APLE - Hotel Income: 6% Monthly Dividends With Apple Hospitality

2023-10-17 16:45:34 ET

Summary

- Apple Hospitality is a hotel REIT that has outperformed since the pandemic and offers a 6% dividend yield.

- The company owns high-quality hotels managed by well-known brands like Marriott and Hilton.

- Despite challenges in the hotel industry, Apple Hospitality has shown resilience and has a strong balance sheet.

Introduction

Is it just me, or are hotels getting really expensive?

Looking at the chart below, I may not be the only one who complains about this issue. Since 2020, hotel and restaurants have massively hiked their prices. Before the pandemic, inflation was consistently close to 2.4%. Even after a downtrend that started almost two years ago, inflation is still above 5.0%.

While there is absolutely no reason why anyone absolutely should have exposure to this rather volatile industry, there are a few good ways to get access to high-quality hotel income.

One of them is VICI Properties ( VICI ). That REIT, with a 5.7% yield, is focused on entertainment hotels. It owns roughly half of the major hotels on the Las Vegas Strip. It's also the favorite REIT of many people on Seeking Alpha.

However, Apple Hospitality ( APLE ) is often ignored.

Although this REIT underperformed the market through the pandemic, it has done very well since then, even outperforming VICI since 2020.

In this article, I'll walk you through what makes this REIT so special and the health of the hotel real estate sector.

So, let's get to it!

Buying The Best In A Tricky Industry

Generally speaking, I am not a fan of leisure real estate. The hotel industry is extremely competitive and prone to above-average demand risks. For example, during recessions, hotels are much more likely to see declining revenues than owners of residential properties - or even industrial properties.

However, Apple Hospitality is doing a terrific job.

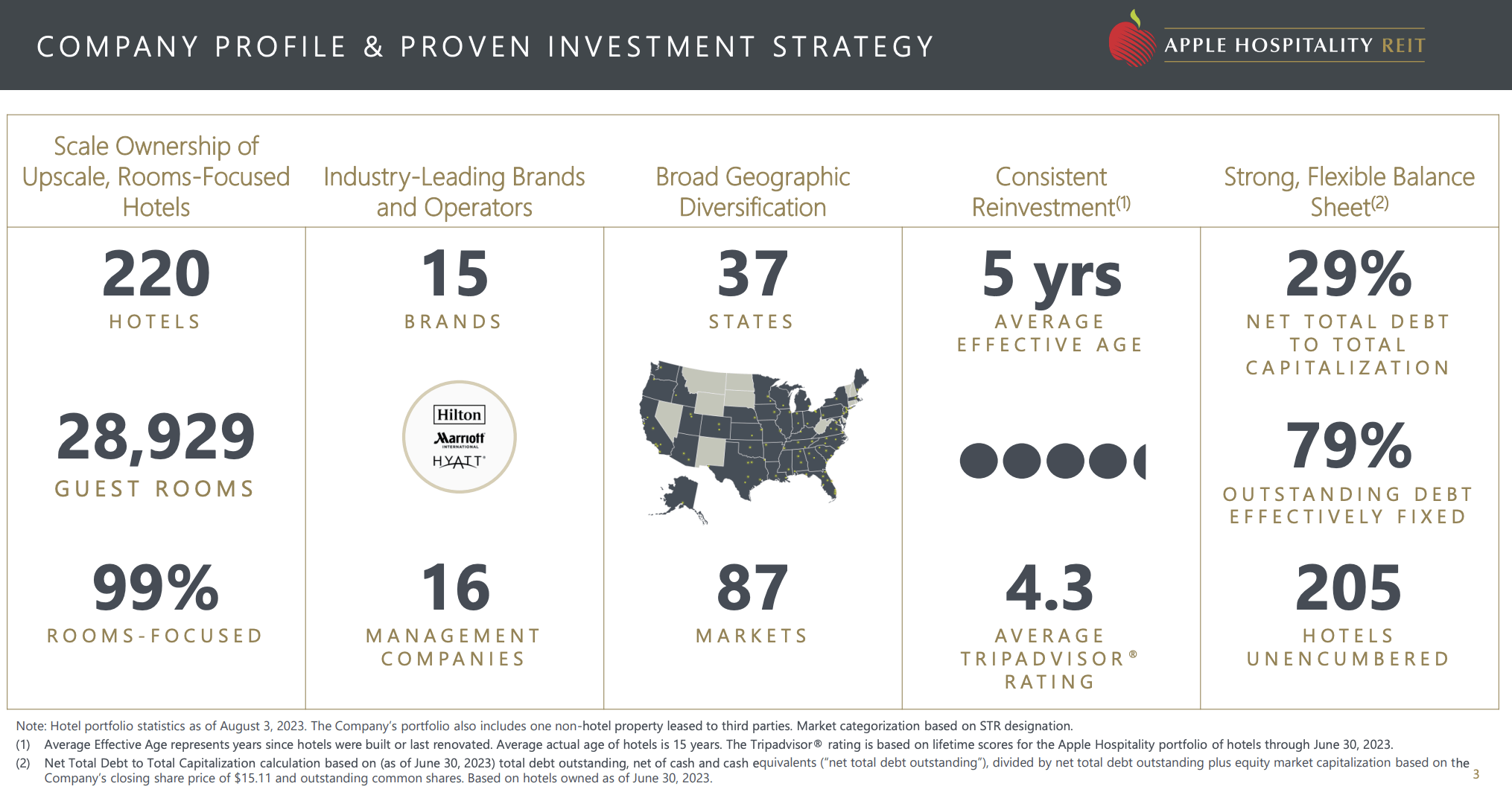

The company, which has a $3.7 billion market cap, operates in 87 markets across 37 states. It owns 220 hotels that cover close to 29 thousand rooms. The company is 99% room-focused.

These assets are managed by 16 management companies that have done a good job, as the average TripAdvisor rating is 4.3 (out of 5).

{kind=link}

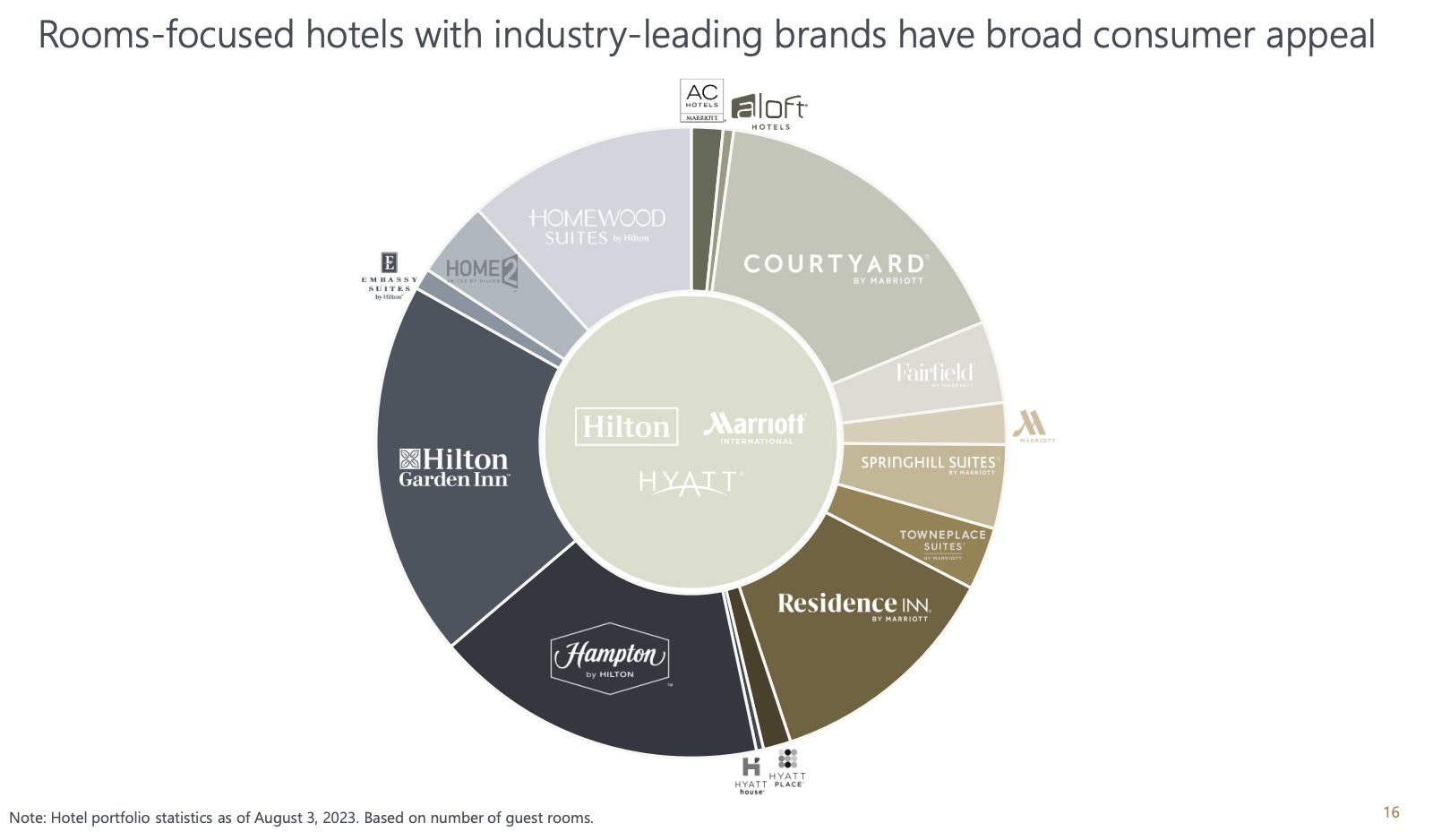

It also helps that Apple doesn't own random hotels.

The majority of APLE's hotels operate under the umbrella of well-known brands like Marriott ( MAR ) and Hilton ( HLT ). These hotels are managed through separate management agreements with the aforementioned hotel management companies, none of which are affiliated with the company.

Essentially, the management agreements focus on fostering a mutually beneficial relationship that includes national advertising, training, quality standards, centralized reservation systems, and marketing programs to enhance brand awareness.

{kind=link}

Without these deals, it would be impossible for APLE to manage so many hotels in an efficient way.

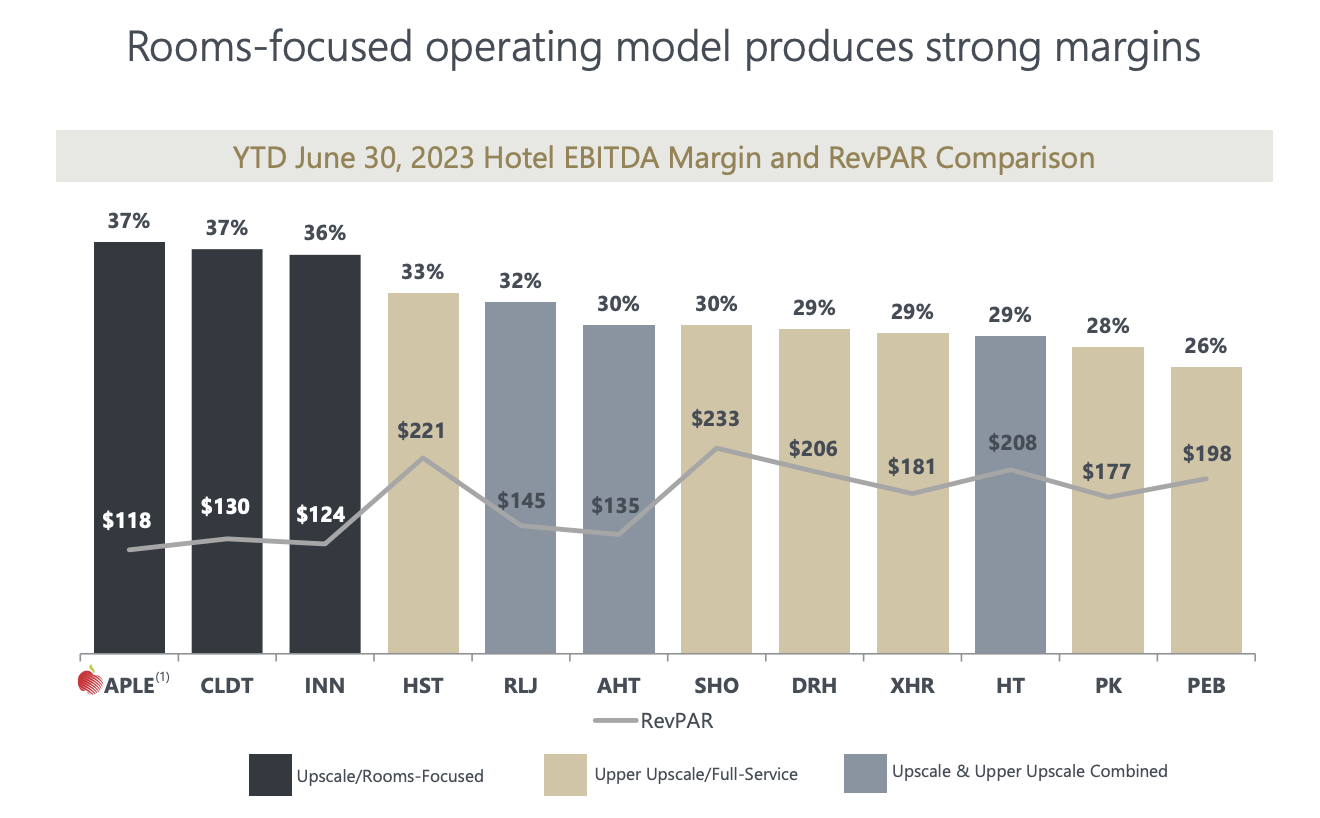

The company's emphasis on high-end hotels and rooms has resulted in industry-leading EBITDA margins despite the fact that its revenue per available room is lower than that of hotel REITs with pricier hotels in their portfolio.

{kind=link}

As a result, APLE has even outperformed the Vanguard Real Estate ETF ( VNQ ) over the past ten years - despite getting nuked during the pandemic!

It also helps that the company has a very healthy balance sheet.

The company has $1.4 billion in total outstanding debt as of June 30, 2023, with a weighted average interest rate of just 4.3%.

Apple Hospitality also enjoys a lot of liquidity and a high portion of fixed-rate debt, which allows it to avoid some of the troubles the sector is facing.

At the end of the quarter, our weighted average debt maturities were 4.1 years . We had cash on hand of approximately $6 million and availability under our revolving credit facility of approximately $626 million. And approximately 79% of our total debt outstanding was fixed or hedged .

In July, we entered into an amendment of our $225 million term loan facility, which extended the maturity of the existing $50 million term loan by 2 years to August 2, 2025, and aligned to the maturity date with the other term loan and the broader $225 million facility. - APLE 2Q23 Earnings Call (emphasis added by author)

How's The Business/Sector Doing?

Speaking of the second quarter, the company did very well.

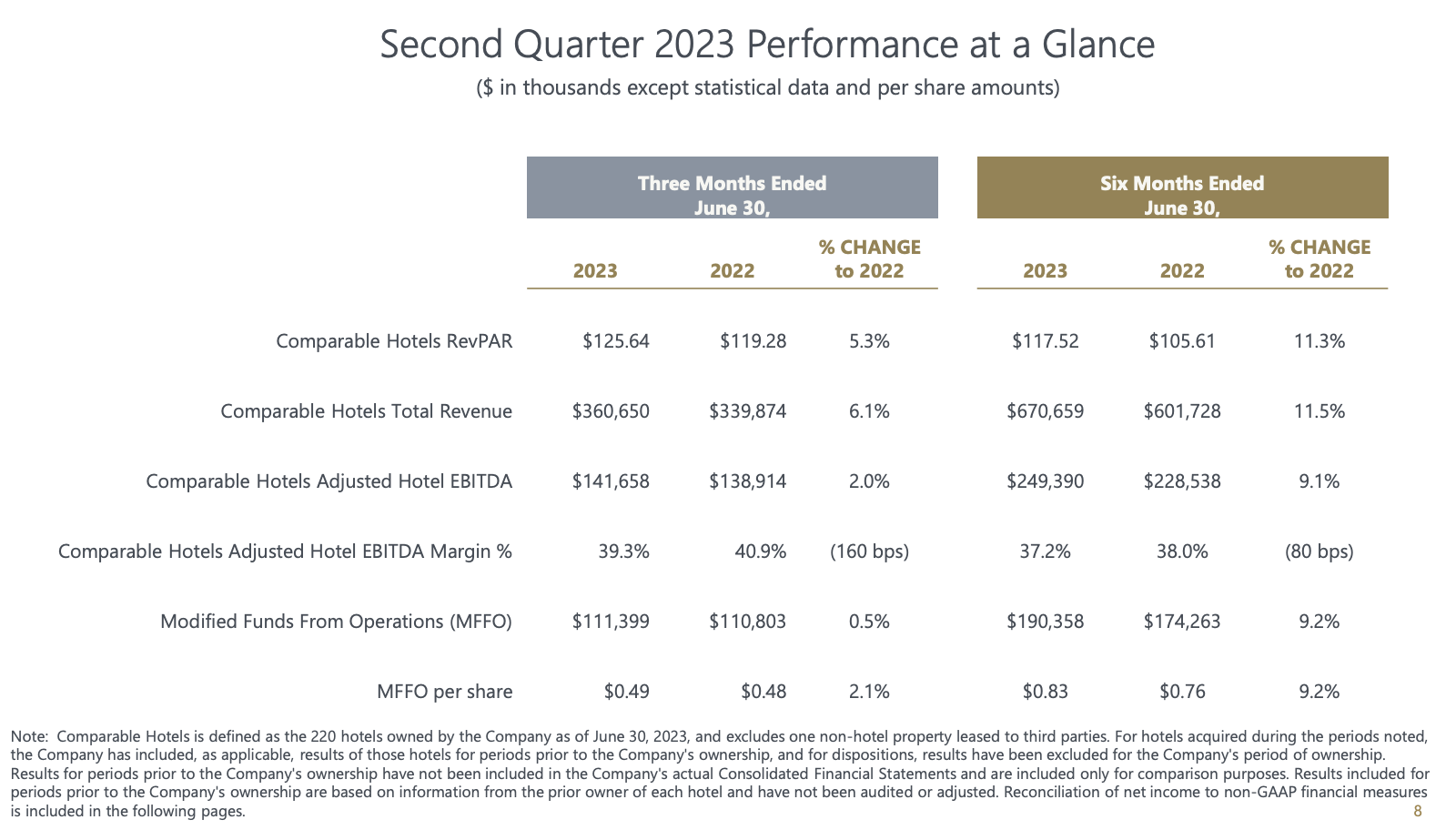

During this quarter, the hotel's total revenue came in at $361 million, which marks a 6% increase compared to the same period last year. For the first half of the year, the total revenue was $671 million, representing a growth of over 11% from the first half of the previous year.

This growth was attributed to continued strength in leisure demand and recovery in business travel during the quarter.

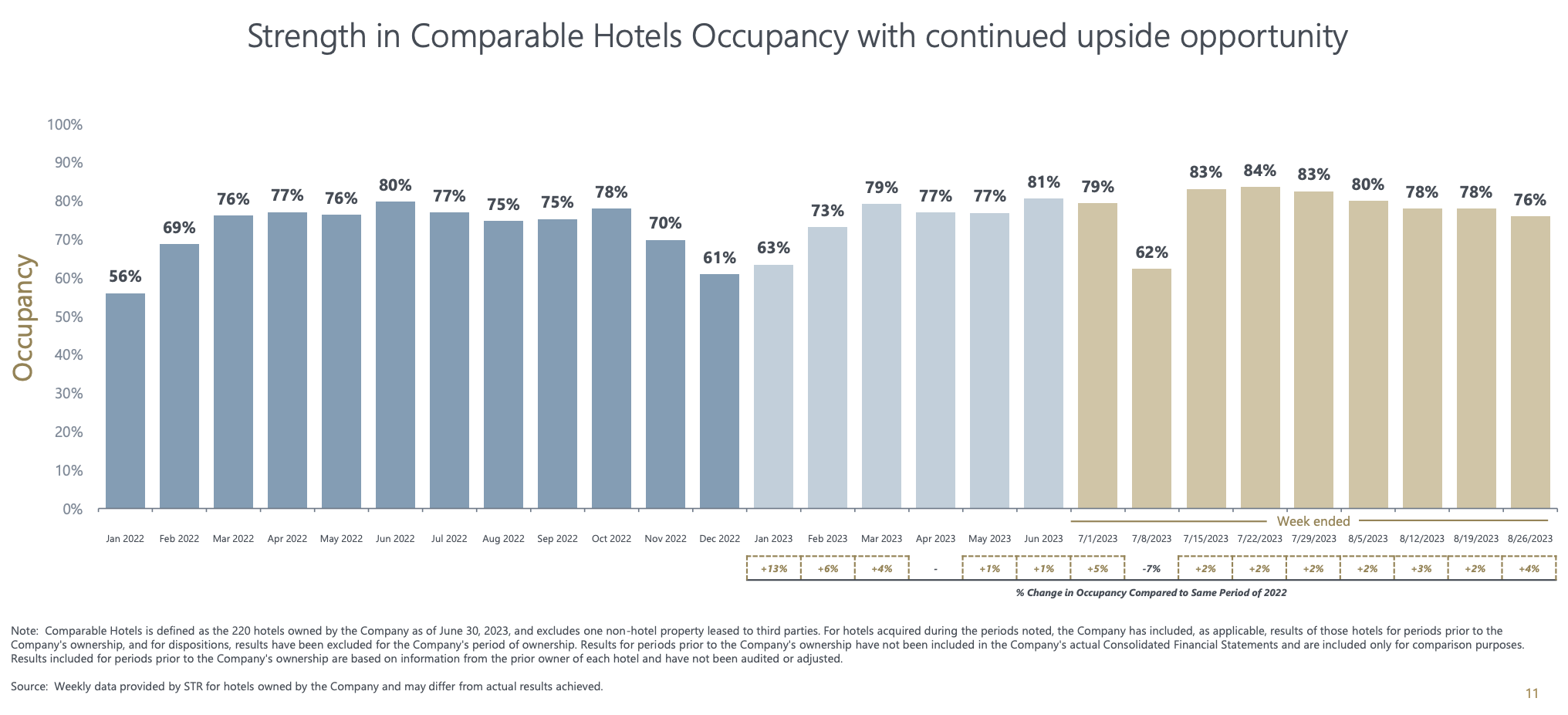

The comparable hotels achieved a RevPAR of $12, a 5% increase over the second quarter of 2022.

Other key metrics like Average Daily Rate ("ADR") and occupancy showed positive trends.

- ADR was $161, up by 5%, and occupancy stood at 78%, up nearly 1% compared to the second quarter of 2022. Year-to-date data through June indicated a consistent growth pattern, with ADR up by 7%, occupancy up by 4%, and RevPAR up by 11% compared to the same period in 2022.

{kind=link}

According to the company, the leisure travel segment remained strong during the quarter, with weekend occupancies in April, May, and June ranging from 82% to 84%.

There was a gradual increase in business demand, improving year-over-year and supporting average weekday occupancies in April (75%), May (74%), and June (79%). Midweek occupancies also strengthened, reflecting improvements in business travel.

{kind=link}

Unfortunately, Wells Fargo found that the recovery in the industry is weakening a bit.

In September, it was reported that the commercial real estate fundamentals, including vacancy rates and rent growth, have softened across various sectors.

In the hotel market, demand for rooms has slightly declined, reflected in occupancy rates comparable to the same quarter of the previous year.

Average daily rates and Revenue per Available Room growth have also moderated, signaling a normalization in the industry.

Wells Fargo

Factors such as the rise of remote work and a slow recovery in business travel have contributed to these trends in the hotel sector.

Nonetheless, APLE was able to hike its guidance.

Outlook, Dividend & Valuation

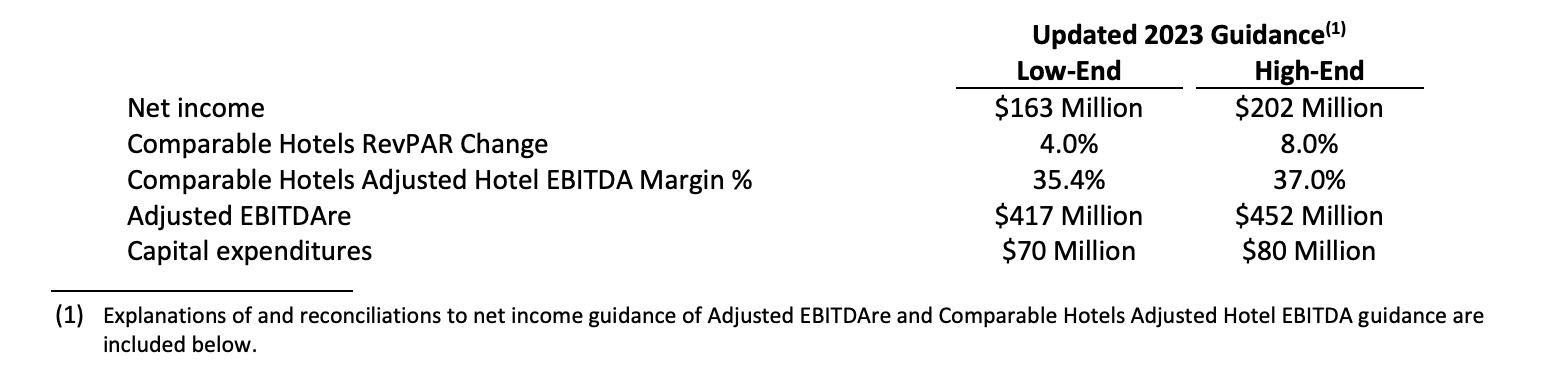

The company adjusted its annual guidance, anticipating a comparable hotel RevPAR growth between 4% and 8%, 100 basis points higher on both the high and low end.

The comparable hotel adjusted hotel EBITDA margin is expected to be between 35.4% and 37.0%.

{kind=link}

The company's dividend yield is currently 6%. This is based on a monthly dividend of $0.08 per share.

This dividend is protected by its healthy balance sheet, the hotel recovery, and a 74% adjusted funds from operations payout ratio. This is in line with the sector median.

Last year, the company paid a $0.08 special dividend in December.

Before the pandemic, the company paid a $0.10 monthly dividend. I expect the company to reach that number again over the next 12 to 24 months unless the economy falls off a cliff, which could cause a shift to balance sheet protection.

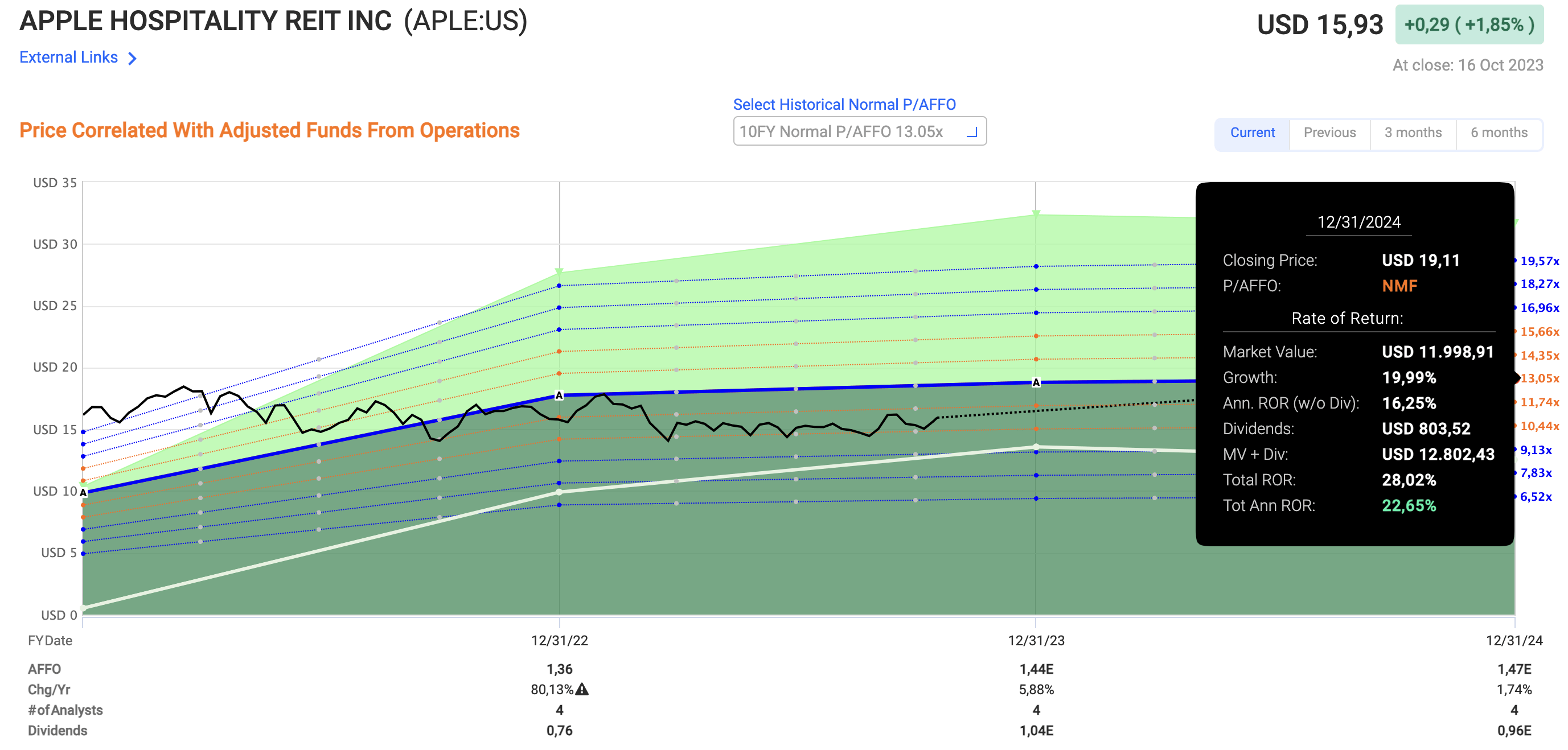

Now, the company is trading at 11x adjusted funds from operations. The ten-year normalized P/AFFO ratio is 13.1. Next year, the company is expected to grow its AFFO by 1.7% after growing it by 5.9% in 2023E.

Hence, a return to its normalized valuation could cause the stock to return 23% per year through 2025, including dividends. All of this data is visible in the chart below.

{kind=link}

The current consensus price target is $18.40, which is 13% above the current price.

Having said that, I expect APLE to continue outperforming the VNQ ETF. I also have to say that it's my favorite hotel play (ignoring gambling and entertainment).

However, while APLE is a terrific monthly high-yield play, the current economic environment is fierce, and pressure on hotels is building. I do not recommend anyone to dive into APLE at these prices.

If you like APLE, start by buying gradually. If the stock drops, investors can average down. If it takes off, investors have a foot in the door.

These economic risks are also the reason why I give the stock a Hold rating.

This is how I currently treat all of my investments.

Takeaway

APLE, with its strategic emphasis on high-end hotels and strong brand affiliations, has proven resilient, showcasing industry-leading EBITDA margins and outperforming expectations.

The company's healthy balance sheet, consistent growth, and attractive dividend yield make it a compelling choice.

However, caution is warranted in the current economic climate, suggesting a gradual, measured approach to investing in this monthly dividend payer.

Despite the sector's challenges, with a well-considered strategy, APLE has the potential to be a rewarding investment in the evolving hotel landscape.

For further details see:

Hotel Income: 6% Monthly Dividends With Apple Hospitality