AZUL - How To Play Azul's 2024 Bonds At A 16% Yield To Maturity

2023-06-20 16:05:26 ET

Summary

- Azul, a Brazilian airline, faced challenges during the pandemic due to the lack of government subsidies and rising oil prices and exchange rates, leading to a cash flow warning in 2022.

- The company has undergone debt restructuring, reducing lease payments and converting debt to equity, benefiting both equity and bondholders.

- Investors can potentially generate a double-digit IRR by creating an arbitrage between the company's bonds and equity, as the latter has reacted more strongly to recent positive news.

Thesis

After issuing a cash flow warning Azul's (AZUL) obligations were downgraded to CAA2 in February. However, its 2024 bonds (USU0551UAA17 Symbol: AZUL4555646 CUSIP: 05502FAA6 ) currently offer a juicy 16% yield to maturity . This is higher than the current 14% effective yield of the CCC & lower index. Implying that they are riskier than the average CCC & lower bonds.

I disagree with this valuation. Since February the chances of these bonds being repaid in a little over a year have increased significantly. Major problems plaguing AZUL, high gas prices and a weak Brazilian real have improved. In addition, AZUL has announced restructuring agreements with its debtors that significantly reduce near-term debt obligations. The equity market has recognized this improvement. While the bonds have rallied also they have not caught up to the equity market.

Debt restructuring

Since issuing the cash flow warning AZUL has worked diligently to restructure its debt. AZUL was an obvious candidate for restructuring as it was a previously successful operator that had been hit by a series of very difficult years. The focus of re-structuring has been to reduce AZUL's short-term obligations.

AZUL has so far announced agreements with its Lessors, OEM partners, and bondholders. This represents an overwhelming majority of their debt.

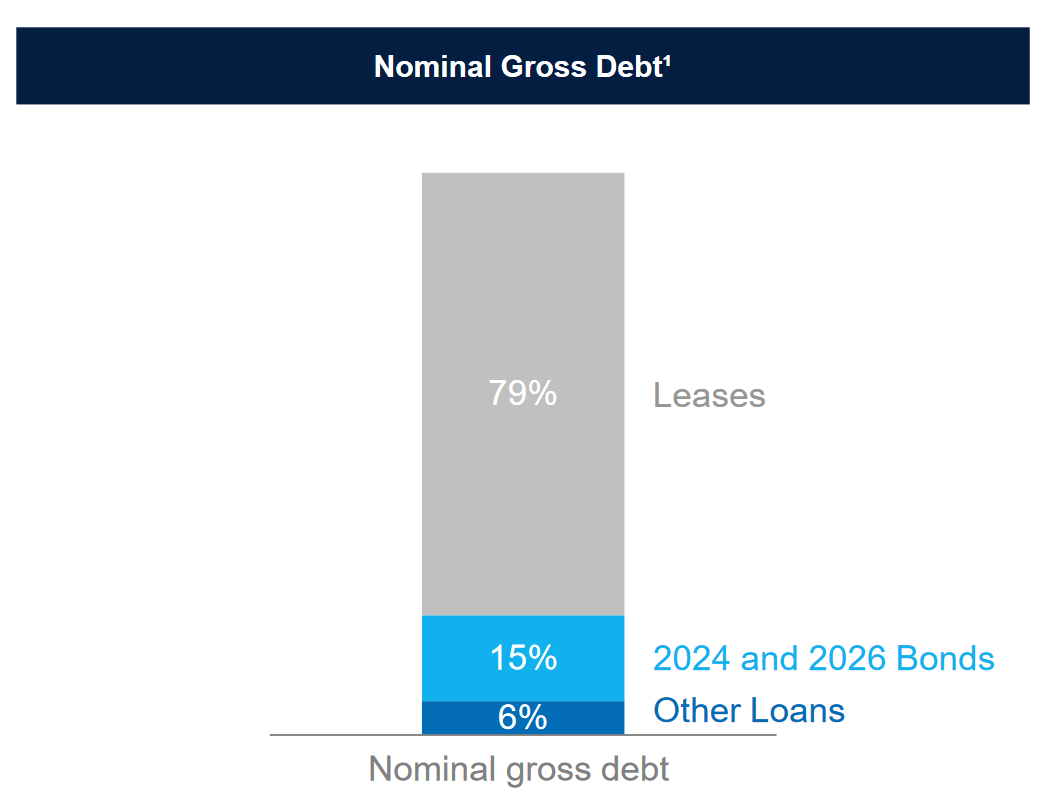

{kind=link}

Majority of debt from aircraft leases pre-restructuring (AZUL investor relations)

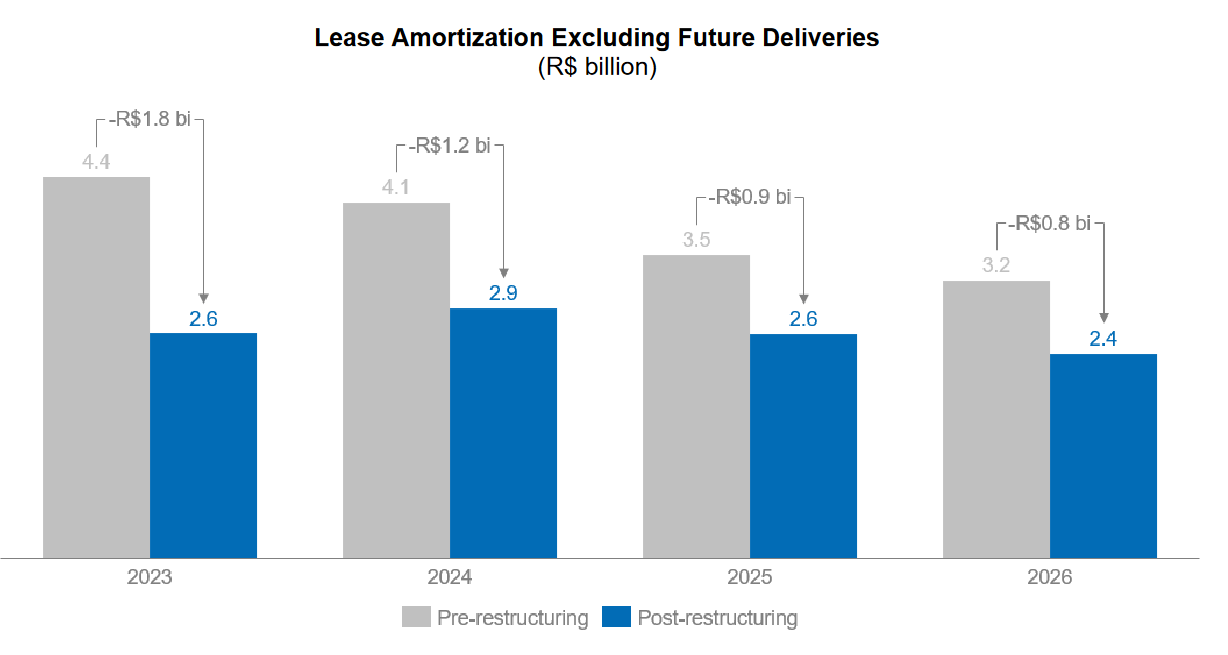

In May Azul announced the restructuring with OEMs and lessors that significantly reduced lease payments by converting future lease payments into longer-dated bonds and an equity instrument.

{kind=link}

Lease payments over the next several years are significantly reduced (AZUL investor relations)

Last week AZUL announced an exchange offer for its 2024 and 2026 notes. The offer pushed out the maturities of the debt in exchange for being secured and higher interest rates.

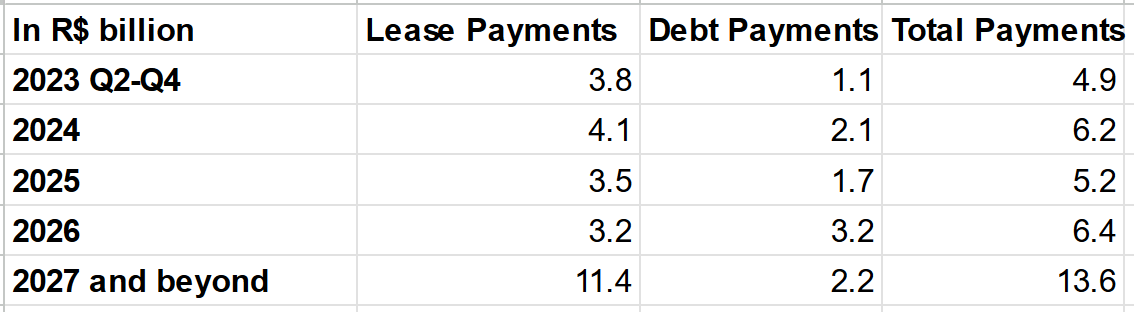

Below I've added a table comparing the required payments of AZUL at the end of Q1 and pro-forma with the restructuring announced so far.

End of Q1 2023

{kind=link}

Author's work

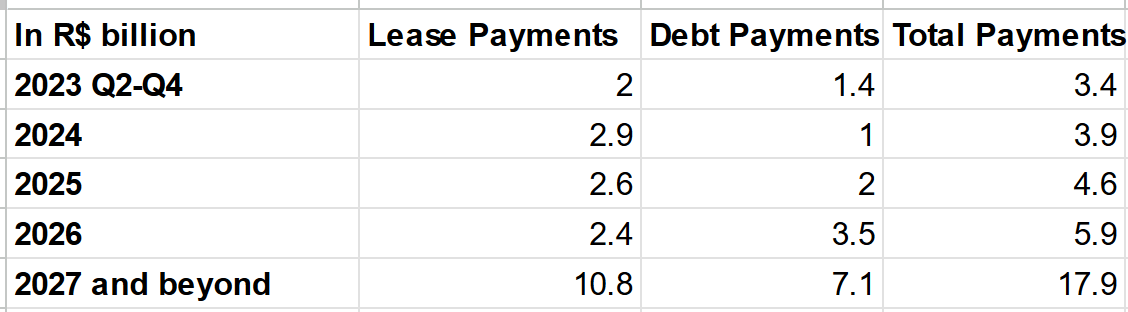

Pro Forma After Announced Restructuring

{kind=link}

Author's work

The key detail is how obligations for the remainder of 2023 and 2024 have been reduced. This will reduce AZUL's current liabilities by ~33%. Making it much easier for AZUL to repay bondholders who choose not to accept the exchange offer.

I present the above pro forma as a capture of the currently announced transactions. The pro forma assumes that only the 65% of 2024 bondholders who have already committed, accept the exchange offer. I'd expect more than this amount to tender in actuality. AZUL is also looking to raise more capital via issuing additional secured debt i n the near term.

Improved operating environment

Although I believe AZUL is a good operator, as far as airlines go, they cannot outrun two critical parts of their cost structure: oil prices and the Brazilian Real/USD exchange rate.

Jet fuel is a huge input cost for any airline and Azul is no different. 2022 saw a rapid spike in oil prices. It is hard for airlines to deal with quick spikes in oil prices as they sell tickets in advance. They must wait for the competitive environment to reflect increased costs before lowering their ticket prices. This year has seen the opposite dynamic so far with oil prices rapidly declining.

The Brazilian real USD exchange ratio is important for AZUL because they collect revenue in Brazilian Real but a significant part of their cost structure is in USD. Jet fuel and airplanes must be paid for in USD. In addition, a significant portion of their debt is USD denominated. So far in 2023, the USD has been consistently weakening against Real.

In 2022 the revenue per available seat kilometer for AZUL was R$40.29 compared to a cost per available seat kilometer of R$36.43. Compare this to 2019 when revenue per available seat kilometer was R$31.90 and cost per available seat mile was R$26.24. Unless we see a huge spike in oil prices through the back half of the year, 2023 will reverse this trend. The unit economics of the Brazilian airline industry should be superior to 2019 if things hold steady helping AZUL's cash flow.

Risk liquidity

While the announced restructuring and improved operations should help with liquidity. My pro forma balance sheet shows a current ratio of .5. So the situation is still quite tight. AZUL needs to be able to roll its working capital debt and positive operating cash flow for the rest of the year. If they are able to raise additional capital as management has promised by issuing more secured debt they should be in good shape to make it past the 2024 debt maturity.

Risk debt is being primed

The new debt that is being offered in the exchange offer is being secured by subsidiaries that don't guarantee the original 2024 debt. This essentially makes the current bond claims subordinate to the assets those subsidiaries control. My thesis is that bankruptcy for AZUL in the next year is highly unlikely. However, if it occurs the 2024 bonds will be in a worse position.

How to play

The simplest way to play is to buy the 2024 bonds with no hedge. After both the announced restructuring transactions it seems likely they are paid out at par in a little over a year netting a healthy 16% YTM.

My favorite way to play though is to buy put options as insurance on the bond. Since the debt is senior to the preferred equity that trades as AZUL I view these put options as insurance. Please note this is a complex strategy that creates a very illiquid position. Both the bonds and AZUL option chain are illiquid so unwinding the trade is challenging.

In the interest of full disclosure and to give you an idea of how I structured the trade here is how I put it on a few weeks ago.

{kind=link}

Author's work

The strategy here is that either the 2024 bonds will be paid in full or the preferred equity will be worth $0 before the options expire. My math above assumes that if the company goes bankrupt the 2024 bonds will be worth 0 and each put contract will be worth $250. However, this is highly unlikely for example receiving one coupon payment and 10 cents on the dollar for my bond in bankruptcy would make me even. I also like this trade since I could end up with a higher IRR either by winning on both sides to some extent or by the bonds being valued at par sooner.

I don't recommend copying my trade exactly. Both the equity and bonds have moved higher since I put it on. In addition, the option chain is illiquid so you need to see where you can find liquidity at a reasonable price. I'd consider hedging the next 6 months to be the most important since that is the time when AZUL could face a liquidity crunch.

Final thoughts

I'd recommend this investment only for investors willing to put the work in on something more advanced. It requires close attention to detail when reading the bond indentures and corporate structure. You'll also need to be patient in finding liquidity in the bond market and the options chain if you choose to hedge. Without the PUT options as insurance, I still like the trade but you may want to wait until after all restructuring is 100% finalized including issuing the new secured debt.

For further details see:

How To Play Azul's 2024 Bonds At A 16% Yield To Maturity