PXD - How Devon Energy Positioned Itself For Growth

2023-08-17 13:17:21 ET

Summary

- Devon Energy has undergone a significant transformation over the past decade, shifting its focus from natural gas to oil and making strategic asset sales and acquisitions.

- The company's share price has followed natural gas prices for the past 12 years, but it is now more balanced and has the potential for a long-term breakout.

- Devon Energy has created significant capital value for shareholders and is expected to continue doing so in the future, with a strong focus on its Delaware Basin play.

The first individual company I will be covering in my return to writing on Seeking Alpha is Devon Energy (DVN).

Devon Energy is a company with an extremely rich history as it was the company that broke barriers with its acquisition of Mitchell Energy all the way back in January 2002. When it acquired Mitchell Energy, Mitchell Energy had only discovered and “cracked the nut” of fracking for natural gas on vertical wells. When Devon Energy entered the picture, they began fracking using horizontal drilling technology, fracking their first two horizontal gas wells in June and July of 2002. And thus, a new epoch of oil and gas history was unleashed on the world. In this new "oil" rush, Devon Energy, like many other companies, over-leveraged themselves with debt and over-leveraged themselves towards natural gas, making the twelve-year period of declining natural gas prices from 2009 to 2021 difficult for them to weather. I actually worked for EOG Resources (EOG) from 2008 to 2012 and I can tell you first hand that these days were frenzied times inside oil and gas companies as they were trying to figure out the scale and scope of what it was that they had just discovered. When it was realized just how much natural gas existed thanks to this new technology, Devon’s natural gas weighted portfolio became less attractive relative to its peers like EOG Resources and Pioneer Natural Resources (PXD).

For the past decade, since 2009, Devon Energy has wisely reversed course and is on a much better trajectory today. This reversal in its strategy was gradual with each eventual asset sale and new oil-focused acquisition, however, the moment that it began was in the heart of the 2009 market crash. Below I will cover some of the acquisitions and changes Devon Energy made following the 2009 Great Recession as I think it is important to understand and appreciate the massive transformation Devon Energy underwent.

NOTE: As you read my writings, you will notice that I always touch upon history. In my mind, if you don’t understand the history of a company, then how are you going to know the future of the company? You can read my bullish case for oil here where I also touch on history, slightly.

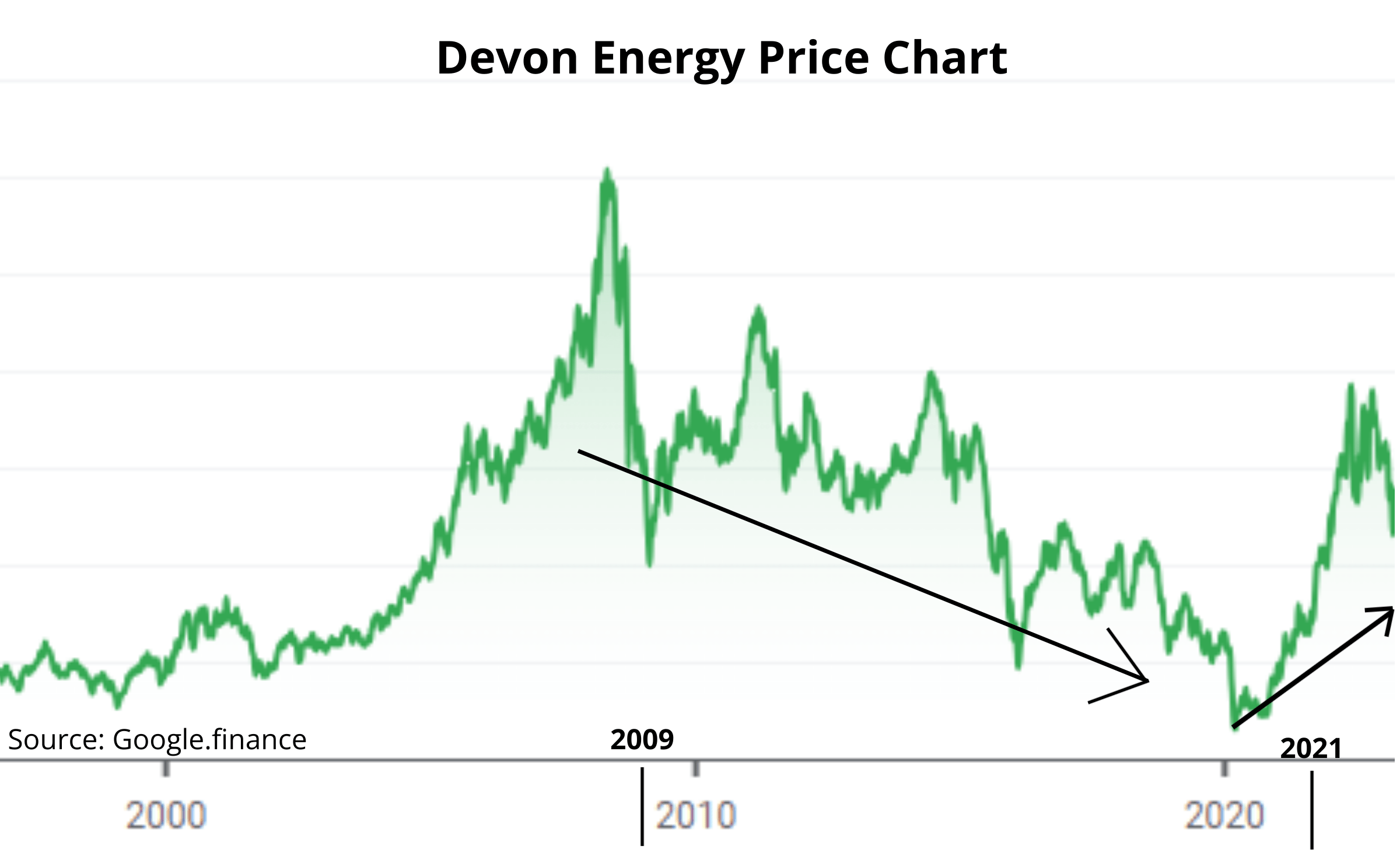

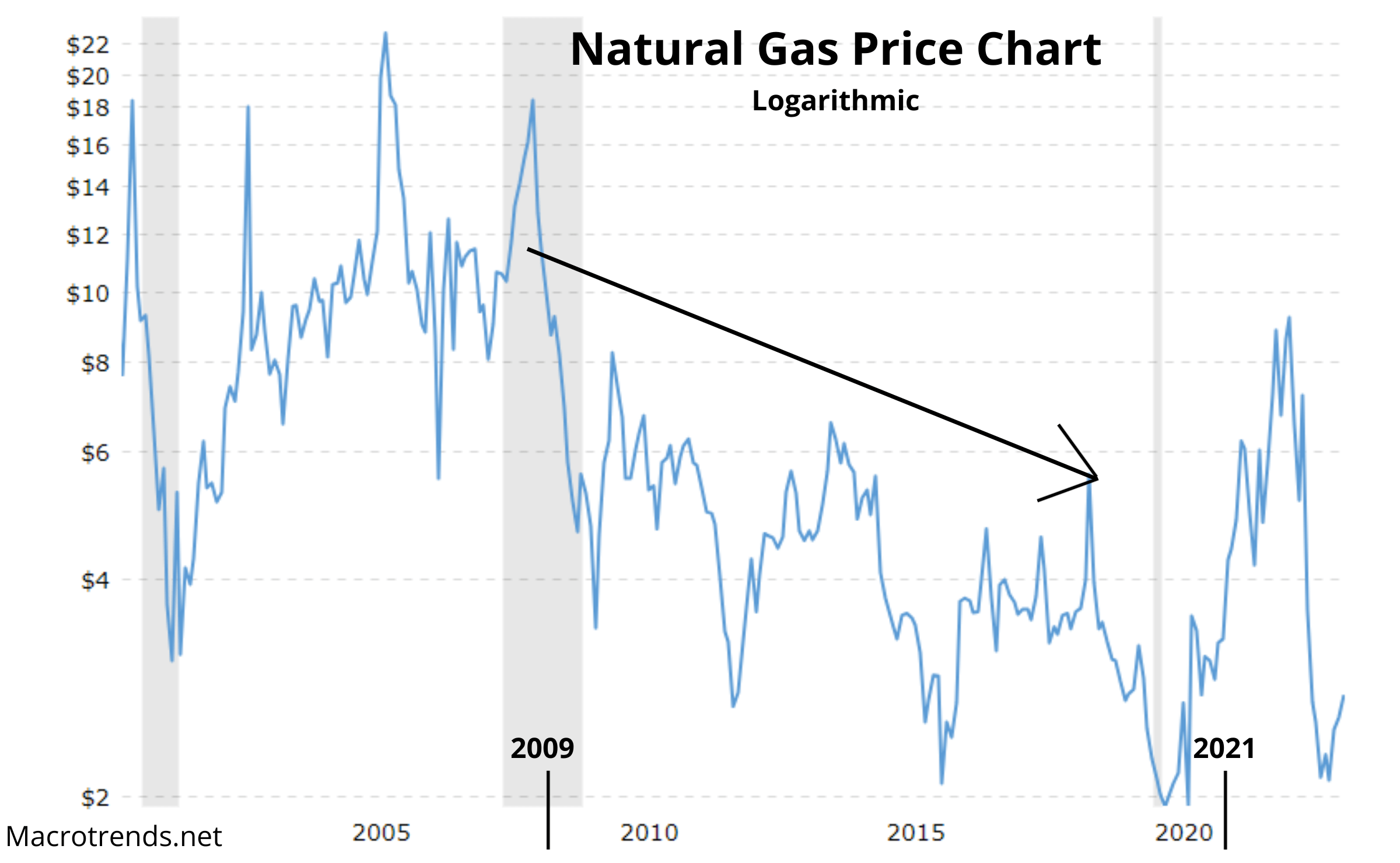

Before we cover Devon's transformation, first, let's look at the historical price charts. Notice the path that Devon’s share price has taken relative to natural gas prices in the two charts below. For twelve years from 2009 to 2012, Devon has been treated like a natural gas company while it tried to transform itself into an oil-shale company. And I would say they were successful.

Devon Energy Price Chart (Google Finance)

{kind=link}

Natural Gas Price Chart (Macrotrends.net)

{kind=link}

I realize my price chart could be a little more "technical" with candlesticks and trendlines and such, but for those who appreciate technical analysis, I believe Devon Energy just completed a giant twelve-year falling wedge pattern where it followed natural gas prices. And in technical analysis, the larger the falling wedge, the greater potential size and length of time of the breakout. Not only have natural gas prices experienced a breakout following 2020-21, but Devon Energy is no longer weighted to natural gas like it once was.

Following Devon Energy's Transformation

In November 2009, Devon Energy announced that they would be selling their Gulf of Mexico assets. Then, immediately following in December they sold a portion to Maersk Oil and Gas for $1.3 billion. Then in March 2010, the company sold the remainder of its Gulf of Mexico assets to BP (BP) for $7 billion strengthening the company’s balance sheet. And one month later, the company sold all of its Gulf of Mexico Shelf assets to Apache for $1.05 billion. When the history books of Devon Energy are written, November 2009 should be marked as a strong turning point for the company.

The transition continued when they made a major asset sale to Linn Energy in April 2014 for $2.3 billion. Two years later, in May 2016, Linn Energy went bankrupt, providing confirmation that their larger strategy of offloading natural gas assets was intelligent in my view.

Immediately following the sale to Linn Energy, the company made a major acquisition in the Eagle Ford Shale by buying GeoSouthern Energy for $6.1 billion. From there, they continued making acquisitions that were more focused on oil as opposed to natural gas shale.

| Company |

| Year |

| $ Amount |

| Play Location |

| GeoSouthern Energy |

| 2014 |

| $6.1 Billion |

| Eagle Ford Shale |

| Felix Energy |

| 2015 |

| $2.5 Billion |

| Powder River & Anadarko |

| WPX Energy |

| 2021 |

| $2.56 Billion |

| Williston and Permian |

| Validus Energy |

| 2022 |

| $1.8 Billion |

| Eagle Ford Shale |

As I review Devon Energy’s transformation over the twelve years from 2009 to 2021, it is very impressive what they were able to accomplish. First, their management along with Mitchell Energy's management should be commended for the technological advancements they unleashed in the Barnett Shale, however, their discoveries caused them to become myopic, in my opinion. Instead, they should have been studying the market and trying to apply this same technology to oil shale. Unfortunately, their shareholders paid the price from 2009 to 2021, for this mistake. However, they should be strongly commended for their aggressive course correction and I believe the company is set up to perform very well over the next six to seven years.

Devon Energy's strategic merger with WPX Energy, completed in January 2021, bookended their twelve-year slide and was a wise move given the company’s complimentary portfolios and the fact that Devon Energy was headquartered in Oklahoma City and WPX was headquartered in Tulsa. This final merger with WPX gave Devon the final piece that they needed, in addition to the combined company's new leadership in CEO Rick Muncrief.

I don't have the bandwidth to evaluate a broad swath of metrics in every article I write, but I will try to choose a unique metric to evaluate a company each time. Overtime, I will collect data and have a more comprehensive analysis. For now, I want to draw your attention to the slide below.

Capital created (Devon Energy Q2 Report)

I really love this chart. However, I will admit it is a little misleading since it is measuring the starting point in 2020, when fear in the market was extreme and company valuations across the board were extremely depressed. Nonetheless, it tells a story. The story it tells is that Devon Energy has created real “capital” value for its shareholders relative to its valuation. When this chart began with the Devon/WPX merger, announced in 2020, the combined companies were worth $5.9 Billion. Year-to-date, the company claims to have created $12 billion in capital value for shareholders since late 2020. I like this metric because it is a direct measure of the capital created for shareholders. Granted, all of this capital doesn’t end up directly in the pockets of shareholders but that’s because much of it gets reinvested into the company.

You might be thinking that this is all well and good, but this is a chart that only looks into the past. Again, I believe history is extremely valuable because it can tell us something about the future.

First, by looking at history, I'm not saying that there will be another "mass-fear" event that will depress valuations in the near future. Do I think there will be a “mass-fear” event like there was in 2020-21 at some point? Yes, I do believe there will be another “mass-fear” event in 2029-30ish (although I don’t believe it will be anything worth “fearing”). And so if that's the case, the question we should ask ourselves is, do we believe Devon Energy will create another $12 billion in capital value for shareholders during the next 3 years the same way they did during the past three years? And my answer to that is yes, I believe they will likely exceed that. If that is the case, with the company only having a $30 billion market cap, I believe the company valuation has room to grow. By this metric, my opinion is that the company is still undervalued.

Next, if Devon is going to create this much capital value over the next few years, where is that going to come from? How are they going to do it? I’m not going to try to forecast hydrocarbon prices, but I believe we are in a long-term bullish environment for prices and so this will be one source of increased value. However, I’d rather not bank on that. To understand where that value will come from, consider that the formation play that Devon Energy seems most excited about is their Delaware Basin play. Once you understand that, understand that in Q1 of 2023, they only had 42 wells completed in the play and in Q2 of 2023, they nearly doubled that number to 76 wells completed. As I listened to the quarterly call, it was clear that Devon is gaining greater efficiencies in the operations each quarter, including in the Delaware Basin. So this is going to create what I believe will be a tremendous source of leverage for the company’s value proposition going forward. The company agrees and is currently dumping 60% of the company's capital investment into the play. In your mind's eye, ask yourself how many wells will Devon have completed by 2026? By picturing this, you can quickly understand how Devon Energy could see some aggressive growth when their flagship project will have been much more exploited by then.

Devon Energy Delaware Basin (Devon Energy Q2 Presentation)

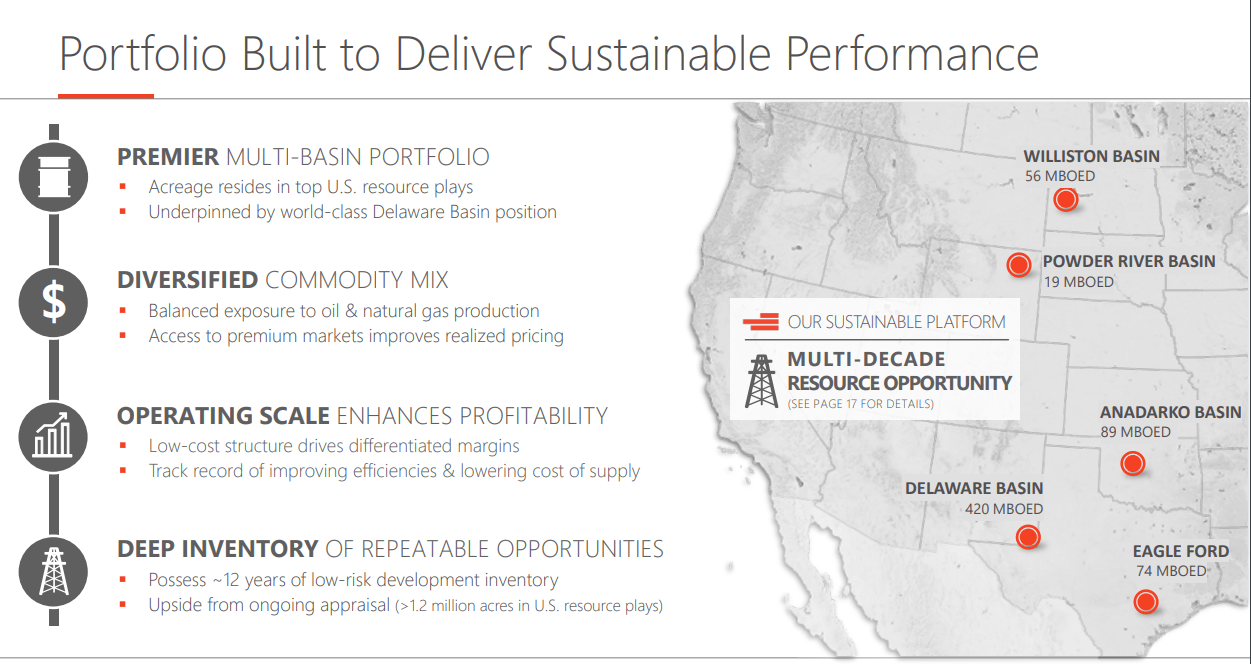

Devon Energy Portfolio of Plays (Devon Energy Q2 Presentation)

{kind=link}

ESG Initiatives and Geothermal Energy

One thing that I don’t really appreciate about Devon Energy is its eagerness to play ball according to the ESG initiatives. However, I will admit that I don’t understand the stipulations that are placed upon them and so I can’t be too critical without first understanding that. I simply don’t appreciate it because I don’t and never will adhere to what I think is a fear-based, climate-change belief system.

They are now publishing an annual "Sustainability Report and Climate Change Assessment Report" which states the various frameworks they are trying to adhere to. See a list from their report below.

The report also reflects Devon’s level of alignment with voluntary frameworks and standards established by IPIECA, TCFD, SASB, United Nations Sustainable Development Goals, American Petroleum Institute, and American Exploration and Production Council.

That said, Devon Energy did do something recently that made me even more excited about their future. They took a step towards investing in geothermal energy . I won’t go into depth in this article about why I believe geothermal energy is the future, but my ears always perk up when I hear about a company investing in geothermal energy. And that is what Devon Energy began doing in April 2023. They dipped their toes into the water with a $10 million investment into Fervo Energy. With such a small investment, it doesn’t warrant a deep dive, but it does show me that Devon Energy learned from their mistakes in the past and is beginning to think about what horizontal drilling technology and drilling technology more broadly means for other sources of energy, not just oil and gas shale. As you will recall, Devon’s tunnel vision focusing solely on natural gas drilling got them in trouble from 2002 to 2009.

To clarify, I'm not excited about geothermal energy because it is "clean" energy, but rather I am excited because it may one day produce energy cheaper than any other alternative.

Conclusion

In conclusion, if your conscience doesn’t bother you by investing in a company that is playing ball by the rules of the ESG narrative, then it is my opinion that Devon Energy is a fantastic investment today. As time continues, I’m not sure you will be able to find an oil and gas company that defies the powers of ESG that are imposed upon them. After all, without even looking, we can likely predict who Devon Energy’s largest shareholders are. Hint: it's the same for many public companies.

Today, I would recommend Devon Energy as a long-term buy. I believe they are well positioned for growth for at least the next 5 to 6 years. I will be keeping tabs on quarterly developments within Devon Energy and as we approach the years of 2029 to 2030, that would be a good time to reassess whether Devon’s strategy over that time has paid off and how they are positioned for the future... and to reassess the broader oil and gas market as a whole.

For further details see:

How Devon Energy Positioned Itself For Growth