FG - How To Benefit From Brookfield's Acquisition Of American Equity

2023-07-17 11:35:14 ET

Summary

- Brookfield Reinsurance has agreed to pay a high price for AEL. It underscores the value of annuity business for alt managers.

- BAM will benefit by adding ~$51B of AEL investments to its AUM. However, the immediate effect of this acquisition is rather small compared with other factors.

- F&G will remain the only independent pure annuity provider and is likely to be acquired in about two years or so.

- The acquirer is expected to pay close to ~$44 per F&G share, generating ~40% annual return plus a ~4% dividend for investors.

On July 5, Brookfield Reinsurance ( BNRE ) announced a definitive agreement to acquire all the outstanding shares of American Equity Investment Life Holding Company's ( AEL ) common stock that it does not already own.

Each AEL shareholder will receive $55 per AEL common share, consisting of $38.85 in cash and $0.49707 of Brookfield Asset Management ( BAM ) class A share (equal to $16.15 based on the undisturbed 90-day volume-weighted average share price of BAM on June 23).

These two paragraphs represent the starting point of our analysis. But before moving further, I have to describe AEL in the briefest possible way.

AEL is an insurance company that issues fixed and fixed index annuities to (future) retirees. A fixed annuity is a promise by an insurer to credit fixed interest for a determined term on a retiree's contribution. Compared to bank CDs, fixed annuities have a big selling point: interest is tax-deferred until withdrawn.

Fixed indexed annuity adds a kick by offering potentially higher appreciation linked to an index, usually to the S&P 500. While its appreciation rate is lower than the index appreciation in good years, a certain minimum return is guaranteed even in bad years. The insurer does not expose itself to equities. Instead, it purchases call options that provide appreciation but limit risks. Fixed indexed annuities are a hot product for retirees who want to benefit from the stock market but do not want to be exposed to its vagaries.

Annuities represent a multi-year commitment from a retiree as it is costly to withdraw prematurely: they are protected by surrender fees for the first 5-7 years, by a market value adjustment if a retiree decides to take advantage of higher interest rates before the term expiration, and by a 10% tax penalty if a retiree withdraws before turning 59.5 years. Still, mass surrenders are the most significant specific risk that annuities providers are facing. However, short of a truly disastrous economy, this risk appears remote. For example, during the recent banking crisis, when customers were withdrawing deposits, annuity surrenders did not increase.

Insurers invest contributions into mostly fixed-income assets earning higher interest than what is promised to retirees. This spread less operating expenses becomes insurers' most important source of income.

Brookfield and AEL

Is there anything surprising in the acquisition terms? In my opinion, it is the consideration that Brookfield agreed to pay.

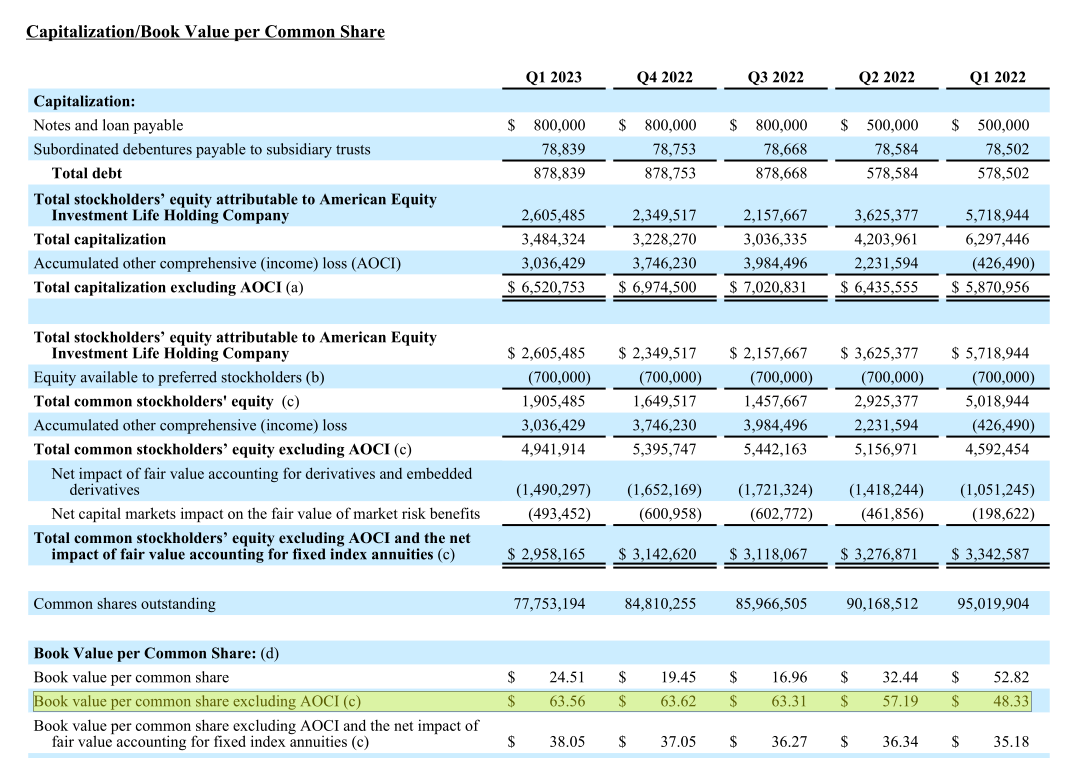

As often with life insurers, it is next to impossible to decipher AEL's GAAP statements, and both management and analysts are typically using adjusted non-GAAP numbers. The book value per share ("BVPS") is the easiest metric to value insurers.

For BVPS, AEL reports three sets of data - book value, book value excluding AOCI (accumulated other comprehensive income), and book value excluding AOCI and the net impact for fair value accounting for fixed index annuities. Of those, BVPS excluding AOCI seems the best metric. Simply speaking, AOCI represents an increase or decline in the value of bonds due to interest rate movements. Assuming no defaults, AOCI is a temporary distortion that will disappear at bond maturity.

On the slide below, BVPS excluding AOCI for the last five quarters is marked in yellow.

{kind=link}

Superficially, Brookfield seems to acquire AEL at 55/63.56~87% of its BVPS excluding AOCI, or at a 13% discount. But this is only due to a new accounting standard adopted by AEL on Jan 1, 2023 (it is called Targeted Improvements to the Accounting for Long-Duration Contracts, or LDTI, that I will not delve into).

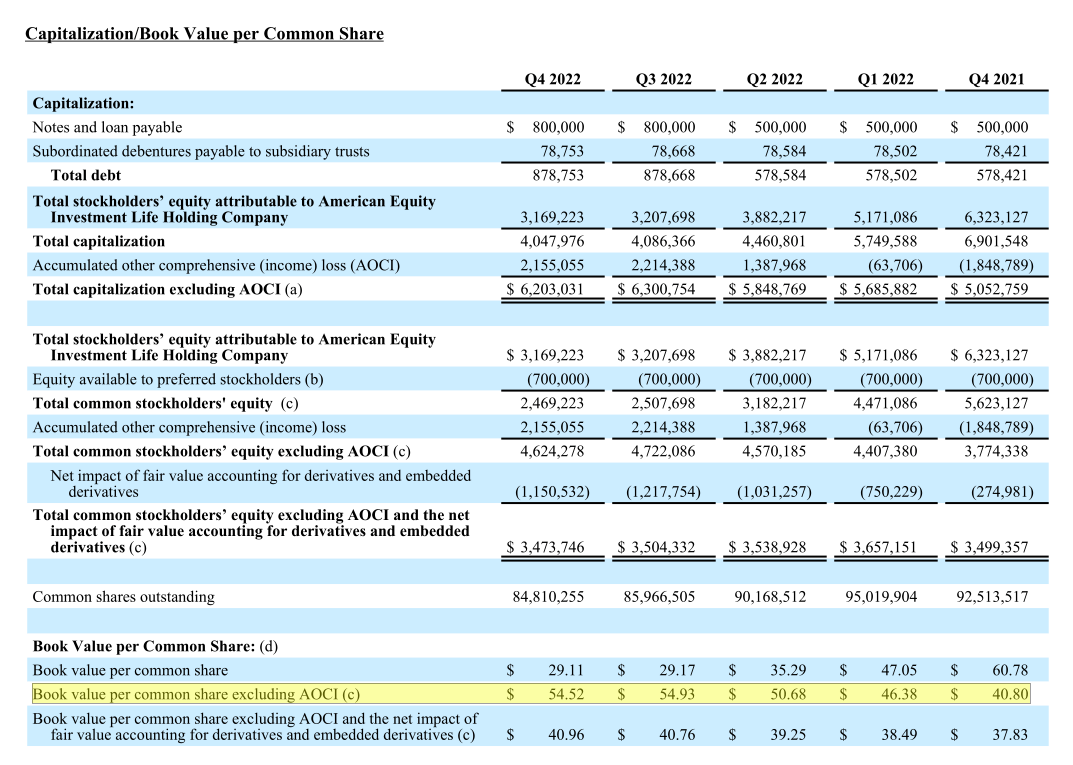

Let us take a look at the same table on Dec 31, 2022, without LDTI.

{kind=link}

Comparing two tables, $54.52 on Dec 31, 2022, without LDTI, became $63.62 with LDTI. Correspondingly, $63.56 on March 31, 2023, should be ~$54 without LDTI. Now we understand the nature of the $55 per share acquisition consideration - it is slightly above BVPS ex-AOCI following the old accounting standard.

Based on the same old accounting standard, acquirers tended to pay for fixed annuities companies either something close to BVPS ex-AOCI when interest rates are low or at a discount to BVPS ex-AOCI when interest rates are high. For example, in late 2022, a consortium offered to acquire AEL at $45. Or in late 2020, KKR ( KKR ) acquired General Atlantic at BVPS ex-AOCI. Paying above BVPS ex-AOCI while interest rates are high is unusual.

Moreover, BNRE had to pay ~30% of the merger consideration with BAM shares to reach the agreement. And this is something that surprised me even more than the high price.

BAM shares represent the crown jewel of Brookfield Corporation's ( BN ) holdings. In its turn, BNRE is a Bermuda BN subsidiary. So BNRE will acquire BAM shares from its parent (likely either for cash or issuing preferred shares to BN) to deliver them to AEL shareholders.

Here are a couple of numbers to understand the importance of BAM shares. The current BN's market cap is ~$53B. The fair value of BAM shares on BN's balance sheet is ~$39B (technically BN owns 75% of Brookfield's asset manager rather than BAM stock directly but it does not matter here) i.e. BAM shares represent 74% of BN's value.

BAM is trading at ~4% dividend yield paying out 90% of its earnings. The best comp is another asset-light and management fees-centric alt manager Ares ( ARES ) that is trading at a 3.3% yield with a similar payout ratio. In addition, Ares has arguably an inferior business compared to BAM. So, BAM seems 15-20% undervalued. This makes the acquisition even more expensive.

Brookfield has valid justifications for making such a substantial payment. Without delving into the specifics of their motives, it is important to note that annuities already constitute a sizable and expanding market. With the retiree population in the US rapidly increasing as baby boomers exit the workforce and advancements in healthcare leading to longer lifespans, the value of scaling up Brookfield's annuities business becomes evident through the AEL acquisition.

How to benefit - BAM

BAM seems the first beneficiary that comes to mind. Without spending a dime, BAM's assets under management ("AUM") will increase by a cool ~$51B of AEL's investment portfolio. Since BAM charges BNRE fees to manage investments, BAM's fee-related earnings ("FRE") will increase. Does it make BAM more valuable than before the acquisition?

Yes, but marginally so due to several reasons. Typically, alt managers charge insurers a fee equal to 0.20-0.30% of their AUM. In addition, incremental fees may or may not be charged for providing certain alternative assets. The contracts are normally long-term but may be terminated by both sides. Significant parts of AEL's portfolio are already managed by several alternative managers and these contracts have to expire or get terminated before BAM gets involved.

Another part of AEL's portfolio consists of plain bonds and until they mature, BAM will not be necessarily involved either as it cannot add any value.

Finally, while the BNRE portfolio is advised (or managed) by BAM, it is sub-advised by a credit specialist Oaktree, two-thirds of which is owned by BAM. In addition, Oaktree margins are twice lower than BAM's. It means that only a small fraction of the fees charged by Oaktree will end up as BAM's FRE.

Long-term, BAM will benefit from the acquisition but the initial effect will be rather small. In my opinion, BAM should rise because of other reasons rather than from this acquisition.

So far, BAM has reported only one full quarter of earnings and this quarter was rather mediocre without quarter-to-quarter FRE growth. Normally, BAM's FRE grows 15-20% per year or 4-5% quarter-to-quarter. Once FRE starts growing from private funds in infrastructure, renewables, private equity, and real estate rather than insurance, its dividend will grow as well, and the stock will be rerated at a lower yield. Even modest 10% FRE growth for the rest of this year and rerating at, say 3.5% yield, should deliver about 25% appreciation towards the end of 2023. This effect is much stronger than marginal positives from the AEL acquisition to be closed next year.

How to benefit - F&G Annuities And Life

In my opinion, the most obvious beneficiary of the acquisition is F&G Annuities & Life ( FG ). F&G is very similar to AEL and focused on fixed annuities (and similarly structured products) as well with negligible Life business. This April, I published "F&G Annuities and Life: Likely Acquisition Target With Projected 30%+ Annual Return" with a company description. I will update my investment thesis below and suggest checking the previous publication for details.

Back in April, there remained two independent pure fixed annuities companies - AEL and F&G. All other players had been already acquired by either alt managers or big Life companies. After Brookfield acquires AEL, F&G remains the only survivor. Since Brookfield paid a lot for AEL, F&G's value has become higher and more obvious.

Before rumors of the AEL acquisition (June 23), F&G was trading at $20-21. Within the next 10 days (until July 3 when the deal was announced), F&G price shot up to $24-25 and has remained at this level since. Is F&G attractive at this level?

Before answering, I need to provide additional information regarding F&G. The company was acquired on June 1, 2020, by Fidelity National Finance ( FNF ) and had been its full subsidiary until December 2022. At that point, FNF spun off 15% of F&G to the FNF shareholders to expose its subsidiary to outside investors and unlock its value. Section 355 of the Tax Code specifies that starting from June 1, 2025 (after 5 years of ownership), FNF can spin off the rest of F&G to FNF shareholders tax-free.

FNF did similar transactions in the past and they are very profitable for its shareholders. Wealthy FNF insiders own 5.8% of its stock and are highly interested in tax-free transactions. We think F&G's full spin-off in 2025 is very likely. After that, F&G as the only available fixed annuity player will become an acquisition target following AEL's trajectory.

F&G models its operations on Apollo's ( APO ) Athene with Blackstone ( BX ) managing its investments. Blackstone should be interested to retain this management contract and may partner with a bigger insurer to acquire F&G (Blackstone is asset-light and unlikely to become a full owner). If not Blackstone, another alt manager (say, Brookfield or KKR) or a bigger insurer may step in. In any case, F&G is unlikely to remain independent for long after the spin-off.

At the end of 2022, F&G BVPS ex-AOCI was ~$37. By mid-2025, we can expect this number to appreciate ~20% (assuming mid-teen ROE in line with Athene's and deducting ~4% dividend) and reach ~$44. Based on the AEL example, the takeover proposal should come close to this number delivering ~40% annual appreciation plus ~4% dividend.

Conclusion

We are bullish on both BAM and F&G. For BAM, AEL's acquisition is just another longer-term positive without significant immediate consequences. For F&G, AEL's acquisition is a strong immediate positive crystallizing its value.

F&G is a very volatile stock that may revisit lower trading levels due to various reasons. Taking a position in F&G and accumulating more on weaknesses may be the right strategy.

For further details see:

How To Benefit From Brookfield's Acquisition Of American Equity