HT - Hotel REIT Preferred Stock Analysis: Buy Chatham Lodging And Sell Hersha Hospitality Preferreds

2023-06-22 11:00:00 ET

Summary

- It is a fairly simple process to select the best hotel REIT Preferred since they all operate similarly, and all hold the same asset class.

- The primary difference between preferred stocks from the various hotel REITs is their yield and their safety.

- I have calculated leverage for all of the primary hotel REITs which have issued preferred stocks and by also using their current yield, we can easily compare them.

- My conclusion is that Chatham Lodging Preferred “A” stock is the most undervalued or best choice, while Hersha Hospitality Preferred “E” stock is the most overvalued and is rated a sell.

* This article was first published to Conservative Income Portfolio members.

Hotel REITs

Hotel REITs are a very simple business. They own hotels, but they don’t run them. Instead, they hire hotel operating companies, like Wyndham, Hilton and Marriott, to run the hotels. REITS are generally passive in that they own property, but they don’t operate them or use the properties that they own.

Chatham Lodging

Chatham Lodging ( CLDT ) is primarily invested in upscale extended-stay hotels which are operated by and carry the Marriott brand or the Hilton brand. Two examples are Marriott Residence Inn and Homewood Suites by Hilton. They also own “premium branded” traditional hotels that operate under the Marriott, Hyatt, Hilton, and Hampton Inn name.

Personally, I like the extended stay segment, although that is just my personal preference. I don’t want to have to go to a restaurant for every meal if I am staying several days, and it gives better competition to the growing Air BNBs of the world.

Hersha Hospitality

Hersha Hospitality ( HT ) own upscale hotels in gateway cities like New York, Washington DC, Boston with hotels also in Florida and California. Due to its higher leverage than the typical hotel REIT, management felt it necessary to suspend preferred stock dividends for a period of time during the period of the COVID scare and the months following. They have since re-paid the missed dividends, but HT has been the worst performing hotel REIT over the last 5 years. I should clarify that it is the worst among the non-troubled hotel REITs (the ones that are paying a common dividend).

{kind=link}

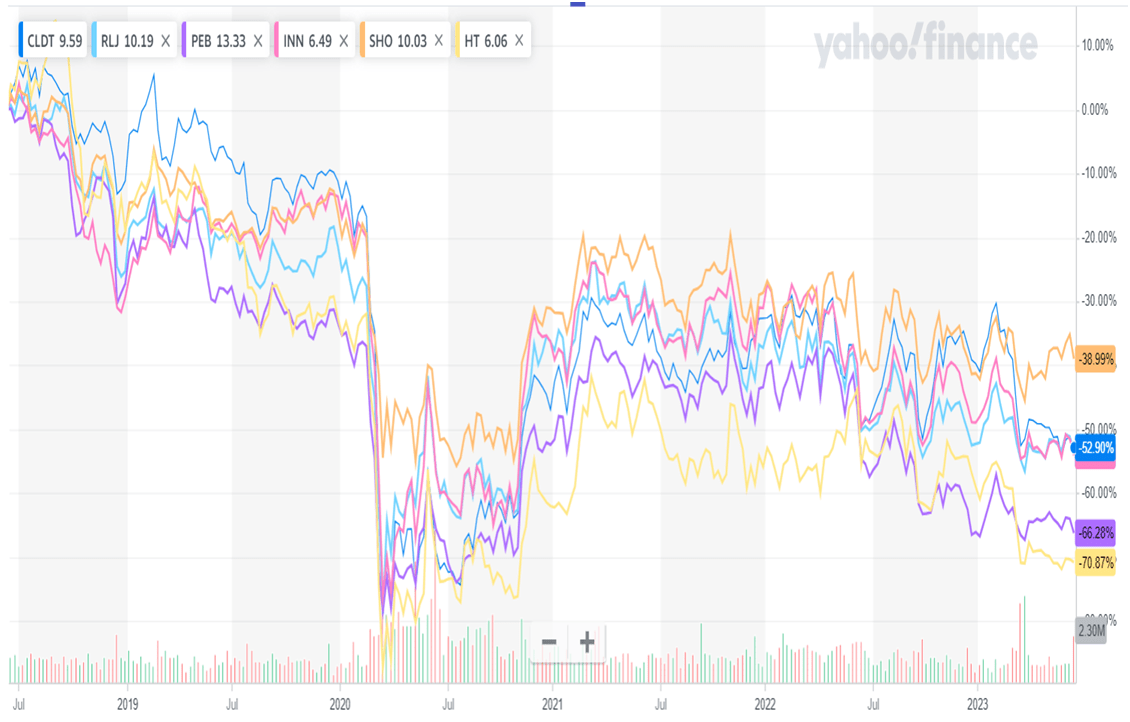

As you can see from the above 5-year price chart, CLDT had an average performance in the sector, while HT was the worst with a 71% drop in the price of its common stock. This is likely due to their high leverage, which exacerbates losses when times are tough.

Comparison of Hotel REIT Preferred Stocks

As you can see from the chart above, the hotel REITS basically move together as a group, which make them a good choice for treating the whole group of hotel REIT preferred stocks as being similar and comparable except for their leverage. The chart below details the current yield, price and leverage of each hotel REIT preferred, excluded those of SOHO and AHT (which have extreme leverage and don’t pay a common dividend) . The leverage is computed as the percentage of liabilities (including preferred stock) relative to the company’s market capitalization (the value of the company’s common stock). A downward adjustment was made to liabilities based on the amount of cash the company holds.

Author

In my view, SHO, DRH, CLDT and RLJ have good balance sheets. PEB and INN are so-so, and HT has a poor balance sheet.

SHO has a great balance sheet with the lowest leverage. However, you can see that its current yield is fairly low relative to the others. Overall, I like SHO preferreds for conservative investors who value safety over yield. This is a rock solid company. But the yield is a bit low for me, but I think that a drop in price of these preferreds would make them a buy.

DRH-PA also sports a nice balance sheet. The problem with DRH-A is that it sells well above par, making it unattractive relative to the others which have large price upside potential. The YTC (yield to call is not interesting here).

CLDT-PA (CLDT.PA) has the highest yield of the REIT preferreds with good balance sheets. I believe there is little credit risk with CLDT-A, so the 8.58% current yield along with 36% upside to its previous high of $26.85 makes CLDT-A quite attractive. And like all hotel REITs, 20% of 8.58% current yield is tax free for Americans .

I should also add that the current yield on CLDT-A looks very good as its yield is higher than the significantly higher leveraged INN preferred stocks, and it is even higher than or equivalent to the poorly leveraged HT-D and HT-E. So to get yields that are as good or better than riskier preferred stocks makes CLDT-A undervalued.

HT-E (HT.PE) is clearly the most overvalued preferred stock in this list, with a relatively low yield yet with the worst balance sheet or most risk. Why anyone would opt to own HT-E is a mystery to me, as even among HT preferred stocks, HT-C is a much better value. If you own HT-E, you should clearly either swap to HT-C, if you feel you want to stay with an HT preferred stocks, or swap it for CLDT-A.

General Comments

The hotel sector, and travel in general, has been holding up well in the face of the Feds efforts to slow the economy. In my portfolio, I always hold at least 1 hotel REIT preferred because they are easy to evaluate relative to one another and volatility generally changes which one is the best value. Thus, I am able to often swap and improve my position regularly. Each swap either increases my yield, lowers my risk, or a combination of both. This is why I expect to always have at least 1 hotel REIT in our portfolio at our Conservative Portfolio Income service, and I recommend that more active investors to do this as well.

Note that CLDT-A goes ex-dividend very soon, on June 29 th .

Summary

In an analysis of hotel REIT preferred stocks, CLDT-A looks to currently be relatively undervalued and the best buy in the sector. The undervaluation is based on a combination of yield and safety. I think CLDT-A is a buy here, with an 8.58% current yield, and Americans also get a tax benefit; that being that 20% of your dividend income is tax free. And CLDT-A is currently deeply discounted from par at $19.65 giving it a large upside; 36% upside to its old high.

On the other hand, preferred stock HT-E is a sell. It has one of the lower yields among hotel REIT preferred stocks, yet it is the riskiest within the hotel REIT sector in terms of its leverage. It is even overvalued versus the other HT preferred stocks, especially HT-C.

For further details see:

Hotel REIT Preferred Stock Analysis: Buy Chatham Lodging And Sell Hersha Hospitality Preferreds