MAR - Host Hotels & Resorts: Stable Company With A Positive Future Outlook

2023-08-17 04:42:35 ET

Summary

- Host Hotels & Resorts is a hotel REIT focused on upper upscale rooms.

- The company has shown a strong recovery since the pandemic and the guidance suggests HST will perform well going forward.

- I present my bullish analysis of the stock.

Host Hotels & Resorts ( HST ) is a hotel REIT focusing on upper upscale rooms and it is the biggest publicly traded lodging REIT. Just like any other hotel REIT, HST experienced a lot of problems during the pandemic that seriously affected their performance. However, the company has been recovering well since then and has shown great growth which we will go over in the following paragraphs.

Overview

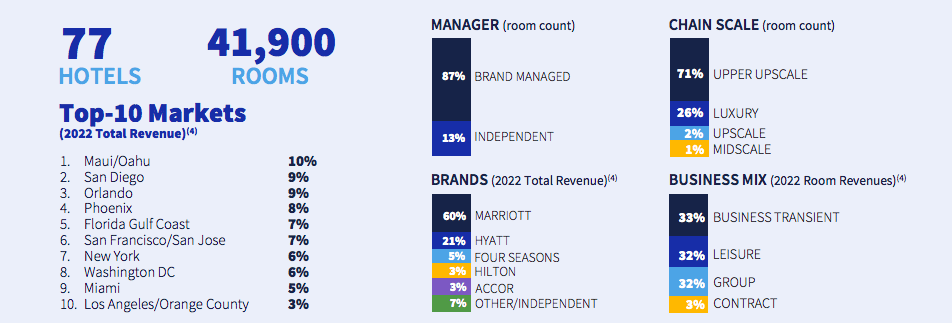

HST owns 77 hotels totalling in 41,900 rooms. The majority of them are located in the US but they have a few outside the states as well (Canada, Brazil). 71% of the rooms are upper upscale and 26% are luxury. This helped the REIT during the pandemic since the affluent target market did not incur many financial losses. Moreover, the REIT rebounded faster because it was more insulated. As you can see in the picture below, the majority of their hotels are managed by Marriott ( MAR ) and Hyatt ( H ) with Marriott providing 60% of their 2022 revenue and Hyatt 21%. Their top markets are Oahu, San Diego, Orlando, and Phoenix. The hotel locations are very well distributed so no single market has too much exposure.

{kind=link}

The FFO per share for Q2 2023 stands at $0.53. The occupancy is 74.2% which is a 7.7% decrease compared to pre-pandemic levels in 2019, however, it is still higher than the average expected occupancy of 63.8% for hotels this year. This suggests that HST is performing well on this end but is still able to perform better.

The same store results show some improvement as well. Their hotel revenues increased by 3.9% and hotel RevPAR (revenue per available room) by 2.7% since last year. On the flip side, net income has decreased by 17.7%, EBITDAre by 11.9%, and FFO per share by 8.6%.

That does not sound that great but the good news is that guidance for the rest of the year suggests better results. Hotel total RevPAR is said to increase by 8.1% at midpoint and hotel EBITDA by 1.5%. FFO is expected to be $1.85 at midpoint, just a bit below $1.9 for the last year.

HST has been both buying and selling properties. Between 2021 and 2023 the company had dispositions of $1.5B (17.5x sales price/EBITDA) and made acquisitions for $1.9B (13.1x sales price/EBITDA). So their portfolio grew a little bit and they sold properties for higher prices compared to the ones they bought.

Balance sheet

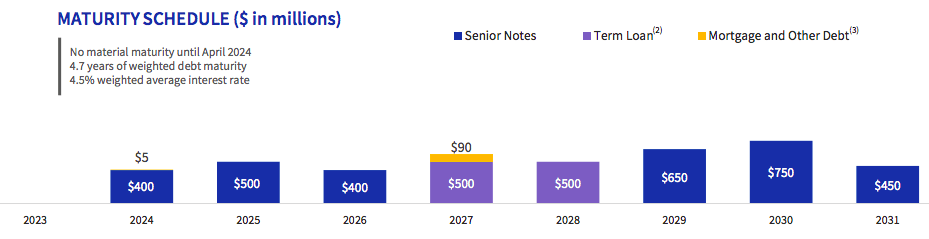

Their balance sheet is pretty solid. They are BBB- rated with $4.2B of outstanding debt. The weighted average maturity is 4.7 years and the weighted average interest rate is 4.5% which is on the higher side but HST has no significant maturities until April 2024 and well distributed maturities in the next years (see below). With $2.5B in liquidity (of which $1.5B is credit line availability) they should have no problems paying off their debt in the coming years.

{kind=link}

Dividend

The dividend is $0.15 per share per quarter which is a 25% increase since last quarter and translates to a 3.7% yield. On the highest levels (pre pandemic) the dividend reached $0.85 per share per year and then was wiped completely in 2021 because of poor performance during the pandemic which was a good move for the company. While the yield is not the highest right now, I have a positive outlook on the future of the dividend. The increase in the last quarter and good performance metrics suggest it could increase again. Furthermore, the payout ratio is only 57% compared to EPS now so there is definitely room for growth.

Valuation

The P/FFO currently stands at 8.83x with a historical average of 14.35x. For comparison, peers trade at the following multiples - Summit Hotel Properties ( INN ) at 6.27x, Apple Hospitality REIT ( APLE ) at 9.46x, Park Hotels & Resorts ( PK ) at 7.32x, RLJ Lodging Trust ( RLJ ) at 6.43x. So HST is on the higher end of P/FFO multiples compared to peers, however, I still don't see it as overpriced. The company has recovered after the pandemic and has been performing well even with slight downturns in the FFO and EBITDAre. But the outlook is good and they have a stable balance sheet. The dividend is lower but it is safe and with room for increase. The stock probably won't make you rich but it is a pretty safe and stable option and could still offer reasonable growth which is why I rate it as a BUY here.

Risks

The risks associated with the company are the following.

FFO remaining flat in the coming years which would mean the company's growth will be slow or negligible.

Since there were several hiccups in the Q2 results, as I mentioned above, it is possible that the guidance for the rest of 2023 will not be fully fulfilled. However, the company is pretty well positioned in terms of their portfolio and they won't have to pay of any maturities for right now which would help them to better handle the situation. Additionally, they were able to recover after the pandemic which shows that the management is able to operate during harder times.

For further details see:

Host Hotels & Resorts: Stable Company With A Positive Future Outlook