QQQ - Hot CPI Print Means Higher Yields And Massive Risks To Stocks

2023-10-12 12:30:11 ET

Summary

- Inflation exceeded expectations, with a 0.4% monthly increase and a 3.7% year-on-year increase.

- Long-term rates are likely to remain high, posing a threat to stocks.

- Market-based inflation targets may be too low, and it may be challenging to achieve a 3.3% year-on-year inflation rate by December.

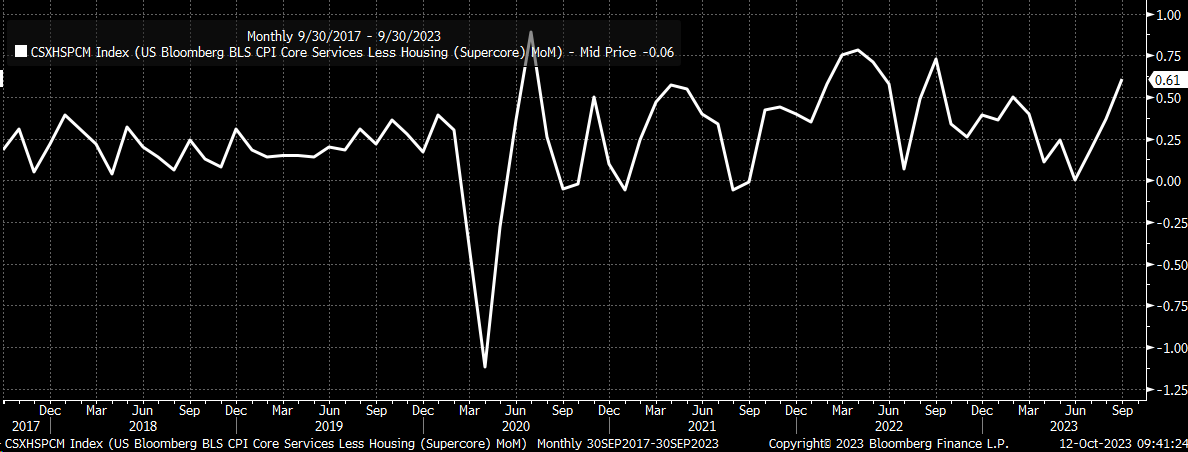

Inflation came in hotter than expected on the Consumer Price Index ("CPI") headline numbers, climbing at 0.4% m/m versus estimates of 0.3% and climbing at 3.7% y/y, hotter than the expected 3.6%. Core CPI came in as expected. Additionally, super core came in hotter in September, rising by 0.6% from 0.4%, which marked the second month in a row of increases.

This will mean that long-term rates are likely to stay high and may very well go much higher, and this poses a significant threat to stocks, given their stubbornness to go down.

{kind=link}

Market-Based Inflation Targets May Be Too Low

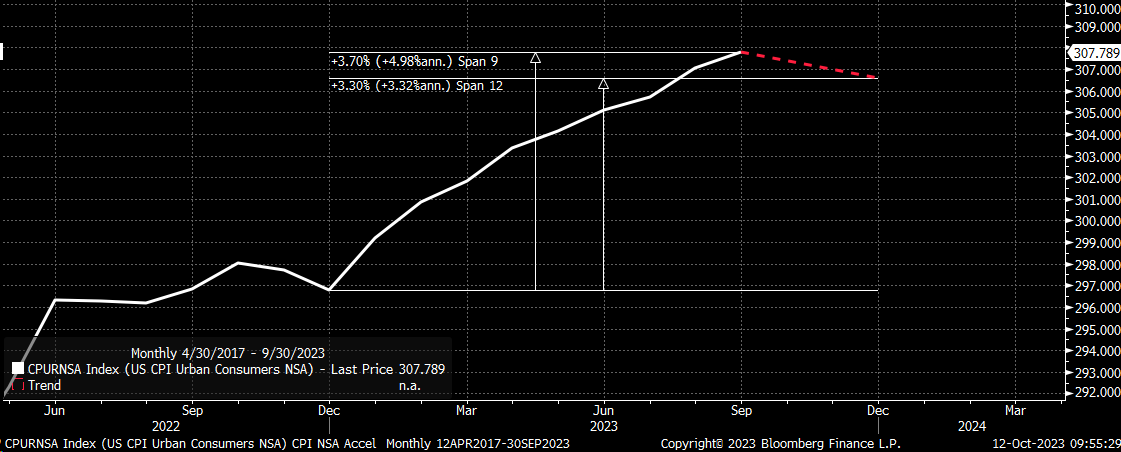

At least over the first nine months of 2023, the headline CPI non-seasonally adjusted annualized rate of change is around 5%, much higher than the current 3.7% y/y rate of change. It also means that for CPI to hit a y/y change of 3.3% by December, which is what the swaps market is currently predicting, non-seasonally adjusted prices will need to fall over the final three months of 2023.

{kind=link}

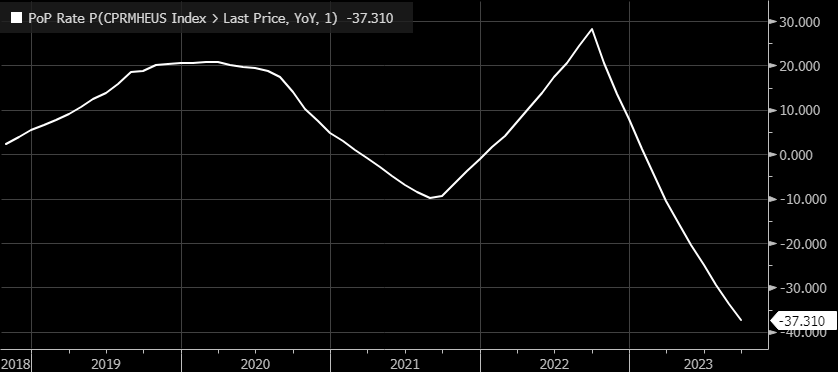

We may see that happen; it just isn't clear how likely it is to happen. What is pretty clear, in my opinion, is that the days of falling health insurance costs are probably behind us. After all, according to the BLS CPI, health insurance has fallen by 37.3% on a y/y basis, which should reset in October.

{kind=link}

Keep in mind that there has been a 3.5% decline m/m in health insurance every month since October of last year, which adds up even though health insurance has a weighting of 0.54% in the non-seasonal adjusted measure, but that is about a 0.2% per month decline, which will be going away.

{kind=link}

So, the disinflationary trend may get harder going forward than many may think, and those market expectations for a 3.3% y/y headline inflation by December may be more challenging to achieve than what the market is currently pricing.

{kind=link}

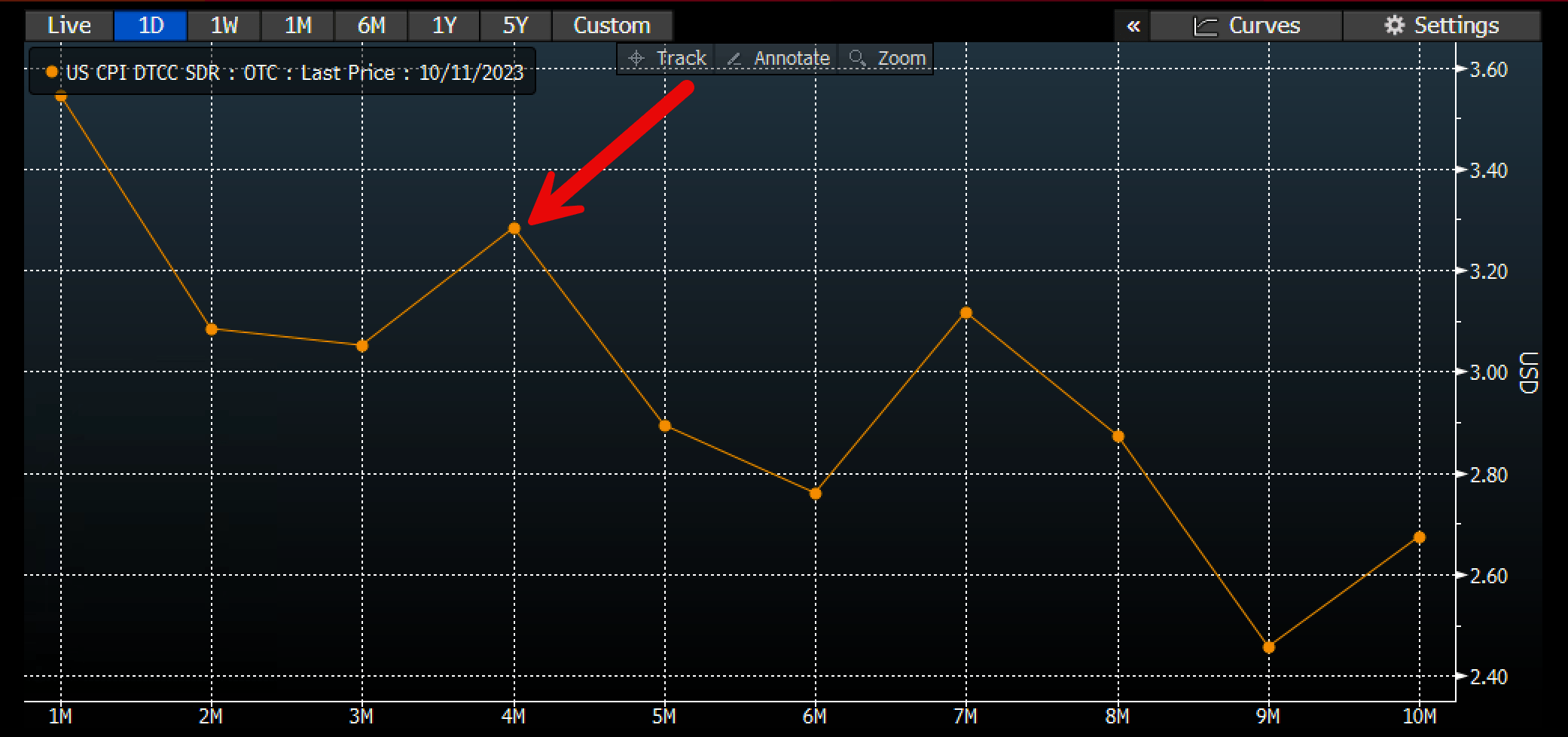

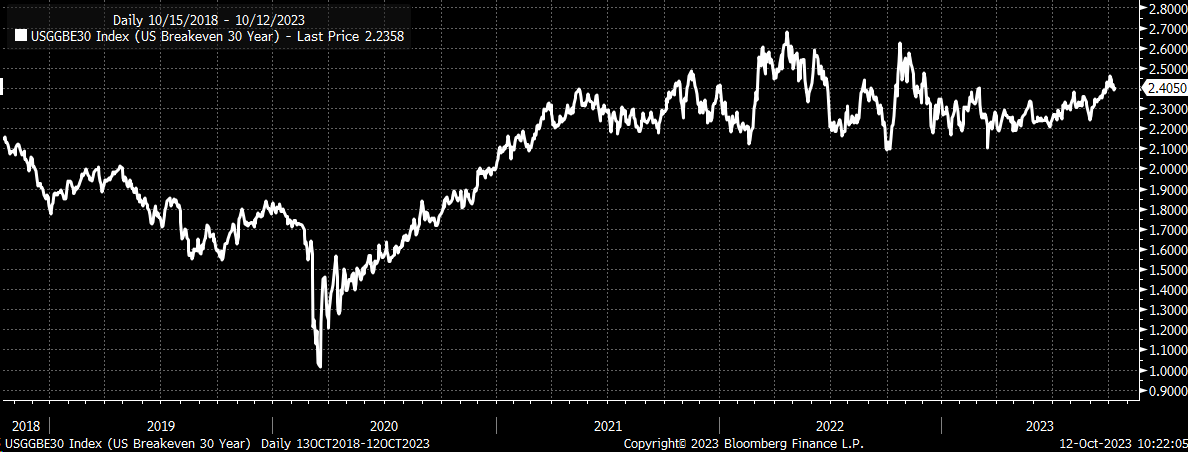

So it is no wonder yields are reversing some of their recent losses and starting to climb again, and 30-year breakeven inflation expectations are rising back to 2.4% and approaching the upper end of their trading range over the past five years.

{kind=link}

Higher Yields

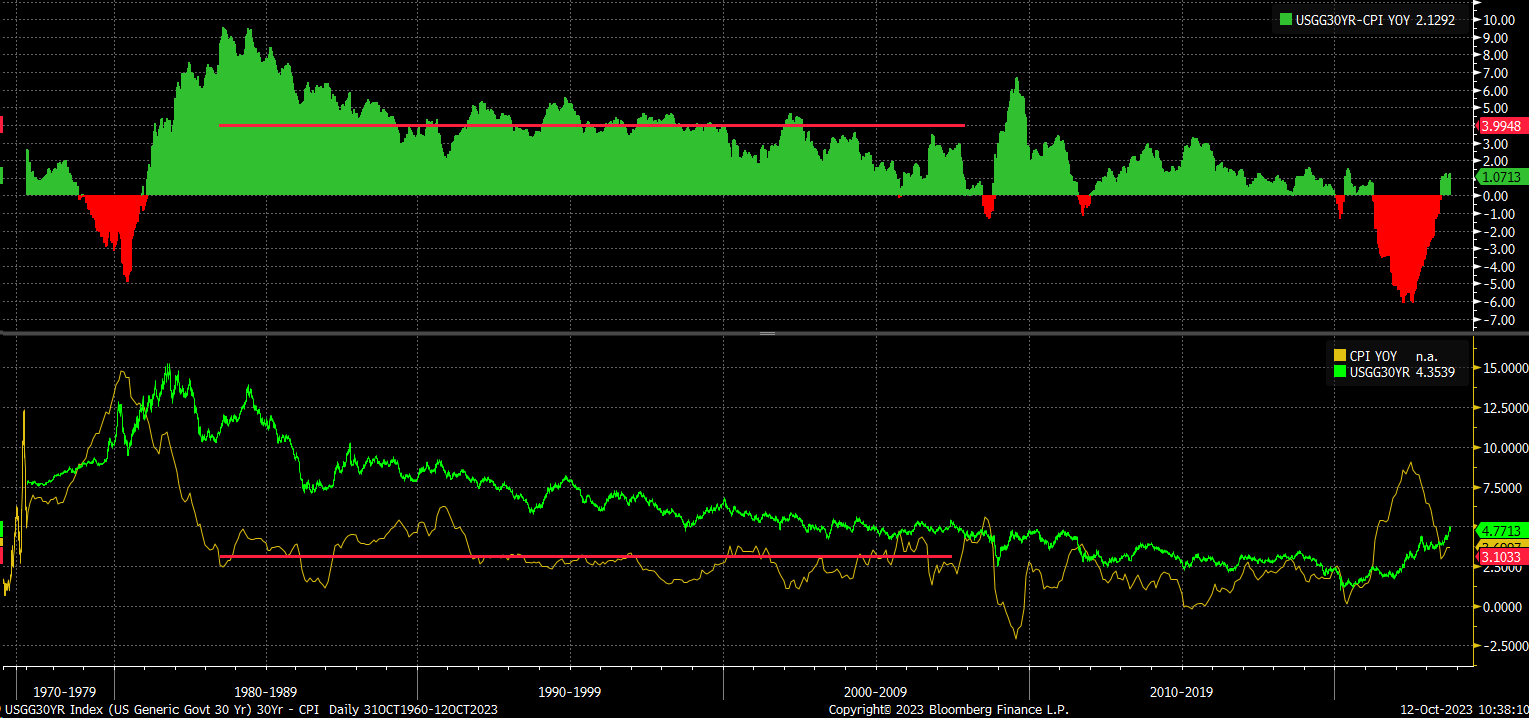

Inflation is just proving to be far more challenging to control than what the market has priced in, and this will result in continued upside risk to rates and is likely to continue to pressure rates on the long end of the curve higher. Looking back into the 1980s, 90s, and 00s, when inflation averaged around 3.1%, 30-year rate trade with a premium of 1.5% to 9.5% but averaged about 4% higher than the inflation. Even if a 4% premium is too high, it still seems like the 1% premium that the 30-year Treasury rate has versus the current headline inflation rate is too low.

{kind=link}

For the most part, regardless of where the premium should or could be, it tells us that the longer headline and core inflation stay elevated, the longer and more likely it is that rates on the long end of the curve will stay elevated.

While stocks have finally started to appreciate some of the risks that come with higher rates, it appears they still have more work to do as they begin to price in rates staying higher for far longer than what appears to be expected.

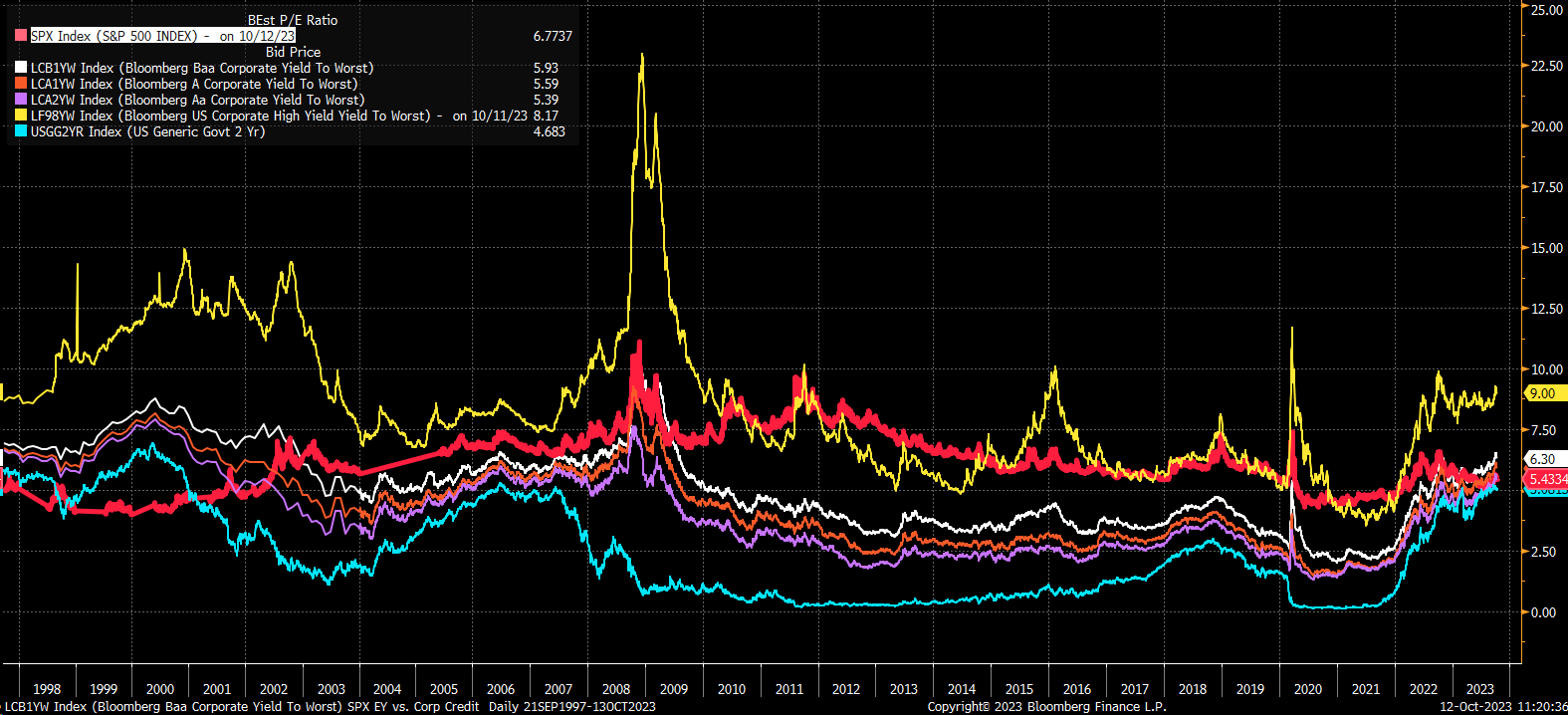

Stocks Too High Relative To Bonds

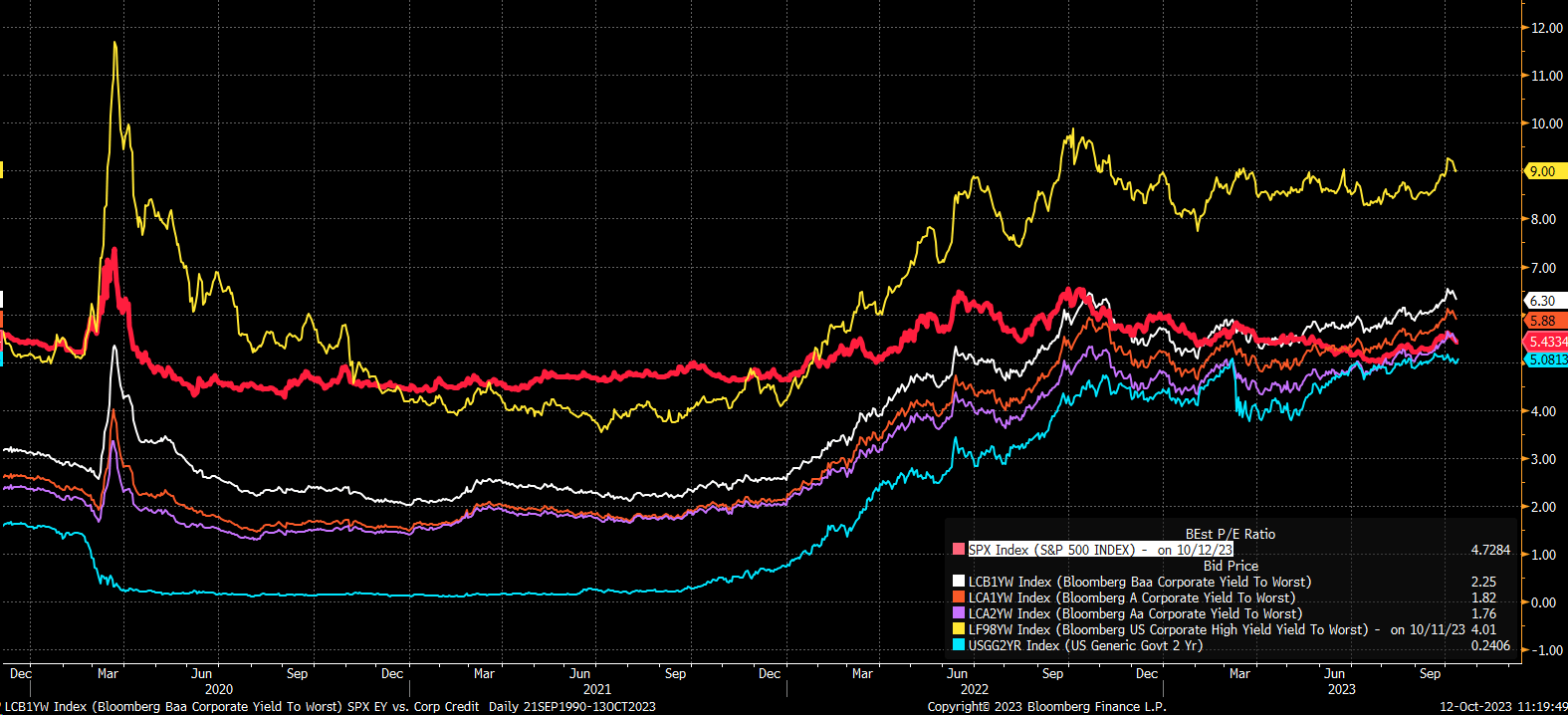

But more interesting, the S&P 500 (SP500) blended 12-month forward earnings yield went from being the highest yielder among corporate and government debt in 2021 to having one of the lowest yields by October 2023. The earnings yield of the S&P 500 in July 2021 was 4.65%, and today, it is 5.43%, while high-yield debt has risen from around 3.5% to 9%, while double AA has gone from 1.75% to 5.4%.

{kind=link}

Going back to 1997, the only time other times we have seen equities yields trade below that high yield, corporate, and 2-year Treasuries (US2Y) was back in 1999 and 2000. At this point, the only debt instruments equities are not trading below are those of 2-year Treasuries.

{kind=link}

But if inflation tells us that the risk is that rates go higher, and the longer stocks hold up versus debt instruments, the more expensive stocks get on a relative basis. The one thing that could keep equities grounded at this point is the hope that earnings in 2024 will deliver significant growth; while that is possible, it is yet to be seen.

But what is clear is that inflation will be here for some time longer, rates will stay higher, and the risk of stock moving lower continues to be extremely high.

For further details see:

Hot CPI Print Means Higher Yields, And Massive Risks To Stocks