KKR - How Brookfield And Peers Make Money And How You Can Participate In 2023

Summary

- Big alt managers include 6 companies but 7 stocks. Brookfield Asset Management Ltd. is now represented by two stocks - asset-heavy BN and asset-light BAM.

- The industry is attractive because the capital supplied by clients remains locked for many years in private funds providing a stable stream of "sticky" and relatively high management fees.

- The industry has grown at 20% for many years and is expected to continue similar growth at least for the next several years.

- Due to its unique profile, BAM appears to be very appealing. BN seems less appealing as some of its capital is not efficiently allocated.

I have authored quite a few posts on Brookfield Asset Management Ltd. (BAM) and its related companies. But they are designated for people who are already familiar with the complex world of private equity and alternative asset managers.

This post is completely different. It is for those investors who are curious about Brookfield and sense related opportunities but need help to start their journey. You do not need to know much to understand the content.

There is an additional benefit to this. Once you understand Brookfield, you will also understand its peers - Blackstone ( BX ), Carlyle Group ( CG ), Apollo ( APO ), Ares Management ( ARES ), and KKR & Co. ( KKR ). This article includes some information about them as well. Together with Brookfield, I will call these companies the Big Six of alternative asset management. Several of them have beaten the S&P 500 Index (SP500) on a multi-year basis. Some of them are also paying generous and quickly growing dividends that retirees find irresistible.

Until recently, Brookfield's parent company was called Brookfield Asset Management represented solely by the well-known ticker BAM. It is different now. The parent company is called Brookfield Corporation ( BN ) and BAM is one of its subsidiaries (I will explain the details later). We will use Brookfield and BN interchangeably. What follows is a manual on Brookfield and its peers with more emphasis on the former for the reasons that will become clear in due course. I will intentionally oversimplify my story to make it more digestible.

Alternative assets

Almost everybody is familiar with traditional asset managers such as Vanguard. These companies manage stock, bond, and money market mutual funds and/or exchange-traded funds ("ETFs") charging small fees for this. For some index funds/ETFs, these fees are measured in hundredths of a percent of investors' balances. They can go higher but are typically well within 1%. Both mutual funds and ETFs are liquid. Investors can easily sell their holdings almost anytime.

Alternative (or alt) asset managers are different. The word "alternative" means that the assets they manage are different from public stocks, bonds, and cash instruments. This is true in most but not all cases. For example, Brookfield has a traditional mutual fund business as well but it is rather small within the company.

The best-known alternative asset is private equity, which implies owning a company that is not public. From time to time, BN acquires a public company making it private, improves it one way or another, and sells it several years later to a buyer or through an IPO at a higher price pocketing a profit. Most alt managers started their business from private equity activities and the industry is still called private equity sometimes. But this term is misleading today. Alt managers have increased their scope dramatically and private equity is nothing more than a segment.

Another familiar example of an alternative asset is real estate. BN has giant non-public real estate operations, developing and managing different types of properties starting with storage facilities and ending with skyscrapers in downtown New York, London, Berlin, Toronto, and Sydney. And everything in between.

One other type of alternative asset is private credit. Loans that banks carry on their balance sheet are examples of private credit. But typically this term is reserved for non-bank loans. Since the Financial Crisis of 2008, banks have become strictly regulated and limited their activities. Alt managers used this opportunity to increase their lending operations taking market share from banks. Differently from banks, they often pursue riskier loans. They also operate in distressed and high-yield debt which can be public or not. Oaktree, one of Brookfield's subsidiaries (Brookfield owns 64% of it), is a recognized expert in these operations.

Two popular alternative assets today are infrastructure and renewables including building and operating toll roads, ports, oil and gas assets, airports, solar, wind, and hydro energy facilities, and so on. Brookfield is leading here and this is, perhaps, the most exciting part of its business.

There are many other types of alternative assets such as venture capital, hedge funds, and cryptocurrencies, but they are not important for Brookfield nor for most of the other Big Six (for Blackstone though, hedge funds represent a separate segment).

Since alternative assets by definition are not being traded on public markets they are relatively illiquid. It may take years to improve a piece of real estate or to turn around a company and sell them. The illiquid nature of alternative assets requires patient capital.

How alt managers source capital

For purchasing assets, alt managers can use their capital and/or raise capital from third parties. Some alt managers use very little of their capital in investments and are called asset-light. Others, like Brookfield, are asset-heavy and may supply 15-25% of their capital per investment. This is called the alignment of interests between an alt manager and third parties.

Alignment of interests is an effective tool to attract third parties, but surprisingly it is less important than it seems. The biggest company in the industry is Blackstone and they are asset-light contributing only about 0.5% to assets under management ("AUM"). Blackstone has established a remarkable track record, particularly in real estate, and this track record - a unique intangible asset - appears more important than a significant alignment of interests.

Since alt operations need patient capital, only institutions with long-term investment horizons can supply it. Or at least that is how it was in the beginning. Please note that the industry is fairly young and quickly evolving. For example, more than a century-old Brookfield entered it only in the XXI century. Blackstone started a decade earlier.

So what institutions have the longest investment horizon? Pension plans, endowment funds, and sovereign wealth funds. These institutions became the first clients of alternative asset managers.

Clients' contributions are aggregated in so-called private funds which are measured in billions. Private funds get closed once the manager receives enough money for its plans. These monies remain locked in the fund until it is wound up 5-7 (or even more) years later. At this point, initial contributions with profits are returned to clients.

Legally, funds are limited partnerships, with the alt manager being the general partner. General partners typically contribute 2% of the funds' capital but control all operations. Clients become limited partners and supply almost all capital but have no say in operations. Asset-heavy managers like Brookfield contribute additional capital to the funds and become limited partners on top of being general partners.

Once the alt manager invests all money in the fund but long before it is wound up, the alt manager starts raising money for a new fund of the same strategy. The word "strategy" is very important here. Alt managers have developed tens of different strategies. For example, there might be one fund for private equity, a different fund for real estate, and so on. Moreover, these strategies are subdivided further fine-tuning to clients' profiles and preferences. In real estate, for example, there are risky funds with target returns of 20% per annum (so-called opportunistic funds) and much safer plain vanilla funds with target returns of 7-8% (core or core-plus funds).

Combining all this, alt managers handle simultaneously a lot of different funds that vary in strategies and vintages. To deal with fundraising, managers form sales teams that approach clients all over the world directly or, sometimes, through intermediaries. Sales teams are often completely decoupled from investment teams and are critical for alt managers.

Clients are paying close attention to the track record of an alt manager and track their experience with this particular manager. Initially, a giant pension fund can trust an alt manager with a small slice of its money for a particular strategy. Provided this experience is successful, the same pension fund can commit more money across several strategies. Currently, the Big Six have hundreds of big clients worldwide each, and many invest in multiple strategies.

Private funds sourced from institutional clients have been the major source of capital for all alt managers. But now all of them are quickly expanding their offerings to individuals and affiliated insurers trying to reach scale. Some have already succeeded.

Individuals can invest in Brookfield's three public subsidiaries: Brookfield Infrastructure Partners ( BIP , BIPC ), Brookfield Renewables Partners ( BEP , BEPC ), and Brookfield Business Partners ( BBU , BBUC ). Each of them exists in partnership and corporate forms that differ only in taxation (the letter "C" in tickers designates corporations). These subsidiaries provide capital to Brookfield private funds and if a retail investor buys a unit/share, she indirectly becomes a limited partner in several private funds at once. Since subsidiaries are public, individuals do not have to lock their capital for many years and can sell units/shares anytime. The volatility of public vehicles becomes the reverse side of their liquidity. Several alt managers have similar vehicles.

However, some wealthier individuals are ready to forego liquidity in pursuit of higher returns. Until recently, they could not do it via alt managers, but this is changing. Blackstone was the first to offer non-traded real estate investment trusts ("REITs") and a credit vehicle to individuals via independent distribution channels (banks, broker-dealers, etc.). Brookfield and others are replicating this strategy now. For these vehicles, alt managers limit the aggregate amount that investors can redeem - say, not more than 5% of assets per quarter. Under normal conditions, these vehicles seem liquid. However, when many investors want to exit simultaneously due to some financial stress, the vehicle quickly becomes illiquid. It recently happened with investors in Blackstone non-traded vehicles and may or may not have consequences for the industry.

Working with affiliated insurers is the latest big trend for alt managers no doubt inspired by Apollo's example. The idea is rather simple in theory. Certain types of insurance products, such as fixed annuities, are long-term in nature. An insurer faces a payout many years after receiving money from an individual (or a company in the case of a group annuity) which makes annuities suitable for funding private credit. This channel is already working remarkably well for Apollo. Brookfield is in the process of building its insurance subsidiary which is expected to contribute to assets under management at scale quite shortly.

Fees

Without much exaggeration, alt managers are about fees. For asset-light managers, fees, in one form or another, dwarf everything else. Asset-heavy managers can also count on returns on their capital and nevertheless fees are the most reliable and valuable part of their business. This is true about asset-heavy Brookfield. Apollo might be the only exception, as giant insurance subsidiary Athene prints money with amazing reliability and grows quickly.

Alt managers are overly creative with introducing various fees. Still, slightly simplifying, all fees belong to two broad categories: management fees assessed on AUM similar to mutual funds and performance fees dependent on beating specific performance targets within funds (much smaller advice and transaction fees are grouped with management fees).

Alt managers charge rather high management fees that typically start with 1% of AUM. Since they are charged quarterly and the private funds are illiquid and "sticky," with a long duration (or even permanent in certain cases), management fees are continuous, recurring, and predictable.

Performance fees are fickle. Some of them are assessed periodically but can be zero if investment targets are not reached. Others (carried interest or carry) represent a slice of investment gain/income received by an alt manager only when a fund is wound up provided its investment performance is above a certain hurdle rate.

While lumpy and not guaranteed, performance fees can be quite big. For some alt managers, they are more important than for others. For Brookfield, Apollo, or Ares, they are small compared with management fees while for Blackstone or Carlyle they are comparable.

Importantly, performance fees are in sync with market cycles. When markets are doing good, performance follows. Management fees, on the contrary, are mostly independent of the markets and deliver in both good and bad weather.

Asset under management

AUM is the single most important metric for all asset managers as it is directly related to the size of fees. Unless you believe that alternative AUM will grow at a high rate, there is no reason to invest in alt managers. The inverse statement is also true: as long as alternative AUM grow fast, there is little risk of losing money investing in the Big Six.

The AUM growth is controlled by both supply and demand. Supply denotes assets in dollar terms that could be turned private provided funding is available. The total amount of alternative AUM today is estimated at ~$13T with 40% of it in private equity. This figure should be compared with the global public equity market cap of ~$95T and the global bond market of ~$106T. Bruce Flatt, Brookfield's CEO, indicates that renewables alone will require ~$100T+ investments over the next 25-30 years on top of it. This list does not include infrastructure assets that are going to be built or privatized, real estate, or natural resources. These figures show that the growth of alternative AUM is hardly limited by supply. What is important to realize, however, is that the Big Six are expected to benefit disproportionately from this growth. First, an alt manager needs a big network of offices and professionals to select the most promising opportunities from the abundance. And secondly, big transactions (which are often the most lucrative) are simply out of reach for smaller players. For example, recently Brookfield joined forces with Intel ( INTC ) to provide $30B for building a chip plant in Arizona on a fifty-fifty basis. How many companies in the world can quickly accomplish due diligence and commit to a check for $15B?

Let us turn our attention to demand now. It exists because alt managers deliver higher returns for their clients AFTER FEES. While it does not happen always, it is generally the case. Otherwise, sophisticated clients, like insurers or endowment funds, would not be increasing their allocations to alts.

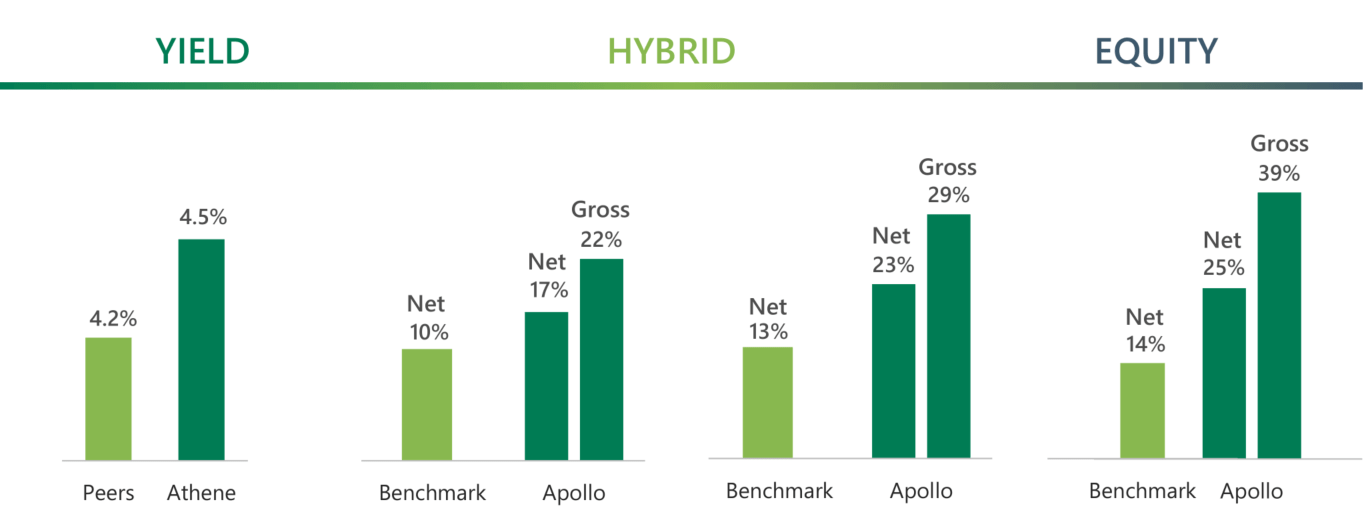

The slide below displays returns generated by Apollo for different asset classes (other alt managers present similar slides). Yield is investment-grade private debt, equity is private equity, and hybrid is everything else. Net returns indicate what clients received after fees.

{kind=link}

When we talk about investment companies, Berkshire Hathaway ( BRK.A , BRK.B ) is always the first to come to mind. But how many people are managing investments at Berkshire? I am aware of four. A big alt manager employs hundreds of investment professionals spread around the world that are sifting through hundreds of investment opportunities in different industries, geographies, and asset classes. Only a small fraction of opportunities is selected for investments and leverage is applied to those few chosen.

Since investment professionals within the Big Six are paid extremely well, investment talent is flocking there. It is similar to how Google attracts programming talent. Blackstone reported that for the analyst class position in 2018, only 86 were hired out of 14,906 applicants. The scale and quality of investment talent represent the second major intangible asset of big alt managers.

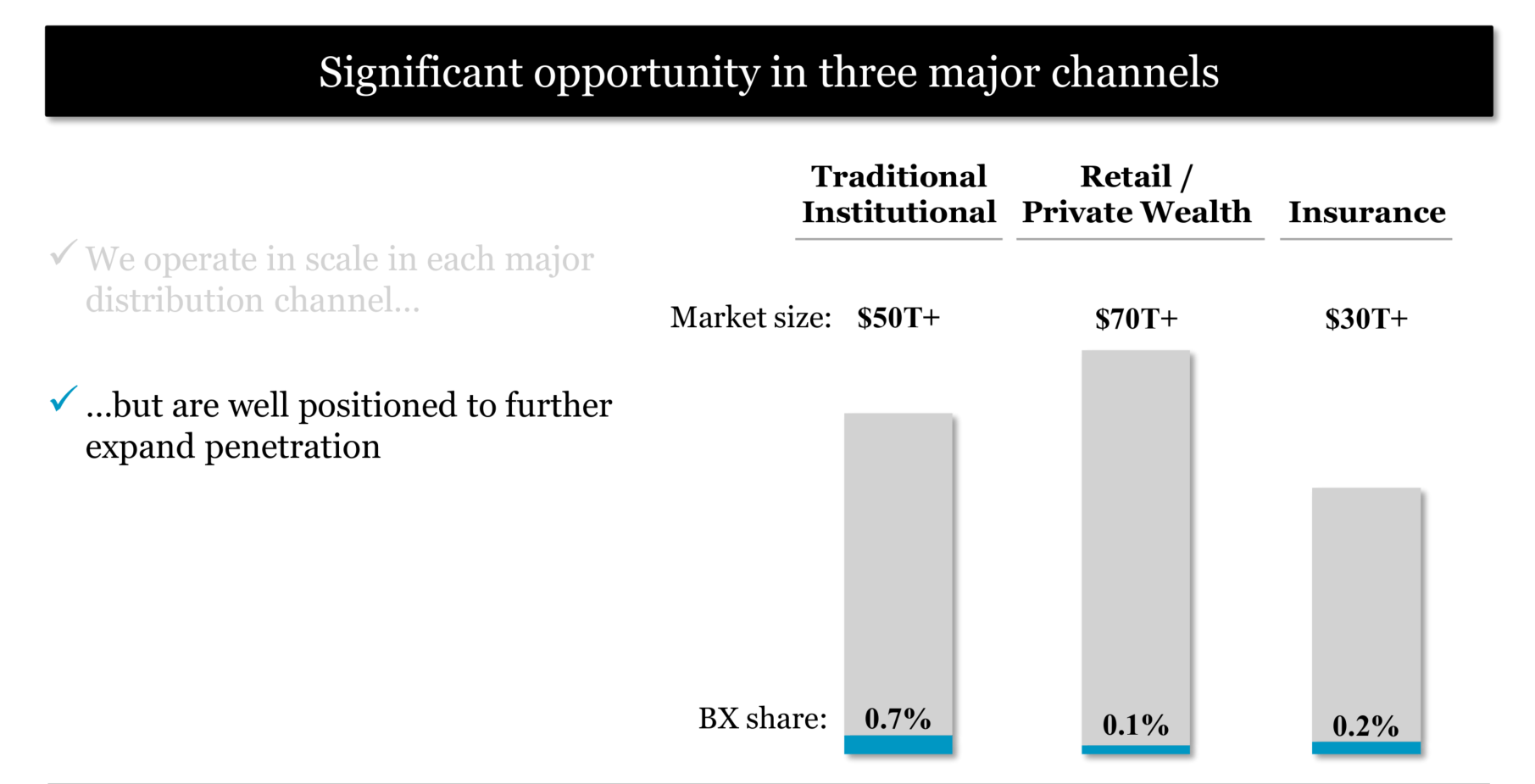

During its last Investor Day in 2018, Blackstone outlined the potential demand for alternative assets:

{kind=link}

The same figures today are, perhaps, 1.5-2 times higher. Importantly, the Big Six together are within 2% of the total size for each channel. There is plenty of room to grow, but demand for alts is still more limited than supply.

The crucial figure is the growth rate that alt managers have achieved. Let us take Brookfield: on Jan 1, 2018, its fee-generating AUM were ~$125B. At the end of Q3 22, they were $356B (prorated for the partial ownership of Oaktree). It translates into more than 23% CAGR. And other alt managers have reported similar results of 20%+ annual growth in AUM.

One reason for this growth is a higher allocation to alternative assets by big players. Harvard and Yale endowment funds, two of the smartest institutional players, currently allocate close to half of their AUM to alternative assets. And they are beating their peers with lower allocation. Affluent individuals, on the contrary, allocate less than 10% of their wealth to alts.

Since we are far from saturation both on supply and demand and since alternative assets deliver, we do not anticipate slowing the growth of AUM within the next several years. Currently, all of the Big Six are planning their growth at about 20%.

Brookfield's place in the industry

So far, my story has been more or less objective albeit simplified. From now on, it will include my subjective opinions and preferences.

Even though we are dealing with six companies, we should consider seven stocks since Brookfield is represented by BN and BAM. BAM is an asset-light manager that is 75% owned by asset-heavy BN. This structure has been around for only a couple of weeks and we can only speculate about how it will unfold.

BN and BAM combined represent the second largest (after Blackstone) company within the industry but several others are very close. In terms of PR, though, Brookfield must be number one. It is quite clear even from the number of publications devoted to it on SA. This is intentional as the management is equally adept in investing and marketing. Brookfield holds annual Investor Days, while the last Blackstone Investor Day occurred in 2018.

Let us try to make some qualitative conclusions about the industry delaying valuations until the next section. I generally prefer asset-light managers vs asset-heavy for several reasons. First, they are much easier to understand, analyze and value. Secondly, their earnings represent pure free cash flow with almost all of it being paid out as dividends (90% for BAM, 85% for Blackstone, and similar for Ares). It is not the same for asset-heavy managers having other uses for their cash flows. Thirdly, capital, sometimes, is not allocated efficiently. For instance, some of Brookfield's real estate assets (weaker malls, in particular) are underperforming and the company is trying to reduce its real estate footprint.

Having said this, I consider Apollo an exception as almost all of its capital is committed to insurer Athene, a retirement specialist, which is very efficient.

I also prefer managers with big management fees (vs performance fees) as these fees are stable and predictable.

BAM and Ares are the only asset-light managers focused primarily on management fees. Between these two, BAM has two important advantages. BAM's strengths are in renewables (including net-zero transition) and infrastructure where both supply and demand are the highest.

BAM's other advantage is having the support of its parent BN. Due to Brookfield's unique structure, BN commits its capital to BAM's funds achieving a material alignment of interests that no other asset-light manager can enjoy.

Based on all this, BAM appears the most promising stock in the industry. It has another subtle advantage of being a Canadian company which is often looked at more favorably internationally.

Even apart from valuations, this line of thinking, however, is open to challenge. For example, Ares, a credit specialist, is the smallest of the Big Six which makes growth easier. I also like that it is less known (compared with others of the Big Six) as value is often found in less crowded places. Surely, KKR and Carlyle have their own fans as well.

Valuations and dividends

Despite all the internal complexity of alt managers, the investment thesis appears disarmingly simple. It is especially so for asset-light managers.

Since asset-light managers are paying almost all their earnings in dividends, their yield becomes an important metric. Let us consider the biggest of them - Blackstone. Over the last twelve months, it paid out $4.94 in dividends which translates into a 4.94/74.94 ~ 6.6% yield.

If AUM keep growing at 20%, fee revenues should grow at a similar rate. Fee-related earnings ('FRE') may grow even faster because of margins expansion due to scale and almost all of FRE (85% per Blackstone's policy) will be paid out. Do you know many other opportunities to buy a 6.6% yield with an expected growth of 20%?

Other asset-light managers are not far behind. Ares, for example, is trading at a 3.6% yield but it will raise its dividend in about a month. The last raise, in early 2022, was for a whopping 30% in line with our estimated FRE growth. And do not think it was a quirk. In 2021, the raise was 25%.

Finally, BAM is trading at a $1.28/28.04 ~ 4.6% and this high yield is sourced exclusively from "sticky" management fees with the same expected 20% growth.

These opportunities remain salivating even if we assume lower growth in AUM, say, only 10%. In the next section, we will try to explain why these opportunities have emerged. Meanwhile, please note that similar opportunities were available before and ended up in the achieved ~20%+ in total return. In 2018, Blackstone was trading in mid-thirties and at ~6% yield. The stock has more than doubled since which translates into ~16% annual appreciation plus a 4-6% dividend.

It is more difficult to analyze asset-heavy managers because they are more complex. Besides, Brookfield and Apollo reorganized themselves in 2022 (Brookfield - in mid-December and Apollo on Jan 1) and Carlyle is going through a top management change. In my opinion, Apollo seems particularly promising for the reasons I already explained.

Risks and controversies

It is time to visit the dark side. In general, alt managers are not particularly liked by the public and it may partially explain their valuations. Many people consider them ruthless and overleveraged predators that make their accounting opaque and inflate their private funds' returns.

This reputation stems primarily from private equity operations with their leveraged buyouts. The slogan "Barbarians at the gate" referring to one of KKR's buyouts is still well-remembered.

As mentioned before, private equity is nothing more than one segment of alt managers' business today. Private debt, insurance, infrastructure, and renewables do not have this negative connotation.

But how about leverage? Are alt managers really that leveraged and risky? They indeed use a lot of leverage but this leverage is non-recourse for the managers themselves. The parent companies carry either a small amount of debt or none at all.

Let me illustrate that with a simple business case. Imagine you want to enter rental operations and have enough cash to buy one rental property without any debt but can also receive a cheap mortgage. Perhaps the best course of action is to buy, say, 3 properties putting 20% down for each leaving 40% of your initial cash as a cushion for possible misfortunes. If everything goes well, you can buy the fourth property with 20% down and still retain plenty of cash from your initial savings and the newly-established rental cash flow. With time, you may own multiple rentals and your position becomes highly leveraged. But is it risky? Not so much because you always keep a cash cushion and enjoy positive cash flows from many independent rentals. Even if one of your projects fails, your risk remains limited to this particular property and you cannot lose more than this property. The leverage is non-recourse to you.

Alt managers utilize a similar structure. They use leverage to produce better returns in each project (be it acquisition, property, or something else) but the risk remains contained and isolated within this project. Moreover, asset-light managers have a negligible risk of losing their capital due to leverage because they invest negligible capital to start with.

Let us move to the next scarecrow. Are alt managers so complex that it is impossible to understand their financial statements? This is true as long as one means GAAP (or IFRS in Brookfield's case) statements. Since alt managers control private funds, they have to consolidate them in their statements even when their investments in these funds are negligible. Alt managers control tens of funds and each fund acquires, turns around, runs, and sells at least several companies (or properties, renewables, pipelines, etc.). Consolidating many companies of different types and at different stages of their life cycle makes GAAP statements mostly unreadable. So each manager publishes non-GAAP statements that exclude these investees and emphasize primarily fees. These statements are not so difficult to understand especially for asset-light managers and they are reconciled back to GAAP statements.

Some people accuse alt managers of inflating their funds' returns to attract "naive" pension plans. This point of view was popularized in the recent book "The Myth of Private Equity" . The book is entertaining and I enjoyed reading it but cannot agree with the author. Due to bureaucracy and politics, some pension plans are not the most sophisticated investors. But I doubt anybody can state the same about other clients such as big endowment funds and insurance companies. And not all pension plans are "naive" either. The total number of alt managers' institutional clients today is likely slightly short of 10,000 worldwide and some of them are the most knowledgeable investors. Alt managers cannot reach this scale without outperformance.

Some alt managers are firmly linked to their founders. For example, Blackstone is associated with Stephen Schwarzman, Carlyle with David Rubenstein, and Apollo with Leon Black even though the latter is not in charge any longer. When Leon Black got entangled in bad publicity last year it was immediately reflected in Apollo's stock price. Never mind that this publicity had nothing to do with the company and that all big alt managers are dependent on big teams of investors rather than on one personality.

Now, let me talk about risks that I consider real. The first of them is extreme volatility. Here is an example: in early 2022, Blackstone was trading at about $130, while now it is about $75. Nothing particular has happened with the business (I would not overestimate the recent case of illiquidity of their non-traded vehicles as all alt funds are illiquid and it was well-known). The slide has been mostly due to the decline of the stock market and climbing interest rates. This is not an isolated event. Something similar has happened to Brookfield as well.

I am not sure that this volatility is justified but it is a fact of life. So investors should be prepared and take advantage of it. I believe Blackstone is so cheap now due to this volatility, and the same might be true about BAM (though in this case it is also related to the recent reorg).

Asset-heavy Apollo has been exposed to volatility as well. I opened my position in mid-2021 when the company announced a merger with insurer Athene. For me, the case of undervaluation seemed pretty clear. What followed was some rather wild gyrations. I am holding APO for 1.5 years now and it has delivered 8% of annualized returns vs -6% for the S&P 500. It seems satisfactory under the circumstances but I expected more.

The biggest risk is an overestimation of growth rates. I cannot pinpoint any specific reasons for it but I should mention it as the forecasted growth rates are not compatible with valuations. Either investors in alt managers will achieve enviable returns or the real growth will be far below forecasts.

Conclusion

My personal preferences are with asset-light managers and Apollo. BAM seems very enticing for the reasons I described. The whole Brookfield organization has a habit of meticulous planning far ahead and recently Bruce Flatt mentioned that the growth of ~20% is already locked in for the next several years.

Asset-heavy BN is a holding company trading below the sum of its parts. BAM represents close to 50% of its value. If BN performs well, it will be most likely due to the strong BAM performance. But in this case, it is better to own BAM directly.

Blackstone is very cheap but is dependent on the combination of management and performance fees and the latter are less predictable. Its AUM are approaching $1T and it may be more difficult for it to achieve high growth.

I will not be surprised if smaller Ares ends up being the best performer. I do not own it at this point but may open a position.

This is my first attempt at writing for investors who are not well familiar with the industry. Dependent on your response I will either continue this effort or drop it completely.

For further details see:

How Brookfield And Peers Make Money And How You Can Participate In 2023