HRL - Hormel Foods: Q4 Earnings Might Not Look Pretty

2023-11-20 09:00:00 ET

Summary

- Hormel Foods has seen a decline in stock performance, down 28.6% YTD, with concerns about future performance.

- The company has diversified its business beyond meat production through several acquisitions.

- Weakness in the retail segment and increased competition are impacting the company's earnings, and it is still sensitive to meat prices.

- In this article, we take a look at why Hormel Foods should probably post disappointing earnings.

Introduction

Hormel Foods ( HRL ) has long been a favorite for investors seeking low volatility, consistent results and growing dividends. And yet, YtD it is down 28.6% with Seeking Alpha Quant System even warning investors that the stock "has characteristic which have been historically associated with poor future stock performance". It doesn't happen often to find a well-established company with a loyal investor-base with a "sell" as its Quant rating .

The company has recently closed its fiscal year and will soon report its Q4 earnings. What should we expect? And, most importantly, is the stock becoming an opportunity or is its current valuation justified?

The company

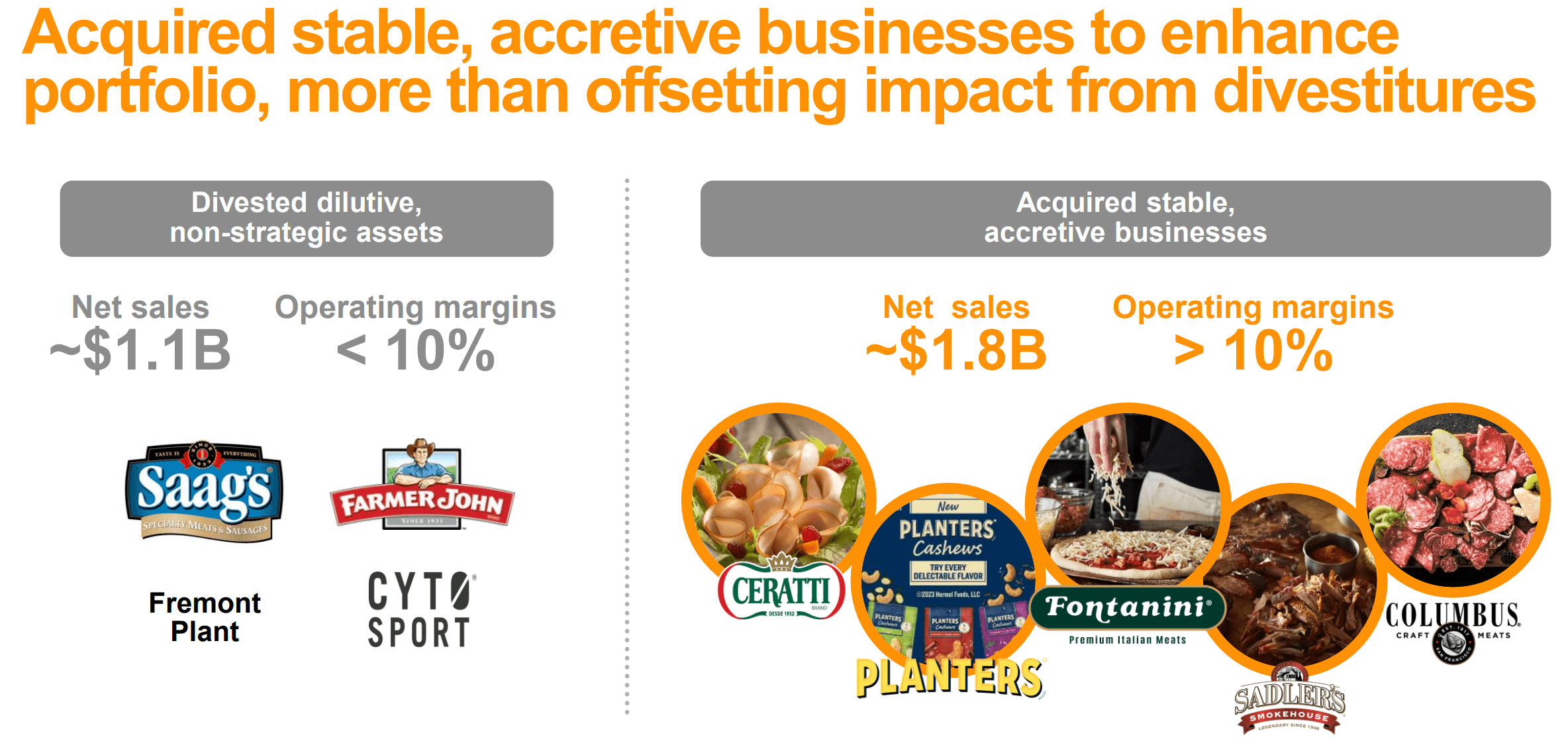

The first thing we need to be aware of is that Hormel Foods is not only a meat producer as it once was. In fact, starting in 2013, the company has evolved beyond its protein-centric business with acquisitions such as Skippy peanut butter and Wholly guacamole. In the past decade, the company has become a true global branded food company, divesting from low margin assets and acquiring higher margin ones.

{kind=link}

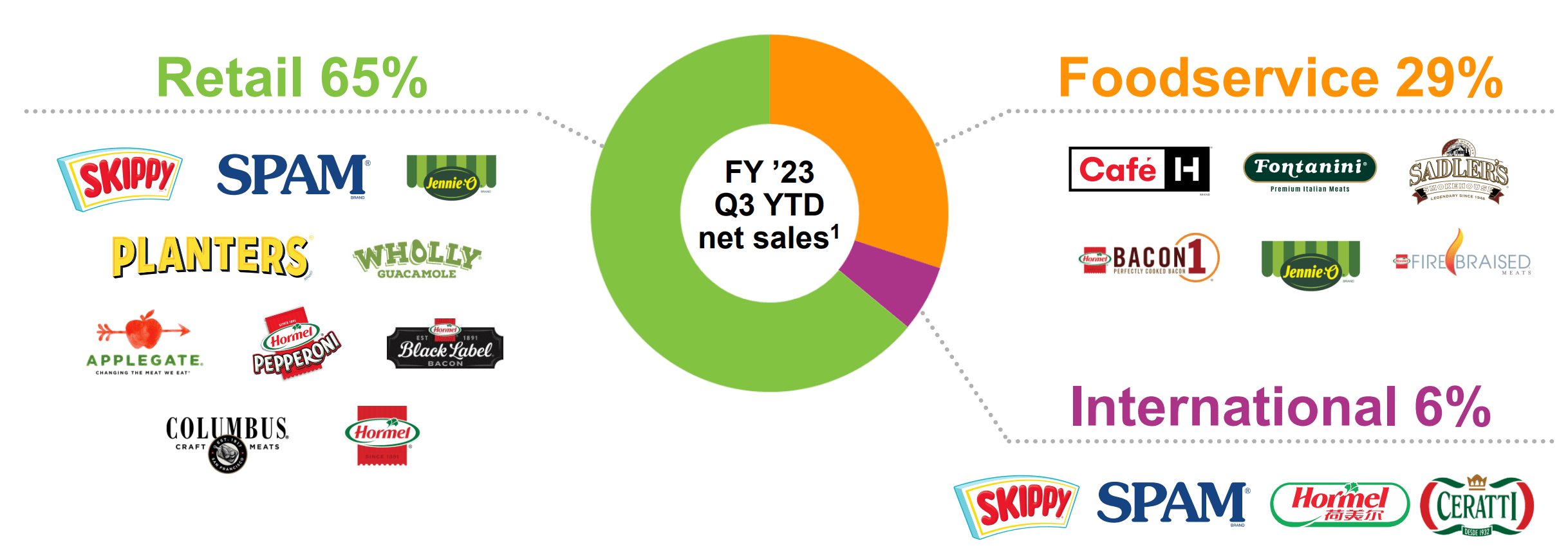

Now, before we move on, we need to understand how Hormel Food's sales are split. This year, the company will report its sales in a new way compared to the past because of its internal re-organization into three main business segments: retail, foodservice and international.

{kind=link}

As we can see, retail is the largest one of the three, with international having only a 6% weight. Yet, it is international the segment where the company expects most of its future growth.

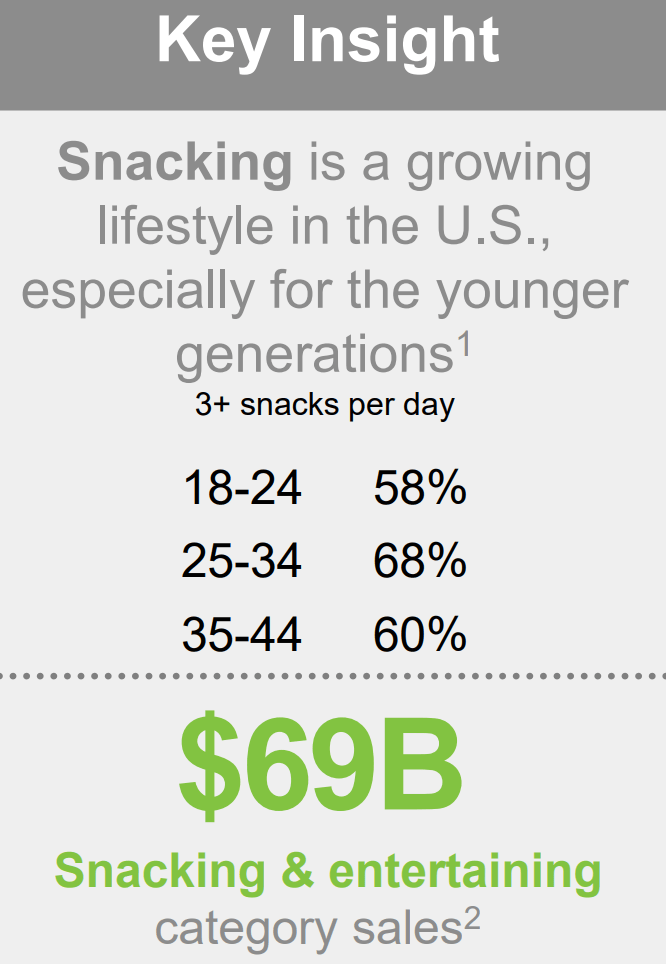

Let's go back to acquisitions. Among these, Planters is the most important one. This is why, last year, during the 2022 Barclays Global Consumer Staples Conference, Hormel Foods pointed out once again how the $3.4 billion Planters acquisition from Kraft Heinz ( KHC ) was the largest acquisition ever made by company. In particular, it helped Hormel Foods become one of the main players in snacking. Why is this so crucial? Because snacking is described by the company as a growing lifestyle in the U.S., especially among younger generations.

{kind=link}

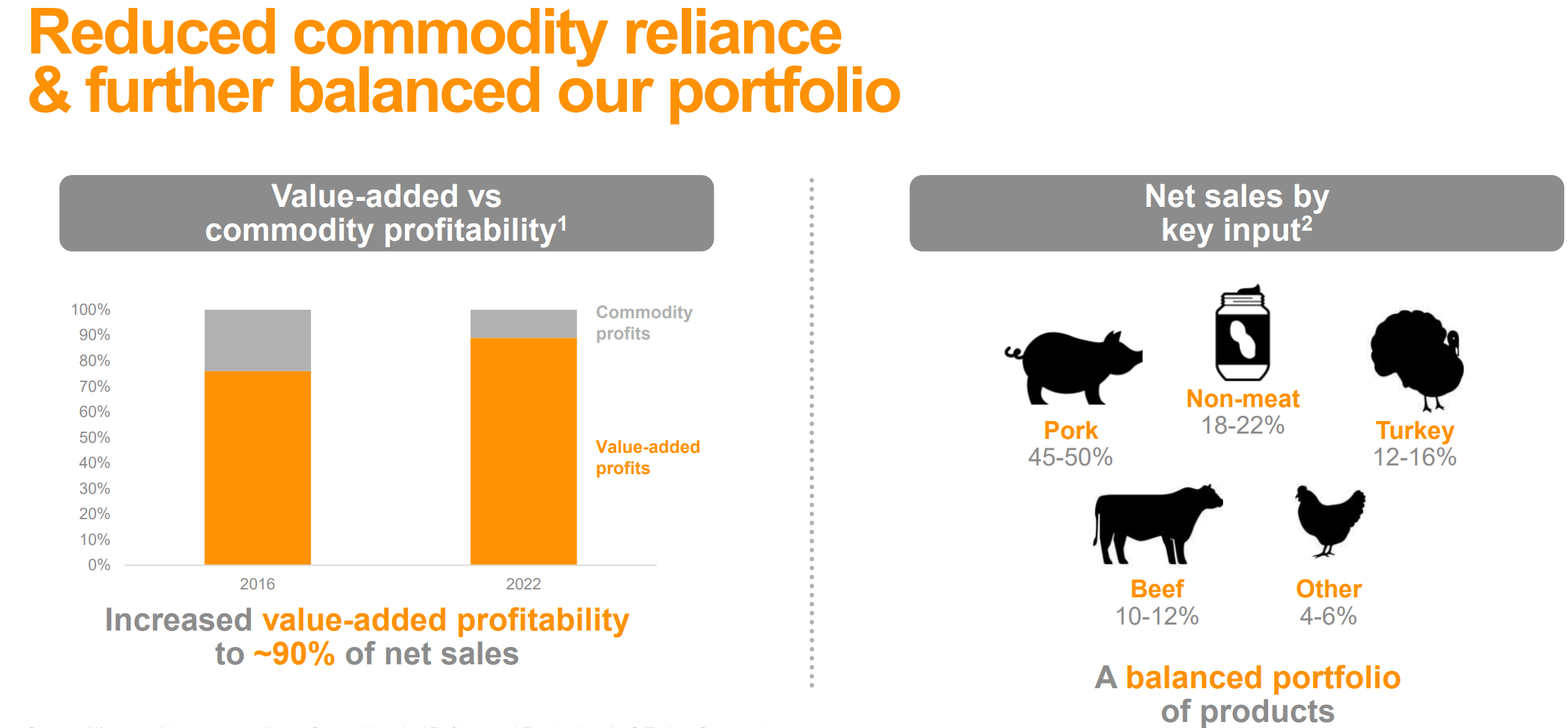

Planters helped Hormel Foods snacking business grow to a meaningful size, up to the point that nor, approximately 25% of Hormel's business comes from nonmeat inputs, complementing its positions in pork, poultry and beef.

However, the expected turnaround hasn't happened yet. Top-line growth is visible, but operating margins have actually been trending downwards since well before the pandemic. This means there is no inflationary environment to blame, but, rather, it is an issue coming from the company's organic operations.

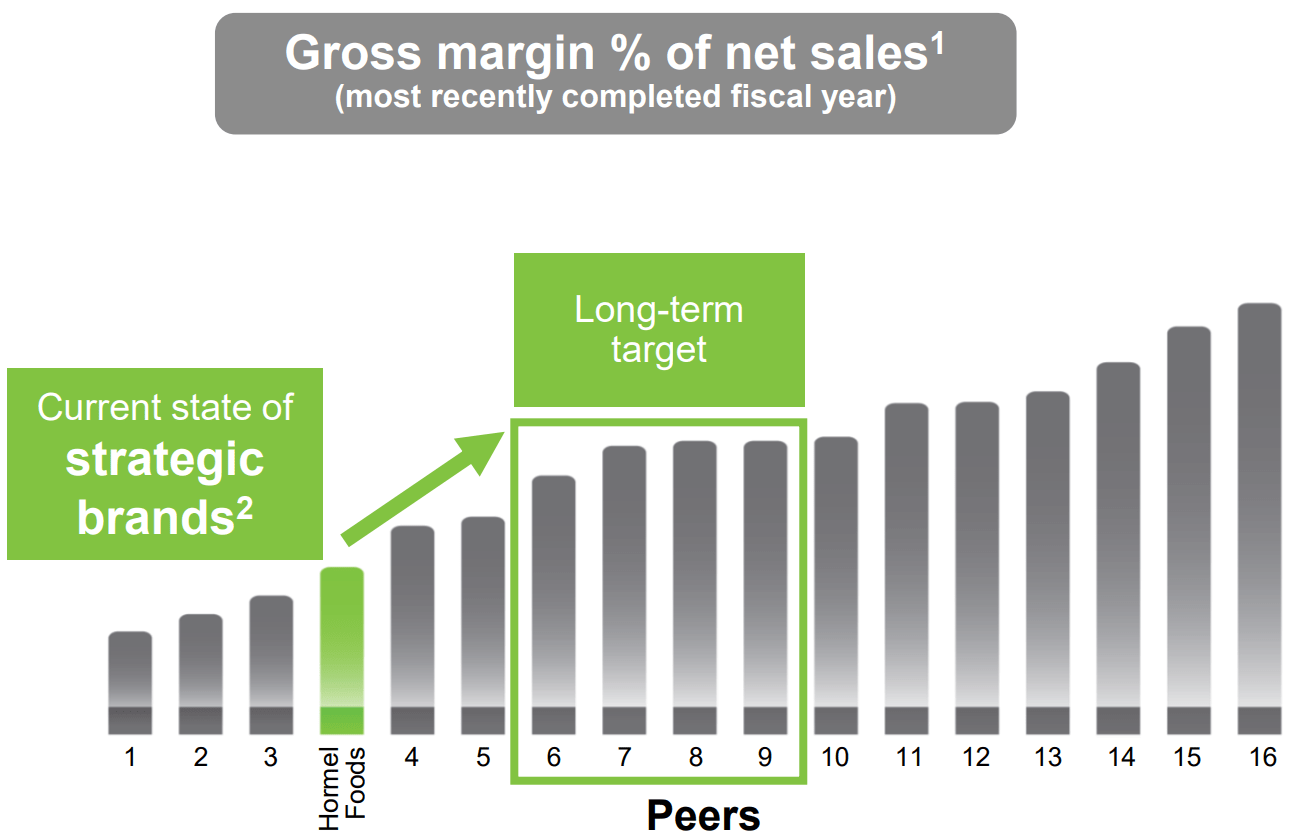

The issue of margins was highlighted in the recent 2023 Investor Day presentation

In the slide below, we can, in fact, see how Hormel Foods is lagging behind most of its peers when we consider gross margins. Even the long-term target of the company is not aiming at placing the company among the industry leaders.

{kind=link}

Hormel Foods has also been quite conservative with its balance sheet. In fact, until the Planters acquisition took place, the company had more cash than debt (in 2019 it carried around $250 million in LT debt and $672 million in cash). Currently, the company reports $670 million in cash against a total debt of $3.3 billion. Now, considering the company's 2022 revenue was $12.1 billion and its EBITDA was $1.4 billion, we have a debt/EBITDA ratio of 2.3 which is below the commonly-used threshold of 3.

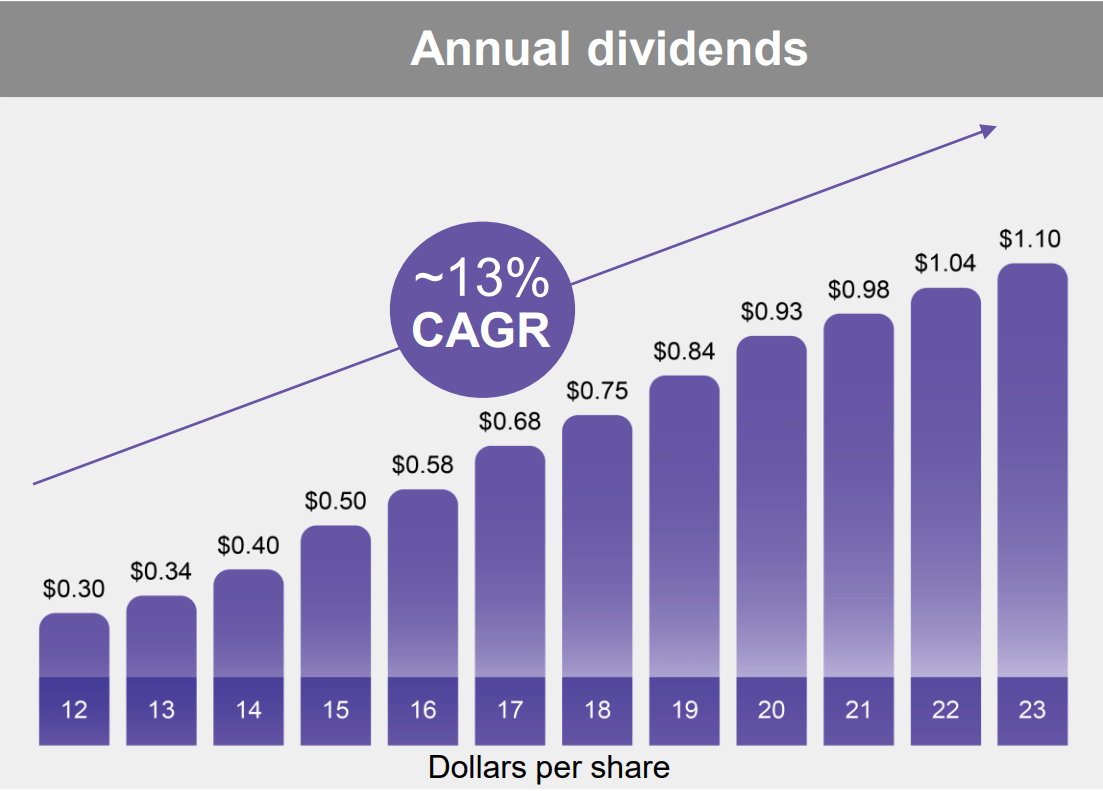

This is why the company has also been able to pay annual dividends constantly growing even during hard times. With over 90 years of consecutive dividends, the company finds a spot in many dividend portfolios.

{kind=link}

Currently the dividend yield is 3.38%, well covered by an annual payout ratio of 63.5%.

Q4 Earnings Preview

While at the beginning of this fiscal year, Hormel Foods was giving a bold guidance, as the year unfolded, Hormel had to moderate its outlook for the fiscal year, writing in its last Q3 report that it was now expecting "modest volume growth, with Q4 sales between $3.1 and $3.6 billion". Now, to give a range of $500 million out of expected sales around $3 billion is something to be noted. It means the company was seeing high uncertainty about its final quarter. In addition, its Q4 guidance was expecting lower EPS due to "continued weakness in the International segment and lower Retail segment results". This is why the company said it was expecting FY 2023 EPS between $1.51 and $1.57 vs. $1.81 reached last year. In other words, it means the company is back to its 2017 levels, while its outstanding share count has slightly increased.

Let's read this straight. We are going to see EPS decrease by roughly 15%. If the company blames weak international sales, things don't match because we have seen above that International makes currently up only 6% of total sales. So, this is a way Hormel Foods tries to swing investors' attention from the real weakness it is seeing: retail.

This can be somewhat confirmed by Jacinth Smiley, CFO of the company, when recently said at the 2023 Barclays Global Consumer Staples Conference that

The areas where we are working on are our International, our International business, that has really been challenged and will continue to be challenged for the rest of the year, much weaker than expected for sure. And then, when we think about our Retail business, that's a little bit more complex, and that's where we're seeing the competition, back to my comment about the industry getting stronger and healthier from a supply chain perspective, that competition on shelf and in market has been more.

This goes along with what Jim Snee, President and CEO, admitted during the last earnings call that

we expect continued softness in our International segment and earnings pressure from heightened competition at retail. We are assuming increased promotional activity this fall in the retail channel as consumer demand moderates to more historical levels and as industry-wide supply chains continue to improve. We also expect an impact from resumed student loan payments, which could pressure overall consumer spending in the U.S.

So, what is going wrong? Commodities. Now, before I explain this, we need to take a step back and be aware that Hormel Foods has repeatedly shown how it is shifting its net sales mix towards value-added profits compared to commodity profits. As we can see, however, its portfolio is still heavily exposed to pork and, to a lesser extent, turkey and beef.

{kind=link}

Now, Hormel Foods has seen pork costs going down. But what has actually been dramatic for the company has been turkey. As Mr. Snee explained:

[...] To start the fourth quarter, pork costs have begun to moderate seasonally. And we expect lower pork input costs compared to the prior year. We began to see a volume recovery in turkey during the third quarter, and we expect to see higher year-over-year turkey volumes in the fourth quarter. To further support our recovery, we have invested in incremental advertising to drive consumer awareness and engagement in the retail channel.

In other words, the turkey meat market has moved lower throughout this year as a result of an unexpected increase of supply, which clearly pressured prices downwards.

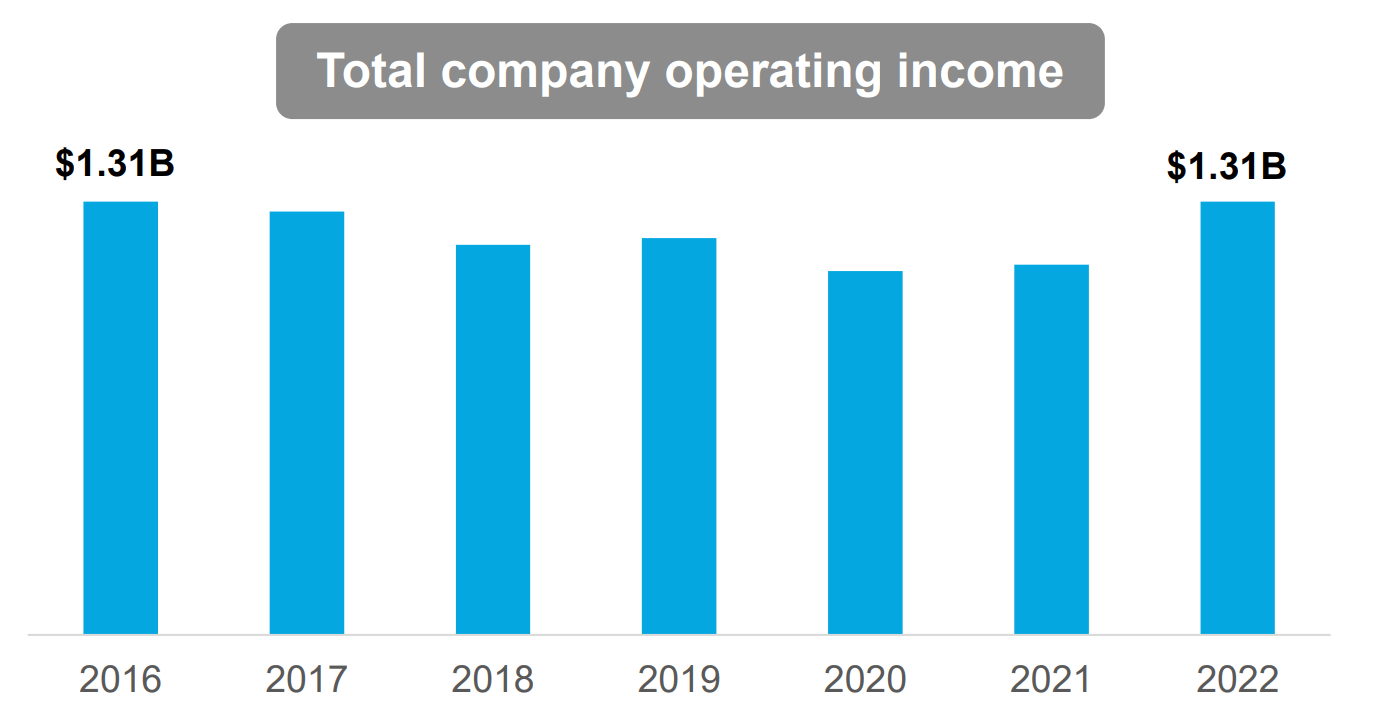

What does this show us? As hard as the company is trying to diversify its revenue stream, it is still sensitive to meat prices and must be looked at as such. This is why, even though the company has finally managed to grow its top-line in 2021 and 2022 (which, it must be said, have been two exceptional years to boost revenues thanks to inflation), it has not been able to increase its operating efficiency as well. As we can see below, at the end of FY 2022, the company was generating the same operating income it had back in 2016. Considering inflation, the company has actually generated less OI than in 2016.

{kind=link}

Now, considering everything we have seen, we can make some rough calculations about what we could expect from the upcoming earnings report.

Earnings and Valuation

I am assuming Hormel will deliver revenues in the lower bound of the range given by the company at $3.16 billion (-4% YoY).

Considering pork costs are easing, I am not expecting very high inflationary pressure on every source of revenues. This is why I am considering a cost of revenues around 82% of revenues (down from the 82.7% seen a year ago). This could lead to $568.8 million in gross profit, which would actually be very good, compared to the last quarterly results. However, SG&A expenses have been increasing and they could be over $300 million in this quarter. This leads us to forecast an operating income of $268.8 million, which is an operating margin of 8.5%. Interest expense has been rather flat just a bit above $18 million per quarter, and it is partially offset by investment income of $9-10 million. The effective tax rate should be around 22% so it could be around $59 million. This gives us a net income of $200 million (268.8-9-59=200.8). If we divided it by the 546.4 million shares outstanding, we have quarter EPS at $0.37, which is well below the $0.51 posted in Q4 of the prior year. Current consensus sees EPS at $0.45, but I believe it is a bit high.

Overall, we know Hormel Foods has already reported for the first 9 months of its fiscal year EPS of $1.09. Adding my forecast, we could end up with yearly EPS of $1.46, down almost 20% from $1.82 of last year.

No wonder the stock has traded down almost 30% YTD. In this case, I don't think much of the blame has to go weight loss drugs as it is true for other peers. As I have tried to show, Hormel still has work to do to get its operating efficiency to higher standards.

Investors have been used to price the stock at a 20+ PE multiple and, as a consequence of low EPS, the stock has traded down to stay around that multiple.

If FY EPS come in at $1.46, the stock would be trading at a 22.3. This could make investors sell out of their positions because the stock would seem expensive. To be aligned with a 20 multiple, the stock should trade at $29.20, which is a 10% discount compared to the current price ($32.50).

Conclusion

I believe Hormel Foods is not an attractive deal right now. Even dividend investors should know by now that Treasuries yield more than the 3.4% Hormel Foods currently sports. The company has been trying to turnaround its operations and become a better and more profitable one. However, I am still not seeing those improvements I would need to make me re-rate the company at a higher premium than the one it is currently awarded with. For now, the company keeps on being a hold. Investors may want to stick with their shares, if they have already gone long at a reasonable price. But for sure I don't see this the right moment to jump in this stock both because of its business and because of its price.

For further details see:

Hormel Foods: Q4 Earnings Might Not Look Pretty