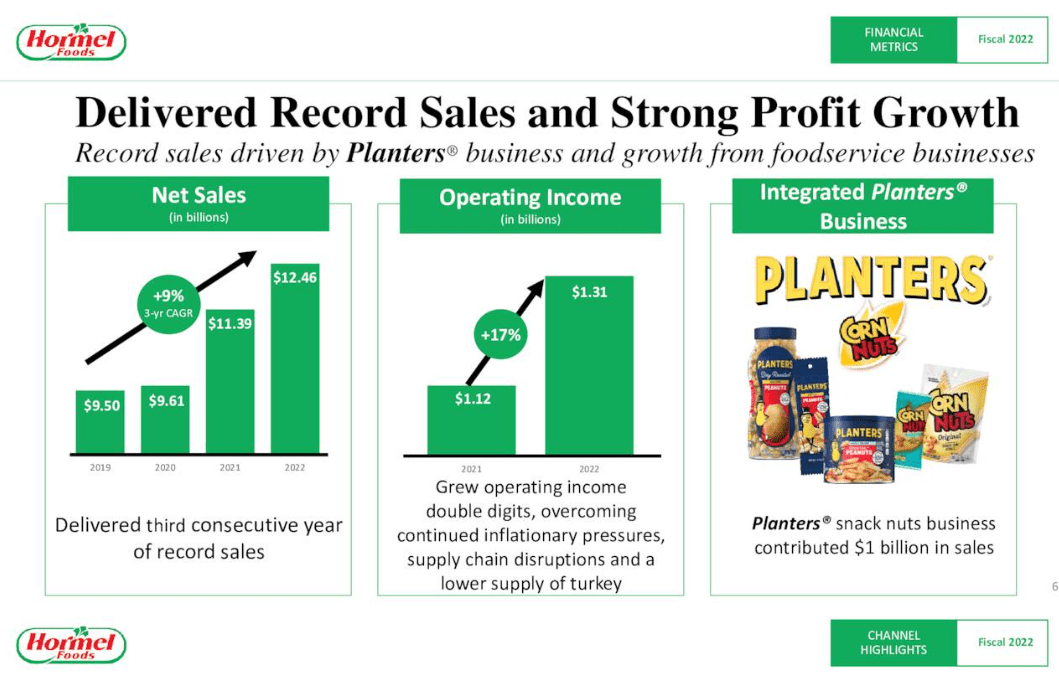

Fiscal 2022

Hormel's fiscal year ends in October. For the fiscal year ended October 30 2022, Hormel produced some decent growth numbers. Net sales jumped on the back of the Planters acquisition from The Kraft Heinz Company ( KHC ) and operating income rose higher by 17%.

{kind=link}

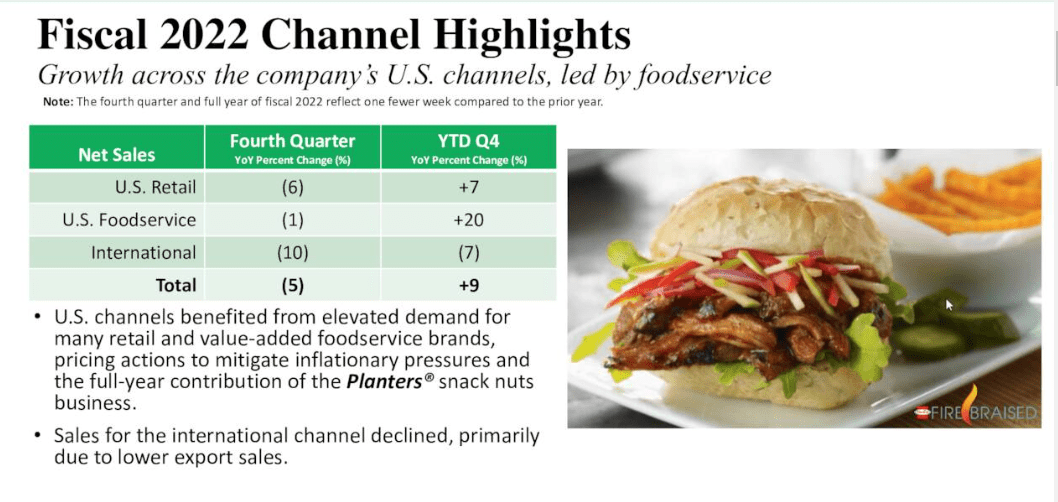

That growth story was for the full year though. Hormel started feeling the stresses of the weaker economy in the fourth quarter. Fourth quarter comparatives were in stark contrast to the whole year. Now, we did have one week less in this comparable period.

{kind=link}

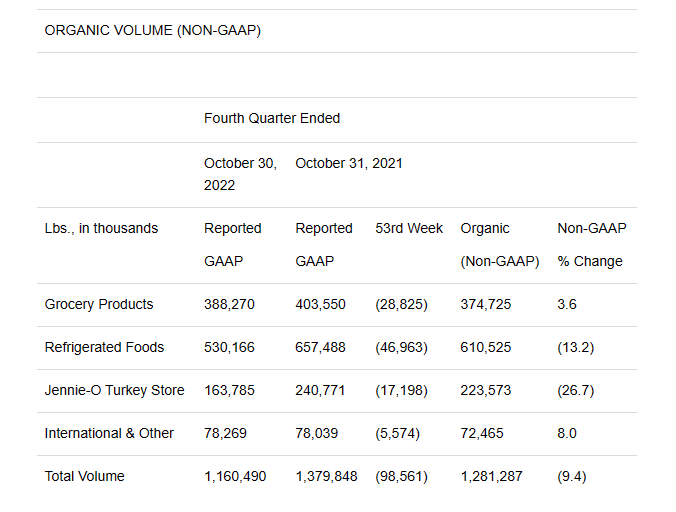

Hormel did show adjusted numbers, where that impact was stripped out. It still wasn't pretty when you examined the sales in pounds (note above stats are in dollars).

{kind=link}

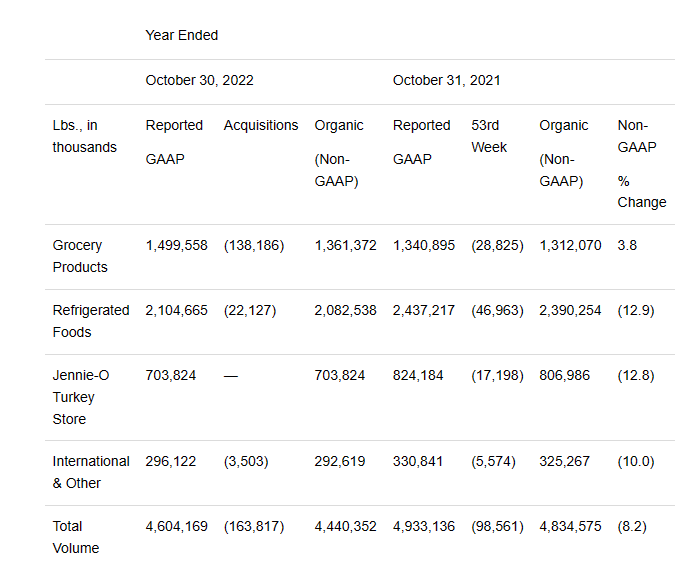

9.4% volume drop is sensationally bad and the stock did dive 7% the day the fourth quarter earnings were released. Even for the entire fiscal year, sales in pounds of product were quite terrible, unless you believe an 8.2% sales drop deserves a victory lap.

{kind=link}

It was the big price increases which held up the revenue numbers. On the plus side, Hormel did do exceptionally well in terms of operating margins.

If you recall our bear thesis, we had predicted significantly higher commodity prices as part of a commodity super cycle. In 2022, independent of that part of the equation, we got a huge uplift in commodity prices from the Ukraine war. In light of those kind of pressures, which far exceeded our base case, Hormel did deliver the goods.

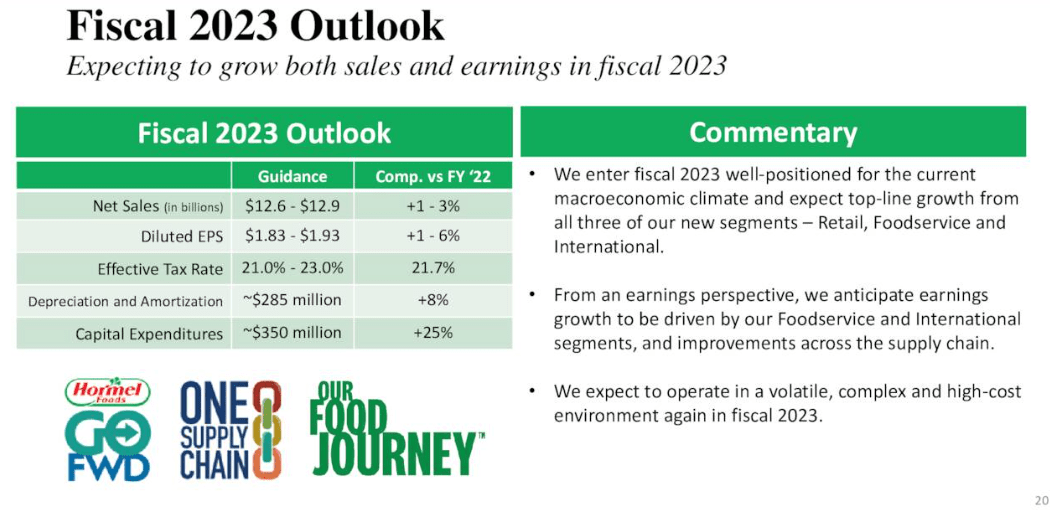

2023

Everything is about guidance ultimately and Hormel's 2023 guidance did disappoint.

{kind=link}

1-3% net sales growth pretty much means that volumes are expected to be down again and price increases will power the revenue change. Analysts have moved towards management guidance, but most were caught offside and had to downgrade revenues and estimates.

{kind=link}

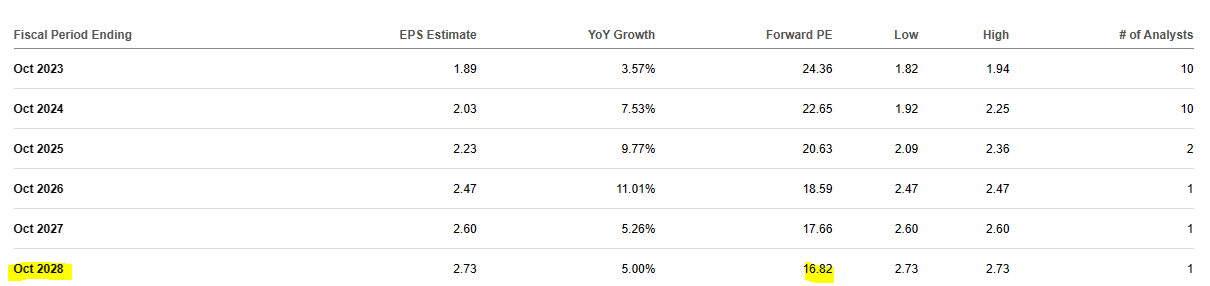

Current numbers look achievable and the idea is that Hormel will deliver an additional 7.5% growth in the following fiscal year.

{kind=link}

Valuation

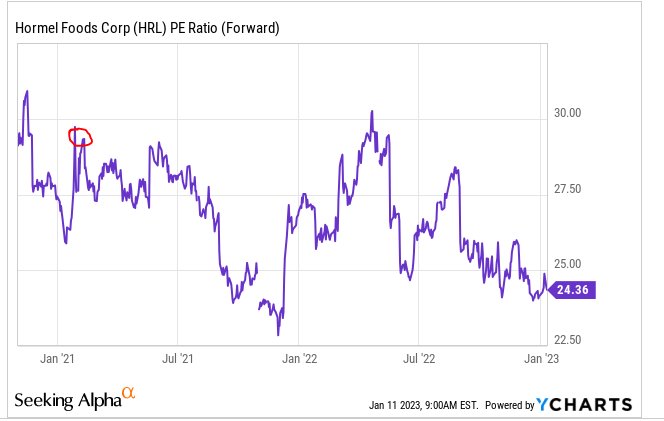

The two years of no returns alongside the Planters acquisition has helped compress valuation a bit. We had made the bear case based on three different numbers and all three have moved in the right direction with earnings growth. The first is the P/E ratio and that has moved down from the February 2021 timeframe (circled) to 24.36X.

{kind=link}

We think we will likely see a 15-18X number on that one ultimately. So if you keep the stock price constant, you are likely to see it after 5 years.

{kind=link}

The second metric was based on price to sales and there we felt the bubble would truly unravel with price to sales reaching 0.8X-1.0X. Lots of work to do on this metric and this is despite the Planters purchase which was done without any equity dilution.

Some might argue that the 0.8X is too low. It probably is from your vantage point. The last few years investors have been mollycoddled into believing in pixie dust and fairy tales. Normalized valuations always return and almost without exception, bubbles end with the company becoming cheaper than usual. Here is exhibit A.

The final metric was EV to EBITDA. Here we had pointed out, again, the insanely high numbers which arguably doomed the stock to poor returns.

We would look for a minimum of 12X on this metric. Since EV to EBITDA includes debt, 4-5 turns on this would be very painful. It would imply a $7.5-8.5 billion drop in equity market capitalization. That would work to about 30-35% lower from here.

Verdict

You can predict the ending valuation and if you are correct, you will generally have no idea when it gets there. Hormel's returns will thus vary, depending on when the correct valuation is reached. If we take a long drawn out move where things just slowly compress over time, you could just see poor returns out over the next 5-7 years. If the market comes to its senses and things compress down to good numbers quickly, we could see a brutal 1-2 years. Obviously the stock is less expensive today than what we saw 2 years back. Thanks to big dividend hikes, the dividend yield is now 2.4%. So this brings us to a good news, bad news situation.

The good news is that our 10 year total return outlook has turned positive. Even in a severe valuation compression you will likely make positive returns including dividends looking out over the next decade. This is different than where things stood two years back.

The bad news is that the total returns relative to the 10 year Treasury rate look even worse than what they did two years back.

Weighing all the factors, we are now upgrading Hormel to just a Sell from a Strong Sell and continue to see downside risks as materially higher than upside potential.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

For further details see:

Hormel: A Mini Spam Bubble Becomes Less Expensive