DGL - How To Be A Successful Gold Stock Investor Part 2

Summary

- It's a substantial advantage if an investor understands the story and spots the catalysts before the market.

- There are many aspects that need to be analyzed when looking at mines or projects and determining whether they are solid or not.

- I can give countless examples of how playing the divergences helped me to outperform in this sector.

- If your research forms a different conclusion than what company execs are expounding, then trust your own data. Sometimes it's best to take what management says with a grain of salt.

- Have a game plan. This is not a sector where one should sit on their hands or become a deer in headlights when a mega-move is starting to develop.

This is Part 2 of my series, "How To Be A Successful Gold Stock Investor." You can find Part 1 here .

Spot The Positive Catalysts Before The Market Does

One difference in the mining sector is that bullish catalysts that could hit within the next 6, 12, or 24 months are rarely priced in early. It's almost as if the market is unaware of what's about to occur (similar to the red flags discussed in Part 1), and it's only after the fact that companies will see their stock price re-rated higher. It's a substantial advantage if an investor understands the story and spots the catalysts before the market.

Whatever the reason for this delay—the complexity of these technical reports (which most investors don't want to dig into), the interpretation needed when it comes to drill results, the lack of understanding of the cash flow impact, etc.—the point is, there are significant windows of opportunities in this market to get in early before positive catalysts are priced into shares.

Typically, it's a new mine that's about to enter production that will result in a re-rating, but there are a host of other bullish catalysts that could positively impact a stock, including:

- The discovery of higher-grade reserves, which could dramatically increase production and lower costs.

- Additional reserves/resources that could result in a 2x increase in the NPV of a project in development or a currently producing mine.

- The completion of an expansion project that will result in a boost in throughput and lower costs.

Technical reports contain a wealth of information. A simple analysis of the life of mine and the breakdown of production year by year lets investors know when more robust mining years will occur.

There are too many examples to list; the point is, if you know ahead of time what companies are better positioned over the next 6-12 months than they were before, then you should have more success in this sector.

Know How To Distinguish A Quality Mine/Project From One That Is Sub-Par

There are numerous facets that investors need to pay attention to when analyzing a mine or project to properly determine whether they are dealing with something of quality or something that might be a little "let's put some lipstick on this pig."

I already discussed grade, reserves, strip ratio, and other aspects in Part 1, which are critically important when determining whether a mine or project is high quality, average, or poor quality. But it goes far beyond those criteria.

What's the production profile? Is it lumpy? I'm looking for consistency, but I also understand that there will sometimes be fluctuations given higher strip ratios in some years, grade variability, etc.

Is it back-end loaded or front-end loaded? Front-end loaded means that there aren't enough reserves, and production will fall off a cliff in 3-5 years if the company can't find additional ounces at similar grades. If it's back-end loaded, then that means that the NPV is going to suffer because you are delaying that cash flow.

A shorter overall mine life (5-7 years) is acceptable if I'm dealing with a company that has a mid to high-grade underground mine, as it's far more efficient to drill closer to the ore body to prove up additional ounces and extend the mine life, rather than trying to drill from surface. Many underground mines have a relatively short mine life, but reserves are continually replenished and mine life is extended. That's typically not the case for open pit operations.

What are the all-in sustaining costs (or AISC)? Inflation has resulted in an increase in AISC over the last few years.

In 2014-2018, when gold was in the $1,100-$1,300 range, a mine producing at an AISC of $800 or below was exceptional, while a mine with an AISC of $1,200 per ounce was considered low quality. Today, a $1,200 per ounce AISC operation is about average and still generates strong free cash flow, while anything at $1,000 per ounce or below is considered top-shelf.

AISC for the industry will constantly move higher over time, and it's all about the margin of those ounces.

In the current environment—with gold above $1,900—I'm comfortable up to about $1,350 per ounce AISC. I would still consider that acceptable, but I would also want to see the potential for cost reductions in the near-term. Mines or projects with higher costs (e.g., $1,500-$1,600) could be problematic and tend to see further cost escalations.

Are costs also consistent year-over-year, or will there be significant fluctuations? That's important as well.

How deep is the mine? If it's underground, the deeper you go, the more costly and difficult it is to mine. 2,000 meters below the earth's surface, and you will be dealing with many more challenges than you would at a depth of 500-1,000 meters. A ramp system has limitations as mines get deeper, and then a shaft is a must (which is a considerable expense and time-consuming to build).

The more shallow the underground deposit, the better.

The same applies to open pits, although a deep pit can be tackled much easier than a cavernous underground mine. Again, though, it all comes down to strip ratio, grade, etc.

Sulfide vs. oxide ore. Oxide reserves/resources can be heap leached, while sulfides will need to be processed.

What are the after-tax NPV (5%) and IRR? The return of any project is critical and will be the deciding factor for whether it's built. Some companies have an internal target where they will only construct a mine if the IRR is at a certain threshold (e.g., 20%, 25%, etc.).

If you have a mine with a paltry NPV at $1,500 gold, then that's a problem. Some projects have a negative NPV at that gold price and are low-quality deposits that have no hope of ever being built. I avoid these as I don't care how much gold there is in the ground; if there is no chance of it ever being extracted, this is simply a "greater fool" investment.

Obviously, the higher the NPV, the better, but a project with a low NPV might not tell the whole story either. There are many projects that will clearly see a vast improvement in economics if there is mine-life extension or an increase in grade. Many gold discoveries are still in the early stages of being proven up, and more drilling could result in a 2 million ounce deposit/project with an NPV of $500 million becoming a 4 million ounce deposit/project with an NPV of $1+ billion. In other words, you can't judge the current economics without doing a little digging first to see if there could be substantial upside to the mine life, reserve grade, etc.

Location is important, but I'm willing to overlook some jurisdictional risks if there are many positive aspects of the project. Canada, the U.S., and Australia are top mining jurisdictions. But you have to be more careful with specific regions in these countries. A project in California will have a tougher time getting permitted than one in Nevada.

Mexico is usually a good jurisdiction to mine, but much stricter environmental regulations over the last few years have heightened the risk and made it more challenging to get a project approved (especially open pit mines).

Latin America is hit or miss, with Chile, Argentina, and Peru decent jurisdictions, but it's also dependent on the province as well. The political climate in South American countries is also constantly changing, so one needs to keep up with elections and the next administration's view on mining.

Some countries in West Africa are acceptable (Ghana, Cote d'Ivoire, etc.), but these are still higher-risk regions.

There are many aspects that need to be analyzed when looking at mines or projects and determining whether they are solid or not. There are always going to be trade-offs, and rarely will you find one that checks off all of the boxes. But there are also clear winners and losers. It's important to be able to distinguish between the two.

Playing The Divergences Is A Must

One thing vital to outperforming in this sector is to play the divergences. Often, some gold miners become more overvalued compared to others, and vice versa. Sometimes that's because of bullish/bearish catalysts; sometimes, there is no rhyme or reason, and sentiment is driving the share price to the extremes.

All of these companies are mining the same end product and selling it for the same price. And I have no attachment to any company in this sector. If I own a stock that has notably outperformed and its relative value isn't nearly as appealing as it was before, I will typically rotate into another quality gold stock that has either underperformed the group or underperformed relative to the stock I'm selling.

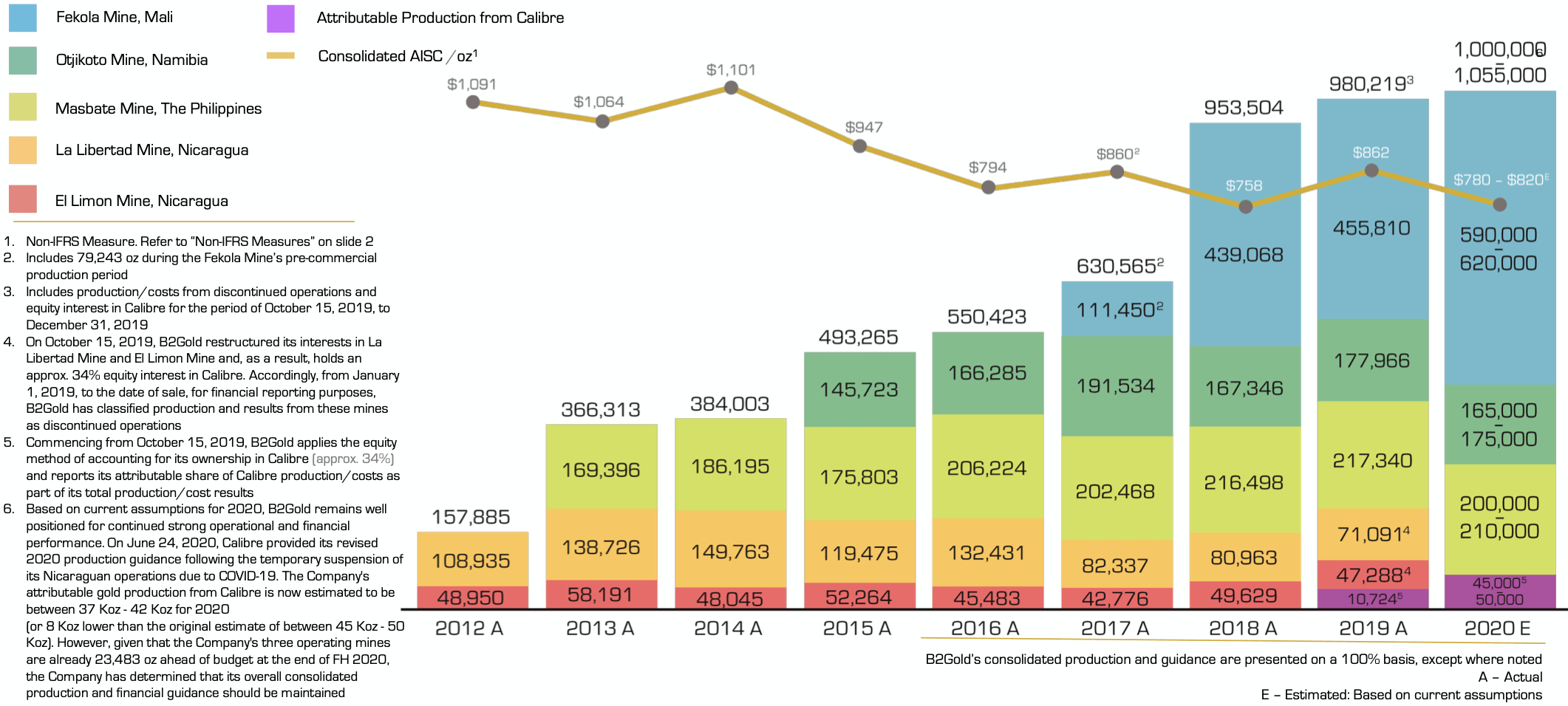

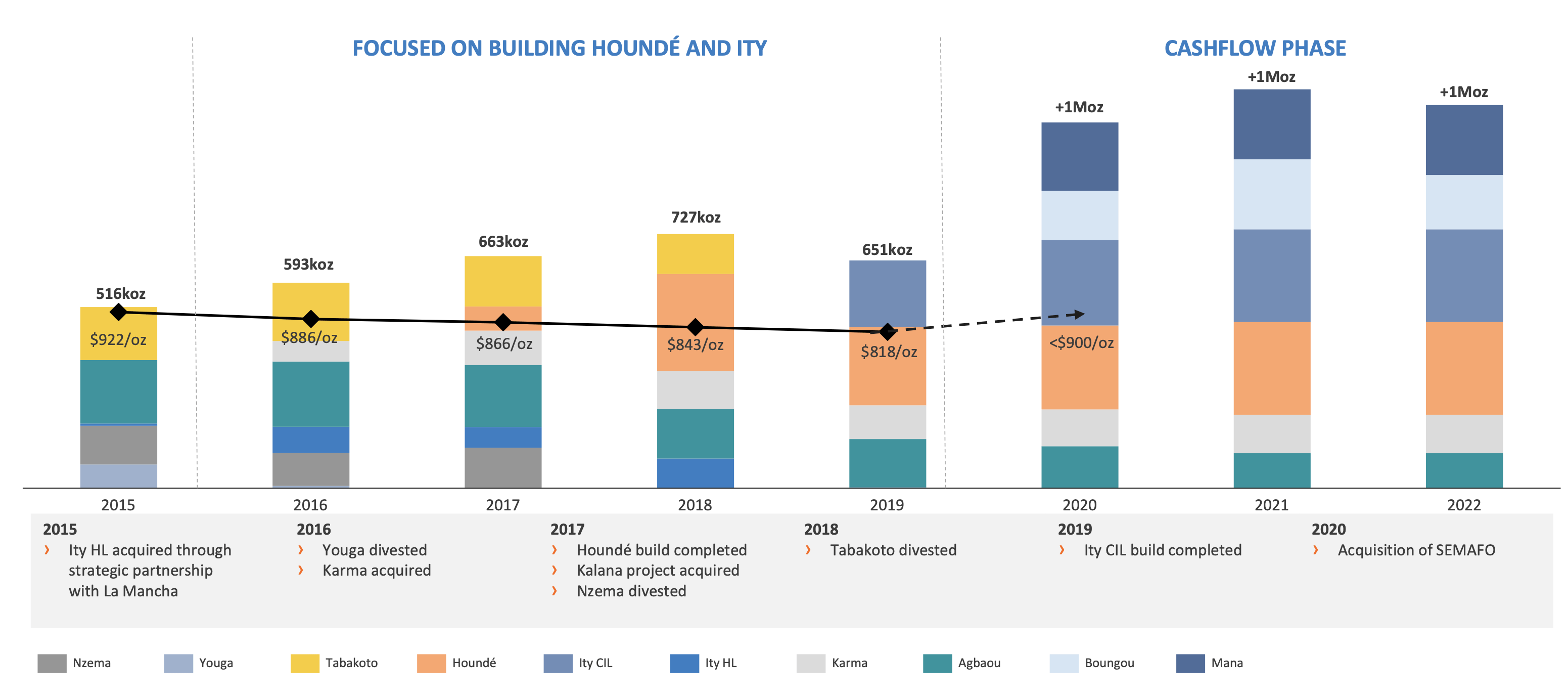

For example, in July 2020, I discussed with subscribers of The Gold Edge how the performance difference between B2Gold ( BTG ) and Endeavour Mining ( OTCQX:EDVMF ) over the previous three years resulted in EDVMF trading at a significantly lower relative value compared to BTG. The gap in enterprise value was US$2.25 billion between the two miners, and this divergence wasn't warranted.

At the time, B2Gold's 2020 production and cost estimates of 1,000,000-1,050,000 million ounces of gold at an AISC of ~$800 per ounce (top graph) were similar to Endeavour's 2020 production and cost estimates of 1+ million ounces of gold at an AISC of under $900 per ounce (bottom graph). The two companies had virtually identical production and cost profiles, were generating tremendous cash flow, and the jurisdictional risks were similar as well. The only advantage that BTG has over EDVMF was net debt was around $0, while Endeavour had about $400 million of net debt, but that was already accounted for in the enterprise values discussed above. An advantage for Endeavour was it was much more diversified, which is a huge plus as it greatly lowers the risk should one operation experience a disruption.

{kind=link}

B2Gold

{kind=link}

Endeavour Mining

EDVMF was the better play going forward, even as a more defensive pick, as the sector was overbought at the time. So I sold BTG and bought EDVMF. EDVMF notably outperformed BTG (and the HUI) over the next 12-18 months, popping its head in positive territory several times, while BTG was down 30-40%. Even today, EDVMF is only down a little more than 9% since July 2020, while BTG is down over 40%, and the HUI is down almost 25%.

I can give countless examples of how playing the divergences helped me to outperform in this sector. Have absolutely zero attachment to these gold stocks, and don't be afraid to sell out of an entire position that has become greatly overextended relative to others in the sector.

Take What Management Says With A Grain Of Salt

If the management team of a gold mining company is telling investors one thing, and your research and opinion of the situation match the expectations being set by management, then that's a good sign. If, however, your research forms a different conclusion than what company execs are expounding, then trust your own data. Sometimes it's best to take what management says with a grain of salt.

Gold mining executives have a tendency to downplay bad news (no surprise) and overpromise on future results. Some might say this is a problem with all sectors, but the mining industry has some of the worst offenders. This isn't because every CEO is shady or is trying to pull the wool over investors' eyes; it's because gold mining is a business where no matter how strong the technical report or how much drilling has been done, there are still many unknowns. It's a tough business.

If you think about what these companies are trying to do—pinpoint exactly where the ore is underground, estimate the grade and ounces throughout the entire deposit, and then extract all of this gold in the most economical way possible—it's certainly not an easy task.

That's why you often see gold miners disappoint, especially when it comes to longer-term projections, which are even more susceptible to downward revisions.

In some instances, they're clear signs that a company won't be able to meet its stated objectives. Management might indicate that everything is fine and stick with guidance, but some due diligence contradicts that rosy outlook and the ability of the company to hit its targets.

Mining companies have gotten much better over the last few years and have learned that it's best to be conservative with guidance and setting expectations. But there are still too many companies that fail to achieve targets because they're way too aggressive with their assumptions, underestimate the problems that are occurring, or they're simply incompetent.

Sometimes, the management succeeds and fixes a problem; sometimes, they fail miserably. Some split the difference, and a mine continues to produce, but expectations for the operation (or the company as a whole) are reset much lower.

Often it just boils down to simple logic. At a certain point, you start to question the statements from management.

I'm not suggesting that investors ignore everything that management tells them; rather, only if your own research and/or opinions don't arrive at a similar conclusion, then don't be swayed by what the company is saying.

Weight Accordingly And Maintain Solid Diversification

Diversification and proper weighting are tremendously important when investing in this sector. I discussed this as well in my recent article, " Building The Perfect Gold Stock Portfolio. "

If this industry had a better track record of execution, then diversification might not be as high on the list of requirements. But considering the difficulties these companies face, and the fact that issues can hit suddenly out of nowhere, it's imperative to be well insulated from potential soured investments.

I understand the desire to find that huge winner that just runs and runs. If an investor spots a "can't miss" opportunity, the temptation is to get very aggressive and load up. But failing to factor in the potential risks of deploying that strategy can lead to rapid and staggering losses in this sector if one goes too heavy on a single play.

Weighting is just as critical as diversification, as weighting can help to adjust the risk exposure of a basket of gold stocks. How I weight a stock depends on several factors: jurisdictional risks, balance sheet, diversification, growth outlook, and AISC, to name a few.

If it's a well-diversified, low-cost, quality senior producer with a stable balance sheet, then I could go very high on weighting. Agnico Eagle ( AEM ) would be a good example. If it's a risky junior explorer/developer - albeit one with an excellent asset - I will likely have a lower weighting. If it's a compelling small or mid-cap, but there are still some strikes against it (jurisdiction, etc.), I might have a weighting somewhere in the middle.

You Must Have A Game Plan

Gold stocks are volatile investments. When the HUI moves to the upside or downside, it can do so in a hurry. After the lows were hit in early 2016, it took just three weeks for the index to increase by 50%. Then the HUI kept going vertical and didn't stop until it was sporting a gain of almost 200%, all over a period of just six months.

Most investors missed the early stages of that run—when the majority of the profits were realized—because their reaction time was too slow, and they didn't know what to do. Many delayed getting in until the tail end of that surge, and by that time, it was way too late, and those investors were left holding the bag.

The same could be said about the lows hit last September. How many are still on the sidelines—after the HUI has already increased over 50%—waiting for gold stocks to drop again?

This is not a sector where one should sit on their hands or become a deer in headlights when a mega-move is starting to develop.

The key to not reaching that "frozen state" is having a game plan. If you are on the sidelines and waiting for a bottom, have a list of stocks ready, know precisely which ones you want to buy and in what order, and have a strategy for those buys.

Usually, when trying to time a bottom or top, I will scale in or out and use target price levels for the HUI and/or gold as my buy/sell indicators. For example, at the lows last September, I took a chance and increased exposure to 70-75% but then waited for further confirmation that a potential low was in place before adding more to my positions. I used the HUI as my guide and increased exposure in 5-10% increments as the index cleared specific price targets (e.g., 190, 210, etc.). I knew exactly what I would do if the HUI hit certain levels, and most importantly, I executed when it did.

I'm always sharing my game plan in every sector update on The Gold Edge.

Paying attention to major breakout levels and knowing what to do when they are breached is also very important and should be part of any solid blueprint. We are on the verge of one now in gold, so it's critical to be well-positioned before that event, or if you aren't, then know what you will do to get positioned.

The same applies when the sector breaks down or enters a deep correction. It's pivotal to be quick in order to protect profits and capital. Know where the key support levels are, and then know what you will do if those are breached.

Having a game plan in place has helped me to avoid sizable losses in gold stocks during the downturns and profit immensely on the reversals and breakouts.

The Patient Gold Stock Investor

In 2015, my message to gold stock investors was simple: anybody paying attention to the sector at the time was likely to do very well as a bottom was fast approaching.

Those that remained engaged and took action profited handsomely.

When gold stocks are getting trashed, that's when investors should have laser-like focus, as there are usually tremendous opportunities brewing.

Taking the opposite approach and straying from the sector because one is losing patience is the downfall of many.

I'm not suggesting that investors should have exposure during these trying times; rather, they should be patient and be ready to deploy funds aggressively when appropriate.

Investors that are moving on from this sector are likely doing so at exactly the wrong time, just like the ones that bailed 5-6 months ago.

It's the same when it comes to individual gold mining stocks. If there are bullish catalysts on the horizon but the stock is doing nothing, losing patience and selling will likely result in a critical missed opportunity.

In Summary

Being a successful gold stock investor is achievable, and one can consistently make money in this sector and outperform. Here are some essential things to understand that should help all that invest in gold miners:

- Pay attention to the balance sheet and never underestimate the importance of the financial condition of a gold company. If there is debt, look at the cash flow and the NPV of assets. Do the math and decipher whether there is a potential issue with repayment. Debt is only troubling if a company has no means to repay it. If it's an explorer, make sure it has ample cash to advance its project over the next 12+ months.

- Grade is king. Reserves are only relevant if the grade is there. Don't get hung up on the size of the reserve base because it's the quality of those reserves that's most important. Having a substantial amount of reserves means little if they are uneconomical to mine. Also, never underestimate the importance of the width of drill intercepts or veins/orebodies, strip ratio, and other characteristics of a project or mine.

- Be careful with the small-scale miners; they likely do not have the experience/expertise to operate their mines and/or build their projects efficiently. Small mines rarely become big winners. Investors should also proceed with caution when it comes to explorers and not overload their portfolio with these high-risk micro-caps.

- Know potential red flags, and don't ignore bearish events when you spot them. It's important to be flexible in this space. If the story changes, accept the new reality and take decisive action.

- There are major windows of opportunity in this market to get in early, well before positive catalysts are priced in. Understand when those are taking place and then react accordingly.

- Know how to distinguish a quality mine/project from one that is sub-par.

- Playing the divergences is a must and can lead to substantial outperformance.

- Sometimes it's best to take what management says with a grain of salt. If your research comes to a different conclusion than what company execs are expounding, then trust your own results.

- Diversification and proper weighting are tremendously important when investing in this sector.

- This is not a sector that one should sit on their hands when a serious move is starting to take shape. Having a game plan in place will help investors avoid that "frozen state."

- When a market is getting trashed, that's when the focus should become laser-like, as there are usually tremendous opportunities brewing. Investors often lose patience and interest in gold stocks at or near the bottom.

For further details see:

How To Be A Successful Gold Stock Investor, Part 2