SPGP - How I'd Invest $2.5 Million Right Now

2023-09-29 07:20:00 ET

Summary

- My family has been rocked by an unrelenting string of medical and life crises. Fortunately, my family's charity hedge fund is saving us from bankruptcy and despair.

- I've updated my family's ZEUS Income Growth fund plan to include my best ideas right now. In other words, if I had $2.5 million in cash, this is what I'd buy.

- This portfolio yields 4.2%, has 13.7% long-term return potential, better than the Nasdaq, and analysts expect it to potentially quadruple over the next decade.

- It consists of 9 ETFs and 7 of my highest conviction stock ideas, all world-beater blue chips that my family trusts with our hopes, dreams, and mountains of medical bills.

- No matter how tough life gets, investing, business, and a joyous life are all about being thankful for your blessings, focusing on what you can control, and adapting and overcoming adversity. That's how you can build your own personal utopia even when life is tough.

Our members have asked me for an update on my family's $2.5 million charity hedge fund. So here it is, along with an explanation for why I'm using the ZEUS Income Growth portfolio tracking tool as a "Top Buys List."

My Family's Personal Situation Is Different Than Yours

At the moment, 50% of our portfolio is bonds because there is a 93% probability of recession in 2024.

{kind=link}

It's still a way off, but given our 6 medical crises we're going through, including two family members with cancer, along with heart disease, diabetes, kidney stones, and several others, we're facing massive out-of-pocket expenses.

My sister was just diagnosed with thyroid cancer and had her second surgery, completely removing her thyroid. The lymph node biopsy on the left side showed some metastasis, but the right side didn't.

She will begin radiation therapy soon, but the out-of-pocket expenses, even with insurance, are at least $15,000.

Why We Hedged With Lots Of Bonds And Managed Futures

Going into a recession with the market likely to fall 24% to 30% before the bear market finally bottoms and facing massive and seemingly never-ending bills (home repair and car repair too), we have to protect ourselves.

S&P Bear Market Bottom Scenarios 2024 Recession Start, October Historical Market Bottom

{kind=link}

The last thing we can afford is to become forced sellers in a market panic.

But of course, life is what happens when you're making other plans.

{kind=link}

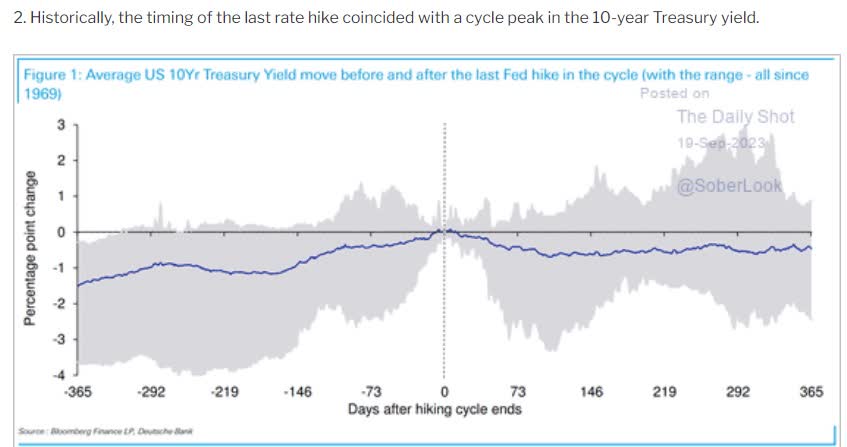

Historically, since 1969 long-term rates peak when the Fed is done hiking rates.

That's the average. It can take as long as 10 months for rates to actually peak.

{kind=link}

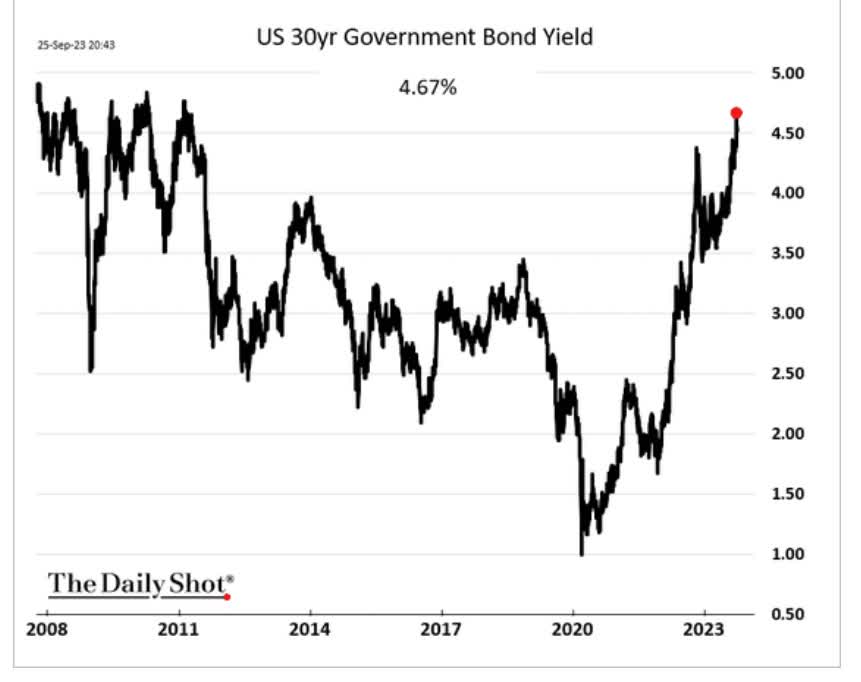

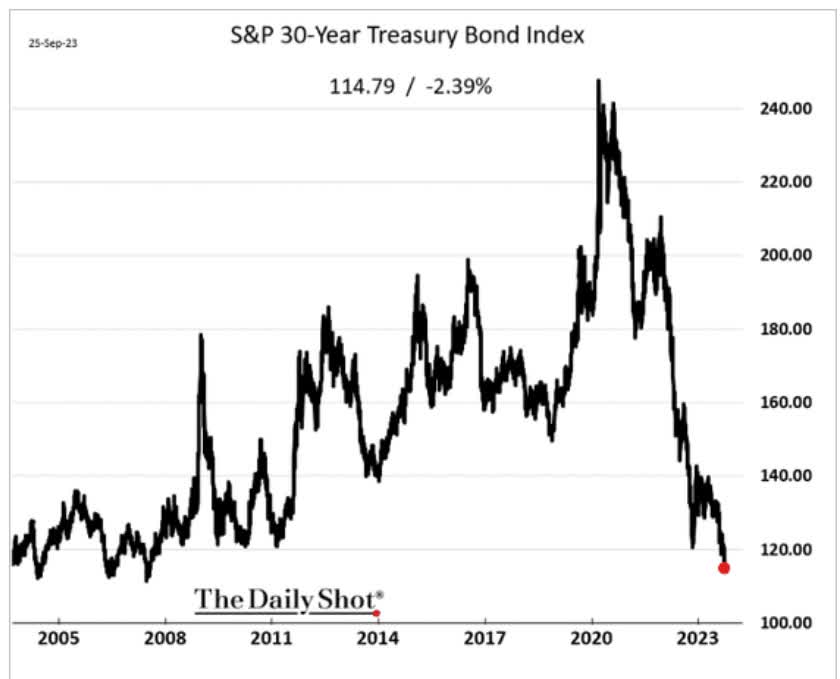

This is what's happening at the moment and the pain in the bond market, and my family's hedges has been historic.

{kind=link}

This is the worst bond bear market in U.S. history by far.

{kind=link}

The crash in 30 year bonds from record highs has surpassed 30 years, and 30 year bonds are now trading at a 15-year low.

Nobody can predict interest rates, the future direction of the economy or the stock market. Dismiss all such forecasts and concentrate on what’s actually happening to the companies in which you’ve invested.” — Peter Lynch.

Indeed, Peter Lynch, while we're 93% likely to be proven right in the long-term, when you are facing half a million dollars in unrealized bond losses, things can become a bit unpleasant, to say the least;)

{kind=link}

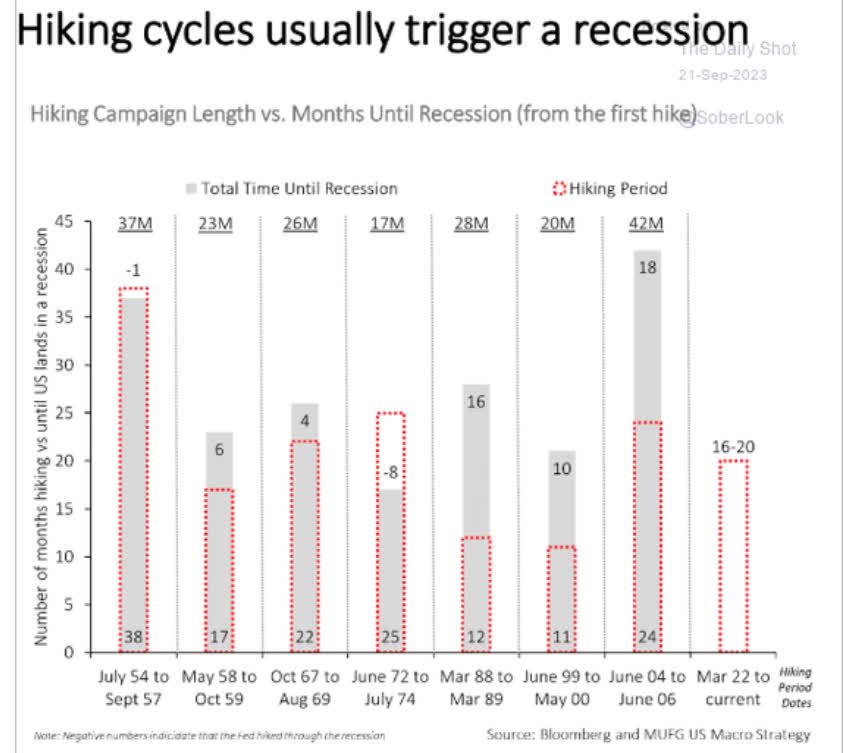

The Fed has caused 9 of the last 13 recessions, and never in history has inflation started out above 5% and the Fed beat it down without one.

How long might it take before we can say with confidence that the Fed has achieved an unprecedented soft landing?

- 42 months from the Fed's first hike is Tuesday September 16th, 2025

- the recession the Fed is 93% likely to cause (per the bond market) could begin as late as the end of 2025.

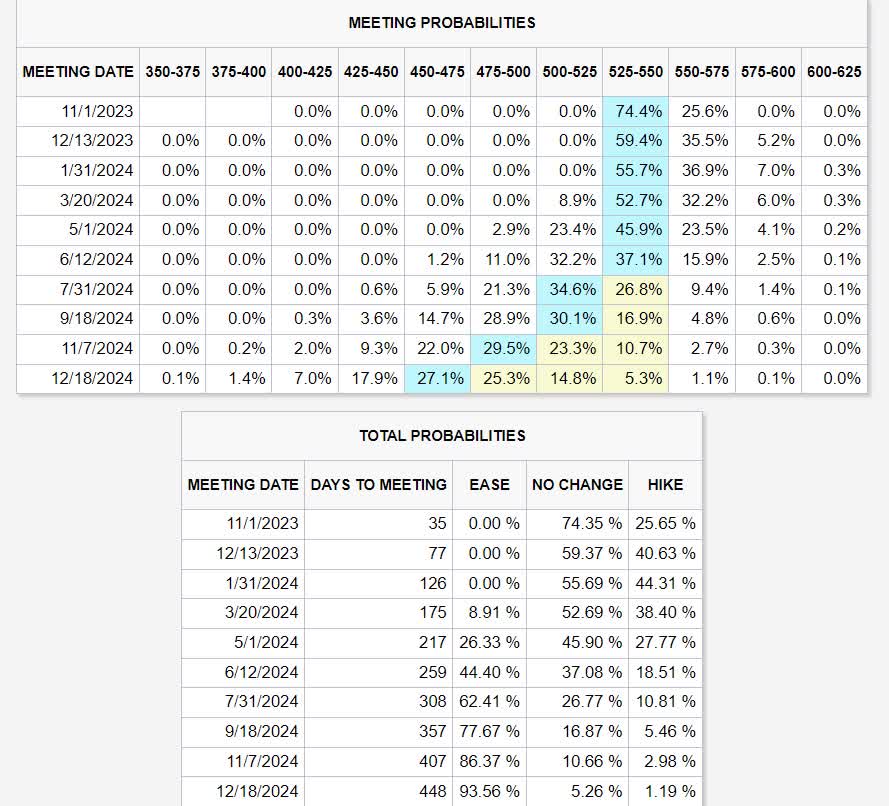

In the meantime the Fed has said, via its latest summary of economic projections, that it plans to hike to 5.5% in November and then keep rates that high for a year.

All while continuing the most aggressive reverse money printing in history ((QT)).

{kind=link}

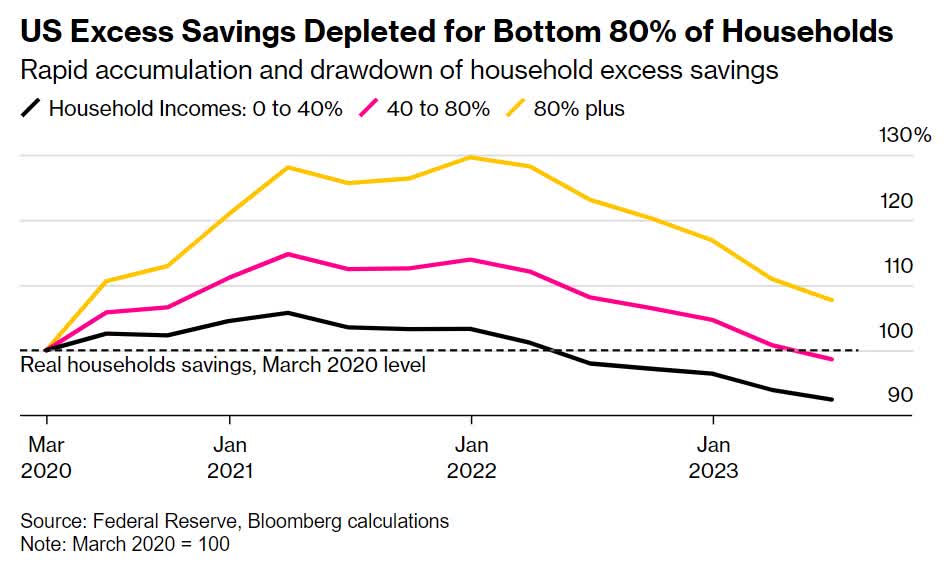

Only the richest 20% of Americans have any excess savings from the Pandemic left ($8,000 on average).

That is expected to run out by the end of the year, one final spending binge during the Christmas season.

{kind=link}

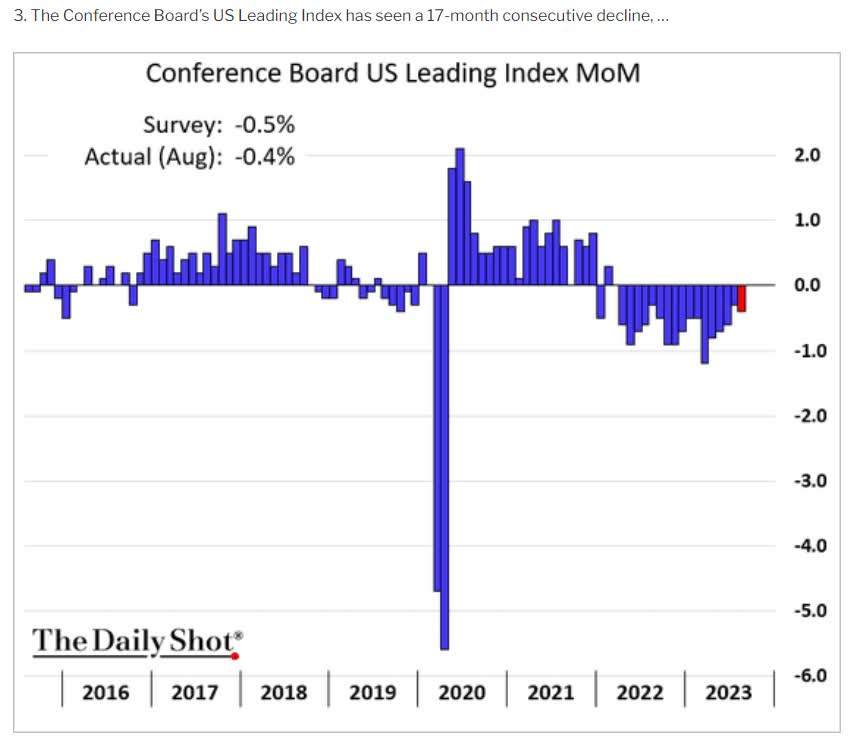

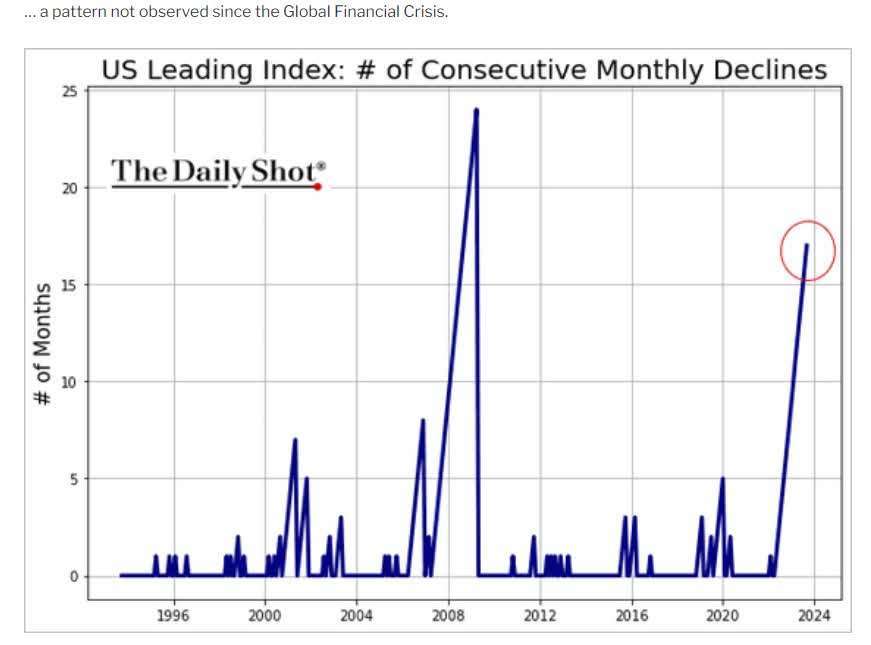

Leading economic indicators have been pointing to recession for 17 consecutive months, the 2nd longest streak in history.

{kind=link}

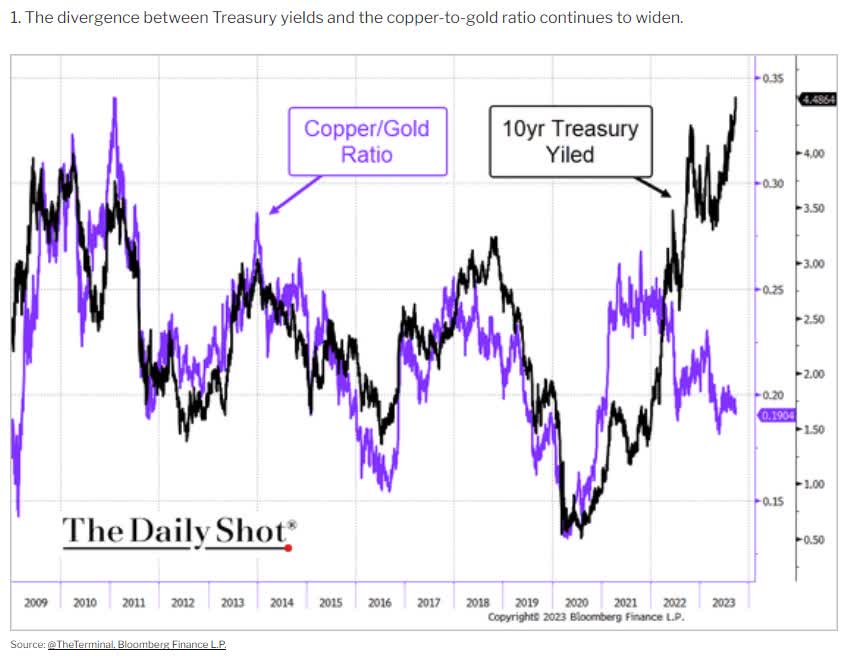

Some models, like the copper/gold ratio, signal that long-term yields should be 1.5% to 1.75% right now, implying a 65% potential upside to long-bonds.

{kind=link}

On the other hand, Jamie Dimon warns that in a worst-case scenario, the Fed might have to go to 7% and Bill Ackman is hedging against 5.5% 30-year yields.

The worst case is 7% with stagflation," he told TOI while in Mumbai for an investor summit. "If they are going to have lower volumes and higher rates, there will be stress in the system." - Seeking Alpha .

In Jamie Dimon's worst-case stagflation scenario, Bank of America thinks the real yield on bonds could hit 3%, implying as much as 9% yields on 10 to 30-year Treasury bonds.

That would be a bond apocalypse that would make the current 50% decline look like a picnic.

- an additional 78% decline from here in this worst-case scenario

- 89% total peak decline (from record highs in 2020) in this worst-case scenario

- vs 87% peak decline in stocks in the great depression.

The probability of this doomsday scenario is very small, less than 1%, (vs 2.5% risk of nuclear war with Russia).

But it's still something any responsible investor must hedge against.

Markets can be irrational longer than you can remain solvent." - John Maynard Keynes.

{kind=link}

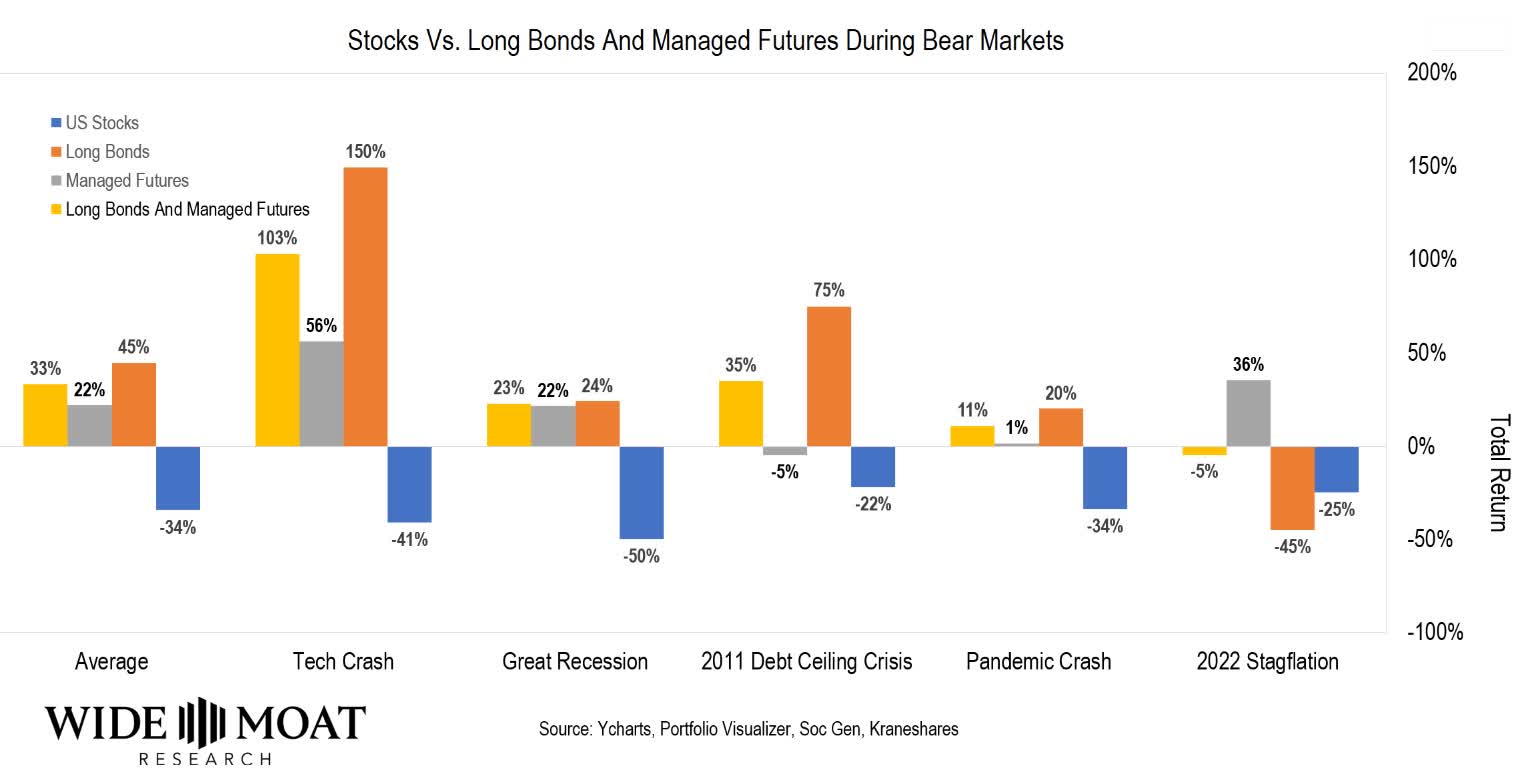

That's why we also own managed futures, which, when combined with bonds, create the most effective hedging strategy of the last 50 years.

- 97% likely to keep working in the future

- it worked in the 1970s stagflation hell (12% average annualized gains).

So what managed futures do I recommend now?

KFA Mount Lucas Index Strategy ETF (KMLM) has delivered 2X the industry's historical returns since 1989, just like Buffett beat the S&P by 2X for decades.

- KMLM is the Buffett of managed futures

{kind=link}

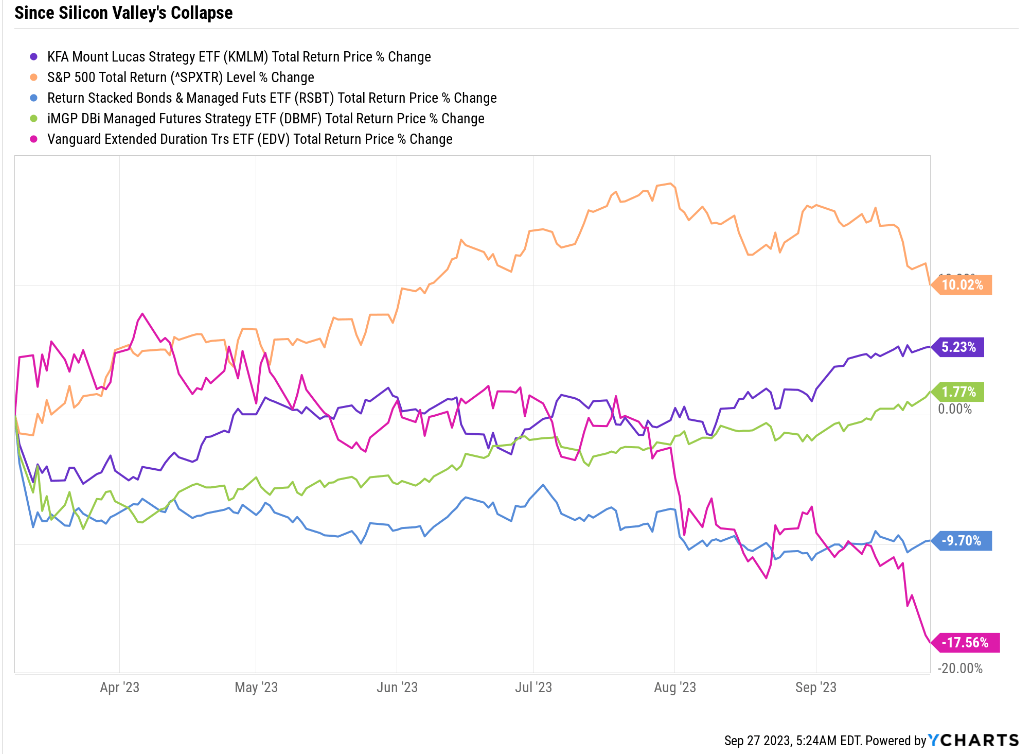

The worst collapse in industry history occurred when the bond collapse suddenly turned into the strongest bond rally in 42 years overnight.

- Silicon Valley Bank.

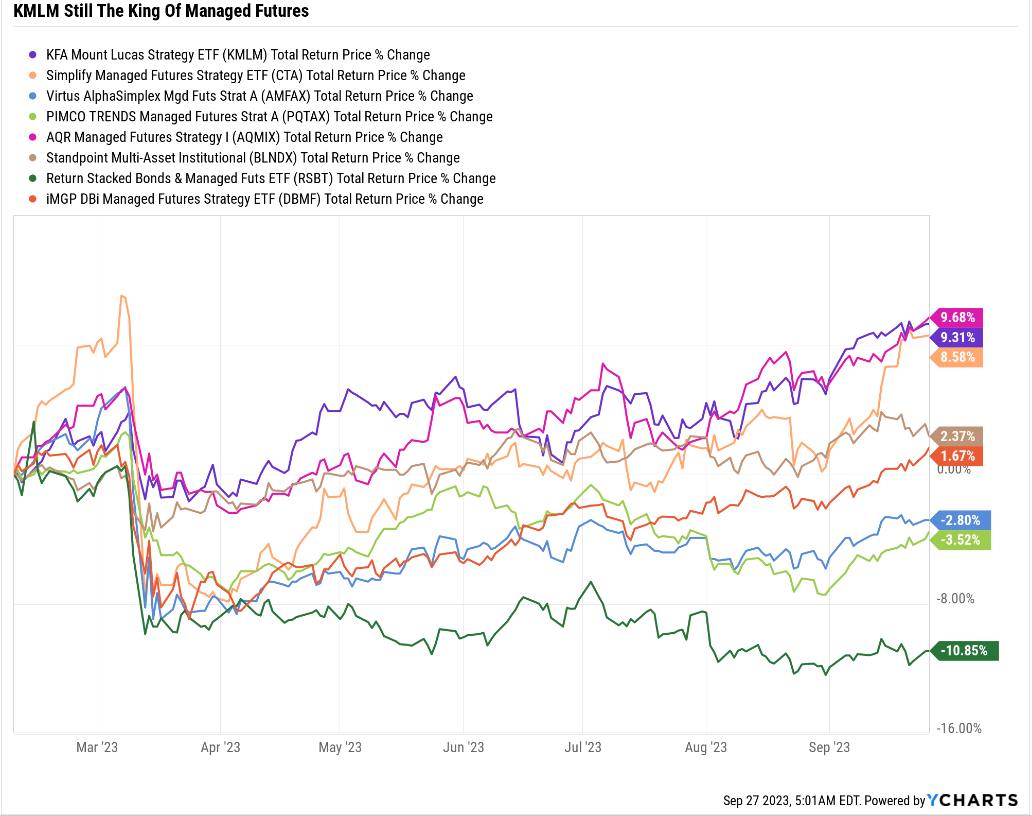

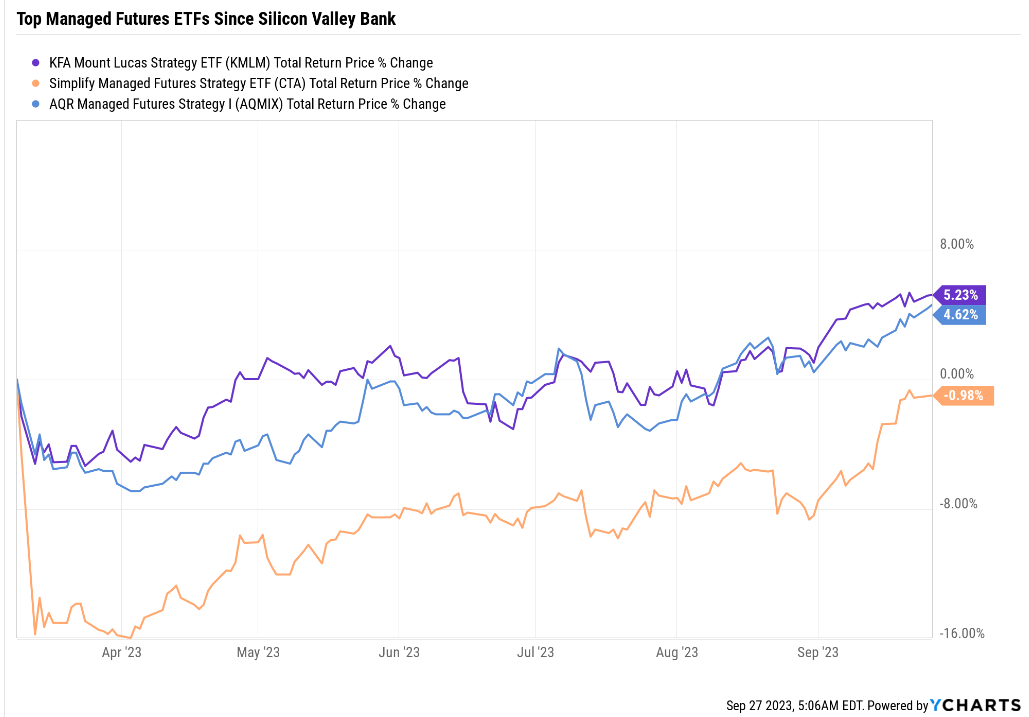

Here are the top 3 performing managed futures ETFs since the start of the regional banking crises.

{kind=link}

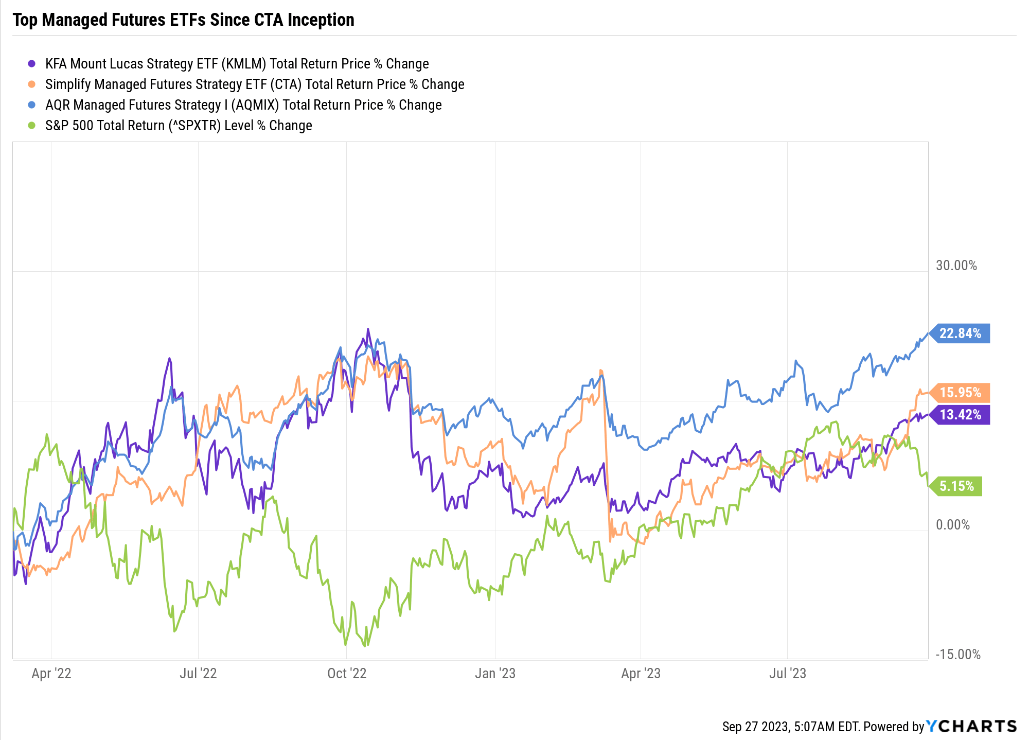

And here is how they have fared since the inception of Simplify Managed Futures Strategy ETF (CTA).

{kind=link}

Wow, that's impressive, managed futures beating the S&P in a recession, right? Naturally, that can't last, but AQR Managed Futures Strategy Fund Inst (AQMIX), the industry titan, doesn't actually maintain its lead over KMLM's superior strategy long-term.

{kind=link}

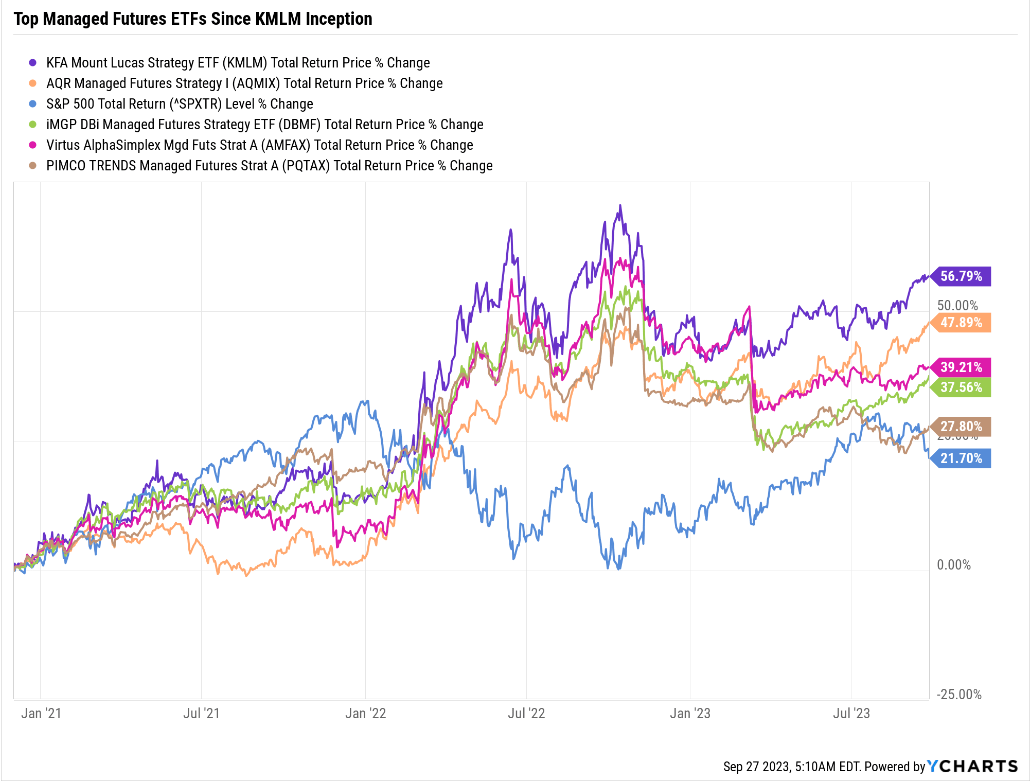

And while KMLM began trading in Jan 2021, the index it's based on, the Mount Lucas CTA index, has been around since 1988.

{kind=link}

9.4% annual returns for 34 years vs. historical 4.5% annual returns for managed futures (0.5% better than bonds).

AQR Managed Futures Since 2010

{kind=link}

KMLM's max decline since 1989 would have been about 28% similar to AQR's 24%. KMLM's index delivered 3X the long-term returns of AQR and with 0.3% lower annual expenses.

- KMLM expense ratio 0.9% vs 1.28% AQR.

The expense-adjusted long-term returns on KMLM (had it existed since 1988) would have been 8.5%, paid out through annual dividends.

Krane Shares, Charlie Bilello

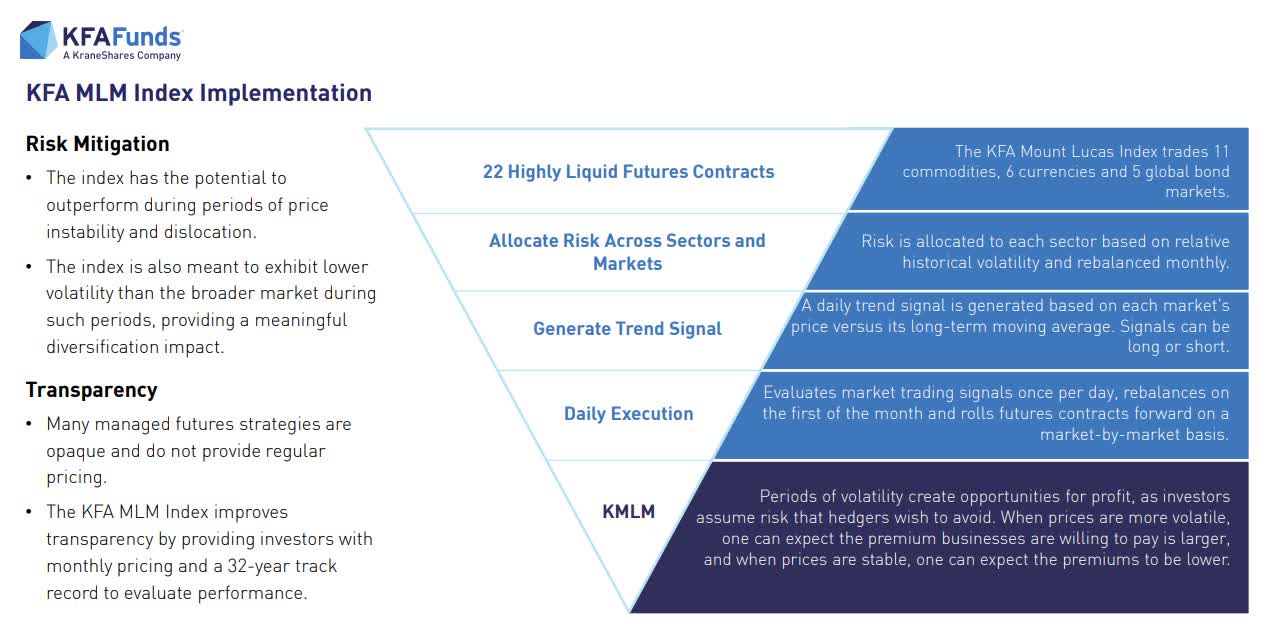

When the market is melting down, Mount Lucas shines brightest. Why?

{kind=link}

Because KMLM has the best strategy of any managed futures fund.

It's 100% rules-based, proven over 35 years through every kind of crisis and interest rate environment.

GFC? Pandemic? Banking crises? 9/11? Recessions? Bear markets, bull markets, and KMLM's index has shined because it has no stock exposure at all (maximum negative correlation) and has a monthly reset on its trend-following strategy.

- monthly reset but daily tweaks

- it pivots quickly but doesn't get faked out like in 2023 when there was no trend until recently.

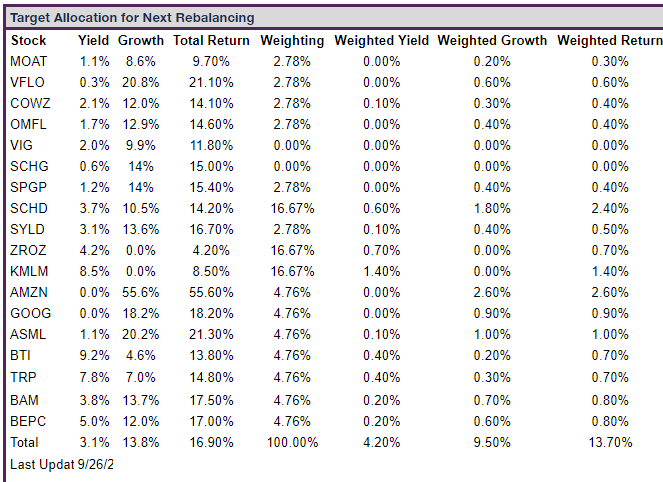

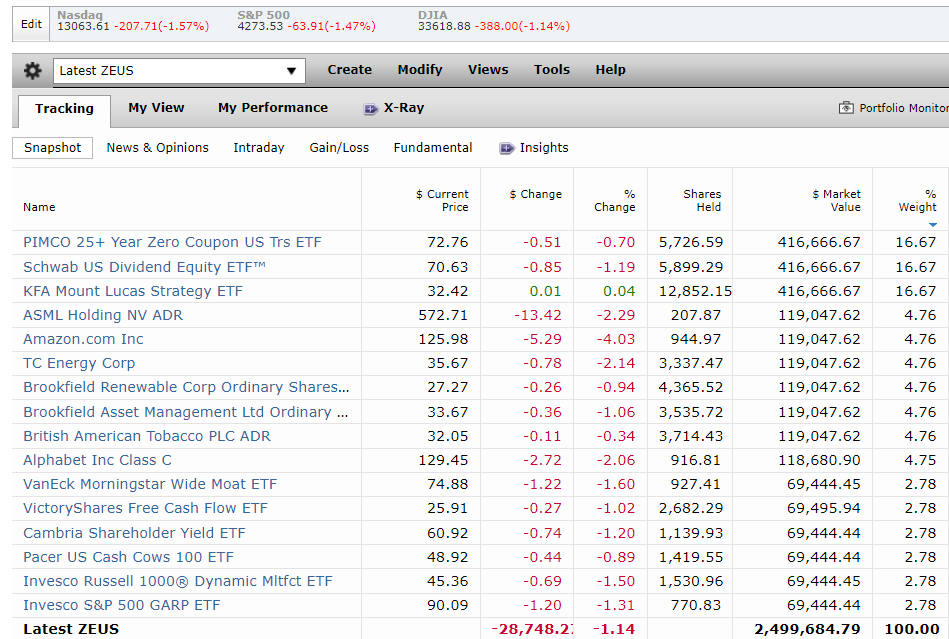

What My Family Charity Hedge Fund Would Buy Today (Our Long-Term Goal)

{kind=link}

I'm not going to show you what I own today because what I bought years ago has no bearing on the best options for investors today.

- would you rather know what Warren Buffett thinks is the best buy today? Or that he owns Coca-Cola (KO), which he bought in the '80s?

- or that Apple (AAPL) is his biggest holding because he loaded up in 2016?

This is what we'd be buying today if we weren't drowning in crises and bills.

Fortunately, my high income is allowing us to pay the massive bills without selling anything, even in the face of short-term catastrophic bond losses.

{kind=link}

Had I known about KMLM's superior strategy and track record from the start (iMGP DBi Managed Futures Strategy ETF (DBMF) was the first managed futures fund I ever learned about), I would have been 50% KMLM and 50% long bonds, and the loss since the banking crisis began would be 1/3rd as large (a $300K smaller paper loss).

DMBF and Return Stacked Bonds & Managed Futures ETF (RSBT) are fine funds that will likely do well over time. However, history is clear that KMLM's strategy is the gold standard in managed futures funds.

Going forward, that is why I will be buying and eventually, my family fund will sell RSBT and DBMF.

- RSBT theoretically should deliver 12.5% long-term returns

- but the actual history (not its fault, poor timing when it launched) is the worst of any managed futures ETF.

Nasdaq's Returns Over The Last 37 Years

{kind=link}

My family's goals are for 13% to 15% long-term returns, and that's what this portfolio is capable of, according to the FactSet and Morningstar analyst consensus.

Portfolio Details

I've linked to articles I've done about each of these companies and ETFs.

ETF Bucket 33%

Core ETFs (Long-Term Holdings Are Stable "I always know what I own"

- Schwab U.S. Dividend Equity ETF ( SCHD ) for high-yield blue-chips.

Strategy ETFs (It's the strategy, not the holdings that matter, high turnover)

- VanEck Morningstar Wide Moat ETF ( MOAT ) (Wide Moat Buffett-style "wonderful companies at fair prices")

- Victoryshares Free Cash Flow ETF ( VFLO ) (Buffett-style deep value ETF focused on growth).

{kind=link}

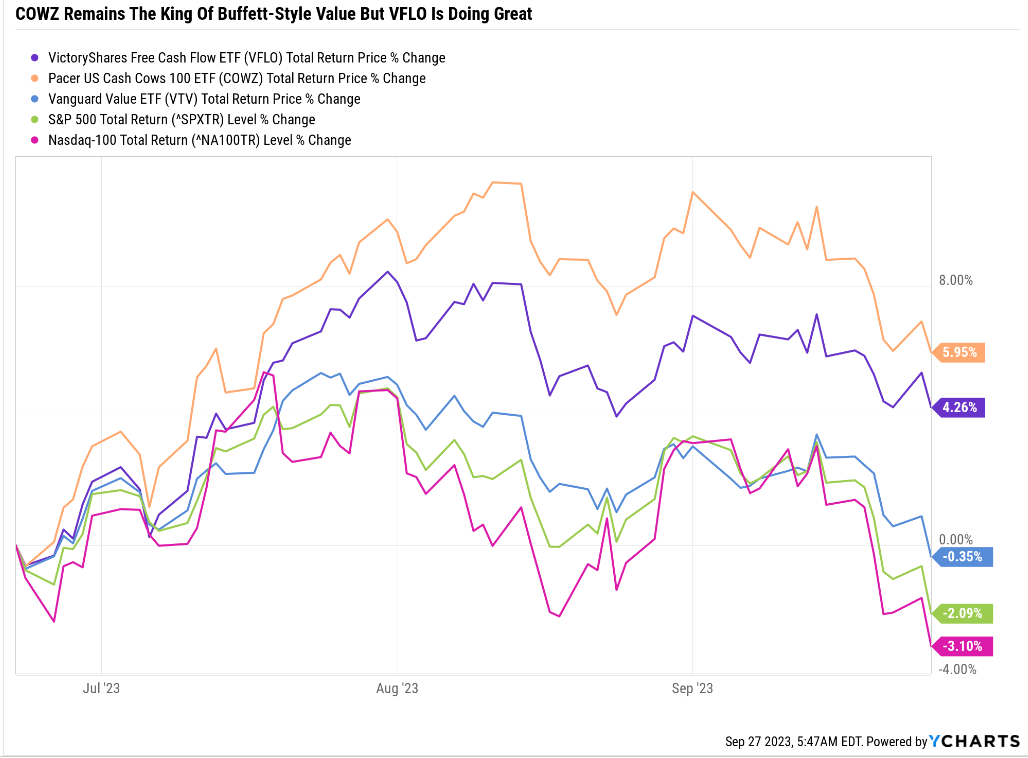

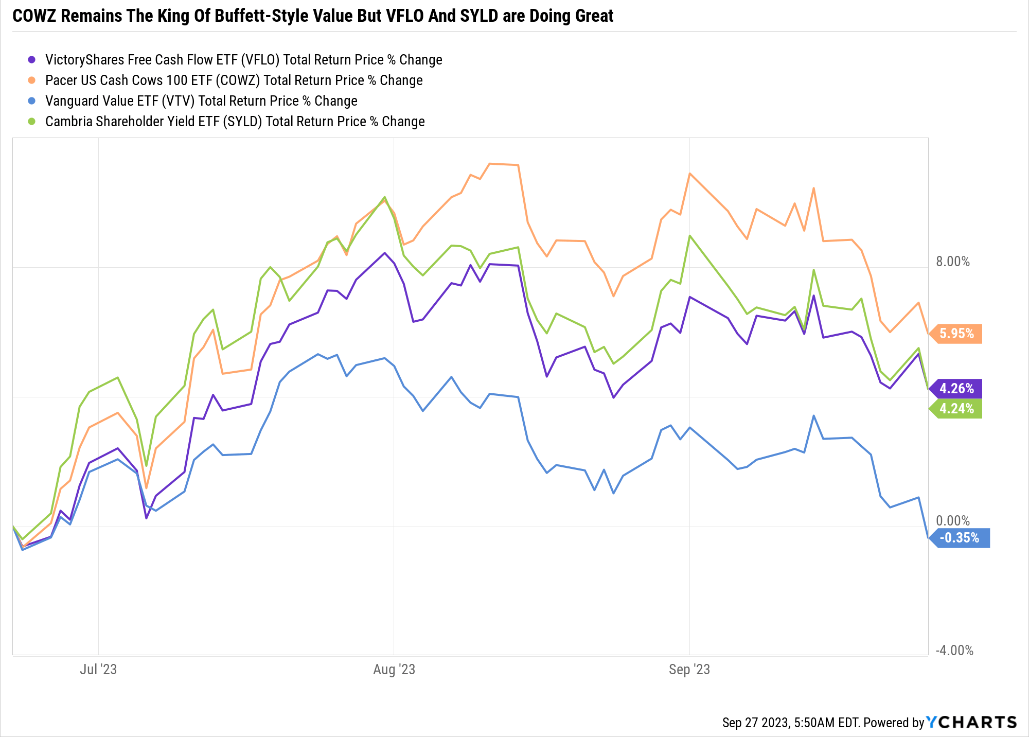

- Pacer US Cash Cows 100 ETF ( COWZ ) King of Buffett-style deep value ETFs

- Cambria Shareholder Yield ETF ( SYLD ) king of actively managed deep-value ETFs.

{kind=link}

- Invesco Russell 1000 Dynamic Multifactor ETF ( OMFL ) - 5-star rated smart beta ETF

- Invesco S&P 500 GARP ETF ( SPGP ) - 5-star rated super GARP fund.

What about SCHG for growth and VIG for dividend aristocrats?

- SCHG is 13% overvalued so I can't recommend buying it.

- VIG I'll cover in an update tomorrow explaining why SCHD is a better buy today.

Hedging Bucket 33%

- PIMCO 25+ Year Zero Coupon U.S. Treasury Index Exchange-Traded Fund ETF ( ZROZ ) - longest duration US Treasury ETF there is

- KFA Mount Lucas Index Strategy ETF ( KMLM ) - gold standard Buffett of managed futures.

Stock Bucket

High-Yield Sub Bucket

- Brookfield Asset Management ( BAM )

- Brookfield Renewable Corp ( BEPC )

- TC Energy ( TRP )

- British American Tobacco ( BTI ).

Hyper-Growth/AI Sub Bucket

Portfolio Summary

{kind=link}

- yield: 4.2%

- growth consensus: 9.5%

- long-term return potential: 13.7%

- discount: 11%

- Forward PE: 13.5X vs 18 S&P

- 10-year valuation boost: 1.2% per year

- 10-year consensus total return potential: 14.9% per year vs. 8.9% S&P

- 10-year consensus total return potential: 301% vs 135% S&P.

Bottom Line: Life And Investing Is About Adapting To Bad Stuff Happening

If you want to make God laugh, tell him your plans." - Yiddish proverb.

Life investing and running a business is all about adapting and overcoming challenges.

Nothing will ever go perfectly right and long-term success is all about focusing on safety and quality first, and prudent valuation and sound risk management.

Not just for your portfolios but for life.

Learning my sister has metastatic thyroid cancer is a shock to my family, especially since she's 26 and has always been very healthy.

Drowning in unexpected bills is something that many Americans can relate to.

But at the end of the day, here is what I've learned from nine years as an analyst. Warren Buffett was right, (big shock I know).

If you don't find a way to make money while you sleep, you will work until you die.” - Warren Buffett.

My family just did a quick calculation and found that combined, we all make about $800K per year.

That's Wall Street money, twice what the President of the U.S. makes.

Yet, when you factor in our mountain of bills and high living expenses for various things (like a new car with record-high auto interest rates), it turns out that $800K gets eaten up completely.

What is the lesson here? Two-fold.

First, you need the passive income that safely grows over time, or else you will never truly be "rich."

If you have to bust yourself for a paycheck, it doesn't matter how big that paycheck is, you are not truly financially free.

Trusting the world's best companies, run by millions of hard-working employees and led by the best management teams in the world, is the ultimate way of achieving financial freedom.

Harness the power of global capitalism to make your dreams come true. That is the power of high-yield dividend growth investing.

The most important thing I've learned though is that you have to find joy in everyday life, even when your life is hard.

Ignoring all the bad things going on right now, both for my family and the world life has never been more joyful or fulfilling.

That might sound crazy, and completely delusional, but the idea is that you find hope in a hopeless world by focusing on what you can control, and how you can improve your life in the future.

{kind=link}

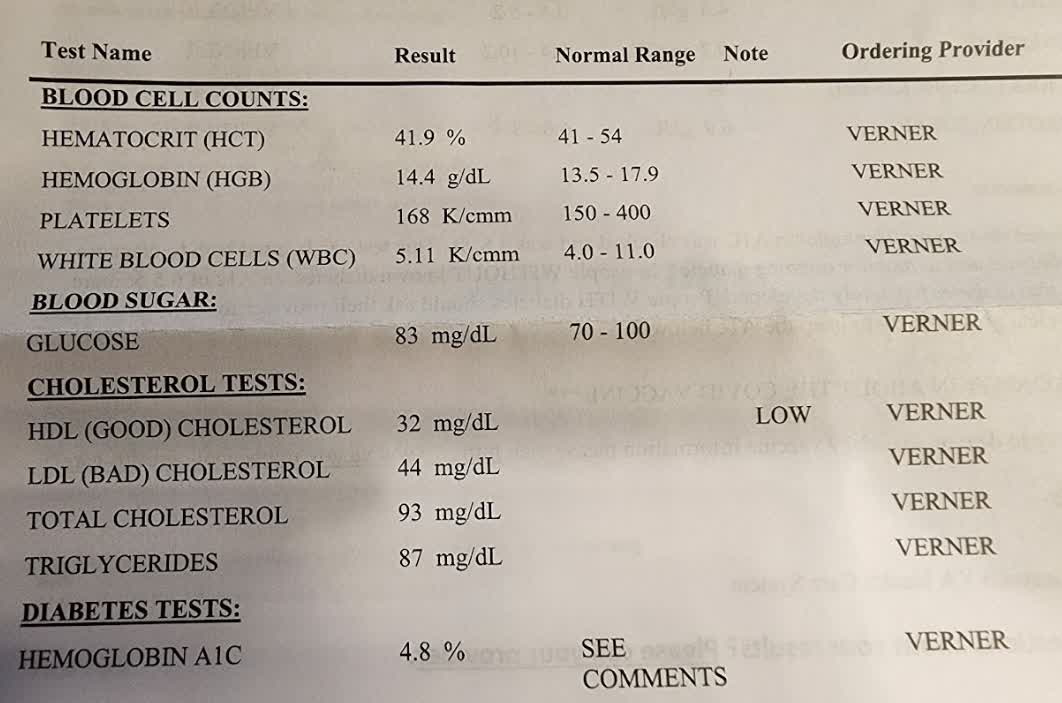

Through diet and exercise (I'm doing it with my grandfather per his doctor's recommendation to save his life), I was able to crash my cholesterol by about 200 points in 6 weeks.

{kind=link}

My doctor told me I was about 2 years away from death the way I was going, but thanks to an optimal diet and exercise (walking) my grandfather and I have a new lease on life.

We're not sure how long this transformation will give him in terms of extra years (up to 15 according to studies), but I get to look forward to well over 50 years (up to 88 years according to science).

And those years will be full of incredible health, vitality, joy, and a sense of purpose beyond anything I've ever felt.

A purpose that my recent family disasters and traumas have taught me about the things that truly matter in life.

- family

- friends

- fido (life isn't really complete without pets)

- Faith (what gives you purpose and strength in life)

- food (healthy food you love)

- fitness (until you're no longer sick, you don't realize the difference).

Well, this portfolio is exactly what my family needs, not just for the near term but for making our long-term dreams come true.

It's what protects us from medical bill bankruptcy.

It's what will fund my parents' retirement dreams.

Buy my sister's homes (at least down payments).

Let me have as large a family as my wife (whoever she ends up being) will bless me with.

Help fund the world's most effective charities ($90,000 in donations this year and hopefully $100,000 next year).

In the decades to come, this portfolio will help me save millions of lives, make the world a far better place, and start a charitable foundation that will one day eliminate global poverty and build a literal utopia over the next 500 years.

Are such dreams realistic? Yes, will they be easy to accomplish? That depends on your perspective.

If you enjoy life, are thankful for the blessings you have, and keep plucking away over time, then yes, you really can move mountains.

The Grand Canyon was formed by water steadily wearing down rock.

With enough time and patience, you can not only enjoy life and thrive through adversity, but you can accomplish miracles.

For further details see:

How I'd Invest $2.5 Million Right Now