KDP - How About Another Dr Pepper? It's Still A 'Buy'

Summary

- I wrote about KDP, or Keurig Dr Pepper back in June of last year, establishing my foundational thesis and PT. I bought some shares as well.

- The company has performed quite decently, being up above market for most of the time, and ending at a close to 3% outperformance for the year.

- I'll revisit KDP here and show you why I might include it in my "basket" of stocks that I'm buying in the next few days.

Dear Readers/Followers,

My stance on Keurig Dr Pepper ( KDP ) is relatively new. I follow beverage companies, including PepsiCo ( PEP ) and Coca-Cola ( KO ) as well as their respective bottlers like Coca-Cola Consolidated, Inc. ( COKE ) closely - and I own some in most of them. Not outsized positions by any means - they haven't been cheap enough to really establish a massive stake, but positions nonetheless.

These consumer staples make for a good investment with conservative dividends, but low downside. It's one of those companies that you "hope" will drop more because, what's going to happen to them? People are going to suddenly stop drinking soda?

They may not be growth monsters - but they're safe. Let's revisit KDP and see what we have here.

Revisiting Keurig Dr Pepper

As I said in my initial article, the company's namesake soda is relatively unknown outside of the US compared to other, even local brands of soda. Of course, Dr Pepper is really only one of the company's many brands, and there is a lot more to this business (and why it is attractive), than just Dr Pepper.

Green Mountain Coffee Roasters and Keurig Green Mountain was, as brand suggests, a Coffee and beverage maker which together with Dr Pepper Snapple formed into the KDP conglomerate in 2018, with headquarters in the US. It employs over 27,000 people.

{kind=link}

More importantly, it has a portfolio of some 100+ hot and cold drinks and as the name suggests, also contains the entire Keurig brewing system. So when investing in this company you really have the opportunity to get exposure to great coffee, which isn't all that easy, except if you consider businesses like Nestle (NSRGY). Most of the coffee companies that I like aren't actually publicly traded.

So the mix today is coffee, hot cocoa, teas, and other beverages under brands for its Keurig brewing machines, plus sodas and juices. It's really one of the most "complete" drink/beverage companies that I know of, and one of the most appealing.

{kind=link}

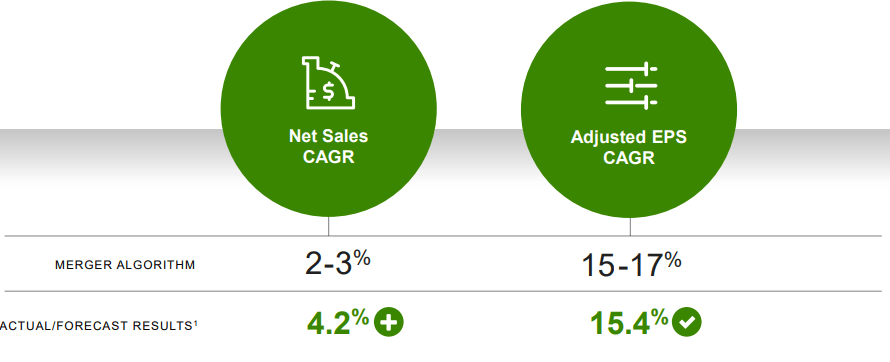

KDP has been able to perform significantly above the peer average since its IPO. It's transforming into what it views as being a "modern beverage company", delivering solid EPS growth while accelerating revenue beyond expectations. Merger forecasts called for sales growth numbers of 2%-3% annually. Actual results have proved well beyond that at over 4% and have also delivered closer to above 15% EPS growth CAGR. Those are not in any way bad or unattractive results, especially in this market.

Still, it remains very U.S.-centric.

KDP IR (KDP IR)

While you can get a Keurig machine here for instance (on Amazon), we're much more used to Nespresso, Tassimo, and other brands and platforms - I myself use Nespresso for my away-from-home coffee and a manual espresso machine at home. Keurig just isn't well-known here.

Beverage markets are, for the most part, incredibly high-moat markets with plenty of crushing costs, shelf space challenges, and other retail-based headwinds that make breaking into the market hard. My choice has always been for the established players that in turn buy up smaller companies that "make it", thus improving their portfolio quality and appeal. That's why I own all 3 majors, but rarely focus on smaller businesses in this segment. The risks are simply too high.

Meanwhile, KDP risks are "limited" really any way you look at them - at least how I see it. The company's growth engines enable it to really "get into" households, with Keurig machines already in 21 million US households back in 2015. That number is up to 33M in 2020 and is expected to rise to beyond twice that going forward.

The non-Coffee beverage portfolio is definitely a performer as well. Take a look at the basics of this portfolio.

KDP IR (KDP IR)

Without exaggerating, I believe this to be a portfolio you want to be a stakeholder of. The company seems to cover the entire beverage spectrum with the exception of alcohol (a whole different beast to get into), and what they have is incredible, as I see it.

Keurig might not be as diversified as Nespresso when it comes to the selection and luxury of its coffee. If you look at some of the latest capsule innovations coming out of Nestlé headquarters, it puts competitors to shame, but it's still a very solid player that either owns, licenses or partners with most of the major coffee companies in the world, and that includes Swedish ones.

KDP is close to future-proof as I see it. People will continue to drink coffee and soda as well as the company's portfolio of drinks, and I view KDP as perhaps the best-positioned player in this entire space, even if it's not the biggest. Like the other soft-drink giants, it trades at a significant premium, but there's a good argument to be made as to why the company is actually worth it, with a higher growth rate than most of the incumbents.

The company reaffirmed the 2022E numbers as late as December 5th. The latest results we have to consider are 3Q22 results, and those came in at very strong levels. The company delivered net sales increases of in the double digits - same for 9M/YTD YoY. it's really an "all-weather" portfolio that while having some exposure to sugared drinks, to coffee, and to teas, has a very good balance unlike say, Coke.

That isn't to say macro isn't challenging. The company is impacted like any other business by the cost increases in raw materials. There was also a massive disruption in the coffee business that has more or less turned around and is showing very good trends going into 4Q22.

All of the company's segments saw impressive growth during the third quarter. Much of it was increased prices that the company, like most other staples businesses, is successful in passing onto consumers.

The fact that GAAP operating income is down 50.4% YoY reflects the aforementioned non-cash impairment on Bai. Gross profit was up though, even though there were inflationary pressures and increased marketing spend. Adjusting for non-recurring, adjusted operating income was up 2%, which came mostly from an 8.6% increase in adjusted gross profit - but pressured by transportation costs, warehouse costs, inflation impacts, labour costs/wage and marketing.

There isn't, to my mind, anything worth mentioning in this quarter's results that could negatively bring the company down, as I see it.

So let's move on to valuation.

Keurig Dr Pepper Valuation

The company's peers remain obvious and aforementioned - but it can also be compared to alcoholic beverage companies, though these tend to trade at somewhat different multiples.

It's mostly Coca-Cola, Pepsi, Anheuser-Busch ( BUD ), Monster ( MNST ), Diageo ( DEO ), Constellation Brands ( STZ ), and other companies that work in the beverage sector. I argue also that we could compare it to bottling companies to see whether we want to own bottlers or manufacturers - in this case, I own a bit in both bought during various times, and it's all about that valuation appeal.

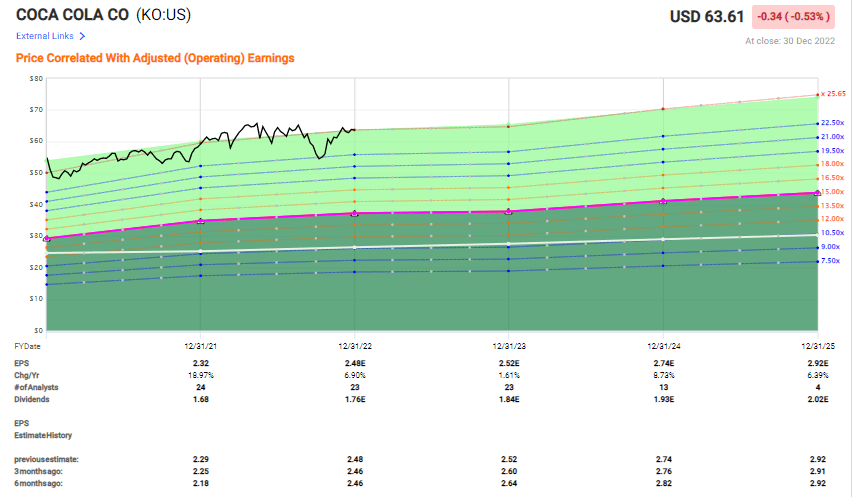

In my first article, I made it clear that I view KDP trading at a discount to most everything except the then-pressured alcoholic beverage companies. The average weighted P/E is up to around 21.17x at this particular time. In terms of P/E, this is still below par compared to most of the incumbents. Take Coca Cola for instance.

KO trades at closer to 26x P/E and has a significantly smaller growth profile for the next few years, but essentially the same yield.

{kind=link}

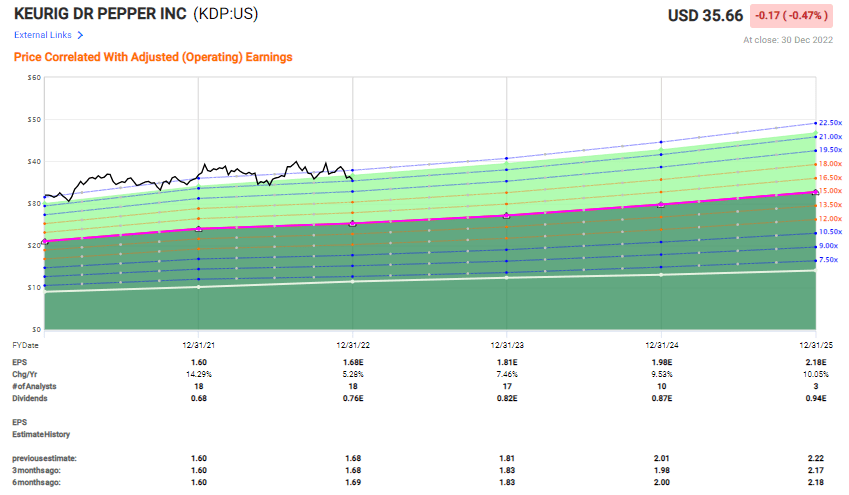

Pepsi is even worse, coming in close to 27x. Now, both of these incumbents are A+ rated in terms of credit - KDP is "only" BBB. Does that mean that the variation is justified?

I would argue that it is not. The variation of 1-2x P/E I could understand, and even agree with, but 5-6x is too much - and not justified given that KDP has significantly better growth prospects - double digits/high singles for the next few years, or close to, averaging at almost 9% per year until 2025E.

{kind=link}

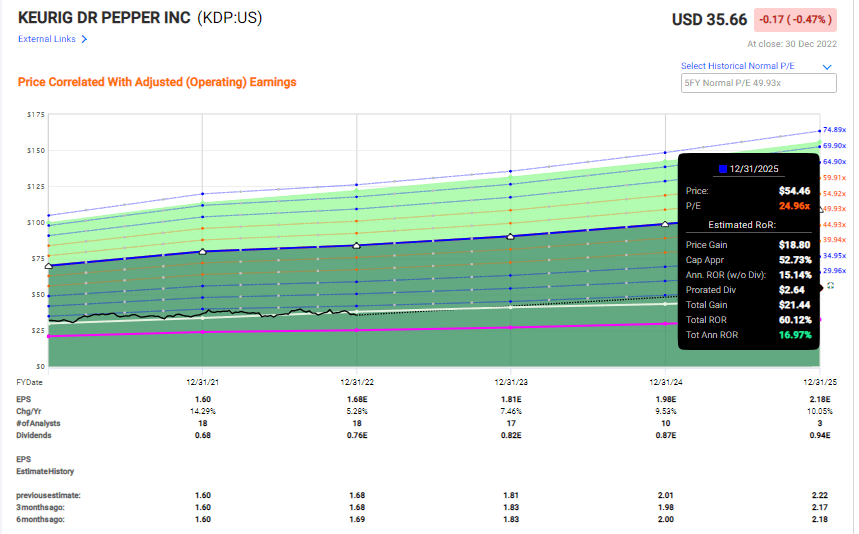

If we assume that the average justified premium in the industry is around 25X P/E, which is around the target given by peers, then the company currently has an upward trajectory of almost 17% annually until 2025.

{kind=link}

Potential downside? Sure, it exists. Is it realistic that we see it decline consistently for a long, long time?

I continue to say no to this possibility. The company is very rarely below a P/E of 20X, and when it is, it bounces back quickly - so any decline that's not foreshadowed by massive fundamental troubles should be viewed as a strong "Buy" indicator for this business.

Remember, these potentials are very likely based on historical accuracy. Analyst forecasts for this company and its predecessors are 100% on point or beaten positively. There is no negative miss with a 10% margin of error in this company's history. This comes to a very secure forecast-based upside in the business and in the stock.

The combined appeal of a cold beverage/tea/soda/water portfolio, coupled with its extremely attractive, already-market-leading Keurig Coffee portfolio, the company is likely to be able to deliver "alpha", outperforming the market on a real TSR (Total Shareholder return) basis.

KDP shareholders won't become millionaires unless they prior to investing in KDP are already millionaires. It's not that type of stock. What you're looking at here is a 15%+ average annual RoR. No matter how you slice that possibility in today's market, that's something that should be viewed as an attractive prospect here - at least for conservative dividend investors.

Thesis for the common shares

- KDP is a fundamentally appealing coffee and soft drink company, with an appealing portfolio of waters, teas, beverages, and coffee systems beloved by many and #1 on the market. Fundamentally, the company is very attractive.

- KDP is one of the more attractive BUYs in the entire sector given its lower valuation not only in P/E multiple, but sales, EBITDA, and EBIT when compared to some of its closest peers.

- I give the company a $40/share price target and start out watching KDP with a "Buy".

Remember, I'm all about:

1. Buying undervalued - even if that undervaluation is slight, and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn't go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them.

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

While you may view it as somewhat extreme to consider a 21.1x P/E beverage company as "cheap", I point you to the peer averages for the company's real competitors. There is value here, and you should not disregard it.

However, some options do exist here.

Options possibilities for Keurig Dr Pepper

There do exist some option potentials for KDP - though I would caution you that most of these is essentially saying "I want to buy and I expect to expire ITM, I just want a better price", as opposed to making a purely-oriented premium play with good annualized yield.

KDP Option (Author's Data)

This represents the farthest out I'm willing to go with a PUT - around 100 days, and 7% annualized isn't all that great, but it's a great price for KDP, with $31.35 if you include the premium. And if it really doesn't drop, that's fine too. I can understand if you feel that 7% isn't enough - my own personal minimum for puts is 8.5% annualized, including the risk-free rate for whatever cash I'm putting on the line and not having to put in straight away.

You could go for the 33 strikes - that would up the return to 8.67% based on the data I'm currently able to pull outside of market hours - but the higher you go, the quicker you're likely to be ITM.

It's a decent/acceptable PUT option, and I might write this one or one close to it. The capital outlay is also conservative, as far as options go.

As we're looking at the market today, it seems that the first day is going to be a positive one - that usually doesn't bode well for writing Puts, but we'll see what happens.

For further details see:

How About Another Dr Pepper? It's Still A 'Buy'