LZ - How To Navigate The LegalZoom Price Yo-Yo

2023-08-20 11:16:20 ET

Summary

- LegalZoom's Q2 earnings report included increased guidance, but the stock price still plunged, indicating a volatile market sentiment that provides on-going "buy-the-dip" opportunities.

- LegalZoom's free cash flow, stock repurchases, and zero debt are clear positives.

- A new product launch for LZ Book and generative AI initiatives hold future promise but the lack of guidance likely contributed to friction in market sentiment.

- On-going efforts to rightsize LZ Tax may also weigh on investor sentiment.

Over the past several months, LegalZoom (LZ) has changed in price much faster than any changes in the business or its prospects. The latest LegalZoom price yo-yo of volatility was driven by a 2023 Q2 earnings report that actually included increased guidance. The subsequent price plunge surprised me almost as much as the rapid price decline ahead of Q1 earnings . Clearly, there is a constituency perpetually on edge about LZ. Thus, when I review results for LegalZoom I need to contemplate alternative ways to interpret the results.

For the Q2 results I assume that expectations had built up over the company’s various product initiatives, none of which are producing immediate results. I do not expect Q3 results to satisfy this crowd, but Q4 earnings will deliver the big test when LegalZoom presumably will lay out expectations for 2024. In the meantime, let’s take a look at guidance, performance, and the various initiatives positioned to take LegalZoom to the next phase of growth. There is every reason to stay even-keeled through the LegalZoom price yo-yo.

Guidance and Performance

LZ plunged despite a small increase in earnings guidance for the year. The following list compares the latest guidance to the prior guidance from the Q1 earnings conference call .

- Total Revenue: $642M to $652M (4% year-over-year growth at the midpoint) vs $630M to $650M

- Adjusted EBITDA: $105M to $110M (17% of revenue at the midpoint) vs $105M.

For the third quarter, LegalZoom expects total revenue of $159M to $161M (3% year-over-year growth) and adjusted EBIDTA of $26M to $28M (17% of revenue).

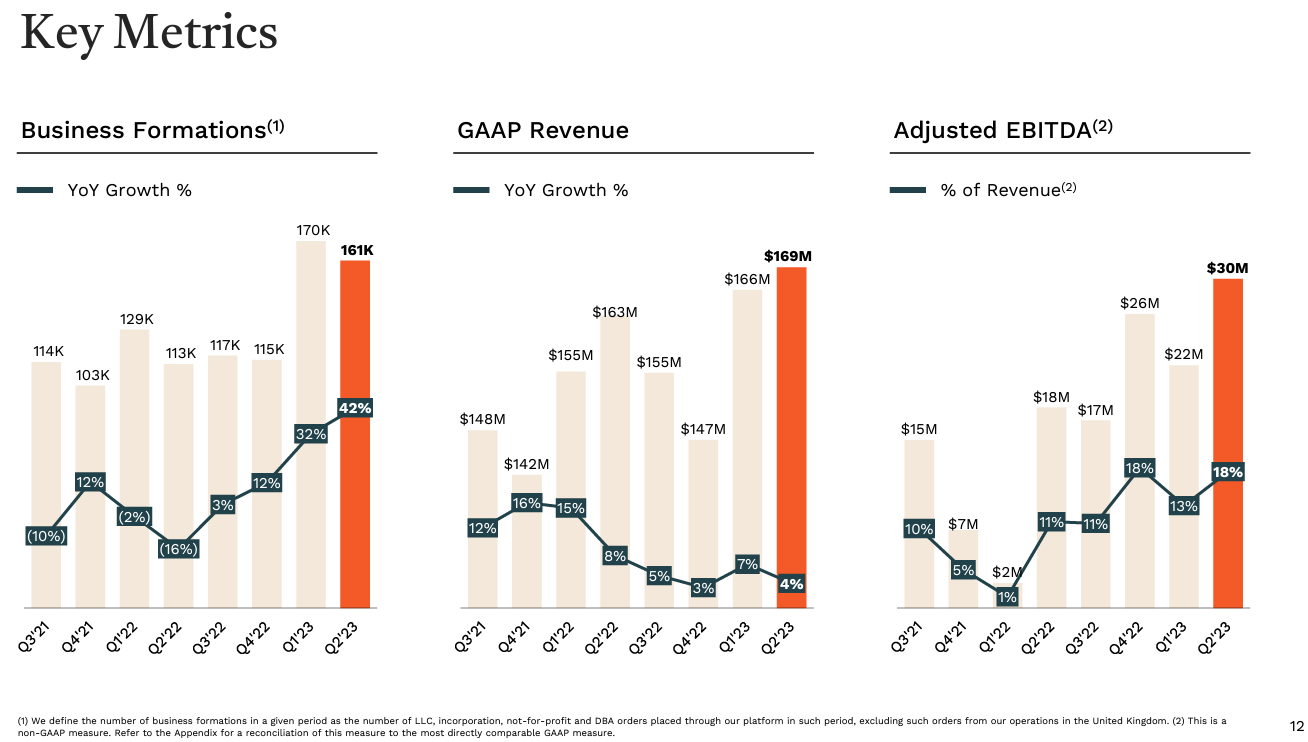

LegalZoom attributed the slight increase in guidance to “macro conditions.” Since guidance went higher, management is implying that these headwinds are slightly better than expected. Management also described census business formations as “healthy” and “steady year-to-date.” Thus, management is showing a slight uptick in confidence in business conditions. The following chart from the earnings presentation gives an overview. Note that strong growth in business formations is not translating into an uptrend in GAAP revenue growth. This growth needs to follow soon to justify a valuation of 3.6x sales and 35x forward (GAAP) earnings .

LegalZoom Key MetricsLZ has bounced up and down like a yo-yo with a triple bottom across November, January, and May. (LegalZoom Earnings Presentation (Q2 2023))

{kind=link}

Management’s commentary suggests potential upside to the guidance if macro conditions continue to surprise to the upside. That prospect alone keeps me bullish on LZ. Management expressed its own incremental increase in its bullishness:

“So we’re overall a bit more bullish, just given the length of the consistency that we’re seeing… We are still leaving some room and embedding some room in terms of caution in our – particularly in our fourth quarter expectation for the macro just as we’ve done year-to-date, just being cautious as we know things can soften and we know there’s still some prognostication around the overall economy slowing. But overall, we’ve taken up our expectation for the macro.”

Free Cash Flow and Stock Repurchases

Free cash flow and the ability to repurchase stock are additional positives in favor of LegalZoom.

LegalZoom increased its non-GAAP cash flow to $37M, 22% of revenue, up significantly from the $6M a year ago. Backing out the purchase of property and equipment, net cash from operating activities was $45M, up from $11M a year ago. (Free cash flow data and GAAP reconciliation come from the earnings presentation).

This free cash flow supported LegalZoom’s stock repurchases. The company was quite opportunistic in its purchases during Q2. The latest 10Q shows the company loaded up on 50,786 shares at an average $8.99 in April (~$457K total spent) and 327,577 shares at an average $7.99 in May (~$2.6M total spent), presumably a large amount of this stock was purchased during the abrupt generative AI panic when LZ dropped as low as $7.11. The company did not buy any shares in June when the stock soared above $11.

LegalZoom’s balance sheet is strengthened by the lack of outstanding debt.

New Product Launch: LZ Book

LegalZoom announced the launch of LZ Books, a platform designed to support solopreneurs and small businesses in their bookkeeping and tax management needs. The new product responds to a market gap for single member LLCs and sole proprietors, who apparently often struggle with complex and expensive accounting software. Management explained that LZ Books aligns with the company’s three strategic pillars: scaling the business, building the ecosystem, and integrating experts. LZ Books not only offers an accessible and lower-priced alternative for bookkeeping but also seamlessly integrates with LZ Tax, the company’s existing tax solution. During the launch of LZ Books, customers will receive free unlimited access to a CPA. Management cited a recent study that concluded roughly two-thirds of LegalZoom’s formation customers are solopreneurs, indicating a significant potential market for LZ Books.

Despite the reported potential, management did not offer any guidance. Instead, they are taking a measured approach: “let’s learn from our customers and then let’s build off of that.” The upshot is that any early success will produce upside to current guidance. Still, the lack of guidance likely disappointed analysts.

Decline in Transaction Average Order Value (AOV)

Management has previously explained the impact of its freemium strategy in the form of declining AOV. In Q2, transaction AOV declined 26% year-over-year. However, Q2 should be the trough of lower year-over-year AOV performance. The year-over-year comps get easier in the second half of the year. This trough should at least be a non-negative for LZ’s stock price.

Transaction revenue was $60 million in Q2, a decline of 7% year-over-year.

On-Going Struggles with the Retention Rate for LZ Tax

While LZ Book should apply positive synergies to LZ Tax, management noted that they “remain constructively dissatisfied with the retention rate of this service.” In response, management is continuing to work on identifying the right customer segment for LZ Tax, what they call a “rightsizing.” This segmentation will create a drag on attach rates as well as generate higher attrition rates from the current customer base. These LZ Tax dynamics will contribute to a slight deceleration in subscription revenue growth for the second half of the year.

Accordingly, LZ Tax will be a “headwind” for revenue going into next year. Since management expects long-term upside, the coming forecast for 2024 will need to explain the path to a turnaround. Until then, this struggle with LZ Tax will likely act as friction on investor sentiment toward LZ.

Management explained the lower attach rate:

“We’re also starting to tamp down attach in a way like we want to get the attach lower because we keep finding that our customers, they know they have a tax question but they aren’t really sure what it is. And so they sign up for the service, and then they may ask that question and then they realize they either don’t have more questions or they don’t have a return to file. And so we see higher attrition. And that churn is something that is expensive for us to support, but it’s also not a great customer experience because they have to go through a cancellation process.”

To rightsize the customer segment, management is testing an annual subscription and removing cross-sells for LZ Tax.

A Reset on Partnerships

LegalZoom is changing its relationship with partners, dropping some that no longer fit their profitability targets or no longer fit the product and service strategy. Management described these less desirable partnerships as “dilutive to economics.” This change is contributing to the deceleration in subscription growth, so an analyst asked for more details.

Management reminded everyone that these changes have been underway for a couple of quarters. Moreover, they remain committed to achieving a 15% share gain and a 15% EBITDA margin despite these partnership changes. Still, I imagine this change can cause friction in sentiment until the upside to these changes become apparent.

Competitive Pressure

Management acknowledged that competitors are dropping prices. This move of course could pressure margins in a generally inflationary environment. (Note management insisted that “we do not believe that inflation has had a material effect on our business, financial condition, results of operations or future prospects.”) Yet, management declared these price drops are positives for small businesses. They even “encourage prices down, especially on the formation side.” Management sees a competitive advantage in its ability to invest in product experience and new products (see the above discussion on free cash flow) where competitors are unable to do so. Its innovation is “funding” LegalZoom’s ability to match pricing.

Accordingly, management insisted that the pricing pressures are “impacting them disproportionately relative to us.” Regardless, pricing pressures are a big yellow flag on investor sentiment, so, here again, investors will need to see direct evidence that these business dynamics are not a drag on margins.

Unfortunately for Q2’s story, gross margins did indeed decrease slightly from 67% a year ago to 65%.

No New News on Generative AI

I earlier surmised that a panic over generative AI caused LZ to plunge ahead of its Q1 earnings. That event turned into a major buying opportunity. After reassuring investors during Q1 earnings, management had nothing new to report during Q2 earnings. That void could be filled by fresh concerns. From the conference call:

“….we talked about this last call, we don’t want to foreshadow product releases before they’re out there. I think the thing I’d say is that we’re making steady progress. We’re trying to do something a little bit different than, I think, most of the alternatives in the market in that – we wanted to serve small businesses directly.”

The vagueness about what LegalZoom might offer essentially left investors with no new news. Again, from the conference call:

“You’re seeing a lot of gen AI products that are built very specifically for attorneys and law firms. And so there’s some things that we need to work through to make that possible. But it will most likely be integrated in a way where you start to think about how people interact with docs, how they interact with their attorneys through documents and how they get insights out of their documents. And so it’s very similar to what I said last quarter, making good progress and you’ll hear some announcements in the next quarter or two.”

In other words, it sounds like generative AI will not threaten LegalZoom’s business model. However, the coming product and service offerings may not be particularly impressive drivers of new growth. Time will soon tell.

Accounting Issues

On March 1, 2023, LegalZoom described a restatement of financials in a 10K . The stock did not react to the news, so the adjustments looked minor even though the company described them as material. However, given the mystery of the poor reaction to earnings, I am including a reference to these accounting issues. There is of course an irony here given LegalZoom seeks to help its customers keep their accounting straight.

From LegalZoom: a “material weakness related to the income tax provision resulted in the restatement of our unaudited condensed consolidated financial statements for the quarters and year-to-date periods ended March 31, 2022, June 30, 2022 and September 30, 2022.”

LegalZoom provided an update in its latest 10Q; the company continues to work on resolving its accounting issues:

- We have hired and are planning to continue to hire additional experienced accounting, financial reporting and internal control personnel and refined our key control roles and responsibilities;

- We provided and are planning to provide additional internal control training programs to all accounting personnel;

- During the three months ended June 30, 2023, we designed and implemented controls to address the identification, accounting for, and review of non-routine, unusual or complex and initial applications of complex accounting standards, including the continued engagement of external consultants to provide support and to assist us in our evaluation of such transactions; and

- We have designed and implemented and continue to design and implement the relevant controls to enable effective and timely review of the income tax provision and certain account analyses and account reconciliations, including the identification of relevant supporting documentation, assessment of the reliability of reports and spreadsheets used, and retention of sufficient detailed evidence of review procedures performed.

LegalZoom indicated it has made progress on these issues but implementation on the remediation is subject to validation and testing. These remediations must also be made in a timely manner.

Given the stock did not react back in February and March, I assume that any further hiccups in accounting issues will be met with similarly small price moves, if any. Still, I am keeping this on the radar in the context of LZ’s overall price volatility.

How to Navigate the Price Yo-Yo

Overall, I do not think nitpicking at the negatives in LegalZoom’s results and story justify the price volatility. I also think LZ will take time to return to pre-earnings levels. So, I consider LZ a buy on the dips with modest expectations for upside.

As I stated in the comments of my last post on LegalZoom, I thought the run-up into earnings got ahead of the story. Accordingly, I managed what I saw as mounting downside risks by taking profits.

The subsequent 20.5% post-earnings plunge looked just as extreme as the pre-earnings run-up. However, I am taking my time to rebuild a position. The overall stock market is in a period that features large downside risks and the current negative sentiment is weighing on high-valuation, high beta stocks like LZ. Thus, navigating this price yo-yo will take some patience. I fully expect to have at least a small position back in place ahead of the next earnings report.

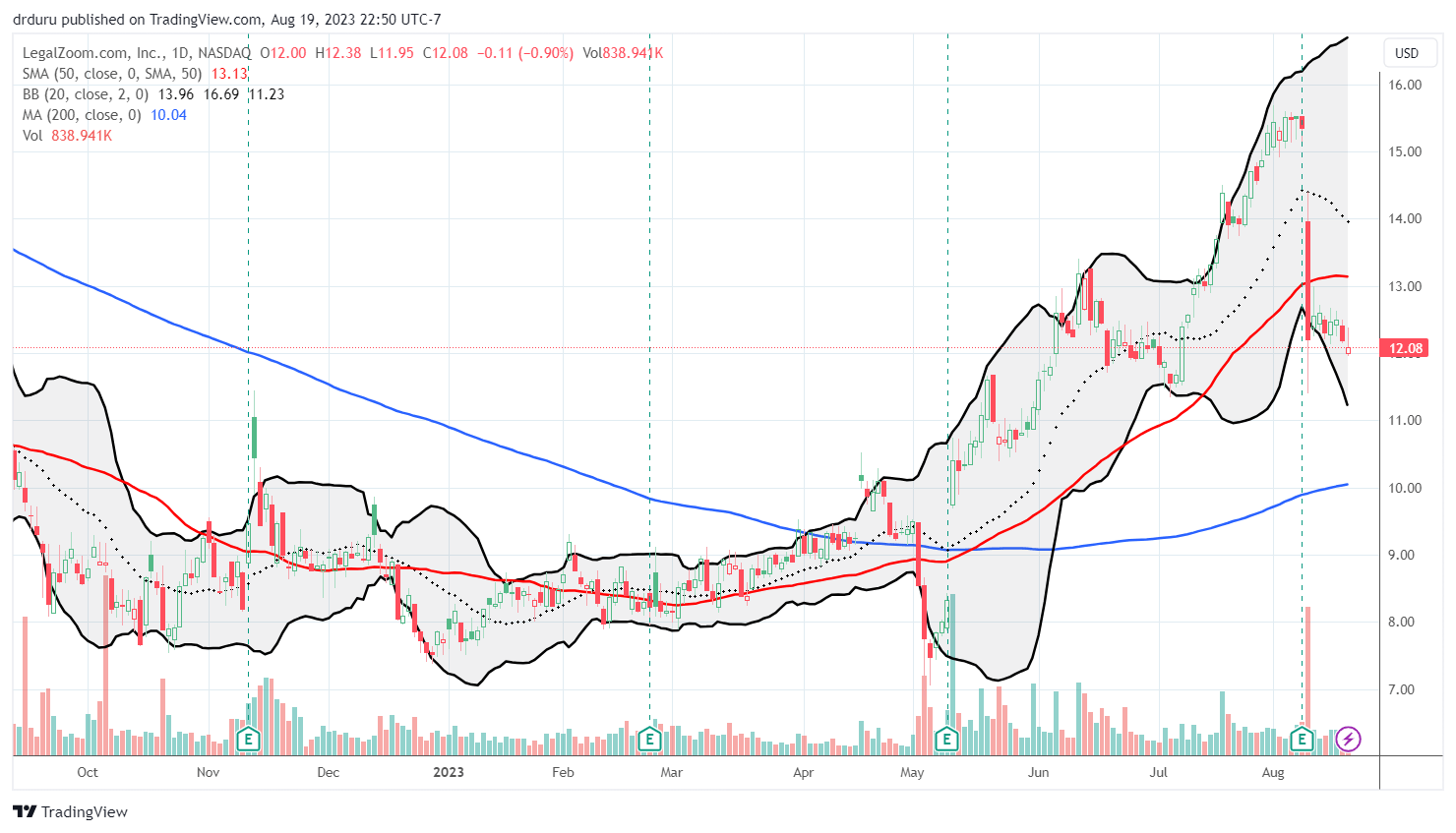

LZ has bounced up and down like a yo-yo with a triple bottom across November, January, and May. (TradingView.com)

{kind=link}

Be careful out there!

For further details see:

How To Navigate The LegalZoom Price Yo-Yo