ETO - How To Use CEFs For A Rich Retirement

Summary

- Closed-end funds are great income investments thanks to tax laws and tradition.

- Being required to pay out most of their taxable gains explains a lot about how CEFs act.

- CEFs can be great income investments.

Co-produced with Beyond Saving.

Introduction

When investing, it is essential to ensure you are buying investments that are consistent with your goals.

At HDO, our goal is to produce a high level of current income. You aren't going to find us buying high-growth stocks. Why? They don't pay distributions. Amazon ( AMZN ) might be a fantastic investment, but it does nothing to achieve our stated goals, so no matter how cheap it gets, you won't find it in the HDO Model Portfolio. This says nothing about the quality of the investment. AMZN might achieve goals and be a great investment for many investors.

A few things determine whether or not a company pays a distribution. One of the most significant factors is the corporate structure. When companies file their taxes, they have a choice of what structure they want to file as. These options come with different qualification requirements and have different tax consequences for the company and investors.

As investors who follow an "income" strategy, we frequently find investments that are Regulated Investment Companies, or RICs, on our radar. The reason is that RICs don't pay taxes at the corporate level, and in exchange for that exemption, they are required to pay out most of their taxable income as distributions. The concept is known as "pass-through" or "conduit" investments, the company passes along all taxes to investors. The distribution requirements ensure that the company cannot be used indefinitely as a tax shield, Uncle Sam wants his cut!

As a result, RICs typically pay substantially higher distributions than companies with corporate structures that don't have similar requirements. Various types of investments fall under the RIC umbrella, including business development companies ("BDCs"), closed-end funds ("CEFs"), real estate investment trusts ("REITs"), and mutual funds. While the details vary, all of these investments fall under the Investment Company Act of 1940, have various asset requirements and limitations, and have distribution requirements.

Today, we are going to zoom in on closed-end funds, or CEFs. As RICs, CEFs are fantastic distribution investments, often providing exposure to investments that have low yields in a vehicle that pays a high yield. This class of investments can provide great benefits for income investors, but it is crucial that we have realistic expectations and understand the role CEFs play in our income portfolio.

The "Closed" In CEF

What differentiates CEFs from "open" funds like mutual funds or exchange-traded funds ("ETFs") is that the share count is fixed. When you buy or sell shares in a mutual fund, you are buying or selling from the manager. ETFs similarly are set up so that new shares are created whenever shares are bought, and assets are liquidated when shares are sold. As a result, the price you buy or sell at will be very close to NAV (net asset value).

CEFs issue shares and use the capital raised to invest in assets. The shares then trade on the secondary market. When you buy a share in a CEF, you are buying from another investor. The fund itself doesn't sell any assets or receive any new capital. If the fund wants to expand, it will have to do a secondary offering and create new shares.

This means that CEF prices can trade at a substantial premium or discount to NAV. The price a CEF trades at is much more reliant on investor demand for shares. NAV only influences share price to the extent that it impacts individual investors' decisions to buy or sell. Since NAV is readily available, many CEF investors do consider NAV and the premium/discount to NAV when buying. So, we often see a strong correlation between NAV and price.

Is NAV Important?

Investors love to have ironclad rules, like "never buy a CEF at a premium to NAV." Yet, CEFs that trade at a premium frequently outperform those that trade at a discount! So, another investor might have the rule "never buy a CEF at a discount to NAV." Which is right? Neither.

If investing was so easy as sticking to bumper sticker rules, you could buy a fund that followed the rules and walk away. Some of the best-performing funds of all time consistently have high premiums. A large discount to NAV could be a great deal or indicate trouble you want to avoid. As investors, we need to be able to assess and to determine if a premium is worth paying or if a discount is the deal it appears to be.

When faced with a premium or discount on a CEF, here are some of the things you want to consider:

- Is NAV even accurate? Some assets are more liquid than others and have a more readily identifiable value. It is important to understand what kind of assets a CEF holds to determine how much weight you should give to NAV. Many CEFs own publicly traded stocks, which have readily obtainable prices, so NAV accurately reflects what the fund could liquidate for. At the other extreme, some CEFs invest in CLOs (collateralized loan obligations), untraded loans, or even real estate. The fund must estimate assets not publicly traded because CEFs are required to report NAV. However, investors shouldn't put too much weight on these estimates. The value of the assets could be materially higher or lower than reported.

- Can you recreate the portfolio? Some portfolios can be easily recreated. A CEF like BlackRock Energy and Resources Trust ( BGR ) has over 2/3rds of its investment in its top 10 companies. So, we could easily recreate a very similar portfolio. For this reason, we would never pay a premium for BGR, but we are happy to buy at a discount. When you look at the holdings of PIMCO funds, you will find complexities that wouldn't be easy to duplicate even if you were a billionaire. Yes, many of the bonds are easily accessible, but the hedging, swaps, repurchase agreements, and scale that PIMCO employs are not. If you tried, the odds are your results would be materially inferior to PIMCO's results.

- Does the manager add or detract value? Speaking of PIMCO, some managers simply add value to funds. Often the market is willing to pay a premium for a fund managed by a proven high-quality manager, even if there are competitors with very similar portfolios. On the other hand, some managers have tarnished reputations, and their funds will trade at a chronic discount. It is often difficult to quantify exactly how much value a manager adds, but you can look at past performance and also look at the historical discount/premium to NAV that the fund has traded at. It is frequently much more meaningful to compare a fund to its own history, rather than comparing the current discount/premium to other funds.

So, should you pay a premium to NAV? It depends. If it is a portfolio that is easily replicated and the manager isn't adding anything special, then you probably want to be cautious about paying premiums.

We issued a sell-alert on Eaton Vance Tax-Advantaged Global Dividend Opportunitie s ( ETO ) when the premium to NAV spiked up to unsustainable levels for no good reason.

We were content holding when the premium was around 5%. While the portfolio is fairly easy to recreate since it only holds mega-cap publicly traded stocks, Eaton Vance has proven to be a good manager over time, and ETO can access much cheaper leverage than we can. So, a modest premium was ok. A premium of 15%? That made it time to exit.

When we look at PIMCO Corporate & Income Opportunities ( PTY ), it has a portfolio that we wouldn't even attempt to recreate, the manager is excellent, and historically it has traded at a double-digit premium to NAV more often than not. The times when PTY has dipped below NAV have been rare and brief.

So while ETO is expensive at a 15% premium, PTY is cheap at the same 15% premium.

Within CEF investing, there is a strong following of a concept referred to as a reversion to mean. This means there is a very strong force that will pull a CEF back to its historically normal premium or discount. When a CEF strays strongly from this norm in either direction, it whips back again like a stretched elastic being released. Investors are benefitted by looking at these historical norms as well when evaluating if a premium or discount is abnormal.

Should You Worry About Price?

First and foremost, CEFs are income investments. Over the long haul, nearly all your total return from CEFs will come as distributions. We've discussed ETO and PTY in this article. Let's look at their long-term performance:

Note their total return relative to the S&P 500 since 2004. Yet notice the two lines at the bottom of the chart representing the share price change. In 18 years, PTY is down 19% in price, and ETO is only up 7%. In other words, the price change has been truly negligible in relation to the total return.

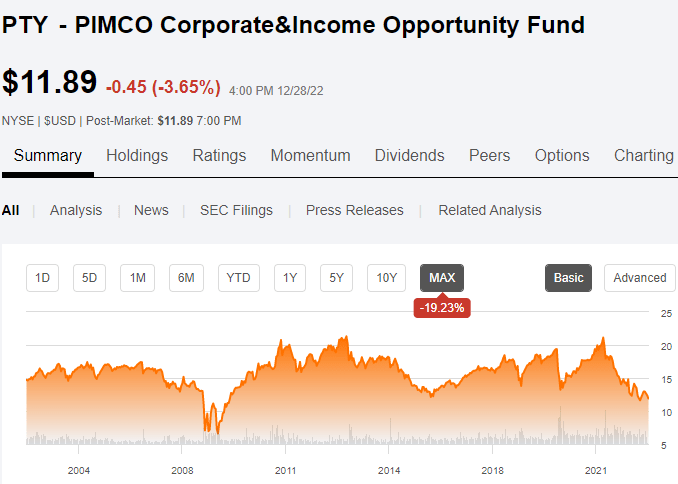

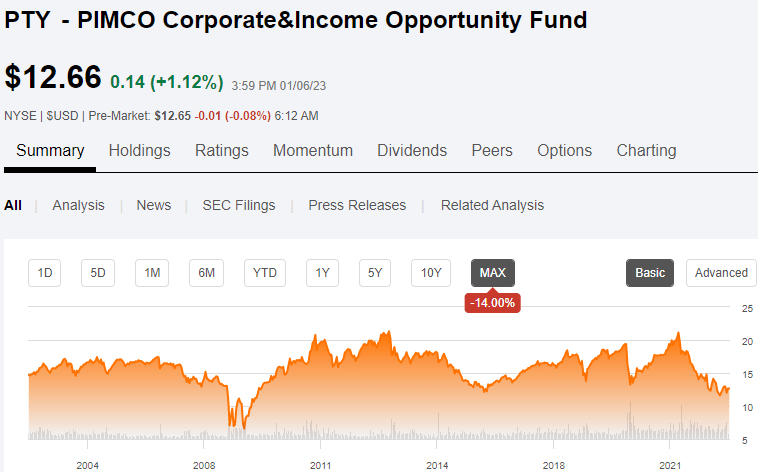

Many investors will look at the price charts of CEFs and immediately dismiss them. They don't look exciting. Here is a look at PTY's chart on Seeking Alpha:

{kind=link}

{kind=link}

It is going nowhere. Why is this so different than what YCharts shows? Because this chart only shows price and does not reflect the substantial value in distributions that investors have collected over the years.

In the short term, the swings in price might feel significant, but over the years your returns from CEFs will primarily be in distributions. Obviously, you want to buy at lower prices. The lower price you buy, the more shares you can buy and the more income you will collect over the years. But income investing is very forgiving. In the grand scheme, if you are following the Income Method and regularly reinvesting excess distributions into the dips, your income will grow and the price you paid will become increasingly irrelevant.

Should You Worry About Distribution Cuts?

It is very difficult for CEFs to have a stable distribution. It isn't particularly worrisome. A distribution cut from a CEF is much less concerning than a distribution cut from a company. This might seem odd for an investment we just described as primarily an income investment, but it is because CEFs are income investments, they will tend to have some variability in their distributions. Why? CEFs are required to pay out substantially all taxable income.

Taxable income isn't going to be the same every year. It just isn't. CEFs are not operating businesses. A business cuts its distribution, and that sets off alarm bells because it raises concerns that something is going wrong in the business and raises questions of future profitability.

CEFs are different. They don't build infrastructure, they don't "grow," and they aren't attracting or losing customers. A CEF takes its capital, invests it in a particular strategy, and then passes along the results to shareholders.

The CEF can't withhold the results. To some extent, management might have the power to delay recognizing capital gains, to do some "tax loss" selling, and try to control the amount of taxable income in a particular year, but ultimately, you can only delay owing Uncle Sam. You can't prevent it.

Anyone who has been investing for more than a few years knows that from year to year, your investment results will vary wildly. If you are averaging 9% per year, you can't reasonably expect to have precisely a 9% return every year. One year you will be up 12%, and the next down 5%, then your portfolio might rebound up 20% in the third year.

I don't care what sector you are investing in or whether you are investing in stocks, bonds, crypto, or baseball cards - your annual returns will not be consistent.

A CEF manager faces two challenges:

- Investors in CEFs want income. Even if the fund has no taxable income, CEF investors expect a distribution. A CEF with no distribution would have no investors.

- In some years, taxable income will be much higher than average. The fund is required to pay it out even if it exceeds the amount that makes investors happy.

So in the negative years, a CEF needs to pay a distribution even though it has no taxable income and no obligation to pay a distribution at all. Otherwise, the manager isn't likely to find investors for future funds. Then during the boom years, the fund needs to pay out even more.

Different CEFs handle these issues differently.

Variable Distributions

Some CEFs just cut straight to the heart - they pay a variable distribution. For example, Tekla Healthcare Investors ( HQH ) pays 2% of NAV per quarter. Investors know upfront that the distribution is variable, and since it is pegged to NAV, HQH will payout more when it has higher capital gains and less when prices fall.

This strategy is great for maintaining the long-term health of the CEF, as its payout will automatically adjust ensuring that the fund is never paying out too much and providing confidence for investors that they will get more as soon as the portfolio rebounds. However, many investors do not appreciate the constant variation in income.

Base + Special Distribution

Perhaps the most common strategy for CEFs is to have a flat regular distribution that is set at a conservative amount and then payout a special distribution in those years where capital gains exceed the distribution.

One well-known fund following this process is Adams Diversified Equity Fund ( ADX ) which pays tiny quarterly dividends and a large year-end one to meet RIC requirements.

This strategy can work great when volatility is relatively low. The fund will occasionally "overpay," but if the distribution is set at an amount that is easily achieved more often than not, it can remain stable for many years. Investors get the occasional special distribution when taxable income is high.

When the stock market gets volatile, this strategy can become problematic as the manager might be faced with the decision to cut the distribution significantly or sell off assets at bad prices to fund the distribution, permanently impairing NAV. Neither choice is appealing, but it is typically better for shareholders if the distribution is reduced, allowing the CEF to continue holding the assets to sell in the future when prices are higher. Remember, CEFs are required to pay out capital gains to shareholders, so if you are a long-term investor, accepting a cut today will often result in higher total returns and higher distributions in the future.

CEFs are a zero-sum game. Every dollar they distribute comes from NAV, and every gain realized or unrealized goes into NAV. Any gains in NAV will be paid out as dividends eventually. Whenever they are realized, they become taxable income.

Return of Capital

Return of Capital, or ROC, is something that many investors misinterpret. Many automatically interpret ROC as the fund returning their capital to them. This does happen, and there are CEFs that overpay and drain capital. But it is important to recognize that ROC is a tax classification and one that is favorable to investors.

Remember, CEFs are required to distribute all of their taxable income, and the shareholders are the ones who pay taxes on it. The taxes you owe on distributions from CEFs will have the same tax character as if the CEF were paying the taxes. It could be ordinary income, interest income, Qualified dividends, long-term capital gains, short-term capital gains, or ROC. ROC means that you don't pay any taxes on it, instead, it reduces your cost basis, and when you sell the shares, you will pay capital gains on your reduced cost basis. ROC essentially defers your tax obligation until you sell.

CEFs can have ROC stemming from ROC distributions the CEF receives from the investments it owns. A distribution will also be ROC if it exceeds the taxable income the CEF reported for the year. As noted above, CEFs will pay distributions even in years when total returns are negative.

How do you know whether you should worry about ROC? In the short term, you can only look at the annual report and determine what the CEF is doing. You can look at the assets and estimate a reasonable expectation of future returns. Make sure you are looking at the yield on NAV, not the market price. If the distribution is lower than that expectation, then I wouldn't worry about ROC.

In the long-term, it is usually very easy to spot which CEFs were overdistributing. Consider Cornerstone Strategic Value Fund ( CLM ). Many investors ask me about it because it is yielding 22% on NAV. CLM has very clearly been overpaying for years, raising new capital and using that to pay distributions. Since its IPO, its NAV is down a staggering 94%.

Over the past decade, CLM's NAV has been on a chronic march down.

When looking at NAV movements, you should consider the asset class. Sometimes, a CEF might have a 30%+ decline in NAV without selling a thing because prices have fallen in the sector it invests in. CLM counts Apple ( AAPL ), Microsoft ( MSFT ), and Alphabet ( GOOG ) among its top holdings - stocks that outperformed during the past ten years. If these were stocks that had declined in price over the past decade, maybe there would be an argument that going forward, returns will be high enough to justify the dividend.

Clearly, CLM is dramatically overpaying its dividend.

Compare CLM to PTY. Note how PTY's NAV has varied over the decades. It has experienced some deep dips and is in one right now. However, it has trended back to its IPO NAV several times, including last year.

By looking at the performance of NAV over the long run, you can tell if the company has overdistributed in the past. All CEFs will see NAV vary, but NAV should tend to be flattish over longer periods.

Note that a CEF overpaying is not something that is necessarily a dealbreaker. Sometimes, gaining extra cash flow upfront might fit your goals better. Even though CLM has had a 93% decline in NAV, its total return over the same period is +219%.

Leverage

Many CEFs utilize leverage, allowing them to pay out higher dividends. Leverage amplifies returns, both upside, and downside. Since the stock market goes up more frequently than it goes down, leveraged CEFs will outperform unleveraged peers more often than not. Of course, in down years, leveraged CEFs will have additional downside and in sustained downdrafts, might be at elevated risk of needing to reduce their dividend.

As long-term income investors, we tend to be comfortable holding through downswings. We're content to collect income with the knowledge that total returns from leveraged CEFs will tend to be higher in the long run than unleveraged CEFs.

It is important to recognize that CEF prices tend to be more volatile than their own NAVs. When investors are bearish on a sector, the CEFs that focus on that sector will tend to sell off more strongly. When investors are bullish, they tend to run up more quickly. This volatility is increased when leverage is added.

Consider Cohen & Steers Total Return Realty ( RFI ) and Cohen & Steers Quality Income Realty ( RQI ). The two funds have the same manager, and both invest in REITs. There is a substantial overlap in the holdings between the two. The main difference is that RFI does not utilize leverage, while RQI does.

RQI has outperformed over the past decade. However, it has had significantly more volatility. RQI has had a beta of 1.12 compared to RFI's beta of 0.96 over the past decade.

When considering an investment in CEFs, investors should keep in mind the potential for price volatility and an understanding that most of their returns will be dividends.

{kind=link}

Conclusion

For HDO, CEFs provide several attractive properties.

- They pay a high yield.

- They provide quick diversification.

- They can provide an income investor-friendly vehicle to invest in sectors that don't pay dividends.

However, based on the questions and comments we have received, some investors have unrealistic expectations for CEFs. CEFs are not going to see their NAV climb up significantly over sustained periods for a simple reason: capital gains have to be distributed to shareholders.

A CEF with a NAV climbing significantly higher than its IPO NAV will be forced to increase its distribution or pay out a special. Some CEFs might be able to avoid realizing gains for a period, but eventually, those gains will be realized, and the cash will be heading into shareholders' pockets. This requirement is why CEFs are such great income investments. It also means that over long periods, you should expect NAV (and price) to be somewhat flat. This does not mean your total return will be flat. Thanks to the distributions you are collecting, your total return will climb with every payment.

When you invest in a CEF, your expectation should be that the vast majority of your return will come as dividends. In 5, 10, or 20+ years, dividends will make up an increasingly large portion of your total return. While the volatility of CEF prices might lead some to try trading in and out, at HDO, our goal is income.

We can use CEFs to gain exposure to sectors not represented in our portfolio or to double down on sectors we are bullish on. We can collect our income and use it to live on or to reinvest as it suits our needs.

For further details see:

How To Use CEFs For A Rich Retirement