HOV - Hovnanian's Valuation Ownership And Debt Concerns: Is It A Viable Investment?

2023-09-28 00:55:41 ET

Summary

- Hovnanian Enterprises has demonstrated operational resilience despite rising mortgage rates, making it an attractive investment opportunity.

- HOV has a rich history in the U.S. homebuilding sector since 1959, offering diverse residential options and emphasizing customer experience.

- The Hovnanian family's control over the company and HOV's financial indebtedness are significant factors influencing its depressed stock price.

- However, my valuation model suggests potential undervaluation, and I provide a sensitivity analysis.

- I project a potential upside of about 163.4% from current prices. However, due to HOV's significant debt and concentrated ownership, I assign it a "buy" rating, not a "strong buy."

Hovnanian Enterprises, Inc. ( HOV ) has demonstrated consistent operational resilience, as evidenced by its Q3 results, despite industry-wide challenges like rising mortgage rates. In my view, this resilience underscores the company's ability to navigate a complex market environment. However, one cannot overlook the significant debt carried by HOV and the potential risks associated with the Hovnanian family's concentrated ownership. These factors could pose challenges for potential investors. That said, based on various growth and interest rate scenarios, I believe that HOV offers a potentially attractive investment opportunity at its present valuation, primarily because its operational strengths may outweigh the concerns.

Business Overview and Revenue Profile

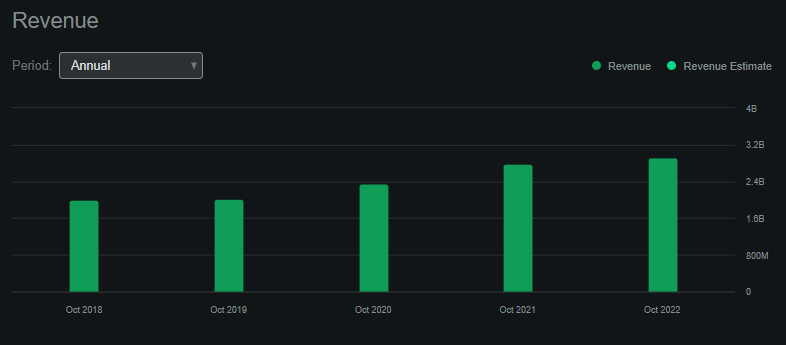

HOV has operated in the U.S. homebuilding sector since 1959. Based in Matawan, New Jersey, the company has delivered 361,000 homes nationwide. With a team of 1,866 dedicated professionals, HOV provides various residential options, ranging from single-family detached homes to urban infill and active lifestyle residences. These homes often have amenities like clubhouses, swimming pools, and tennis courts. The company's offerings cater to diverse customer needs, from first-time buyers to luxury seekers and empty nesters. Their approach , which covers everything from home design to loan origination and post-sales support, emphasizes their commitment to the customer experience. I believe that this all-encompassing approach makes HOV's value proposition a comprehensive solution for homebuyers. Their consistent revenue growth over the years further supports this view and showcases their expertise in the industry.

{kind=link}

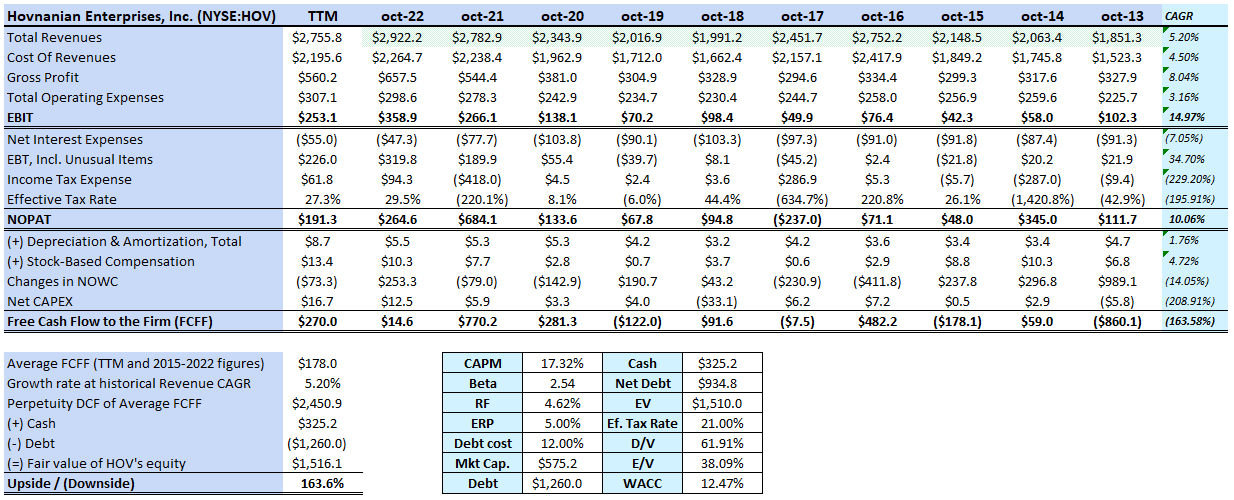

HOV's financial stability is further evidenced by the steady upward trajectory of its EBIT, which has increased at a CAGR of 14.97% since 2013 . Also, despite the surge in mortgage rates, which impacted the entire home sales industry, HOV's robust Q3 results show sound operational management. Unfortunately, HOV's concentrated ownership , largely under the Hovnanian family's control, could potentially sway company decisions in directions that may not always align with minority shareholders' interests (more on this later).

{kind=link}

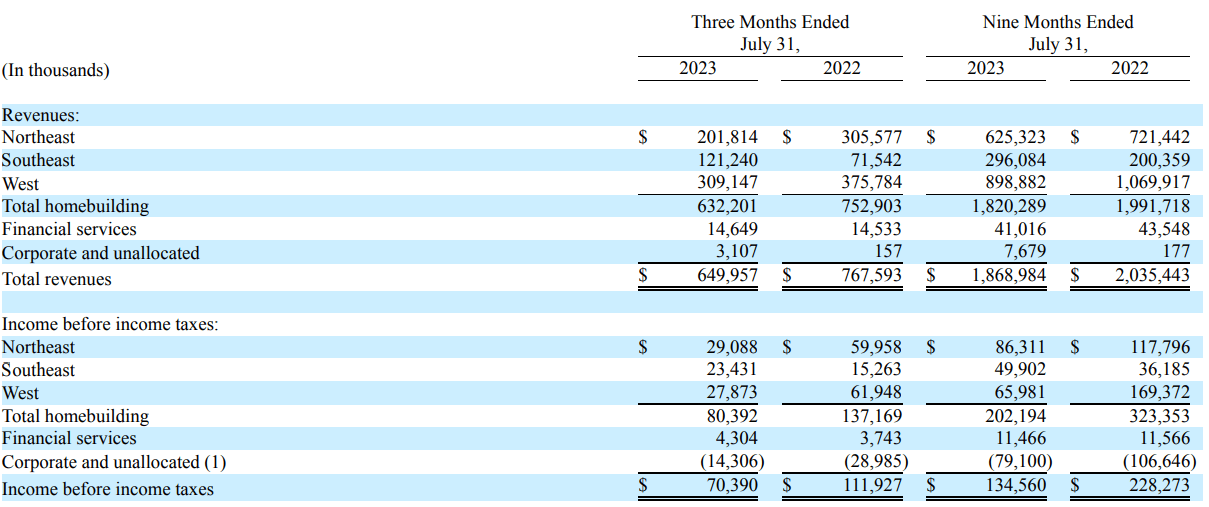

Analyzing HOV's revenue distribution, the West is the largest revenue contributor, while the Northeast boasts the highest average sales prices. Yet, the Southeast's remarkable 28.9% growth in net sales contracts from 2021 to 2022 is a trend that cannot be ignored. I believe demographic shifts, housing affordability, and regional economic growth might drive this surge in the Southeast. This substantial year-on-year growth suggests that the Southeast could soon become a pivotal market for HOV.

Valuation Analysis

At first glance, the company appears undervalued due to its robust FCF. However, HOV's significant debt is pivotal in determining its investment appeal. Leveraged firms, like HOV, often exhibit heightened sensitivity to variations in discount and growth rates. While quantifying this sensitivity can be challenging, a brief sensitivity analysis can show how intrinsic value responds to these rate changes. In my view, a silver lining in HOV's valuation is its historically consistent revenue stream. Although not a growth juggernaut, it has achieved a commendable 5.2% CAGR in revenues since 2013 , largely buoyed by the post-2008-2009 financial crisis recovery.

However, 2023 has shown unmistakable signs of a decelerating housing market. This slowdown, coupled with HOV's sizable $934.8 million net debt, is cause for investor caution. Yet, it's worth noting that with a TTM interest expense of $55 million, HOV's estimated TTM FCFF stands at approximately $270 million. Furthermore, given that HOV's EBIT margins have historically ranged between 6% and 13%, even a hypothetical 50% revenue drop and EBIT margin contraction to 6% would result in an EBIT of about $82.7 million. This amount is sufficient to meet operational costs and interest obligations.

{kind=link}

Analyzing HOV's financials , it's evident that the interest rates on their nonrecourse mortgage loans, secured by assets valued at $418.9 million, have surged from 4.4% in 2021 to 6.7% in 2022. Similarly, long-term debts maturing in 2026 already command interest rates as high as 10.10%. This pattern, combined with HOV's alignment to benchmarks like SOFR and BSBY, which are influenced by broader economic dynamics and central bank policies, underscores a shifting financial landscape. In my view, given the rates on HOV's senior secured notes, which range between 7.75% and 11.25%, and future potential Federal Reserve hikes, forecasting an interest rate bracket of 8% to 15% for HOV's financing is reasonable. For modeling purposes, I'll anchor my projections at a base rate of 12%, incorporating a sensitivity analysis to cater to potential variances.

Author's elaboration

Diving deeper into the valuation, I've crafted a sensitivity analysis for my DCF model. The outcomes reveal that contingent on varying growth rates (0% to 6%) and prospective debt interest rates (8% to 15%), the company's potential appreciation could soar to a staggering 423.8% above current levels or decline by 40.4%. Based on these findings, I believe the company's intrinsic value likely lies between $1 billion and $1.5 billion. When juxtaposed with its market capitalization of $575 million, the company presents a compelling investment opportunity at its current valuation.

Main Factors for HOV's Undervaluation

However, a couple of reasons could cause this value disparity. First, the Hovnanian family, led by Ara K. Hovnanian as chairman, president, and CEO, holds significant sway over the company. Together, they control approximately 58% of the voting power as of October 31, 2022. This consolidated influence, amassed through personal holdings, family trusts, and other entities, grants them the authority to steer key decisions, from board elections to stockholder matters. I think this dominant position, while underscoring the family's dedication, also implies that a shift in ownership is unlikely. This could limit opportunities for activist investors or M&A initiatives that benefit retail shareholders.

In fact, Ara's deep-rooted association with the company began in 1979, leading to his CEO role in 1997 and further solidified after succeeding the company's founder, Kevork S. Hovnanian, as Chairman in 2009. The family's ties to the company extend beyond leadership roles; for instance, a firm owned by Tavit Najarian, a relative, has been a service provider. Ara's son, Alexander, holds a significant position as Executive Vice President of National Homebuilding Operations. It's essential to ensure transparency and balance the interests of all stakeholders in such a scenario.

HOV's financial indebtedness could also influence its perceived undervaluation. As of July 31, 2023, HOV held nonrecourse mortgage loans amounting to $129.1 million, backed by properties worth $373.1 million. The company's obligations under its Master Repurchase Agreements further highlight this. Specifically, the outstanding borrowings under the Chase and Customers Master Repurchase Agreements stood at $6.3 million and $37.7 million, respectively. Delving deeper, HOV's senior notes and credit facilities paint a picture of a highly leveraged company, with the latest quarterly figures revealing approximately $1 billion after accounting for discounts, premiums, and unamortized debt issuance costs.

I believe such a significant debt level can raise eyebrows for investors for several reasons. Primarily, it suggests that a large chunk of HOV's future earnings might be channeled toward debt servicing, possibly sidelining dividends or reinvestments. Moreover, in a climate of escalating interest rates, the expenses tied to variable-rate debt could rise, potentially narrowing the company's profit margins. Additionally, a hefty debt load can curtail HOV's agility in seizing growth avenues or navigating economic challenges. While leveraging debt can be a strategic move for growth, it undeniably brings an element of risk.

Conclusion

Hovnanian Enterprises, Inc. has adopted a commendable approach in the homebuilding sector, consistently achieving growth despite industry challenges. This, in my view, is indicative of its robust operational strategies. On the other hand, potential investors should be cautious of HOV's substantial debt and the Hovnanian family's dominant stake in the company. These factors could introduce certain uncertainties. Based on my valuation analysis, I believe that HOV is currently undervalued. However, the concentrated ownership does add an element of unpredictability. Despite this, considering HOV's longstanding history and current valuation, I think the stock presents a potentially attractive investment opportunity at its current price levels.

For further details see:

Hovnanian's Valuation, Ownership, And Debt Concerns: Is It A Viable Investment?