LSEA - Hovnanian Enterprises: More Weakness Lies Ahead

2023-03-07 05:21:34 ET

Summary

- At first glance, Hovnanian Enterprises looks like a dirt-cheap business that has tremendous upside potential.

- In the long run, the company might very well be fine, but it has a large amount of debt and is seeing signs of additional pain around the corner.

- Investors would be wise to approach this prospect with caution until we see the depths of this downturn.

While most parts of the economy are still showing tremendous signs of strength, one market segment that has begun to show some meaningful weakness because of high inflation and rising interest rates is the home-building market. One firm in this space that has been able to demonstrate this weakness, not only from a backlog perspective but also from a recent financial perspective, is Hovnanian Enterprises ( HOV ). If you look at the pricing of the company as it stands today, shares look incredibly cheap. But when you see exactly how quickly the picture is deteriorating, questions arise about the health of the business moving forward. Generally, I am a huge fan of taking a contrarian stance to the investments that I make. But because of the large amount of debt and how rapidly we have seen a decline in backlog for the firm, I do think a more cautious approach would be a good idea for now.

A homebuilder that’s pulling back

The management team at Hovnanian Enterprises describes the company as a designer, builder, marketer, and seller of single-family detached homes, attached townhomes and condominiums, urban infill, and active lifestyle homes in planned residential developments. The company does describe itself as one of the largest builders of residential homes in the US. But that might be stretching it to some degree. Although the company is definitely larger than the vast majority of home builders, it boasts a market capitalization of only $393.2 million as of this writing. Compared to the majors out there, this is of microscopic size.

Operationally, when combined with its unconsolidated joint ventures, the firm has delivered over 361,000 homes throughout its lifetime. This includes 6,090 homes during the 2022 fiscal year. Operations for the company are spread all across the US, including in states like Florida, Georgia, South Carolina, Texas, California, and more. It also has operations in parts of the northeast like Ohio and Maryland. In all, the company's operations are focused around 20 of the 50 top housing markets in the country, granting it the ability to benefit from pockets of high demand. The firm used to be larger by the way. Starting in 2016, the company began exiting certain markets such as Minnesota and North Carolina. It also left the San Francisco Bay area, as well as Tampa, Florida, during the 2018 fiscal year. It also no longer operates in places like Chicago.

{kind=link}

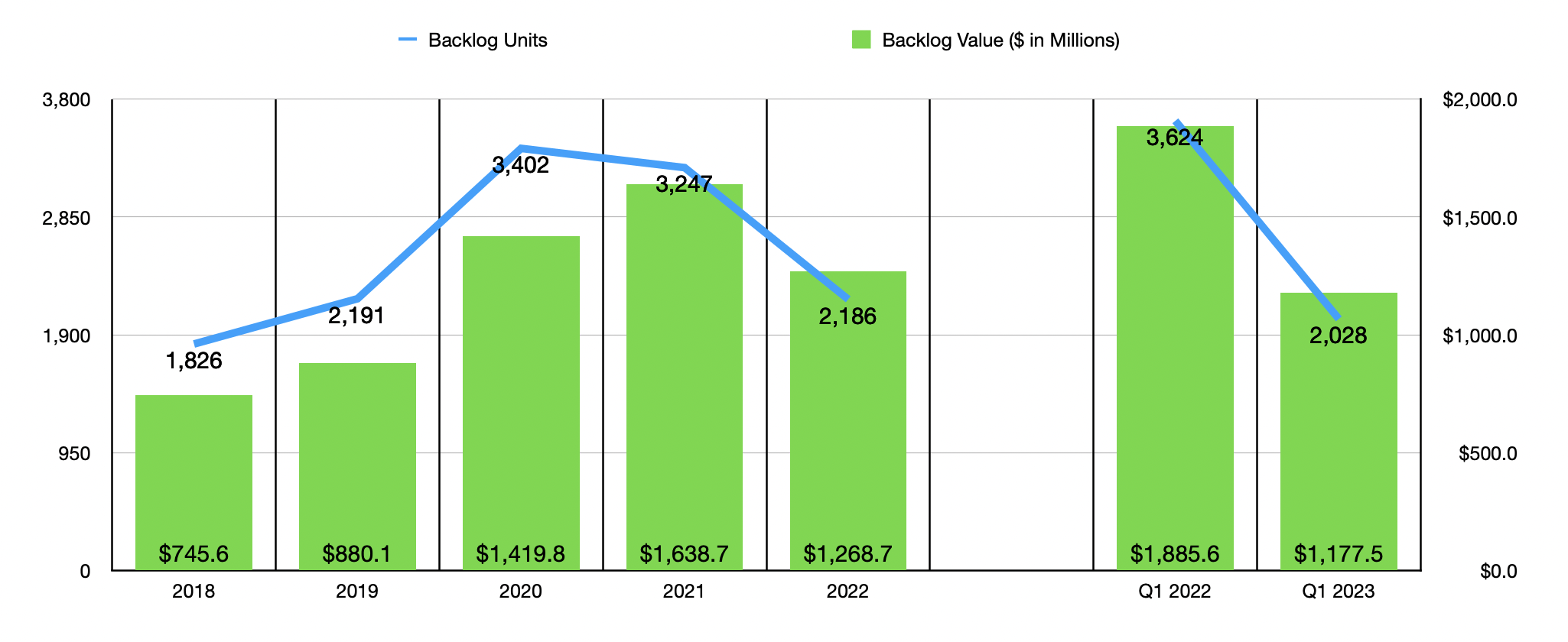

Over the past five years, the financial picture for the company has looked quite positive on the top line. Revenue increased in each of the past five years, rising from $1.99 billion in 2018 to $2.92 billion in 2022. Naturally, both an increase in home prices and a rise in the average price of homes aided in this upswing. For instance, by the end of the 2018 fiscal year, the company had backlog totaling 1,826 homes. By 2020, this number peaked at 3,402. Since then, the business has seen a decline in the number of units in its backlog. As of the end of the 2022 fiscal year, this number had dropped to 2,186. But it wasn't until the 2021 fiscal year the backlog as measured by total dollar value peaked, hitting $1.64 billion at the end of the year. By the end of the 2022 fiscal year, this had dropped to $1.27 billion. Given this rapid decline relative to the continued increase in revenue, it was only a matter of time before sales would eventually fall.

{kind=link}

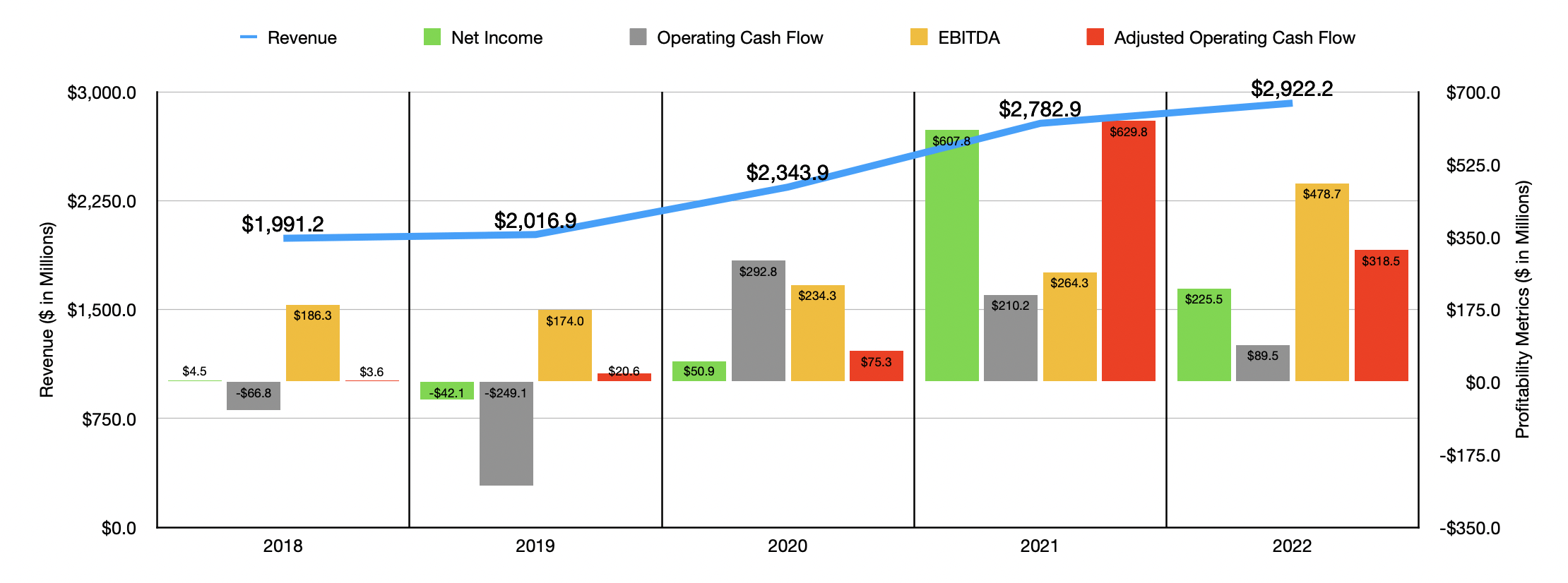

Before we get to that, however, we should discuss profitability. As you can see in the chart above, net income for the firm has been all over the map in recent years. The company has gone from a net loss of $42.1 million all the way up to a profit of $607.8 million. Operating cash flow has been little better, ultimately peaking at $292.8 million in 2020 before declining to $89.5 million in 2022. Even if we adjust for changes in working capital, we would see a tremendous amount of volatility. The only metric that shows any real degree of stability on the bottom line is EBITDA. After falling from $186.3 million in 2018 to $174 million in 2019, it began a steady increase, ultimately hitting $478.7 million in 2022.

{kind=link}

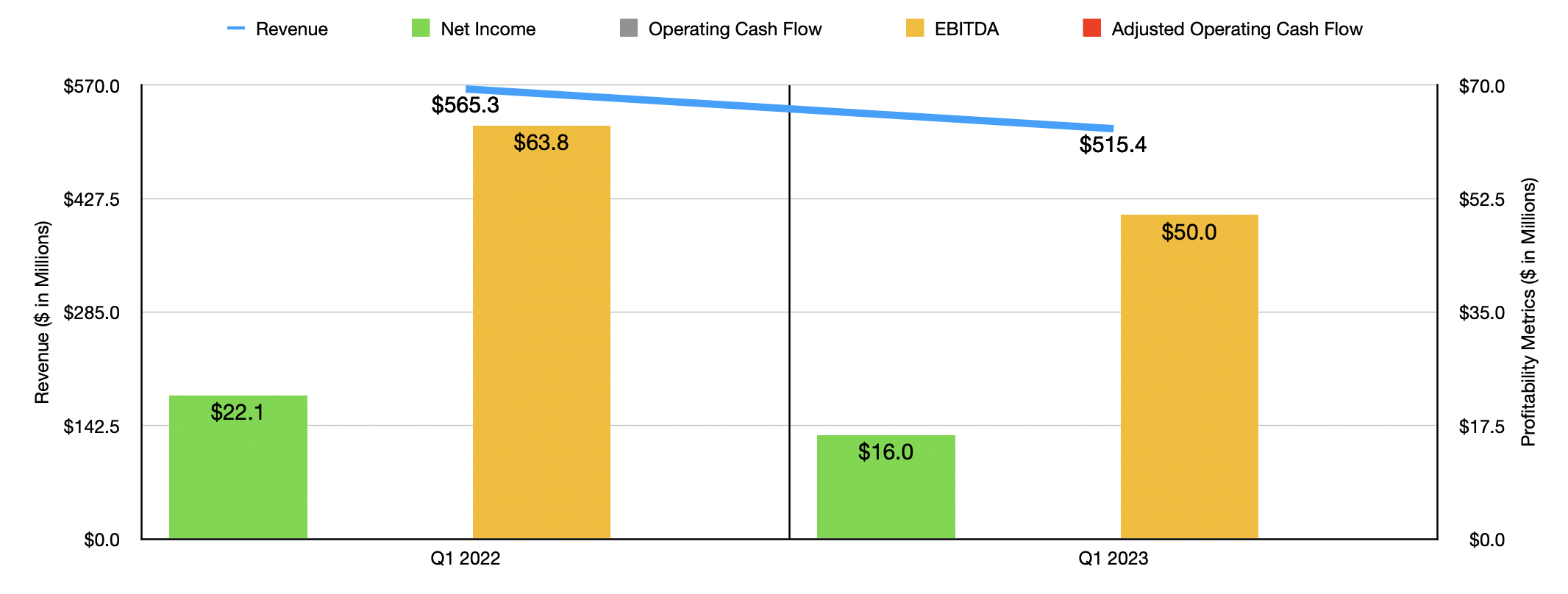

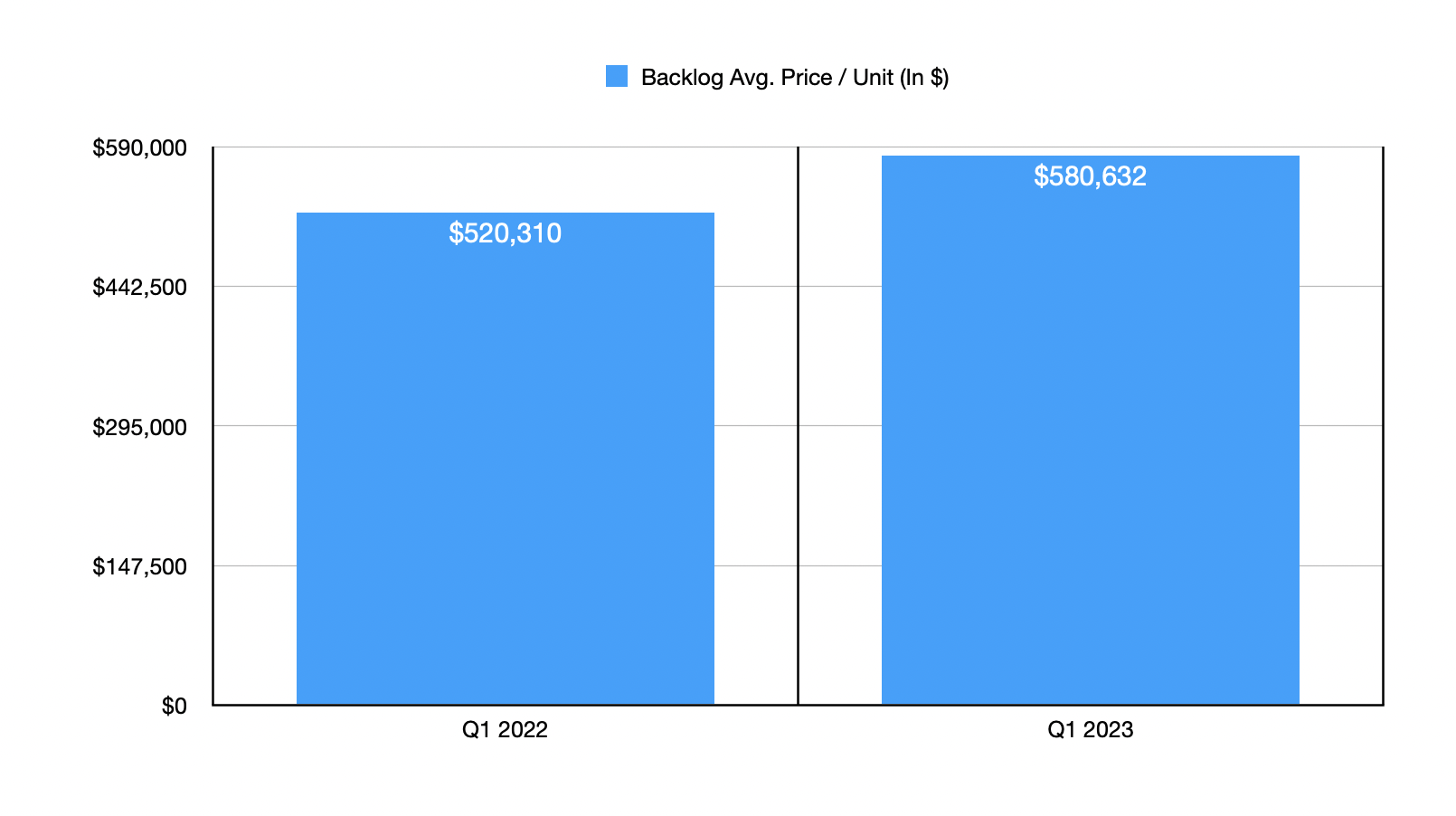

For the first quarter of the company's 2023 fiscal year, financial performance has worsened on both the top and bottom lines. The business went from generating revenue of $565.3 million in the first quarter of 2022 down to $515.4 million in the first quarter of 2023. This decline was driven by a drop in the number of units delivered. It was offset, to some degree, by a rise in pricing. If you look at backlog, for instance, and ignore the contributions from unconsolidated joint ventures, you would see the overall backlog drop from 3,624 in the first quarter of 2022 to 2,018 in the first quarter of 2023. Meanwhile, the average price of a home in backlog jumped from $520,310 to $580,632. Sadly, this increase was not enough to offset the decline in the value of the company's backlog. This fell from $1.89 billion in the first quarter of 2022 to $1.18 billion in the first quarter of 2023.

{kind=link}

On the bottom line, the picture for the business has also worsened. Net income fell from $22.1 million in the first quarter of 2022 to $16 million in the first quarter of 2023. Unfortunately, management did not provide data for operating cash flow yet. The firm has also not reported its 10-Q for the quarter as of this writing. But odds are, it also declined, because during this window of time, EBITDA for the enterprise shrank from $63.8 million to $50 million.

{kind=link}

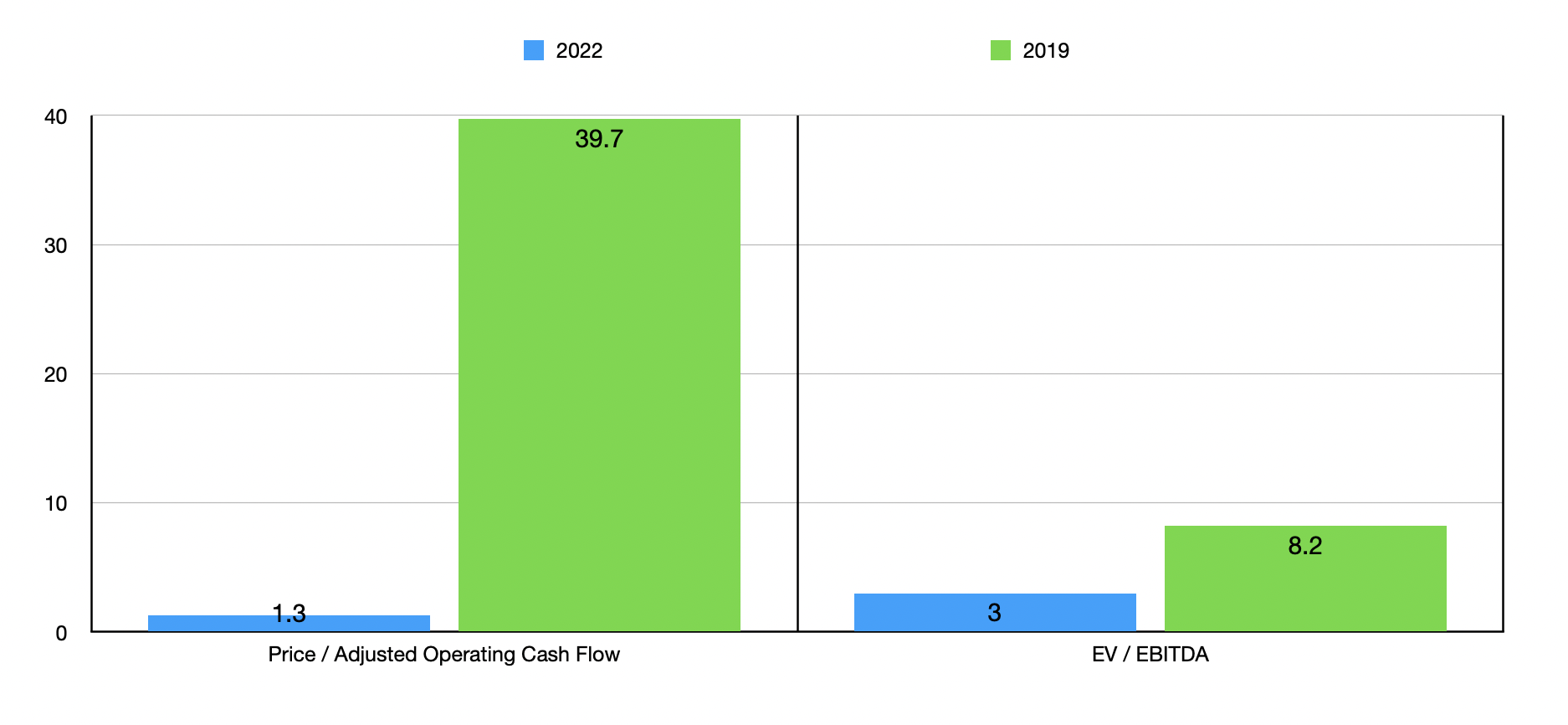

If we use data from the 2022 fiscal year, we can see that shares of the business look to be trading at dirt-cheap levels. The price to adjusted operating cash flow multiple comes in at 1.3, while the EV to EBITDA multiple should be 3. But again, this was based on robust pricing and backlog that we are not likely to see again for the foreseeable future. If, instead, we would look at the company through the lens of the pre-pandemic year of 2019, shares look a lot pricier. The price to adjusted operating cash flow multiple of the firm would come in at 39.7, while the EV to EBITDA multiple would be a much more reasonable 8.2. Using the data from the 2022 fiscal year, I did compare the company to five similar firms. On a price to operating cash flow basis, these companies ranged from a low of 3.9 to a high of 47.1. And when it comes to the EV to EBITDA approach, the range would be from 3.5 to 6.4. In both of these cases, Hovnanian Enterprises was the cheapest of the group.

| Company |

| Price / Operating Cash Flow |

| EV / EBITDA |

| Hovnanian Enterprises |

| 1.3 |

| 3.0 |

| Beazer Homes USA ( BZH ) |

| 6.6 |

| 4.9 |

| Legacy Housing Corporation ( LEGH ) |

| 47.1 |

| 6.0 |

| Landsea Homes Corp. ( LSEA ) |

| 3.9 |

| 6.4 |

| M/I Homes ( MHO ) |

| 9.4 |

| 3.5 |

| Toll Brothers ( TOL ) |

| 6.8 |

| 4.9 |

Takeaway

From the information of my disposal, I will say that, at first glance, Hovnanian Enterprises is the kind of company that would pique my interest. Having said that, the fundamental condition of the company is worsening and that trend is set to persist for some time. It is true that if we go back to prior years, shares don't look necessarily unreasonably pricey, at least when it comes to the EV to EBITDA multiple. But between the severity of the decline in backlog, combined with the fact that the company has $902.2 million in net debt and $140 million in preferred stock that it must pay toward, I think that it's not without its risks.

For further details see:

Hovnanian Enterprises: More Weakness Lies Ahead