SJM - Hostess Brands: Not Such A Sweet Deal For The J. M. Smucker Company

2023-09-12 11:44:35 ET

Summary

- The J. M. Smucker Company is to acquire Hostess Brands, Inc. in a $5.6 billion deal, with the cash-heavy nature of the deal causing concern.

- J. M. Smucker aims to focus on the "convenient consumer occasions" category, which aligns with Hostess Brands' snack offerings.

- The acquisition is expected to bring additional revenue, profits, and cash flows, along with potential synergies, but it comes at a high price.

On September 11th, after a day or two of rumors circulating, news broke that The J. M. Smucker Company ( SJM ) had agreed to acquire snack manufacturer Hostess Brands, Inc. ( TWNK ) in what ultimately is a multibillion-dollar transaction. The market reacted in an interesting manner to this news, with shares of Hostess Brands closing up 19.1% while shares of J. M. Smucker dropped roughly 7%. Truth be told, had this transaction been done on an all-stock basis or using an overwhelming majority of stock, I would be bullish about the transaction. But because of the cash-heavy nature of the deal and the fact that this will result in significant interest expense for the acquirer, the picture does not look as appealing as some might initially think.

A look at the transaction

Before the market opened on September 11th, news broke that J. M. Smucker had agreed to acquire Hostess Brands in a deal valued at $5.6 billion. This is the enterprise value of the deal, with net debt accounting for just under $900 million. That leaves about $4.7 billion for shareholders. Based on the closing share price of each company on September 8th, this deal translated to a price per share of $34.25.

However, that is not a fixed price. And that's because, while $30 per share of the purchase is being done in cash, the rest is being done in stock. For each share of Hostess Brands that somebody owns, they will receive, upon closing of the deal, 0.03002 of a share of J. M. Smucker. The only reason why this doesn't sound like much is because, prior to the deal being announced, shares of J. M. Smucker traded at $141.58. Upon closing of the transaction, shareholders of Hostess Brands should own approximately 3.8% of J. M. Smucker.

To some market participants, this transaction may seem a bit odd. And that is because J. M. Smucker is most famously known for its production of jelly and peanut butter products. Although this isn't terribly far removed from the snacks that have made Hostess Brands a household name, a case could be made that there might be other areas of business that J. M. Smucker could focus on that might be more logical. However, it's also important to keep in mind that J. M. Smucker is not a small and simple company. In addition to the aforementioned offerings that it makes available, it has also come to focus, over the years, on a variety of other products such as pet food and snacks, canned milk, coffee, and more. This makes it a diversified food play and, when talking about a company adopting a diversified growth strategy, Hostess Brands makes a lot of sense for a bolt-on acquisition.

{kind=link}

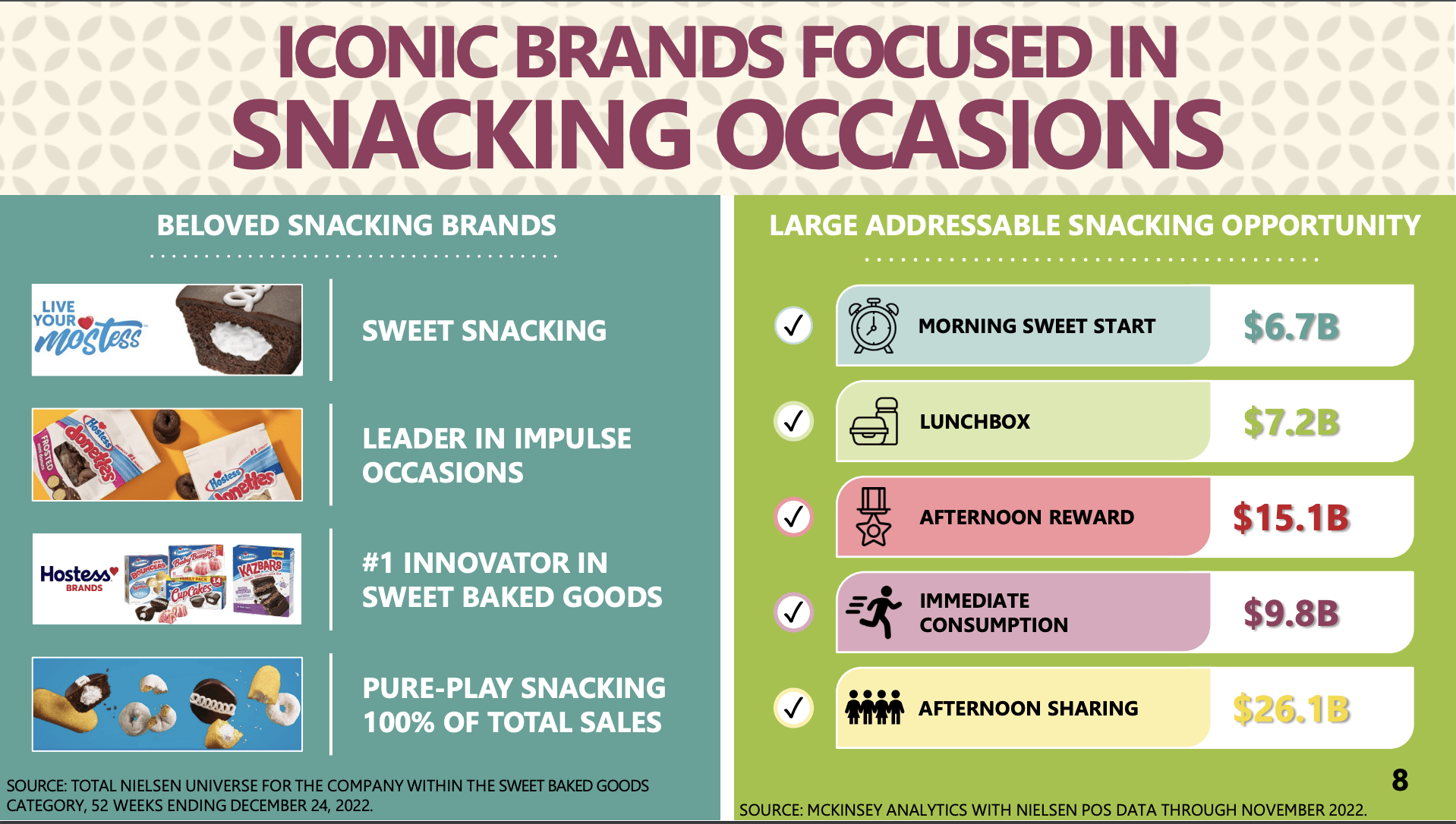

The management team at J. M. Smucker has been clear that their objective from this transaction is largely to intensify its efforts on what it calls the "convenient consumer occasions" category. And if you have been inside a gas station at any point in the past several years, you know that this describes Hostess Brands perfectly. For those not overly familiar, Hostess Brands' offerings include , but are not limited to, Donettes, Twinkies, CupCakes, Ding Dongs, Zingers, Coffee Cakes, Ho Hos, Mini Muffins, Fruit Pies, and more. It also owns the Voortman cookie brand. Management has identified this as a major market opportunity. All combined, this market is estimated to generate about $64.9 billion in revenue each year. The largest chunk of this is the afternoon sharing market that management pegs as being worth $26.1 billion.

Besides the additional revenue, profits, and cash flows, that this transaction is expected to bring, there's also the possibility for significant synergies. The management team at J. M. Smucker estimates that around $100 million worth of annual synergies can be realized during the first two completed years following the completion of the acquisition. From my experience, it might be best to assume that synergies do not come to pass. More likely than not, some will. But I would prefer to be overly conservative and surprised in a positive way than to be liberal and surprised in a negative way.

This acquisition does not come cheap. For the current fiscal year, Hostess Brands expects to generate net income, at the midpoint of guidance, of $149.2 million. Meanwhile, EBITDA should be between $315 million and $325 million, with a midpoint of $320 million. No guidance was given when it came to other profitability metrics. But based on my own estimate, adjusted operating cash flow should come in at around $274.7 million.

It might be tempting to stop here. However, there is another item that we need to take into consideration. The fact of the matter is that the amount of cash that J. M. Smucker will have to dole out should be somewhere around $4.1 billion. And at this time, cash and cash equivalents on its books total $241.1 million. More likely than not, all the purchase price on the cash side will have to come from the issuance of additional debt.

{kind=link}

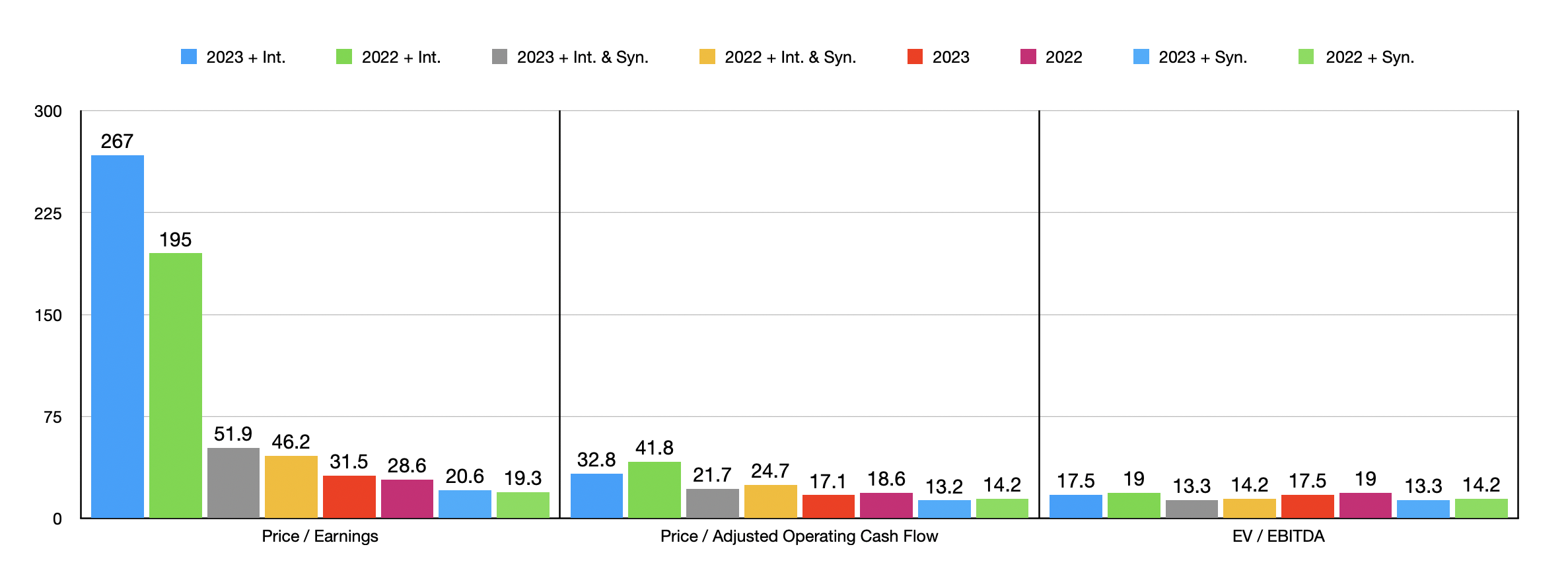

Looking through the existing debts that are on J. M. Smucker's books, the highest interest rate is for some notes for which the company has to pay 4.38% per annum. If we assume that this is what the company will have to pay on this big purchase, then annual interest expense would be $180.3 million. In the table above, you can see what impact this will have on the company's profitability metrics if we were to apply this interest expense to financial performance for the current fiscal year. I am assuming a 27% effective tax rate, which is in alignment with what the management team at Hostess Brands has indicated. The table also shows what financial performance would have looked like last year have this interest expense applied then and assuming the 22.3% effective tax rate the company experienced at that time.

{kind=link}

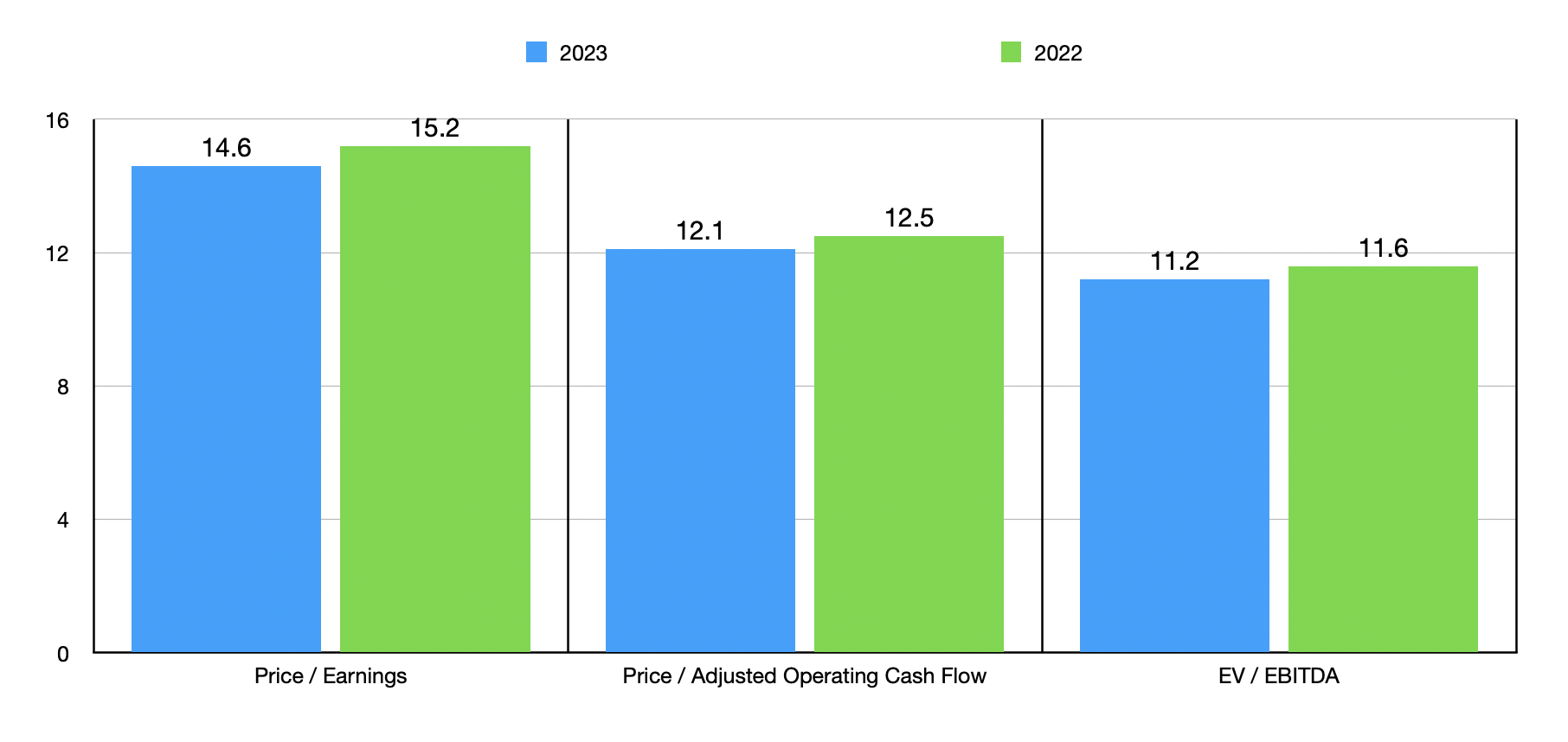

Using the aforementioned data, I would like to point you to the chart above. In it, you can see just how expensive shares of Hostess Brands happen to be. The chart also shows pricing if we did not have to worry about the interest expense. Meanwhile, in the chart below, you can see how shares of J. M. Smucker are priced using forward estimates for this year and using financial performance for last year. Because of the interest expense that has been implied, Hostess Brands looks incredibly expensive.

Some might argue that the stock was still pricey relative to its suitor without the interest expense. But I don't think that premium is unrealistic.

{kind=link}

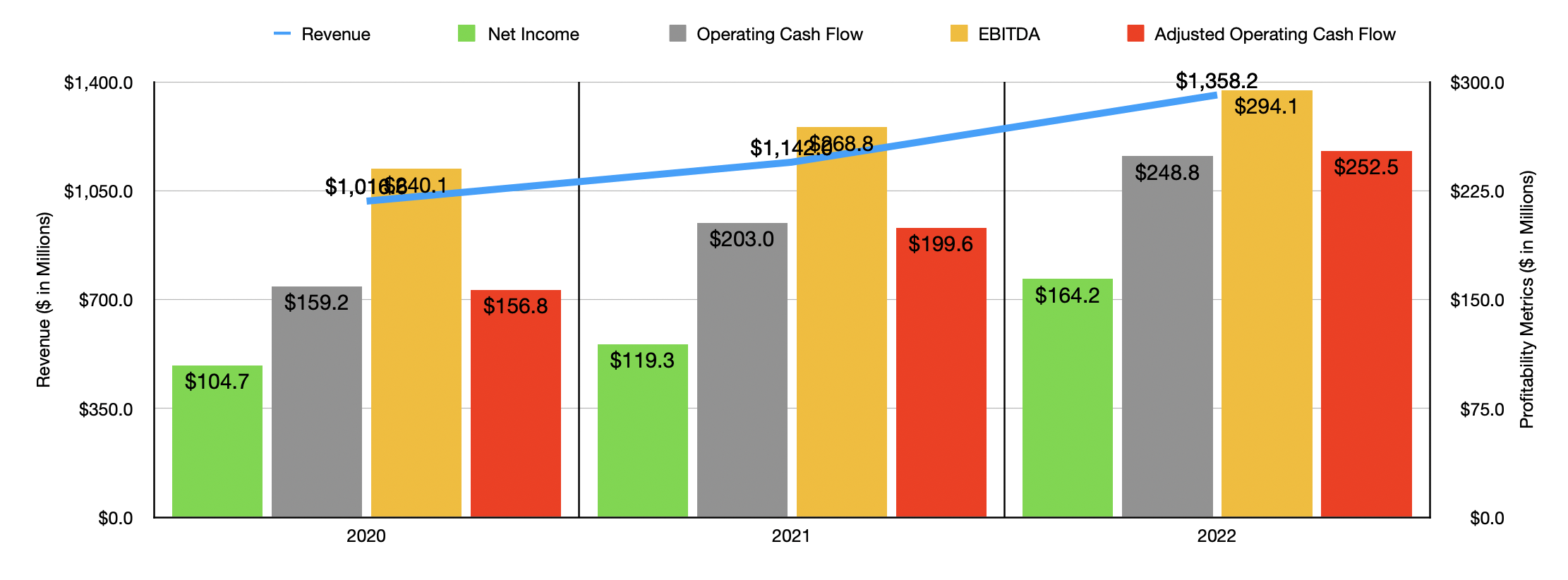

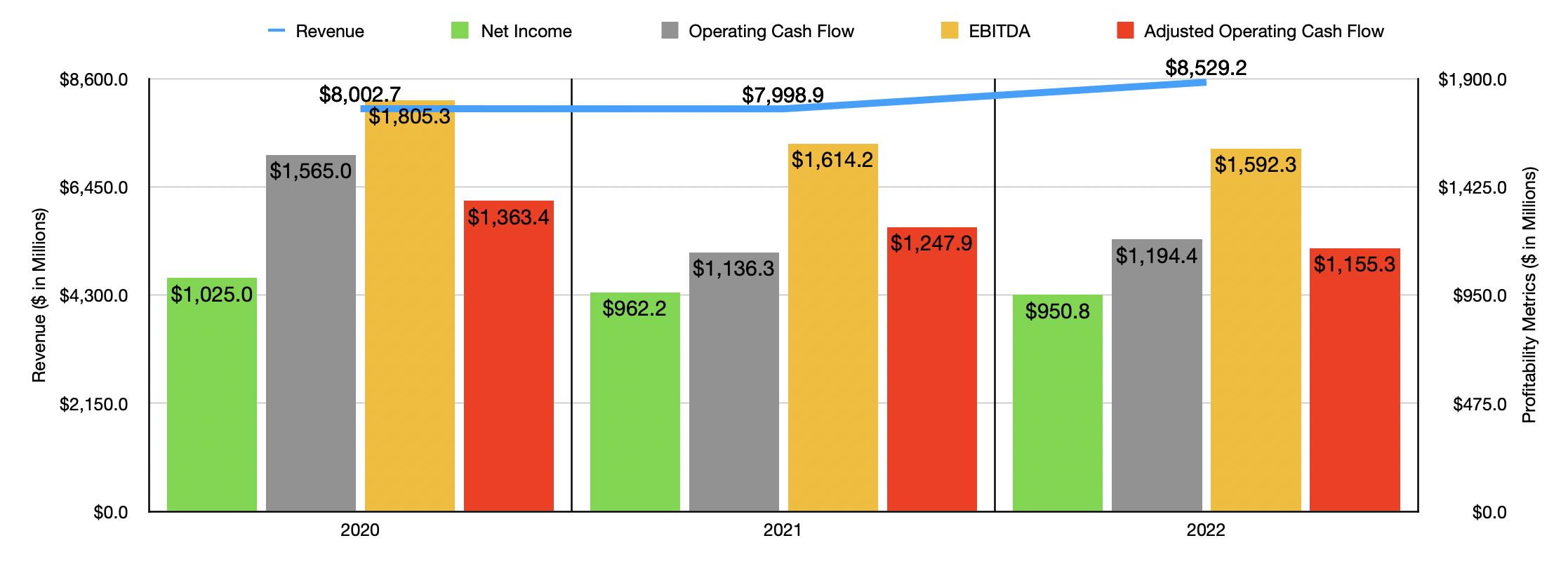

The reason for my thinking on the premium relates to the financial performance of both companies over the past three fiscal years. In the first chart below, you can see how Hostess Brands performed from 2020 through 2022. And in the second chart, you can see the performance of J. M. Smucker. No matter how you stack it, Hostess Brands has a far better track record of growth, both on its top line and on its bottom line. So paying some premium for a relatively high growth prospect is not an issue to me. But when you factor in the implied interest on the purchase, shares become far more expensive than I would be willing to be comfortable with, even if synergies can be achieved as predicted.

It should be noted that J. M. Smucker does have a history of making interesting moves. In April of this year, for instance, the company sold off some of its pet food brands for $1.2 billion. These brought in sales of about $1.5 billion annually, though it was also the only significant asset sale the company has made in years.

{kind=link}

{kind=link}

Takeaway

At the end of the day, we will have to see how things play out between J. M. Smucker and Hostess Brands. As I started analyzing the picture, I was hoping that I could write a piece that was somewhat bullish. But I had to base my conclusion on what the data said. And at this time, I don't see a compelling reason to feel any differently about this than the market seems to.

While Hostess Brands is a solid company, especially compared to the mediocre J. M. Smucker, the price being paid is difficult to swallow, even if synergies are realized. To be clear, I have previously been bullish on Hostess Brands. Back in December of last year, I rated the company a buy. And since then, shares have experienced upside of 43.9% compared to the 16.5% seen by the S&P 500. But because of how shares are tied to J. M. Smucker stock, a company that I believe to be only a mediocre prospect, I've decided to rate both companies a "hold."

For further details see:

Hostess Brands: Not Such A Sweet Deal For The J. M. Smucker Company