SPMO - How Rates Stand After The Fed Pivot

2023-12-27 01:31:27 ET

Summary

- The Fed is signaling rate cuts starting next year.

- Interest is down on the news, and seems to have stabilized.

- An overview of where rates stand after the Fed pivot follows.

Interest rate policy is starting to pivot, with the Federal Reserve guiding for three rate cuts next year . The news have sent markets reeling, with benchmark 10Y treasury rates down 0.50% these past two weeks, 1.0% peak to through. As market conditions seem to have somewhat stabilized by now, I thought to have a closer look at how interest rates currently stand.

Rates are down from their peaks but remain elevated. Bond yields look quite attractive right now, especially compared to equities.

The yield curve is inverted, as the market expects significant rate cuts in the coming years. Expectations are very dovish, so long-term bonds might not necessarily see further gains from here on out.

Credit spreads are wider than in the recent past, and tighter than long-term averages. Default rates are a bit elevated and expected to increase a bit more in the coming months. Investment-grade bonds look more attractive than high-yield bonds right now.

Rates Are Down, But Remain Elevated

Interest rates are down across the board, as Federal Reserve guidance has investors expecting significant rate cuts in the coming years and are re-pricing bonds accordingly. Benchmark 10Y treasury rates are down 0.6% this month, 1.0% peak to through.

Seeking Alpha - Table by Author

Other market interest rates are down too, mostly by more.

Seeking Alpha - Table by Author

Although rates are down from their peaks, they remain elevated on a more long-term basis. Benchmark 10Y treasury rates are currently higher than their post-financial crisis average, and the same is true of most other relevant rates.

Above-average rates increase the attractiveness of bonds as an asset class, for obvious reasons. I've argued the same in the past , and I do believe that most of my top bond picks have performed quite well since.

As an example, my top high-yield bond ETFs have all seen double-digit returns YTD. Equities did outperform, but equities are riskier and current equity returns are probably long-term unsustainable (can ' t expect +25% annual S&P 500 returns forever).

Bond yields also look attractive relative to equities. As an example, the S&P 500 earnings yield is currently quite a bit lower than the yield on BBB-rated corporate bonds, even though equities are much riskier, and junior to bonds.

JPMorgan Guide to the Markets

BB-rated bonds currently yield around 2.0% more than the S&P 500 earnings yield, the widest gap in decades, excluding recessions.

Data by YCharts

As should be clear from the above, high-yield bonds offer very attractive rates right now, relative to their history and equities.

In my opinion and considering the above, income investors, retirees, and investors looking for strong risk-adjusted returns should focus on bonds over equities. I still expect equities to outperform long-term, but at much greater risk.

Inverted Yield Curve

In the vast majority of cases, long-term bonds have higher rates than comparable short-term bonds, as compensation for their increased duration, and for tying up investor capital for longer.

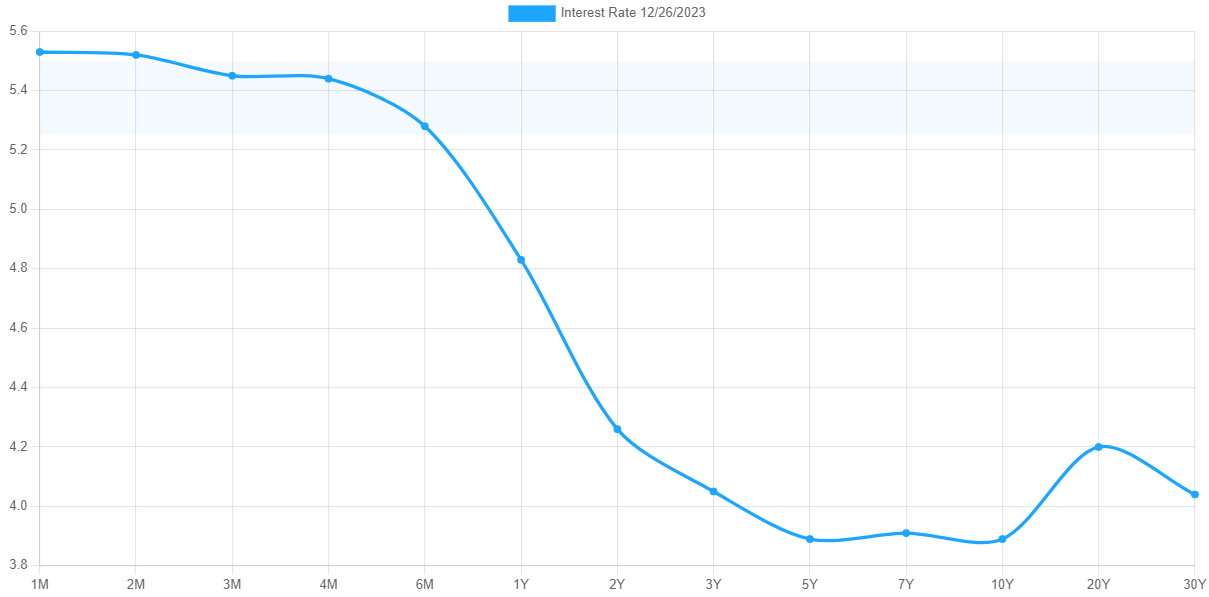

Right now the opposite is true, with long-term bonds generally yielding less than comparable short-term securities. As an example, the current treasury yield curve.

{kind=link}

As can be seen above, treasury yields uniformly decline from the 1M to the 5Y mark and oscillate thereafter. These declines are due to market expectations of future rate cuts. 10Y treasury rates at 3.9% seem unattractive with T-bills at 5.5%, less so if the Fed cuts rates to 3.0% and lower in the coming years.

The higher yield on short-term bonds is a straightforward, significant benefit for investors. Said benefit is of particular importance to more risk-averse, short-term investors, who can receive strong income with very little risk by investing in said securities. For these investors, T-bills are a natural choice. The Janus Henderson AAA CLO ETF (JAAA) is another solid choice, with a growing 6.0% yield. I last covered JAAA here .

The higher duration and interest rate exposure on long-term bonds could lead to significant capital gains, depending on Fed policy and market expectations thereof. Which brings me to my next point.

Dovish Market Expectations

Right now, the market expects significant rate cuts in the coming years. As per market-based treasury futures, investors expect Fed rates of 3.75% - 4.25% next year, equivalent to 5 - 6 cuts.

CME

As the market is pricing-in several rate cuts already, longer-term treasury yields might not necessarily fall all that much in the event of moderate rate cuts. In other words, longer-term treasury yields are already down due to rate cut expectations, further declines might not occur.

Seeking Alpha - Table by Author

Importantly, investors expect more rate cuts than the Fed itself, which is guiding for around 3 - 4 cuts next year.

Federal Reserve Projections

In my opinion, the above issues imply the following.

Long-term bonds should yield more than short-term bonds sometime around 2025 - 2026, as per Fed guidance. As such, long-term bonds should somewhat outperform short-term bonds in the coming years.

Significant, sharp interest rate cuts would almost certainly lead to materially lower long-term rates and significant long-term bond outperformance.

Slower, shallower rate cuts should not lead to significant decreases in long-term rates or significant long-term bond outperformance, as these are priced-in already.

Although long-term bonds should outperform short-term bonds from here on out, their overall risk-return profile seems a bit weak.

Short-term bonds yield more than long-term bonds right now and with much lower interest rate risk or volatility. In most cases, focusing on higher-yield, lower-risk securities are the obvious play. Conditions will likely change in the next few years, but they genuinely might not.

In most cases investors demand a higher yield on long-term treasuries for taking interest rate risk. Accepting a lower yield because maybe T-bill rates will significantly decrease a year or two from now is a much worse trade or situation than average. Don't lose sight of the fact that the current situation is abnormal and that short-term bonds are rarely as attractively priced in relation to long-term bonds as they are right now.

In my opinion, and considering the above, I lean towards shorter-term and variable rate securities on risk and risk-adjusted return grounds. Some of my favorite funds in this space focus on CLOs, as these investments offer very competitive yields. These include the Janus Henderson AAA CLO ETF ((JAAA)), with comparatively low risk and a 6.0% yield, the Janus Henderson B-BBB CLO ETF ((JBBB)), with a bit more risk and an 8.0% yield, and the Panagram Bbb-B Clo ETF (CLOZ), with the highest risk, and the highest 9.8% yield of the bunch.

Credit Spreads

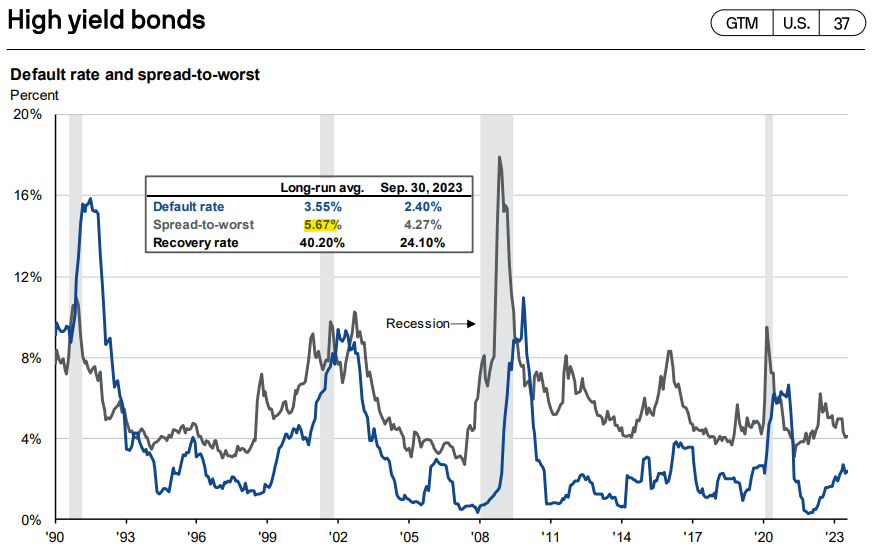

Non-investment grade bonds almost always yield more than investment-grade bonds, to compensate investors for the added credit risk. Spreads do vary, and currently stand at 3.4%, slightly higher than for the past three years:

but quite a bit lower than their long-term historical averages:

{kind=link}

At the same time, corporate default rates are slightly higher than their long-term averages. JPMorgan ( JPM ) estimates default rates at 3.6%, S&P at 4.1%, compared to a historical average default rate of 2.4%.

Considering the above, high-yield bonds look somewhere between the same and somewhat worse than investment-grade bonds. I am quite bullish so think high-yield bonds will perform quite well regardless, but the data does somewhat tilt the other way. Waiting for wider spreads might be a good idea: these were around 1.0% wider a few months ago, and 0.5% more a few days ago.

There is something of a dearth of particularly strong investment-grade bond ETFs. Most are adequate , including the iShares iBoxx $ Investment Grade Corporate Bond ETF ((LQD)). JAAA and JBBB both focus on investment-grade CLO tranches, although some investors might prefer fixed-rate alternatives.

Conclusion

Right now, nominal rates are above historical averages, the yield curve is inverted, and credit spreads seem about average. Under these conditions, short-term, investment-grade bonds seem to offer particularly compelling risk-adjusted returns.

For further details see:

How Rates Stand After The Fed Pivot