JEPI - How JEPI And Other Covered Call Investors Can Cut Risk And Keep Those Dividends Flowing

2023-08-30 09:29:00 ET

Summary

- Covered call ETFs are a great tool, but sometimes they need some help.

- This article shows how and why I often supplement my covered call ETF positions with hedging trades.

- I demonstrate using JEPI and TLTW, though this concept can be applied to any covered call ETF.

If the stock market falls, but can't get up, like that woman in the famous TV commercial, covered call ETF investors could have a problem they might not be prepared for. This article aims to give them a life line, one they may like even if we don't get more than a mild correction for a long time.

Covered call writing strategies are all the rage. ETFs that use them are multiplying like rabbits. And one in particular, JPMorgan Equity Premium Income ETF ( JEPI ), has captured the hearts of investors, amassing more than $28 million in assets in just over three years.

But as I've written before, all covered call strategies have a big risk. It appears in certain types of market declines, and occurs because volatility before the decline was on the low side. That means that the option premiums investors were receiving were lower than they would be when volatility was higher. This is currently the case, and thus the risk, for any covered call ETF that's equity focused. Investors who don't recognize this risk are setting themselves up for disappointment.

Remember that in this "buy the dips" era, it's rare that the stock market gets knocked down and stays down. 15 years of central banks coming to the rescue does a lot to instill confidence.

But since I'm concerned that confidence has, in some quarters of the market, morphed into cockiness and complacency, I wanted to share something I've been doing with my own covered call ETF positions. I'll start with a bond ETF as the first example, then show an example of how the strategy might work using JEPI, which I don't own, but many Seeking Alpha community members do.

Importantly, I would caution readers of this article that my opinion on JEPI as an ETF is not the main point of this article. I rated JEPI a Hold, only because having it as the lead ticker for this article requires that I rate it. As I've written in the past, I have no major issues with JEPI, I just think it's more popular than it should be. And there are issues that can come with size, especially the way JEPI handles its option transactions.

So, to get the most out of this article, I suggest investors focus on the hedging concept I explain, not whether I think JEPI is better or worse than any other ETF in its peer group. That has been covered ad nauseum in the comments section of a couple of previous articles I have written that involved JEPI.

OK, with that out of the way, let's go try to save some money through proactive hedging!

How to reduce potential for major loss when owning covered call ETFs

There are two ways to do this. One involves owning out of the money put options on an index ETF that closely matches the makeup of the equity portfolio you own the covered call ETF on. But options are not for everyone, and so I'm focusing this article on using a second ETF alongside a covered call ETF to:

1. Cut down the potential for major loss

2. Keep the dividend income rate earned from the covered call ETF flowing in, albeit at a slightly reduced rate.

Here's a base-case example using The iShares 20+ Year Treasury Bond BuyWrite Strategy ETF ( TLTW ), which I own in some size in my personal portfolio, alongside a slug of T-bills and some other covered call ETFs. Together, they comprise my retirement income portfolio. I'm only partially retired (in fact my wife says I work more than ever!), but that's because when I sold my financial advisory practice, it simply allowed me that much more time to focus on investment research and developing techniques like this one.

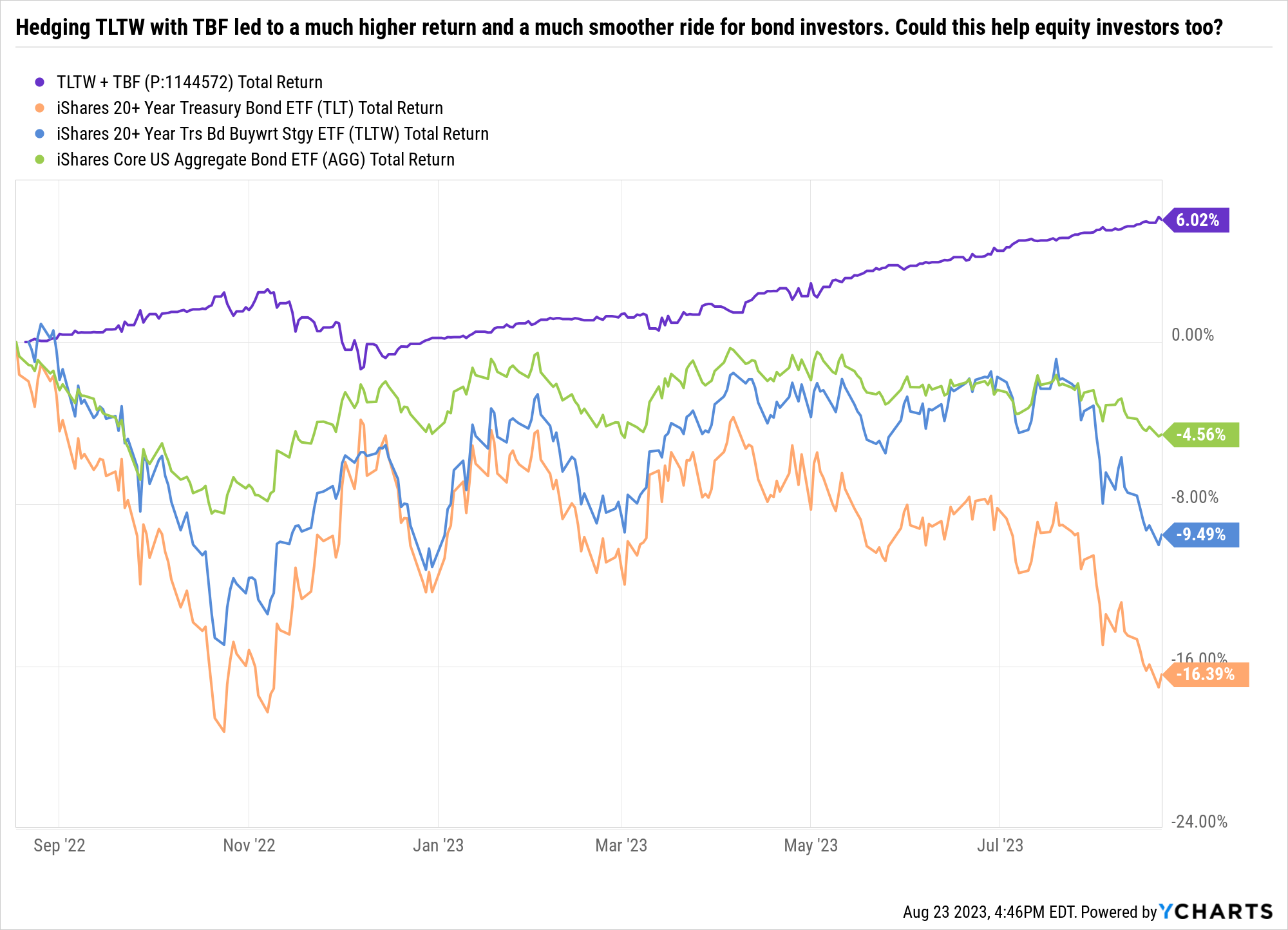

This is just a base example, but intended to allow you to personalize it as you see fit. TLTW just hit its first anniversary. During that 12-month period, it lost 9.5%. That's because iShares 20+ Year Treasury Bond ETF ( TLT ) fell by 16.4%, net of its dividend earnings. TLTW receives monthly cash flow from writing covered calls, close to the money, and refreshing that covered call position each month. That's similar to how many covered call ETFs work, where the covered call part of the strategy is regimented, and the timing is known to investors before they invest.

Sungarden Investment Publishing (using Ycharts)

{kind=link}

It has been a very bad 12-month period for bonds, though the full year 2022 was worse. The chart above shows that the aggregate bond index was off more than 4%. So with all of these negative signs attached to bond ETFs, and the potential for still-higher rates, that could continue the red ink for bonds, what's a TLTW covered call investor to do?

The answer: Hedge it!

What you see above in the purple line is a 50%-50% mix of TLTW and [[TBF]], which is an ETF that shorts the same index TLT is invested "long" in. So it's roughly the opposite. And, in a period like the one we just saw for bonds, pairing TBF with TLTW produced a much higher total return than TLT or TLTW.

This is not the end of the story. After all, we're cutting off a lot of potential return here by using half the portfolio to hedge. But that's the point: There are times in the market cycle, for bonds or stocks, where some hedge or a lot of hedge, can be an elegant way to let, in this case, my TLTW position continue to do its thing as a long-term holding. The nuance is in determining how much to hedge, and that's an individual position. But the concept is there to be had, and you can see how much it helped in a rough period for TLT and TLTW.

JEPI and other covered call ETFs: You can play this game too!

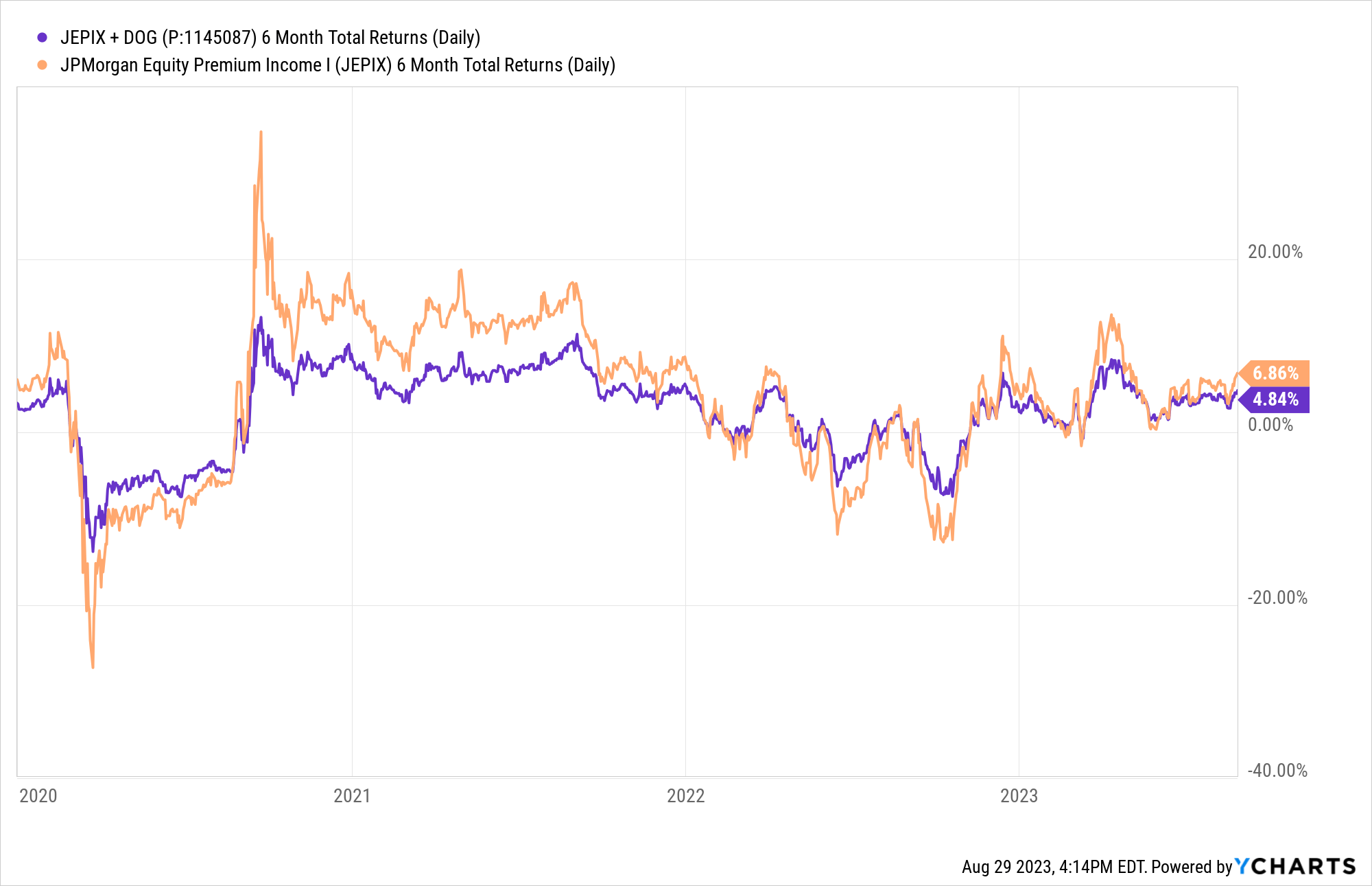

Now, let's take the same concept and apply it to a covered call ETF focused on stocks instead of bonds, using the uber-popular JEPI. I'm actually using JEPI's mutual fund clone, symbol JEPIX, because it has a slightly longer track record than the JEPI ETF, but they move in sync.

{kind=link}

I created a "JEPIX-DOG" portfolio, allocating 80% to JEPIX and 20% to the ProShares Short Dow 30 ETF (DOG), which aims to deliver the opposite return of the Dow Jones Industrial Average. JEPI's portfolio tends to emphasize dividend-paying stocks, so while I'd rather use the S&P 500 as the hedge (which is the index that JEPI targets in its covered call writing activities), this is not the era to hedge a portfolio like JEPI using the S&P 500. That's because that index is so top heavy with tech stocks that don't pay dividends, as well as companies with valuations in the stratosphere, it's nowhere near an apples-to-apples with JEPI. I'd prefer to hedge JEPI using something that better resembles the style of that fund's active stock selection process. So at least for now, in this demonstration, DOG is used to hedge JEPI, and the model portfolio I created is 80/20 JEPI/DOG.

Why bother? Isn't JEPI just perfect on its own?

I suspect a lot of shareholders among JEPI's nearly $29 billion asset base feel that JEPI is fine on its own, and does not need to be hedged, ever. To that I say: Good for you! This and all of my other communications, on Seeking Alpha and elsewhere, all have the same objective: To show investors what I'm doing, based on my experience and my risk tolerance, and after more than 100,000 hours as a professional investor.

My number one rule is ABL: Avoid Big Loss. "Big" is defined differently by every investor, so take this covered call "enhancement" technique I'm describing, and personalize it. Or discard it. Either way, this seems like the ideal time to make public the idea that this is a strategy that any investor can do, if they think it will help them. I know it has helped me to "ABL" over the years.

In that chart, I show the rolling 6-month returns. Much of the time, the 80/20 portfolio is slightly behind JEPI on its own. The math is super easy here. In up markets, a 100% invested portfolio ( JEPI ) should outperform a 100% inverse (short) portfolio, DOG. In down markets, DOG should outperform JEPI. This is the case most of the time, but not all of the time, since JEPI does not behave exactly like a long-only ETF.

The highlight here, for those who do have an interest in hedging their downside, at least some of the time: The 80/20 mix preserved significant capital, as it should have, during the three significant drops in JEPI's value. In early 2020, JEPIX fell 27.2% in six months. The 80/20 mix fell by 13.8% during that time, so it cut out half of the decline.

I know that modern markets have been friendly to the "buy the dip" crowd, and so losses have just about always been temporary. But for those who like the covered call approach, but want to be able to protect that ETF investment and leave it alone from time to time, I think this is good to know.

Relatedly, to me it just helps for peace of mind to have some type of disaster protection alongside of a covered call strategy, which by its very nature provides only a partial cushion against big stock market drops. Even during 2022, when JEPI fell 9.5% and 12.3% during two separate six-month periods, the 80/20 mix limited the damage to 4.9% and 7.1%, respectively.

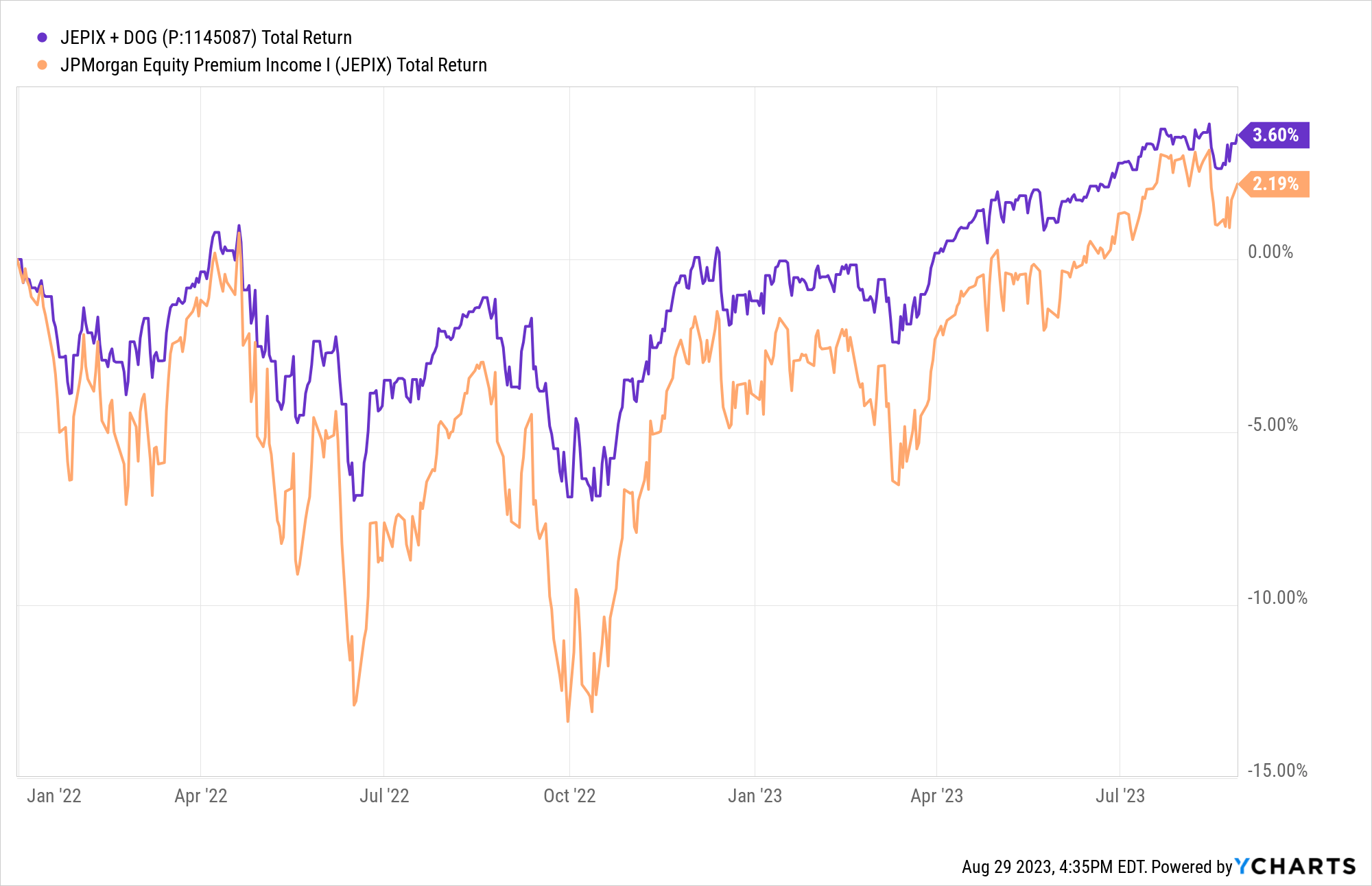

One more picture, and this is probably the key takeaway for folks reading this and on the fence about whether they care about this concept. Below is a chart of the total return of both JEPI and that simple 80/20 mix. I started the tracking on Jan. 1, 2022, which for all we know, could end up being seen in market history as the moment when all previous history became less relevant. After all, it was when we went from 40 years of declining rates to a rapid series of Fed hikes, which made investors realize that bonds can go down in price at the same time as stocks (sorry, 60/40 lovers!).

It's also when, in my opinion, the markets became "everybody's business." We investment pros and geeks used to go about our business quietly, since investing was not so "mainstream." It picked up in the 1990s, accelerated during this century, but now it feels like a huge portion of the population is "in the market" as a trader or at least as a learner. So, these past 20 months may end up being the start of a new investment era, from a participation standpoint.

{kind=link}

Notice what's happened since Jan. 1, 2022. The 80/20 mix has outperformed JEPI, pretty much from day one. Not a landslide by any means. But there have been long periods, as long as a decade or more, when the stock market was more "choppy and sloppy" than anything else. Like I said, we're two years into a period of a lot of up and down, but the net result is a flat S&P 500. So if there's anything an investor can consider to smooth out their performance, albeit giving up a bit of the covered call ETF yield, this is the time to get educated about it.

Conclusion: 5 reasons the modern stock market makes hedging covered call ETFs worth considering

Today's stock market is:

1. Top heavy like we've never seen

2. Emotional as ever, thanks to so much attention, so many players and instant communication

3. Flat for the past two years, based on the S&P 500's return (much worse for small caps, value, international, and just about anything that isn't FAANG-infused)

4. Overpriced from many valuation perspectives (due primarily to those top-heavy holdings)

5. Competing with bonds for investors' attention, given higher bond yields

Those reasons and more prompted me to look into how to take a great concept, covered call writing ETFs, and see if I could apply my risk-management-first approach to it. For what it's worth, I currently own three covered call ETFs:

TLTW, as noted above

Global X NASDAQ 100 Covered Call ETF ( QYLD )

Dow 30 Covered Call ETF ( DJIA )

In all three cases, I'm ready, willing and able to apply a hedge to those positions, either through options or through an inverse ETF method, as I focused on in this article. As a tactical investor, I tend to rotate in and out based on my trusty technical signals, which I have built and used over 30 years.

Not everyone wants to do all of that thinking about their portfolio. They prefer to leave it to the covered call ETF manager, be they active or passive.

To me, covered call ETFs are a great investment consideration, but are best if they are not always left "home alone" so to speak.

For further details see:

How JEPI And Other Covered Call Investors Can Cut Risk And Keep Those Dividends Flowing